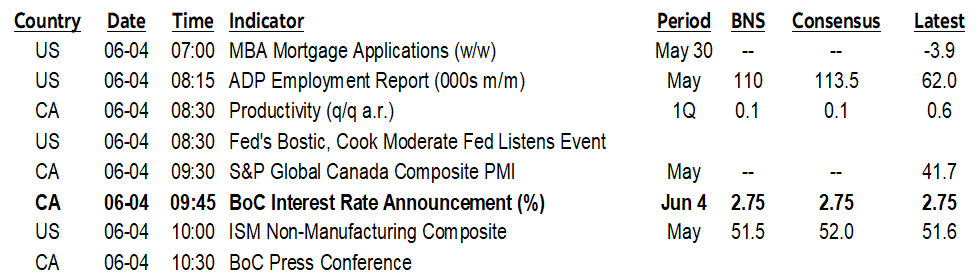

ON DECK FOR WEDNESDAY, JUNE 4

KEY POINTS:

- Mildly constructive global market tone faces key N.A. developments

- BoC is likeliest to hold today

- Why Canada’s SEPH payrolls data is unreliable

- How Musk’s impure motives could be influential

- US steel and aluminum cos are sticking it to their customers

- Canada doesn’t need to retaliate. The US is doing enough damage to itself!

- US vehicle sales fell as tariff front-running faces a pothole

- Canadian vehicle sales also slipped absent any tariff front-running effects…

- …because Canada arguably doesn’t need American vehicles

The tone across global asset classes is mildly constructive so far this morning ahead of key developments in North America. Equities are slightly higher across N.A. futures and European cash markets. Sovereign bond yields are largely just treading water with one mild exception being underperformance of South Korea’s curve after election results. The dollar is little changed on balance again with the exception of a stronger won. We’ll see how it all unfolds after the BoC, some US data and the aftermath of more foolish US tariffs amid the ongoing budget spat that is continuing to divide the GOP. It also seems like US negotiations with China are failing after Trump’s remark that China is “extremely hard to make a deal with.” That’s because the US administration totally miscalculated how China would behave when threatened. Ditto for the EU. Ditto for Canada.

BOC LIKELIEST TO HOLD

The Bank of Canada will be the main focus today at least for me and for many of you. The statement and Governor Macklem’s opening remarks to his press conference arrive at 9:45amET. The press conference begins at 10:30amET and you can watch it at CPAC.CA with your chosen English or French translations on the fly. You could also watch it on the BoC’s website here. Bloomberg subscribers have another option to watch at live <go>. My recommendation is always to run multiple feeds because a/v hook ups often have glitches at this event for some reason.

A hold is priced with just around 5bps of a cut baked in. You could argue that risk-reward favours positioning for a cut. You could also argue that doing so would be largely on a lark and if you want to bet such money, then do it with your own funds. You pick. The BoC has a tendency and willingness to surprise, but I’d have serious problems with this central bank if they went ahead with a cut absent any evidence they’ve licked inflation to date and with forward-looking uncertainties surrounding the outlook for inflation risk.

Consensus expects a hold. All of the ‘big six’ domestic banks now expect a hold with the other five very recently joining Scotia’s call that has been in place for this meeting all year long. A lot of the expectations from foreign players in consensus surveys are stamped out of date. Please see my weekly for supporting arguments. This is a statement-only affair with published remarks from the Governor and accompanying Q&A in the press conference. The next MPR is due at the July 30th meeting.

I won’t repeat the arguments here and instead refer readers at this late stage of the game to my weekly (here). There is, however, one added argument worth exploring next.

CANADA’S PAYROLLS SURVEY IS ALSO UNRELIABLE

Last week through this week has brought forward several clients that have been asking about Canada's SEPH payrolls measure. Specifically, they point to how the Labour Force Survey may have its issues like the wild SA factors that I wrote about in my weekly, but SEPH is also flagging job losses this year. The thesis goes that SEPH is hard payrolls data and so we can’t ignore the signals being sent by that measure and the BoC should be alarmed. Here are several points on why I disagree with that thesis with much of the emphasis upon how SEPH’s Achilles Heel is the massive revisions.

1. SEPH lags by 2+ months to LFS. It’s too stale, unlike the US that releases both the household and payrolls surveys simultaneously.

2. SEPH only captures nonfarm payrolls. It excludes not only ag, but also many small businesses including the self-employed that are important in Canada and that are up about 40k jobs ytd.

3. SEPH also excludes ‘off the books’ employment which can be sizeable in Canada (think taxes, benefits rules etc). LFS is self-disclosed and doesn’t face the same issue.

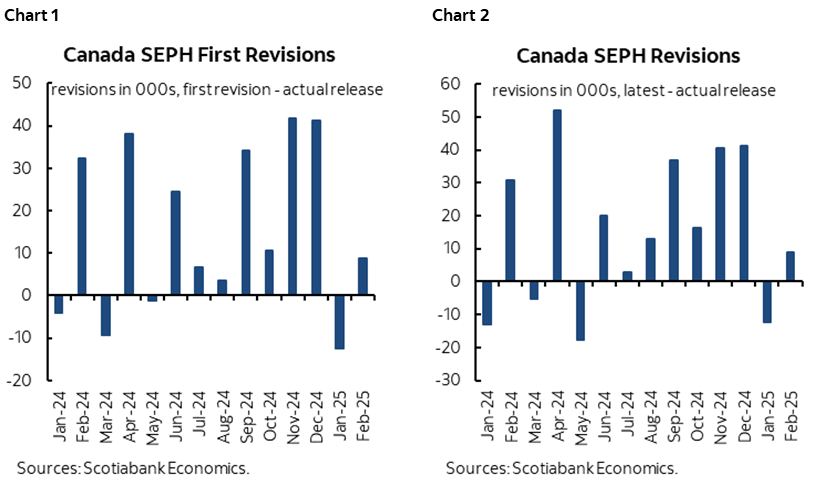

4. SEPH is revised monthly, LFS annually, and SEPH monthly revisions can be huge. They are very often in the tens of thousands of jobs per month. Chart 1 shows the revision to the prior month as each new month comes out. Chart 2 shows cumulative revisions to SEPH by taking the current understanding of each month’s change minus the initial reading. LFS, by contrast, revises only annually with fresh population counts.

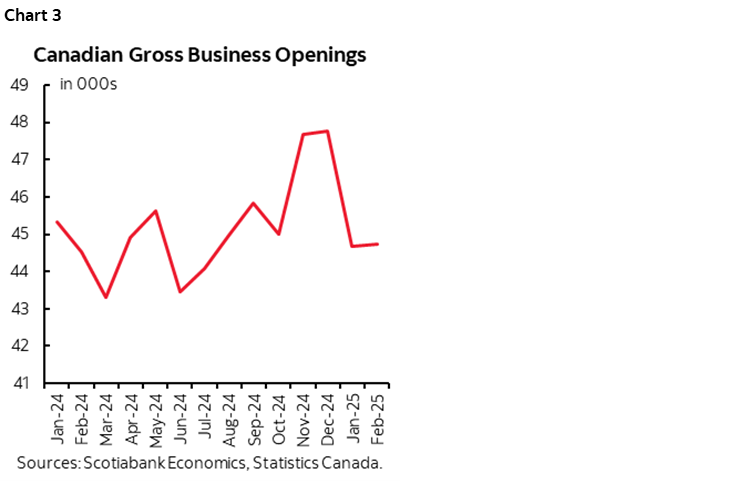

5. Why does SEPH have such large revisions to monthly jobs estimates? Partly because SEPH incorporates business openings with a lag as data becomes available (chart 3). This drives the undercounting of jobs in the short-term, as Statcan acknowledges, and which may be why significant revisions are more likely to be up than down. SEPH is therefore often falsely portrayed as hard data when it’s not.

6. Statcan offers a series for LFS adjusted to SEPH measurement concepts. Adjusted LFS is persistently tracking higher than SEPH using the same concepts (chart 4).

7. Over time, however, LFS and SEPH generally follow each other after all the revisions are accounting for, but there can be significant differences.

8. Also note that SEPH offers no picture of the labour force and unemployment which is critically important and features only in LFS. The UR outlook won't be captured in SEPH figures but faces risks to job growth but also labour force growth as immigration rules are tightened. To look at one without the other is like eating the cake and tossing the icing. Who does that anyway??!

In summation, both LFS and SEPH have issues which is why the BoC looks at all labour force readings from those and other sources. At present, I wouldn't say there is a lot of slack in Canada's job market. One approach is to look at the official UR of 6.9% compared to estimates of the equilibrium or NAIRU rate of unemployment. The OECD's estimate of the latter is 6.2%.

Regardless, the BoC’s issue is with inflation risk and the job market offers a tenuous connection to inflation risk a) in the short-term, and b) even over time through a Phillips curve.

US DATA RELEASES COULD MUDDY THE WATERS

Data may also figure into markets with most of the emphasis upon US ISM-services (10amET) that arrives at around the similar time to the BoC’s communications. That could easily dirty the pool water in terms of market effects.

ADP private payrolls will also be updated with figures for May (8:15amET). My guess is no different from consensus this time (114k consensus, Scotia 110k). Who cares, ADP throws too many head fakes to matter as a guide to Friday’s private nonfarm payrolls.

US STEEL AND ALUMINUM TARIFFS

Talk about masochistic economic policy. Late yesterday, Trump enacted his threat to double tariffs on steel and aluminum imports to 50% effective today (here). Fool. The US steel lobby including its Canadian offshoots with a large presence in the US obviously represent vested interests in support of protectionism from foreign competition that fattens their margins. The problem lies in the fact that this industry’s dance with the protectionist US administration is stiffing everyone else including other industries that are intensive users of steel and aluminum, as well as end consumers. The ripple effects through supply chains will be highly disruptive, damaging growth, unemployment and inflation in the US. The longer-term effects motivate substitution away from US producers by global customers. Further, the lessened competitive zeal could well make US metals firms less competitive behind a protectionist wall over time. The rise in input costs will be passed through multiple products, damaging demand for things like vehicles. This is just bad policy all around.

The US is using Section 232 to impose these tariffs. See my weekly for an explanation of why these tariffs are more immune to legal challenges than the IEEPA tariffs that are bogged down in the courts.

The average effective tariff rate on US imports increases by 1.2% with this move to 12% on all goods and services (14.6% on just goods). Chart 5. That’s a severe terms of trade hit to the US economy compared to around a 2% effective rate on all imports before all of this nonsense began. The average effective tariff rate on total Canadian exports increased by 1% to 4.8% (5.7% for US-bound exports) and on Mexican exports by 0.5% to 4.8% (5.9% for US-bound exports).

So, will Canada retaliate? There are two perspectives on this issue. One is that Canada arguably no longer needs to be retaliating. The US is imposing enough damage on itself as it fights all of its major trading partners. Second is that PM Carney has indicated a preference toward being “engaged in intensive and live negotiations to have these and other tariffs removed as part of a new economic and security partnership with the United States.” Hopefully that doesn’t include some ‘Golden Dome’ fiasco at the expense of Canadian taxpayers. Ontario Premier Ford’s comments also indicate that he is hopeful Canada is ‘very close’ to an agreement with the US.

WHY MUSK’S BUDGET RANT MAY MATTER

The US budget spat continues. Just days after Trump and Musk exchanged vows in the Oval Office, Musk’s ongoing feud with Treasury Secretary Bessent was likely among the motivators behind the fact that Musk pulled no punches, describing the House bill as “a disgusting abomination,” and a “massive, outrageous, pork-filled spending bill” while declaring “Shame on those who voted for it: you know you did wrong. You know it.” I wonder what he really thinks! Not that I disagree with the broad assessment of profligate US fiscal policy, but Musk’s motives are rather impure. Having said that, he may be influential if he starts throwing money around in midterms once more and supports candidates against GOP senators and representatives who were strongly in support of the bill. Regardless, it was only a matter of time before this crew all started to turn on each other.

US VEHICLE SALES DROP

US vehicle sales fell to 15.65 million SAAR last month (17.27 prior, 16.0 consensus, 15.8 Scotia). Chart 6.

The thrill is gone as auto sales, while still decent, have returned toward January levels in the US and hence before the rush to beat tariffs. A large pothole lies ahead including substitution effects toward raising used vehicle prices in CPI/PCE.

The drop in auto sales volumes will shave about 1% m/m off May's retail sales reading. A partial offset may be auto prices. Another uncertainty is whether folks substitute toward spending more on other things and away from vehicles during the month. Income figures have been robust of late.

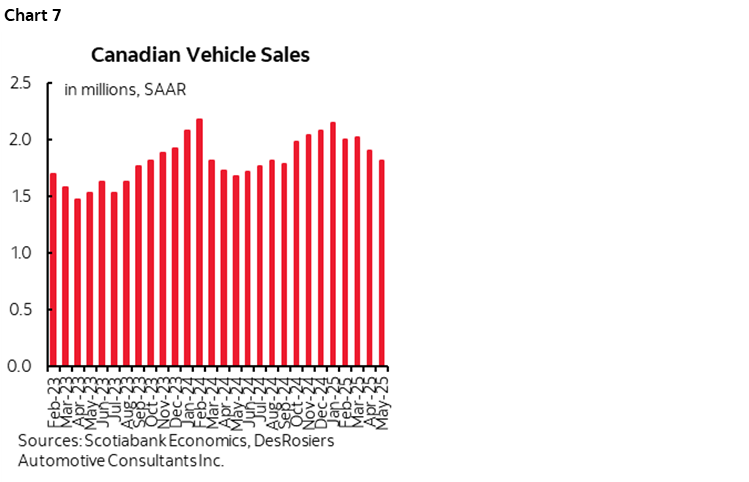

CANADIAN AUTO SALES

Canadian auto sales fell again last month (chart 7). They were down by about -4.7% m/m SA (here). They peaked in January and fell in each of April and May which indicate that there was no tariff front-running immediately around the April vehicle tariffs.

One reason for that could be that—unlike the US—the Canadian auto tariffs have not been broadly applied. They've only been applied in retaliatory fashion and so there is scope for substitution toward made in Canada vehicles and toward European and Asian imports.

Put plainly, there was no need to front-run auto tariffs in Canada given alternative choices. One could therefore quip back at Trump that Canada doesn’t need American vehicles.

So I'm sure some will point to weak auto and home sales in Canada and say cut. One counter to this is that you need confidence and reduced uncertainty to take on a four-, five- or six-figure liability to do so. Otherwise, rate cuts face the problem of 'pushing on a string.' Kind of like in China where rate cuts haven't done much to property markets. Then there are all of the other arguments in my weekly.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.