FORECAST UPDATES

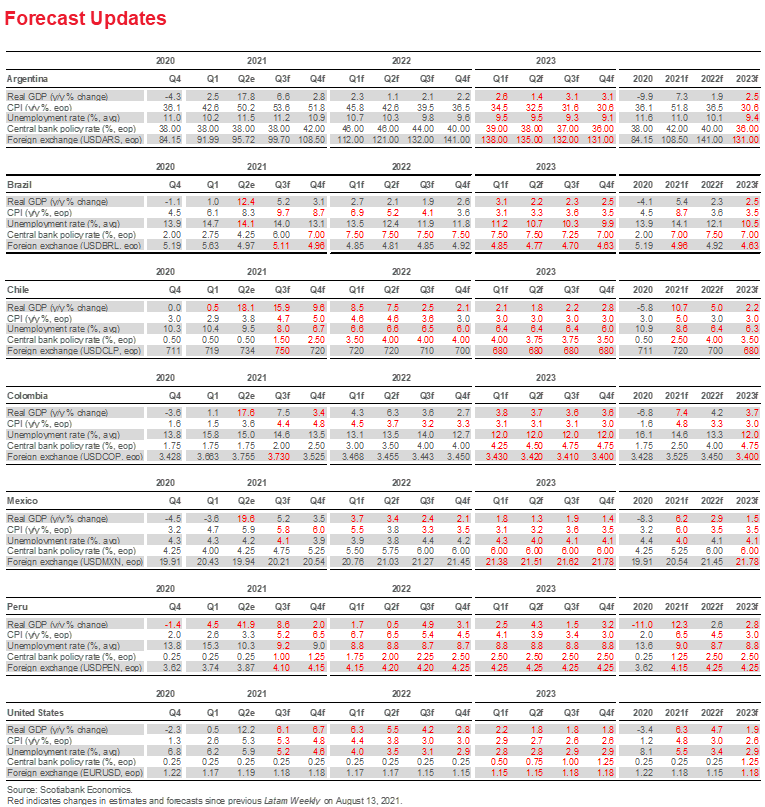

- Developments on the inflation front highlight substantial and wide-ranging revisions to key variables. Changes are identified in the following table.

ECONOMIC OVERVIEW

- Higher inflation has brought monetary policy to the forefront. While recent price pressures undoubtedly reflect supply-side shocks emanating from bottlenecks in global supply chains, there is no room for complacency.

- Central banks must guard against temporary inflation surprises becoming entrenched in inflation expectations. This means higher interest rates. Our country teams have revised their forecasts.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

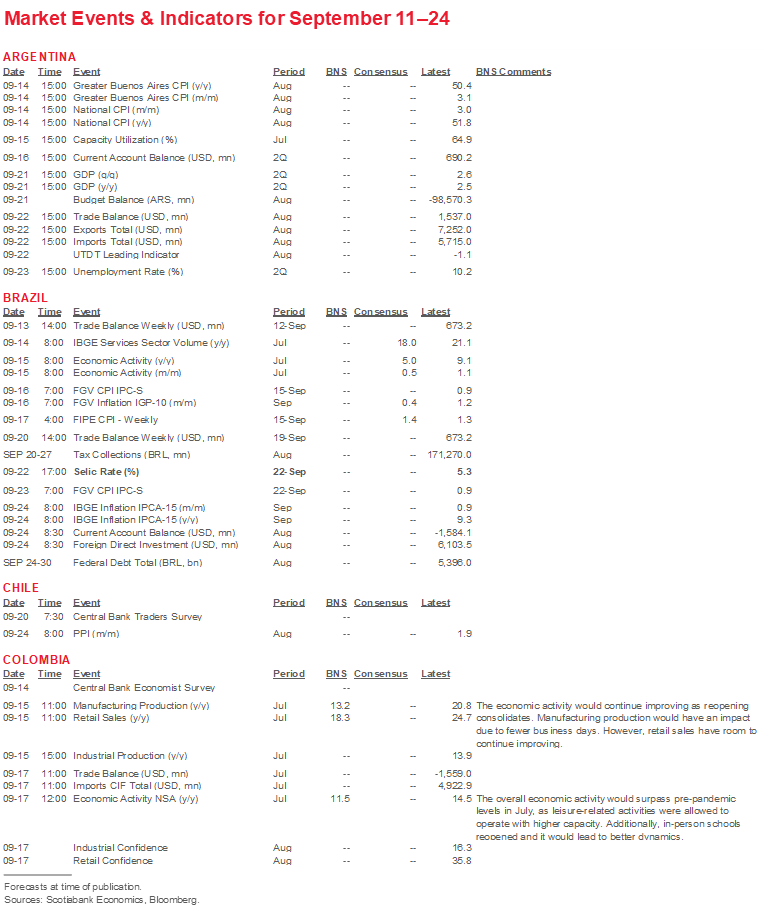

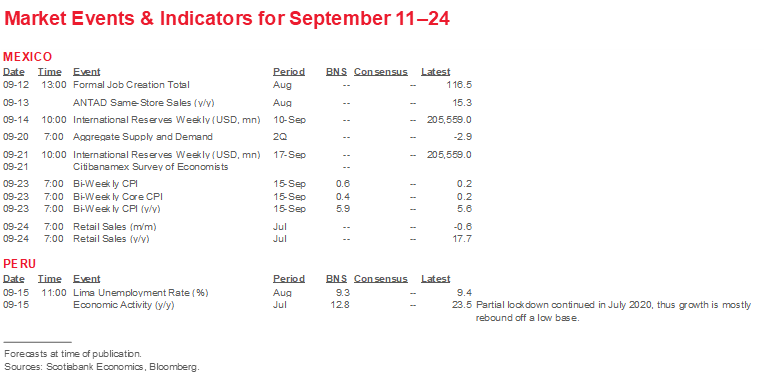

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period September 11–24 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Higher Inflation, Higher Rates

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Inflation has risen across the Latam region, testing central bank price stability commitments.

- Failure to provide a nominal anchor to the economy could risk transforming transitory price shocks into sustained inflation.

- Central banks have already responded to higher inflation, or are poised to do so, to prevent temporary price pressures becoming entrenched into inflation expectations. Key policy rates have been raised; our country teams project further rate hikes are coming.

- The overarching message is clear—higher inflation means higher rates.

INFLATION, MONEY AND INTEREST RATES

As noted in the recent update to Scotiabank’s Forecast Tables, supply chain constraints appear to be longer-lasting and more binding than previously assessed. These constraints are not only impairing short-term growth prospects in advanced countries, they represent a global inflation shock that could, potentially, test central bank price stability targets if not addressed in a timely fashion. Inflation has already surged across the Latam region.

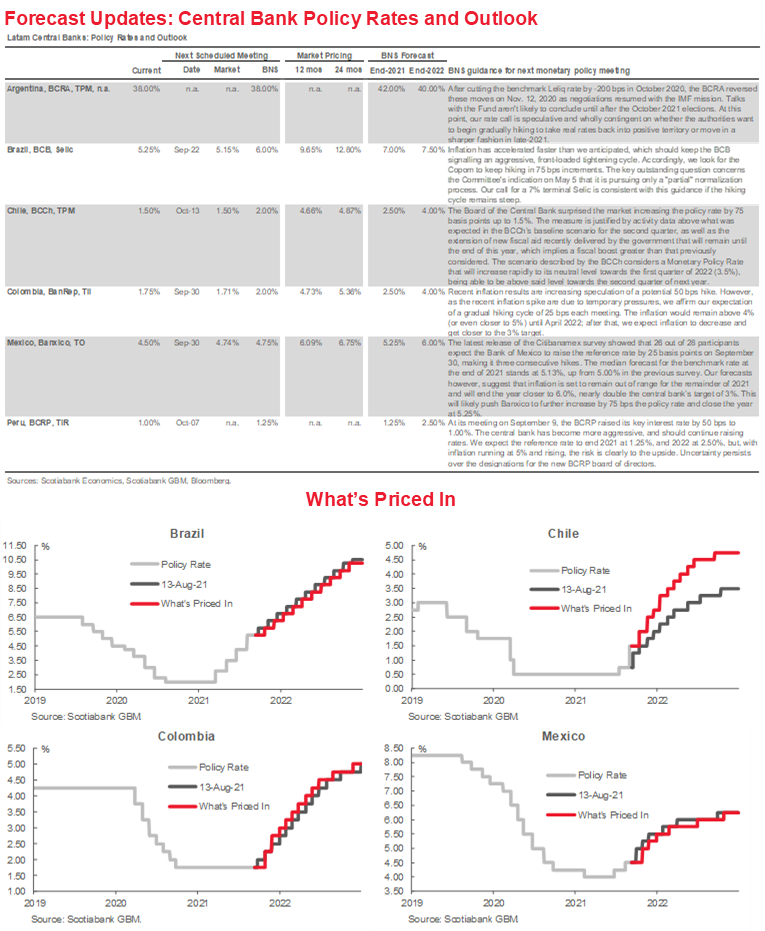

Most Latam central banks have responded to higher inflation. The central banks of Brazil, Chile, Mexico and Peru have all moved to raise key policy rates; our team in Colombia expects BanRep to follow suit at its next policy meeting, scheduled for September 30. In Peru, the BCRP coupled rate hikes with a steep increase in reserve requirements, which our experts in Lima point out is not without precedent (see discussion below).

In raising their policy rates, central banks are balancing short-term support for the economic recovery with longer-term commitments to price stability. A key issue here is the extent to which the current surge in inflation is temporary. While all countries in the region have been affected by disruptions to global supply chains, there are, as well, country-specific idiosyncratic shocks (see discussion below on Colombia).

But even if recent price pressures reflect transitory supply-side shocks and bottlenecks in global supply chains, there is a risk that they could become embedded in inflation expectations. The potential for this effect explains the importance central banks attach to monitoring expectations. In this respect, most Latam central banks have well established inflation-targeting frameworks to anchor expectations.

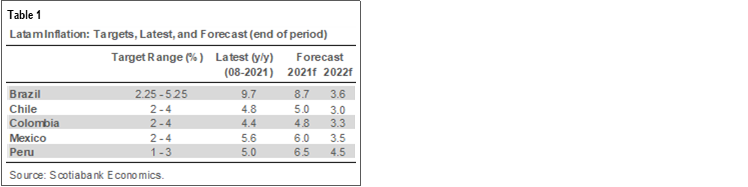

The credibility accumulated through the successful operation of inflation targeting frameworks should assist Latam central banks to strike a felicitous balance in their policy balancing act. Nevertheless, the speed with which inflation has increased clearly raises the stakes—the longer that tightening is deferred, the greater the risk that expectations become unmoored. And with inflation breaching the upper bound of inflation targets, the credibility that central banks need to anchor expectations could be eroded (table 1). Added to this is the observation that inflation can rise quickly, like an elevator, but usually only comes down slowly, like an escalator; often after a painful and protracted period of slow growth. These considerations account for the proactive policy actions by some central banks.

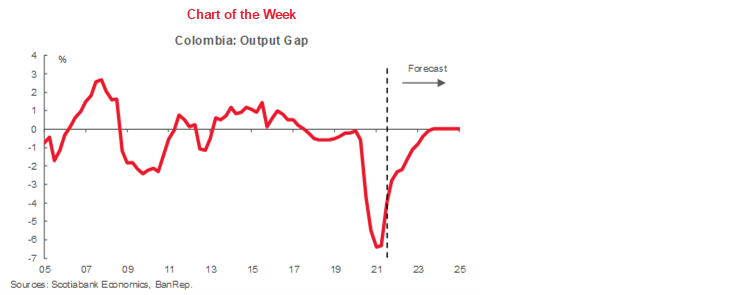

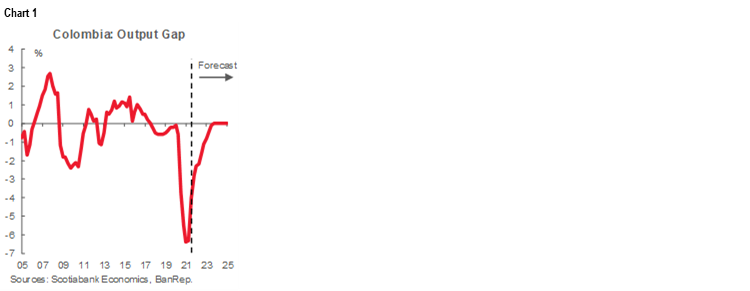

At the same time, these measures have been taken against a background of economic recovery. Latam economies are bouncing back from the pandemic and, as the discussion of Mexico below highlights, with mobility restrictions easing in most countries, the recovery should continue. Reflecting these developments, growth prospects have been marked up across the region since June, substantially so in most cases. (Of course, the outlook remains uncertain and further pandemic setbacks could reverse some of the progress made in terms of the recovery.) Stronger growth over the medium term would close output and employment gaps. For example, our team in Colombia anticipates the output gap closing over the forecast horizon (chart 1). In Chile, meanwhile, the employment gap continues to steadily narrow (see discussion below). Progress in closing these gaps is being made elsewhere in the region.

Maintaining the current stance of monetary policy in these circumstances would likely fuel inflation, quite apart from any supply-side price pressures. This is because most reference rates in the region remain deeply negative in real (after inflation) terms, despite recent rate hikes, given the surge in inflation. At some point, however, real policy rates will have to “normalize,” that is, move to a level that is consistent with price stability at full employment.

There is no debate about the direction of change. Interest rates must move up to safeguard price stability commitments. In this respect, the lesson from the “great inflation” of the 1970s is that failure to provide a nominal anchor could well transform temporary shocks to the price level into a problem of continuing inflation. The critical question is the speed at which central banks move down the path of monetary tightening.

All of this has led our country teams to revise their policy rate forecasts. For Brazil, our team now anticipates the policy rate to hit 7.00% by end-2021, up from our June forecast of 5.75%. Smaller upward revisions have been made to the rate forecasts over the same horizon for Chile (100 bps), Mexico (100 bps) and Peru (75 bps). In Colombia, in contrast, our team in Bogota has pared down its forecast of year-end inflation by 100 bps owing to country-specific factors that could contain price pressures there. In all cases, however, rates move higher relative to current levels. The overarching message is clear: higher inflation means higher rates.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Positive Economic Figures Amid the Reopening

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

56.2.2619.5435 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

56.2.2939.1495 (Chile)

waldo.riveras@scotiabank.cl

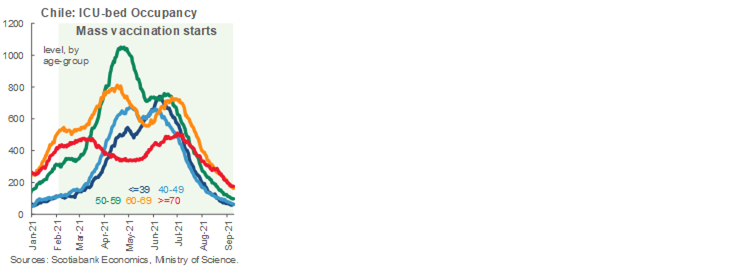

The number of confirmed COVID-19 cases per day has continued to decrease, falling to its lowest levels since April 2020. Similarly, the positivity rate is at the lowest level seen since the beginning of the pandemic and COVID-19-related deaths are decreasing. Vaccination reached 87% of the target population, while the occupancy of ICU beds continues to decrease in all age groups (first chart). Thanks to these developments, mobility has continued to increase, reaching—or surpassing for some activities—pre-pandemic levels. As of September 9, no commune is in lockdown, while more than 97% of the population has reached the highest degree of mobility in the “Paso a Paso” Plan.

In the political arena, on August 21, the centre-left coalition Unidad Constituyente, held an unofficial primary election that saw Yasna Provoste surge as the coalition’s chosen representative for the presidential first-round election on November 21. With this result, the Electoral Service (Servel) confirmed the candidacy of Gabriel Boric (left), Sebastián Sichel (centre-right), José Antonio Kast (far-right), Marco Enríquez-Ominami (Progressive Party), Franco Parisi (People’s Party) and Eduardo Artés (far-left).

On Tuesday, August 31, the Board of the central bank (BCCh) surprised the market by increasing the policy rate by 75 basis points up to 1.5%, significantly above the consensus, which expected between 25 bps and 50 bps. The measure was justified by activity data above what was expected in the BCCh’s baseline scenario for the second quarter, as well as the extension of new fiscal aid recently delivered by the government that will remain until the end of this year, which implies a fiscal boost greater than that previously considered.

On Wednesday, September 1, the BCCh published its Monetary Policy Report for the third quarter of 2021, in which it raised its GDP growth forecast for 2021 to a range between 10.5% and 11.5%, due to the most recent positive surprises and the greater dynamism of consumption. In addition, the BCCh increased its forecast for the CPI inflation from 4.4% y/y up to 5.7% y/y to December 2021. All in all, the scenario described above considers a Monetary Policy Rate (MPR) that will increase rapidly to its neutral level towards the first quarter of 2022 (3.5%), being able to be above this level towards the second quarter of next year.

On a positive note, our high-frequency indicators point to a new upturn in purchases with credit and debit cards in August and early September, evidence that the liquidity coming from fiscal aid and withdrawals of pension funds is fueling consumption. Private consumption is reaching new historical highs. Department stores continue to benefit from high liquidity while services show some recovery due to greater mobility and reopening of the economy (second chart).

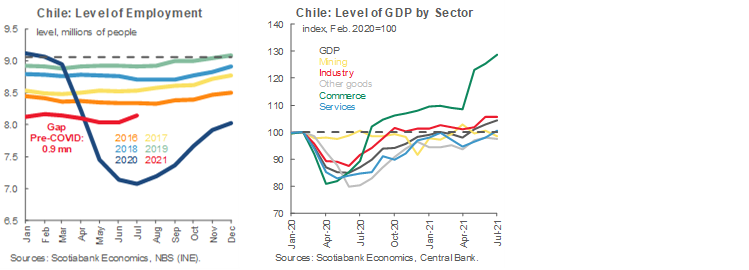

On August 31, the statistical agency, INE reported a drop in the unemployment rate to 8.9% in the quarter that ended in July, better than expected by the market (9.2%). Employment grew again (+108 thousand), after four consecutive months of falls or stagnation. Overall, the employment gap improved against pre-pandemic levels, narrowing to 914 thousand jobs (third chart), of which 476 thousand are formal jobs (52% of the total) and 439 thousand are informal. Moreover, on September 1, the BCCh released the July monthly activity index (Imacec), which expanded 18.1% y/y, in line with both market and Scotiabank expectations. According to the BCCh, only mining and construction sectors remain marginally below pre-COVID-19 GDP levels (fourth chart 4).

On September 8, the INE released the Consumer Price Index for August, which increased 0.4% m/m (4.8% y/y), above our expectations (0.2% m/m). The increase was largely explained by price rises in the restaurants and hotels component and housing. In our view, the process of reopening of the economy during August led to several services experiencing important and counter-seasonal increases in prices. Goods prices, meanwhile, showed signs of stabilizing.

In the fortnight ahead, on September 15, the BCCh will release the Minutes of its latest Monetary Policy Meeting.

Colombia—Is Higher Inflation Temporary?

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

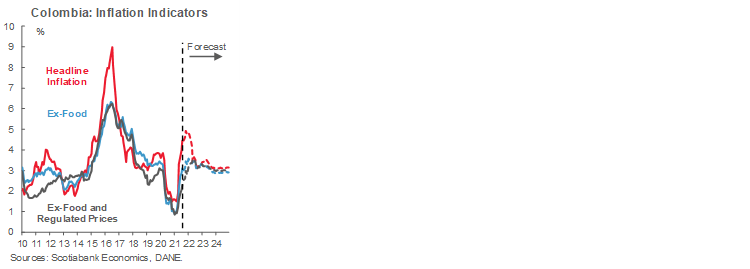

The global spike in inflation has affected all Pacific Alliance countries (PAC), although the impacts have been rather different across countries. For instance, inflation has gradually increased in Colombia during 2021. In fact, while inflation is twice the upper bound of central bank targets in Peru and Mexico, in Colombia, headline inflation barely exceeded the BanRep’s target range in August. This more modest pace of price increases has given the central bank more time to start the hiking cycle later, and allowed it to continue to support credit and domestic demand recovery for longer. Having said that, the question that arises is whether headline inflation and, more important, core inflation will continue to remain relatively “well behaved” or if Colombia is just lagging the movement to higher inflation observed elsewhere, in which case we would need to expect much higher inflation in the coming months.

Inflation in Colombia has been affected by several shocks that are important to understand in order to anticipate the future behavior of prices. These shocks include:

1. Statistical base effects reflecting the effects of the pandemic that play an important role in annual inflation. In 2020, CPI inflation displayed highly unusual behaviour, with six months of price declines and inflation ending the year below BanRep’s target.

2. FX depreciation that puts pressure on tradable goods. In the year to date, while the COP depreciated more than 11%, tradable inflation has accelerated by 218 bps (roughly a pass-through of 8% on total inflation), which increased headline inflation by 44 bps (tradable goods weight is 20% of the CPI basket).

3. International bottlenecks owing to problems in global supply chains have also boosted inflation from higher import costs.

4. The nationwide strike, especially in May 2021, led to large increases in some food prices. In addition, mobility restrictions and road blockages affected prices. The protests’ effect on prices has also lasted longer than expected as the normalization of food distribution channels has taken more time. Currently, food inflation is 11.5% y/y and is expected to increase a bit further to almost 13% by the end of the year. However, headline inflation will face a high base effect next year, which would bring food annual inflation down to levels close to 3.5%.

5. The economic activity recovery path has been healthier, pushing up domestic demand and core prices close to BanRep’s target. In fact, December 2020 Inflation ex-food and regulated prices ended at 1.1% y/y, whereas up to August 2021 this measure is at 2.31% y/y.

In view of these considerations, we expect the economic recovery to continue and core inflation to return to 3% by the end of the year (first chart). For 2022, we expect core inflation to hover around 3% once the base effect and bottlenecks in the distribution channels normalize, which should compensate for consumption recovery next year.

This outlook reflects several considerations. In this respect, among the shocks identified above, we think consolidation of the economic recovery and stronger demand next year are likely to have the most long lasting impact. Having said that, however, we anticipate that the normalization of food prices next year will reduce headline inflation by about 140 ppts. And while the resolution of global supply chain issues will not reduce prices, it would relieve further upward pressures on import goods, allowing base effects to play out in favour of lower annual inflation next year. Finally, the bias is that the COP will appreciate somewhat given stronger international demand and higher domestic investment fueled by FDI, which also helps headline inflation to return to the target range.

All in, we think current upward CPI pressures will continue this year and start to decline gradually in the H1-2022, bringing headline inflation closer to BanRep’s target range, while domestic demand will continue on its recovery path, but still under a negative output gap. Therefore, despite recent upward inflation surprises, we stick to our base case scenario in which BanRep will start the hiking cycle at the September 30th meeting, increasing the policy rate by 25 bps to 2% by year-end and gradually getting a neutral rate of about 5% by the end of 2023 or Q1-2024. We acknowledge that the likelihood of a more front-loaded hiking cycle has increased, but we think this scenario will depend on future core inflation and inflation expectations, so we expect BanRep’s Board to fine-tune the speed of the hiking cycle according to the data that comes out each month.

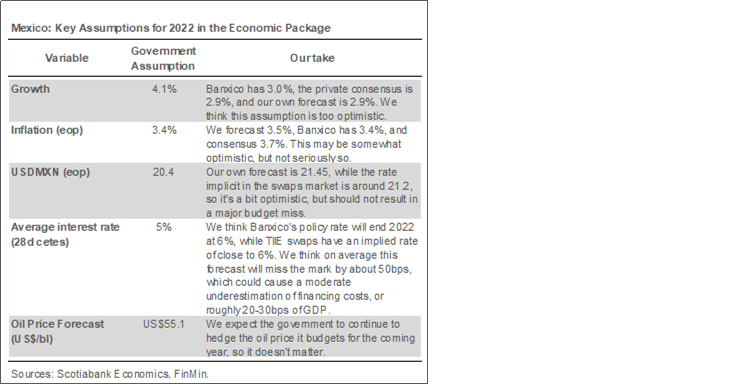

Mexico—2022 Economic Package

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

On the policy front, new Finance Minister Rogelio Ramirez de la O presented his first economic package, including the budget and revenues law for 2022. Implementation of the package is a three-stage process. First, the Economic Policy Guidelines must be ratified by the Legislative, setting the assumption framework under which the package is supported (table 1). Second, the Revenues Law (including the debt ceiling) will follow and requires ratification by a 50% + 1 majority in both houses. Third, approval of the Expenditure Decree, which only needs ratification (also a 50% +1 majority) by the Lower House by the November 15 deadline. Morena’s coalition has the necessary votes in both houses, and we don’t anticipate major changes to the package.

As was expected, the budget is largely consistent with those of previous years. However, as discussed below, there are some elements of the new Finance Minister’s initial presentations that suggest differences in style relative to his predecessor, Minister Herrera. Key elements of the package include:

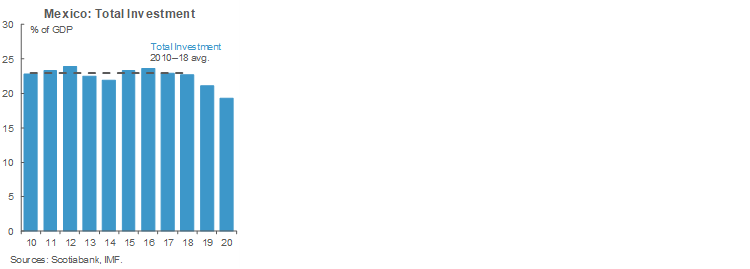

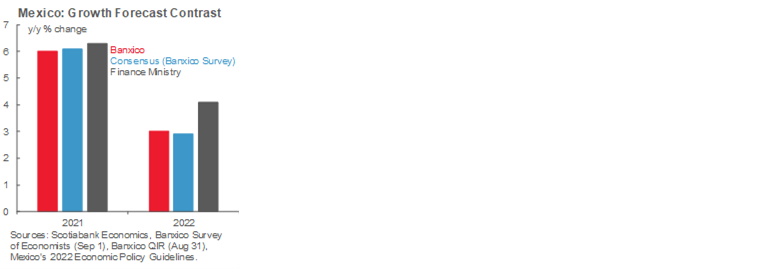

- The government’s 2022 budget is based on a growth assumption of 4.1% for the year. This contrasts with the 2.9% consensus among private economists, and the 3.0% anticipated by Banxico. As we wrote last week, we believe that new Finance Minister Ramirez de la O sees himself playing the role that Alfonso Romo (former Presidential Chief of Staff and liaison to the private sector) held as liaison between the government and the private sector, seeking to boost investment by instilling confidence. In an interview released on September 9, the Finance Minister is said to have pointed towards a recovery in private investment as the anchor that will support the government’s much more optimistic growth projection for 2022. The 4.1% growth estimate is explicitly premised on the assumption that the government will succeed in boosting confidence. To some degree, we do agree that investment should pick up somewhat in 2022—not necessarily because firms will seek to expand (which requires a recovery in private sector confidence), but because after two years of deep contractions, which has seen investment to GDP drop by almost 20% of its pre-2019 level, companies will have to invest simply to keep market share in an economy with a growing population (first chart).

- The budget assumes a 7.5% increase in revenues—including a more optimistic growth estimate than either Banxico or consensus expects, as well as a relatively optimistic estimate of oil production of 1.826 mm b/d, implying a 4% growth over 2021 (second chart)—coupled with a 9.6% growth in spending. This combination implies a widening in the deficit owing to faster spending growth, but also because of risks to missing the oil revenues target and growth that is lower than forecast, should either Banxico or private economists prove correct. However, there does not appear to be a major increase in indebtedness looming, even with these considerations. In this respect, the structural problem with Mexico’s public finances is not unsustainable deficits, but rather slowing potential growth due to poor investment (i.e., a long term structural public finance risk).

All told, while we see risks that the budget will miss the mark, we don’t see a miss (or a necessary adjustment) in the debt-to-GDP ratio larger than 40–70 bps of GDP. This is relative to the budgetary deficit of 3.1% of GDP that the package anticipates.

Revising our growth and inflation forecasts higher

We have revised both our 2021 and 2022 growth forecasts upwards. Our changes are based on an earlier-than-anticipated reopening of parts of the service sector (despite the third wave of the pandemic) as well as stronger-than-anticipated impulse from the US economy. We had expected the third wave to lead to broader lockdowns at the end of Q2 and the start of Q3, but the government decided that, with progress being made in vaccinating some of the more vulnerable members of the population, stronger restrictions were not necessary.

Next week we expect Banxico to publish its Report on Regional Economies, in which we anticipate seeing a continuation of some trends that back our upwards growth revisions, including:

- A recovery in south of the country, which has lagged the rest of Mexico, led by improvements in activity levels in tourism and entertainment-linked services. With the tourism sector recovering, we also expect the employment gap will continue to close (it is almost shut now).

- Stronger infrastructure spending—heavily concentrated in the south of the country as the government accelerates its Maya Train and Dos Bocas refinery investments.

- A modest loss of steam in industrial activity in the north of the country, which is partly caused by supply chain disruptions. Banxico’s Quarterly Inflation Report (Box 3, p. 38) included an interesting and detailed analysis of this issue, with estimates showing that the supply chain disruptions would actually be more costly in 2021 H2 than in H1.

Peru—It’s All About Monetary Policy

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head of Economic Research

51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

The week was fraught with events having to do with the future of monetary policy in Peru. Much of the domestic debate this week focused on whether the government would or would not ratify Julio Velarde as head of the BCRP. The signals the government had been giving in the past about their intentions to do so have grown somewhat stale, and their delay in confirming Velarde’s designation makes one wonder about their conviction. Finance Minister Pedro Francke stated this week that a decision would not be made until the end of the month. This seems to suggest that the government is still weighing its options.

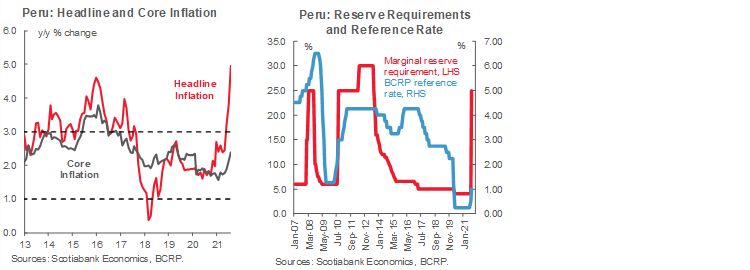

Meanwhile, yearly inflation surged to 5% in August (first chart). The BCRP answered in force, raising the reference rate by 25 bps in August, and 50 bps on September 10. The reference rate now stands at 1.0%. Furthermore, the BCRP raised the marginal reserve requirement that banks must deliver on PEN deposits (second chart). Whereas before banks had to withhold PEN 5 out of each PEN 100 in new deposits they received for purposes of meeting BCRP reserve requirements, it will now have to reserve PEN 25 out of each PEN 100 received. This is a huge increase, although not without precedent. The BCRP did something similar in 2010. Note that this occurred as it raised its reference rate by 300 bps over the course of little over a year, from 1.25% to 4.25%. The context is different now, what with the risk of a third wave of COVID-19 looming, and an economy still trying to catch up with 2019 levels.

The question is, given current circumstances, just how quickly the BCRP will move. On the one hand, the BCRP surely recognizes the need to control price instability as soon as possible. Earlier this week we had brought forward the BCRP tightening schedule, with a view that the BCRP would raise its reference rate to 1.25% in 2021 (our previous forecast was 0.50%), and to 2.5% in 2022, from 1.0% previously. However, the 50 bps increase suggests that the BCRP may be even more aggressive, and the risk is now clearly to the upside. This in spite of the fact that core inflation is still within the target range, at 2.6%, and that inflation expectations are at a still-mild 3.07%, up very little from 3.03% in July. In its guidance document, the BCRP continued stressing that inflationary pressures are transitory, and that it expects inflation to return to the target range in 12 months’ time. At the same time, the document states that the BCRP will keep a keen eye on inflation expectations. Although inflation expectations, at 3.07%, continue to be relatively subdued, this most likely simply reflects a lag between expectations and a headline inflation which has risen with surprising speed. Over time, the gap should close, putting more pressure on the BCRP.

Provided, of course, that the new BCRP Board will behave similarly to the current one. Until we have greater insight on the composition of the Board, this is also a source of uncertainty.

The reality of inflation has changed swiftly in the country. Earlier this week we raised our inflation forecast to 6.5% for 2021, from 3.5%, and to 4.5% for 2022, from 3.0%. These are hefty changes. The pass-through from higher import prices (especially energy, and soft commodities such as wheat and maize), higher freight, containers and other transportation costs, and a rising FX rate, has still to be felt fully in headline inflation (third chart). Wholesale price inflation, soaring at 12% yearly, is telling in this regard. A year ago, wholesale inflation was negligible at 0.1%. Domestic political and policy uncertainty is also spurring volatility, with the risk that the PEN depreciation of recent months could generate a feedback loop with inflation. The BCRP needs to disrupt this loop quickly, which is why it is acting more aggressively, despite an economy that is still trying to get back on its feet after the 2020 COVID-19 lockdown.

In sum, there are a number of factors that will be putting pressure on headline inflation for some time still, and it will likely take some time before the BCRP’s tighter monetary policy will get inflation back within the bounds of the BCRP target range. More so, considering that much of inflation is due to global cost factors outside of the BCRP’s control.

Finally, given persistent political turbulence, and in view that the USDPEN continues to ignore external account fundamentals, we are raising our FX forecast from 3.65 to 4.15 for 2021, and from 3.60 to 4.25 for 2022. We note, however, that visibility is low, and there are strong countervailing forces in play. Terms of trade are at their best level since 2012. The trade balance is on its way to an all-time high of USD 13.8 bn this year, and then on to USD 16 bn in 2022, according to our forecasts. Given this background, the PEN should be strengthening. And yet, it’s not. With inflation rising, and political uncertainty high, both local businesses and households are taking refuge in the USD. There has been a record outflow of nearly USD 10 bn of business and household short-term capital in the first half of 2021, mostly in the second quarter. We understand that this outflow has since slowed, but it has not been stemmed. At the same time, and to add to the conflicting factors bearing on the FX market, the withdrawal of monetary stimulus by the BCRP should give support to the PEN. Considering the complexity and degrees of uncertainty of the factors involved, the PEN FX market has become very hard to forecast. Our forecast is somewhat of a compromise: the weakening trend continues, but at a slower pace than in the past.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.