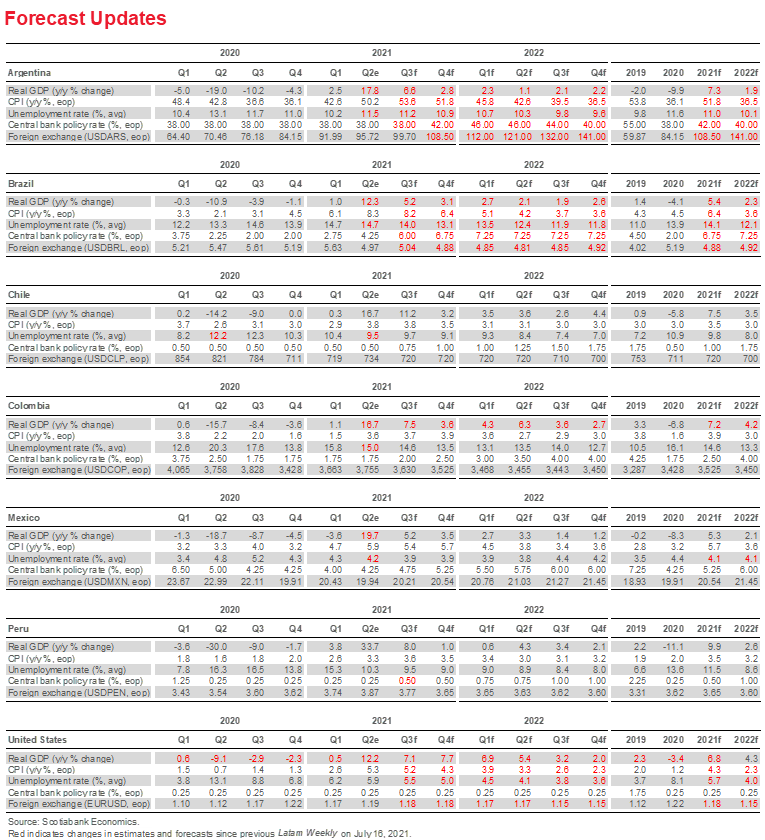

FORECAST UPDATES

- Key highlights of central bank policy considerations and interest rate developments.

ECONOMIC OVERVIEW

- Central banks have begun rebalancing monetary conditions in response to higher inflation.

- Policy rebalancing requires careful management; inflation-targeting frameworks can assist regional central banks deliver on their commitments to low, stable inflation.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

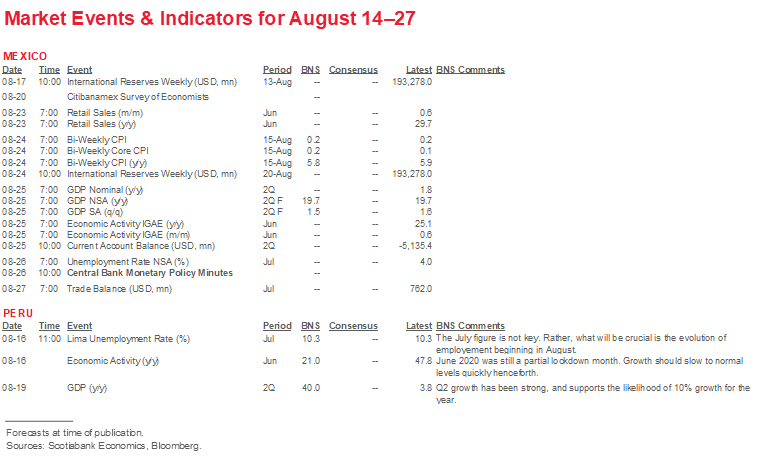

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period August 14–27 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Monetary Policy in the Spotlight

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Policy rate hikes in Mexico and Peru in response to rising inflation highlight the challenges facing Latam central banks.

- Minding the three Rs—recovery, reflation, and rebalancing—can help them meet the challenge.

- Inflation-targeting frameworks have allowed central bankers to build credibility; that credibility should help them adhere to low inflation commitments.

The Three Rs of Monetary Policy in a Time of Contagion

Latam central banks are in the spotlight. The attention focused on them reflects the fact that, as output and employment lost in the pandemic are recouped, inflation has increased. And for central banks operating under inflation-targeting frameworks, sustained inflation above target levels could erode their credibility, and with it their effectiveness. Such considerations militate for timely action to contain inflationary pressures. But moving too soon, too aggressively could derail nascent recoveries and retard the progress that has been made assisting vulnerable groups side-swiped by the pandemic. The challenge facing Latam central bankers is getting the timing right.

Meeting this challenge entails three R’s. The first “R” is recovery. Central banks will have to accurately gauge the pace and resiliency of economic recovery. In this, they must “watch the plots and mind the gaps”; that is, carefully assess prospects for the global economy and closely monitor output gaps in their own economies. The somewhat hawkish “dot plot” projections of US Federal Reserve governors in June signaled higher future global interest rates. A rapid closing of the gap between potential output and actual output in their own economies, meanwhile, could presage domestic demand-driven price pressures.

The second “R” is reflation. While inflation is rising across the Latam region, the extent to which this process reflects a temporary reflation from the low levels of inflation recorded earlier in the pandemic, or a possible acceleration of ongoing price pressures, is unclear. What is clear is that the rebound in economic activity across the region has driven prices higher. Supply-side bottlenecks and relative price effects, as demand surges over available supply, have exacerbated price pressures. And while these shocks may prove transitory, there is a risk that higher inflation—even if temporary in nature—could become embedded in expectations with possible consequences for ongoing inflation.

The third “R” is rebalancing. Latam central banks responded to the economic contraction resulting from public health lockdowns and March 2020 financial market turbulence by adopting a range of extraordinary measures, including sharp cuts to key policy interest rates. Those cuts, which drove real policy rates (actual rates adjusted for inflation) into negative territory, were critical to stemming market dysfunction and stabilizing economic activity. Such counter-cyclical and financial stability responses are entirely appropriate. But as inflation increases with the economic recovery, there is a risk that real policy rates become even more negative, imparting a expansionary impulse as output gaps close and the economy returns to its full employment level. That outcome would entail a pro-cyclical stimulus that could fuel inflationary pressures and possibly lead to other macroeconomic imbalances. Going forward, therefore, central banks across the Latam region will have to rebalance monetary conditions to ensure that appropriate support is given to the economy without undermining the inflation objective.

Most have already begun the process, with central banks in Brazil, Chile, Mexico and Peru raising policy rates. The Banco Central do Brasil increased its Selic rate 100 basis points on August 4, extending an aggressive tightening cycle started earlier in the year that had featured three previous 75 bps hikes. Mexico’s Banxico and Chile’s BCCh surprised markets with smaller 25 bps increases on June 24 and July 14, respectively, which our teams in Mexico City and Santiago view as the start of monetary policy rebalancing. Banxico followed up with a widely-expected 25 bps hike on August 12 (see discussion below). In Peru, the BCRP also raised its policy rate 25 bps August 12, in a move that was telegraphed by earlier policy pronouncements. Our experts in Lima likewise see the move as the start of gradual tightening cycle. Moreover, while the BanRep in Colombia has yet to pull the trigger on rate hikes, despite above-target inflation, it is a question of “when” not “if.” Scotiabank’s team in Bogota anticipates the rebalancing process to begin in September with a 25 bps hike, followed by successive increases that leave the policy rate at 2.50% by year end. More generally, central banks across the Pacific Alliance and Brazil have clearly signaled their resolve to uphold long-standing commitments to low, stable inflation.

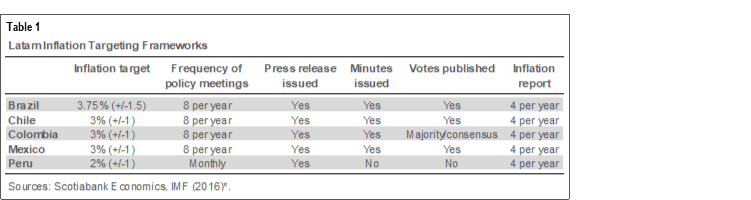

These central banks have benefited from the adoption of inflation targeting regimes (table 1). Key elements of those frameworks include the inflation target to be pursued as well as transparency and accountability measures. The latter are critical to anchoring expectations: inflation targeting central banks that consistently meet their targets will steadily build credibility. This credibility, once secured, allows the central bank to achieve its target with lower output losses in the face of inflation shocks. In the current conjuncture, rate hikes by central banks in Brazil, Chile, Mexico and Peru likely reflect concerns that their hard-won credibility could be eroded if temporary increases in inflation are allowed to bleed into expectations of higher future inflation.

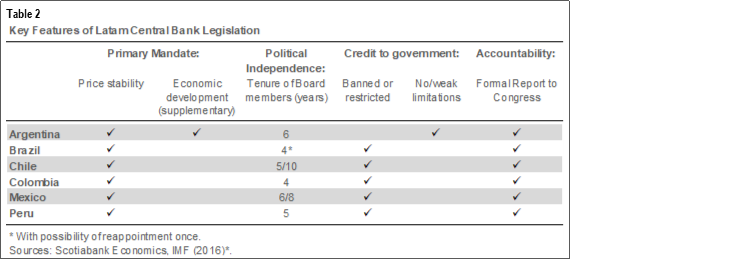

Inflation targeting frameworks also require sound legislative foundations (table 2). Foremost among these foundations is a price stability mandate as the primary objective of monetary policy. This specification recognizes that with limited policy tools at its disposal a central bank that tries to achieve too many objectives may be unsuccessful in meeting any. Central banks in Brazil and the Pacific Alliance countries all have legislated price stability mandates. Argentina, in contrast, adds an economic development mandate, creating the potential for the central bank to deviate from inflation control in pursuit of development objectives.

* Carriere-Swallow, Jacome, Magud and Werner: “Central Banking in Latin America: The Way Forward,” IMF Working Papers, Volume 2016, Issue 197, 30 September 2016.

At the same time, the exchange rate is a crucial metric for Latam central bankers; they may be more likely to intervene in foreign exchange markets than, say, advanced economy central banks. While this focus on exchange rates may appear at odds with the primacy attached to price stability, there is no inconsistency given the potential for exchange rate pass through effects from sharp depreciations to feed through to higher inflation (as well as potential financial stability effects that could deflect the central bank from its primary goal). In this respect, smoothing exchange rate shocks may keep expectations moored, achieving the overarching objective of price stability.

A framework of constrained discretion is another critical element of inflation targeting. This framework has three elements: first, independence from the political authorities, especially as regards to the government financing—the second element of constrained discretion—and, third, accountability mechanisms by which the performance of independent central bankers is assessed. Independence to exercise policy discretion is promoted by having explicit timelines on central bank board tenure (typically with a stipulation that a member can only be removed “for cause”).

Meanwhile, the risk of fiscal dominance—the situation in which monetary policy is subordinated to the needs of government financing—is contained by outright prohibitions or clear restrictions on the provision of central bank financing. Such provisions reflect the fact that effective monetary policy requires a supportive fiscal environment to achieve low, stable inflation and good economic performance. While central banks in Brazil and the Pacific Alliance have clear legal restrictions on government financing, this is not the case in Argentina. As the discussion in the country notes below highlights, for example, reforms in Colombia to ensure long-term fiscal sustainability are an important element of the government’s agenda. Similarly, the new government in Peru has sought to reassure wary investors that the economic reforms it champions are not necessarily inconsistent with sound macroeconomic policies.

Central bank accountability, the third element of the constrained discretion triad, is achieved through reporting to the legislative authority in which the central bank explains why it has failed to meet its inflation targets and presents its projections going forward. Performance cannot be assessed if goals are not fully articulated.

Going forward, these foundations and the credibility that central banks have built over time may be tested as economies bounce back and global interest rates rise. A steep increase in US rates, for example, could animate sharp currency depreciations and exchange rate pass-through effects that feed through to inflation expectations. However, Latam central banks that have persevered in their commitment to long-term price stability, supported by governments that follow a prudent fiscal path, should pass the test, provided they heed the three R’s.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Government Announces USD 7 Bn in New Aid to Support Households

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

56.2.2619.5435 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

56.2.2939.1495 (Chile)

waldo.riveras@scotiabank.cl

The number of confirmed COVID-19 cases per day has continued to decrease, falling to its lowest levels since April 2020. Meanwhile, the positivity rate is at its lowest level since the beginning of the pandemic. Vaccination reached 82.5% of the target population, while the occupancy of ICU beds continues to decrease in all age groups (first chart). Thanks to these favourable developments, mobility has continued to increase, reaching levels similar to those observed before the pandemic. As of August 5, only 0.2% of the population is in quarantine.

In the political arena, on Sunday, July 18, the presidential primaries were held and included the two key coalitions at both ends of the political spectrum. On the right, Sebastián Sichel (43) (independent) won with 49% of votes in a four-candidate race. On the left, Gabriel Boric (35) from the Social Convergence Party won with 60% of votes from his coalition, upsetting the Communist Party candidate Daniel Jadue. Both will move on to the presidential first-round election on November 21, running against candidates from other parties and coalitions. On July 23, the current president of the Senate, Yasna Provoste (51), announced her candidacy for Chile’s presidential election, which will be defined in primaries of the “Unidad Constituyente” coalition (to be held on Saturday, August 21).

On July 21 and 22, the Ministry of Finance (MoF) reported the issuance of USD 2.06 bn and 3.75 bn of treasury bonds in international markets. Including both issues, Chile has now issued public debt totaling USD 21.93 bn in 2021, of which USD 13.65 bn were bonds in foreign currency. The latest bond offerings are part of the updated financing plan for this year, which allows additional debt issuance for up to USD 8 bn in foreign currency, as authorized by the Transitory & Emergency COVID-19 Fund. All in all, of the USD 8 bn mentioned above, there is approximately USD 2.2 bn remaining in debt issuance for this year, which is expected to be mostly in foreign currency denominated bonds. Additionally, on August 10, the Ministry of Finance announced the extension of the Emergency Family Income program up to November 2021. The government has indicated that the cost of this new aid is around USD 7 bn, of which USD 4 bn would come from redirections and positive adjustment in tax collection due to greater economic growth. The remaining USD 3 bn would be financed with liquidation of the sovereign wealth fund and cash. The government will not issue new debt to finance this aid.

On a positive note, on July 30, the INE reported a drop in the unemployment rate to 9.5% in the quarter that ended in June, better than expected by the market and Scotiabank (10%). Moreover, on August 2, the BCCh released the June monthly activity index (Imacec), which expanded 20.1% y/y, marginally exceeding private sector expectations. These encouraging figures are the product of a few specific ingredients: greater openness and mobility, a very strong expansion of public spending on direct transfers to households, and capital spending in conjunction with liquidity injections from withdrawals of pension funds. The latter has boosted the GDP growth of the trade sector, which expanded 46.4% y/y in June.

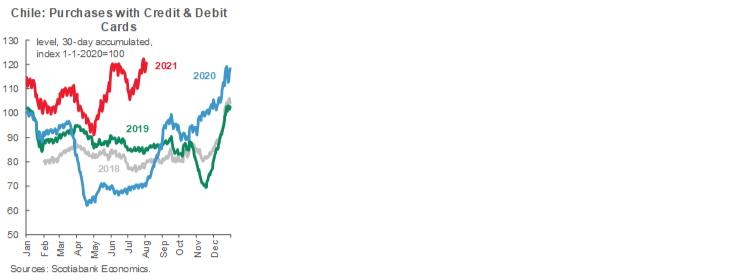

Our high-frequency indicators point to an upturn in purchases with credit and debit cards in July and August (second chart), evidence that the liquidity coming from fiscal aid and the withdrawal of pension funds is fueling consumption. However, liquidity in non-remunerated bank accounts (mainly “Cuenta Rut Banco Estado”) has doubled from that of a year ago, signaling that a significant part of the liquidity has been saved or kept aside. Department stores continue to benefit from high liquidity. A rebound in the consumption of services and fuel reflects the increased mobility of the economy.

On August 6, the INE released the Consumer Price Index for July, which increased 0.8% m/m (4.5% y/y), above both our and market expectations (0.4% m/m). July figures reflected broad increases in all divisions of the index, with increases at the core level that exceed the expected impact of higher prices for fuels and food. Core inflation of 0.6% m/m (3.6% y/y) stems from higher prices for goods (0.9% m/m; 4.7% y/y) and services (0.4% m/m; 3% y/y).

In the fortnight ahead, the BCCh will release the GDP growth for Q2-2021 on Wednesday, August 18. We expect an increase around 17.4% y/y.

Colombia—Fiscal Accounts from a Historic Perspective

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Colombia has been characterized by a robust institutional framework at the political and economic level in recent years. In fact, since the new Constitution came into effect in 1991, the central bank has demonstrated considerable independence in the context of an orthodox inflation-targeting framework with a free-floating currency. The constitutional changes also included important reforms with respect to political and legislative institutional frameworks that clearly delineated three different institutional powers: Congress, the Presidency, and the courts. History has shown that these branches are independent of each other and, in critical moments, complementary.

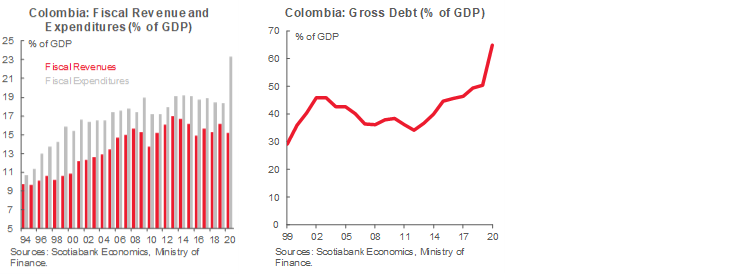

However, the Constitution also has brought higher government expenditure (first chart) and debt (second chart). Since 1994, government expenditure has increased by 8 ppts of GDP (in the pre-pandemic period) and debt has jumped to almost 64.8% of GDP in 2021, from an average of 29% of GDP at the end of the 1990s and 39.4% of GDP in the first decade of 21th century.

In addition—from an historical perspective—since 1991 Colombia has failed to modernize fiscal accounts and give them more flexibility. This means that the tax code hasn’t been adjusted at the same pace as the economy has become more open and service-based, producing a tax framework with ample opportunity for tax evasion, which can be as large as 5–6 ppts of GDP every year. Therefore, the only ways that governments have to deal with the problem of rising deficits and debt are: i) passing every two years a tax reform increasing taxes to the formal sector and making fiscal policy procyclical in periods of weak growth; and ii) trying to raise growth that boosts tax collections to keep fiscal accounts afloat.

This time is no different. Since the beginning of 2021 the government is trying to pass a fiscal reform that brings some new revenues to the accounts while doing whatever it takes to open up the economy to increase economic activity growth that helps to improve tax collection and keep fiscal accounts, somehow, controlled.

What is new this time in comparison with recent history is that Colombia—along with the rest of the world—is exiting a major crisis that hit not only fiscal accounts with deficits above 8% of GDP this year and 7% of GDP next year, but also produced a massive loss of employment (around 2 million people or 9.5% of the labour force), which put even more pressure on the government, since higher resources are needed to help the low-income population and accelerate the recovery in labour markets.

Therefore, the government is currently using several different—some more extreme than others—measures to raise some new money, including:

1. A failed tax reform that was intended to solve some structural issues from the tax collection side but, owing to bad timing, fueled the fire instead of putting it out.

2. An attempt to pass a Colombian standard tax reform to put some band-aids to the revenue side, while maintaining the extra social expenditure needed to offset the COVID-19 shock.

3. Selling one of the crown jewels, electricity transmission giant ISA. However, the government will keep control of the company with this transaction, since Ecopetrol (a public oil company) will buy it. Rather than a sale, therefore, the transaction is essentially a different way to fund expenditures. Ecopetrol (which is not included in the central government accounts) will raise the money in the international bond market, taking advantage of the high oil prices to ensure cheap financing.

4. Opening the economy to allow almost 98% of the economy to return to work since June 8, in the midst of the COVID-19 third wave, during which time the vaccinations scheme has been improving significantly.

We think the first three measures will help maintain extra social expenditure this year and next year. However, they will neither help reduce the debt-to-GDP ratio, nor send a message of fiscal sustainability to markets and international agencies.

Therefore, the next government will have to achieve two goals in order to restore confidence in fiscal accounts and maintain countercyclical fiscal policy. First, keep the economy open even if a COVID-19 fourth wave arrives and allow the private sector to continue the path of recovery, especially for the conventional sectors such as commerce, construction, and hospitality among others. Second, the next president and Congress must pass real structural fiscal reforms that align the tax system with the evolution of the economy, increasing revenues and significantly reducing tax evasion. For now, we have a high level of confidence in the goal of keeping the economy open—the vaccination rollout is going faster than expected, and regional and general governments have shown no intention of restricting mobility again. On the second goal, we need to wait for how the campaigning for next year's election evolves. However, current information leads us to be optimistic, since apparently center-leaning candidates are gaining steam, increasing the likelihood of a pro-market administration and a good relationship with Congress that makes reforms easier down the road.

Mexico—Banxico delivers a 3–2 Split Vote with a More Hawkish Stance

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Paulina Villanueva, Especialista Investigación Económica Especial

+52.55.5123.6450 (Mexico)

pvillanuevac@scotiabank.com.mx

As widely anticipated, Mexico’s Central Bank delivered a 25 bps hike on August 12, leaving its key reference rate at 4.50%. The vote was a 3–2 split decision, with Governor Alejandro Diaz de León, and deputy governors Irene Espinoza and Jonathan Heath supporting the hike. Deputy governors Gerardo Esquivel and Galia Borja voted for a pause.

Based the social media postings of deputy governors Heath and Esquivel, as well as the monetary policy statement(and previous minutes), we currently see them as the two most likely to switch from the hawkish to the dovish camps, which could potentially either lead to a pause in the tightening cycle, or a 4–1 vote hike. On August 12, deputy Esquivel sounded more upbeat about the nature of the employment recovery, pointing to the speed of the recovery relative to past crises. On the flip side, deputy Heath posted an article on his personal web page in which he appears to disagree with economists (like us) who expect an uninterrupted/front-loaded tightening cycle between now and the change of Governor at the end of 2021.

The governing Board mentioned that global inflation and the effects on supply chains and production processes have fueled headline and core prices, causing inflation expectations in 2021 to rise again. Headline inflation is now expected at 5.7% y/y for year-end, revised up from 4.8% y/y in the latest Quarterly Inflation Report but inline with the Scotiabank forecast of 5.7% y/y (table 1). Given the broad-based inflation pressures, with energy price declines—driven by base effects—offset by food inflation, rising correlations in merchandise price inflation, and earlier than expected services inflation, prices are now expected to converge to the 3% target by the first quarter of 2023 (from 2022 Q2 the previous meeting), signalling a more hawkish tone. Core inflation has also been revised up across the forecast horizon (table 2).

- Even as the board refers to the surge of inflation as “largely transitory”, they highlighted that the decision is mainly targeted at containing the increase in inflation expectation since the balance of risks for inflation are still skewed to the upside.

- The balance of risks for growth remains uncertain, but with persistent slack conditions in the economy and marked differences across sectors. Mexico’s economy is set to expand at a 6.0% y/y rate in 2021 and around 3% y/y in 2022. And while growth will be strong, it will take some time for Mexico’s output to return to pre-pandemic levels.

Against a challenging inflation outlook and the impending change in leadership at Banxico, we continue to expect a further 75 bps of tightening coming in 2021 to close the year at 5.25%, with the Board making raising the policy rate 25 bps at every meeting scheduled for the rest of this year. Our longer-term profile for monetary policy has a 6.00% terminal rate by Q3 2022—essentially the neutral real policy rate based on our inflation forecasts, which is consistent with consensus long run inflation, and Banxico’s own estimates of neutral real policy rates.

Recent Evolution of Banxico’s monetary policy framework, and market’s reaction:

While we would argue that there are several reasons why Banxico’s bias has been gradually moving to the dovish side over recent years, the speed of the transition has accelerated. The most relevant changes we see are:

- During his tenure, Governor Carstens adjusted the growth-inflation trade-off in Mexico’s pure inflation targeting regime by shifting to what he called an “efficient convergence to target”. With this change, he sought to control inflation, but increased the weight on growth by stating he sought to converge actual inflation to the target level with the lowest possible cost to growth. Although this trade-off may be obvious and intuitive, we saw its formalization as a change in relative weight between the two variables, giving growth increased priority.

- Under the current Banxico leadership, the most recent relevant tweak is the move towards “inflation expectations targeting”. Although all central banks look at both current inflation and various measures of expected inflation, we read the current discourse as signaling a move to a larger weight to expectations versus observed inflation. In the current environment, in which expectations is the lower of the two, this is, on the margin, more dovish.

- However, we also think that as we move forward from the August 12 decision, gauging the relevant weight of different inflation expectations measures will be relevant (i.e. economic consensus, Banxico’s measure, and UDI breakeven, etc.).

- One potential signal came from the August 5 change in Banxico’s communication strategy, which not only included explicit identification of board member votes, but also the announcement that Banxico will now publish its inflation forecasts alongside its monetary policy decision as well as in the Quarterly Inflation Report (as is currently the case). We take the more frequent update to Banxico’s forecasts as a signal these will be an important guide to monetary policy biases, and potentially the most relevant of the different inflation expectations measures.

- It’s worth noting that in the June 24 surprise rate hike Banxico revised upwards its inflation forecasts from 3 weeks prior (with its expected convergence to the 3.0% target being pushed back a quarter), and again revised inflation forecasts higher in the August 12 decision.

- In addition, Banxico’s board composition has seen marked changes. Traditionally, Banxico had 4 members who were career central bankers, and one external one. That has changed; starting in 2022 the board will no longer have any career Banxico members. There is also an apparent shift in the bias of board members, with those appointed by the current administration leaning more to the dovish side. It is interesting that one tweet noting this change in board member bias, and a possible further dovish shift with the arrival of Arturo Herrera, was re-tweeted by one of the current board members.

Markets seem to interpret the recent dovish tilt as likely to lead to higher longer-term inflation, at least based on the pricing of UDI break-evens. Whereas last year 5yr UDI breakeven inflation averaged close to 3.6%, the 2021 average is now close to 4% (4.2% at the current time).

Peru—A Government Without an Identity and a Central Bank Without a Head

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head of Economic Research

51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

There are two topics that are dominating the discussion on Peru. The first is just what kind of government do we have, and what can we expect it to do. The second is who will head the central bank, and how will this affect monetary and FX policy in these times of increasing price volatility.

The Castillo Government is not easy to define, as it does not seem like it can quite place itself on the political spectrum. Castillo adopted a leftist, albeit moderate and conciliatory tone during the July 28 inauguration speech, only to unnerve the political and business communities, the press, and much of public opinion when he designated the controversial and potentially destabilizing Guido Bellido to head the Cabinet. Bellido is closely identified with the radical wing of Peru Libre. Castillo’s balancing act between radical and moderate staffing and agendas is creating confusion and tension. And this uncertainty regarding the government continues to embroil the business environment and perplex markets.

This, even as Pedro Francke, the new Minister of Finance, has been striving to send market-friendly signals. Francke does seem to have a firm control over macroeconomic policy. However, even though his presence promises that the economy will be managed properly, he has little power over non-economic issues. This raises the question of whether Francke is enough to generate confidence and stability over time. Thus, the importance of having Julio Velarde continue at the head of the BCRP to boost additional confidence.

Castillo’s government is fragile and has been made more so by Bellido and other cabinet appointments—plus the subsequent questionable designations within the institutions they lead— which have eroded the moderate measure of political and popular support that Castillo had. The surge in inflation is also, no doubt, taking its toll on the government’s popularity.

According to a poll by Datum, 51% of the population want Congress to deny Bellido’s cabinet a vote of confidence. The vote will take place most likely before the end of August, and Bellido may actually try to appease Congress with a moderate tone, in hopes that this will be enough to ensure that the cabinet receives a vote of approval.

Given what we have witnessed so far in the Executive and Congress, we expect the government to follow a moderate economic agenda, with an expansionary fiscal policy, but within reasonable bounds. Our base case also assumes that key economic institutions, such as the BCRP and banking superintendency, will remain in qualified hands. We do expect the political environment to remain tense and the government’s non-economic actions to be less reliable and more uncertain. However, the government will face checks and balances. Congress has begun to take on this role. Its members elected a presiding Board that excludes members of the governing party. The head of Congress, María del Carmen Alva, is a moderate from the centre-right opposition party, Acción Popular. Key Congressional committees, including the Budget and Constitutional Matters are led by members of the opposition. To compound the message, the Committee on Constitutional Matters is presided over by Fuerza Popular, a party which opposes changing the Constitution. Overall, Peru Libre does not really seem to have the power to overcome institutional obstacles. This could include Constitutional change, which is becoming increasingly identified with the unpopular radical wing of the government.

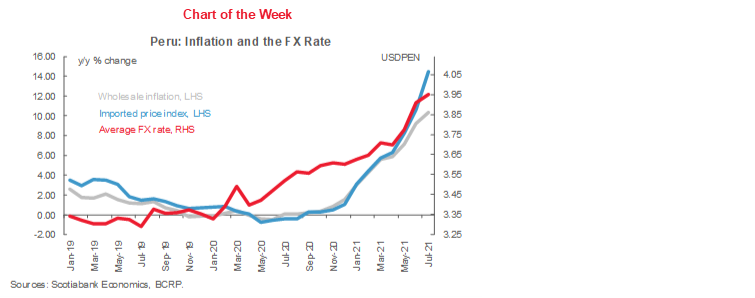

Lately, inflation and currency depreciation have emerged as new concerns for the government (first chart). Yearly inflation reached 3.8% in July, and we expect it to surpass 4% in August, and perhaps even 5% in the future, depending on what the new BCRP Board will look like. Neither Congress nor the Executive appear in much of a hurry to determine their candidates to the Board. Although government officials are blaming inflation on global contagion, there must be some level of awareness that domestic issues are involved. While it is true that high global energy and soft commodity prices, as well as higher logistics costs, are contributing to inflation, the issue at heart is domestic confidence which is driving the exchange rate up and feeding inflation through import costs.

Press reports suggest that Velarde would be inclined to accept to remain at the BCRP, but he appears to be waiting for a greater show of conviction from President Castillo first. Meanwhile, the current Board is still in control. Barring a change in mentality once a new Board is appointed, the BCRP may become increasingly uncomfortable as inflation expectations, currently at 3.03%, continue rising. This would conceivably pressure the BCRP to contemplate raising the reference rate sooner and faster.

Two aspects are moving in the government’s favour: the evolution of COVID-19 (second and third charts), and tax revenue. COVID-19 contagion is currently down 84% from peak levels, and hospitalizations are down 70% from peak levels. Approximately 27% of the population has been vaccinated with at least one dose.

Fiscal accounts also continue improving. January-July tax collections were up 41% y/y. The fiscal deficit (12-month trailing) has declined from 8.9% of GDP in January to 6.4% in June, and the full-year deficit is in line with our 4.4% of GDP forecast. Tax revenue is actually rising faster than expected, but this will be compensated by recent government spending initiatives.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.