- Colombia: June economic activity rebounded more than expected

- Peru: Central bank raises rate at 0.50% reacting to higher inflation and inflation expectations

COLOMBIA: JUNE ECONOMIC ACTIVITY REBOUNDED MORE THAN EXPECTED

June manufacturing production and retail sales data published by Colombia’s statistical agency (DANE) on August 12 show that Q2-2021 closed with robust economic activity, registering a surprising rebound from the economic disruptions of the nationwide strikes in May. As a result, risks to our Q2-2021 GDP growth forecast (16.9% y/y) are skewed to the upside. Regardless, we reaffirm our view that the central bank (BanRep) will begin moving its hiking cycle by September 2021 with gradual adjustments of 25 bps.

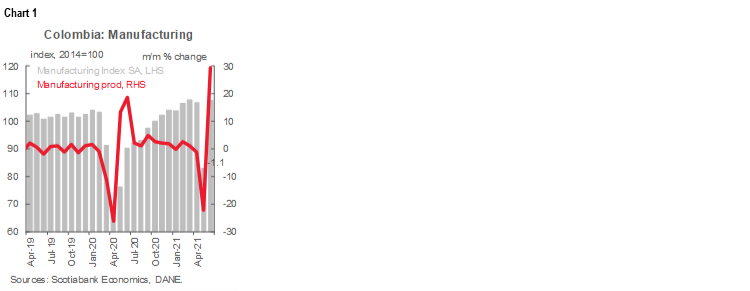

Manufacturing production

In June, manufacturing production increased by a robust 20.8% y/y, above market expectations (16.5% y/y) and our own expectation (14.0% y/y). Compared to the same pre-pandemic period (June 2019), the index grew by 8.7%. And, on a monthly basis, manufacturing increased 29.5% m/m in seasonally adjusted figures (chart 1), rebounding from the collapse in activity caused by nationwide strikes in May. In fact, manufacturing activity is close to its highest level since the pandemic began (March 2021). Manufacturing grew by 16.1% y/y in the first half of the year. Compared to the same period in 2019 (pre-pandemic), manufacturing activity is 1.6% higher.

Comparing pre-pandemic levels of activity across sectors, the best performer activities were: beverages (16.1%), chemical products (26.2%) and plastic manufacturing (15.5%).

On the negative side, employment remains a concern. June employment remains 4.5% below its level at the start of the pandemic, with half of the contraction is explained by four sectors: clothing (-11.3%), furniture (-13.5%), vehicles manufacturing (-39.0%) and bakery (-9.1%). Comparing H1-2021 to H1-2019, employment is down 4.6%.

From a regional perspective in the H1-2021 Antioquia (24.1%) and Cundinamarca (+19.3%) led the rebound, while Cauca (-7.6% y/y) and Valle del Cauca (-2.1% y/y) continue to lag the recovery as they were the most hard hit regions by the nationwide strike. In fact, in Cali (the capital city of Valle del Cauca), manufacturing activity fell -8.9% y/y.

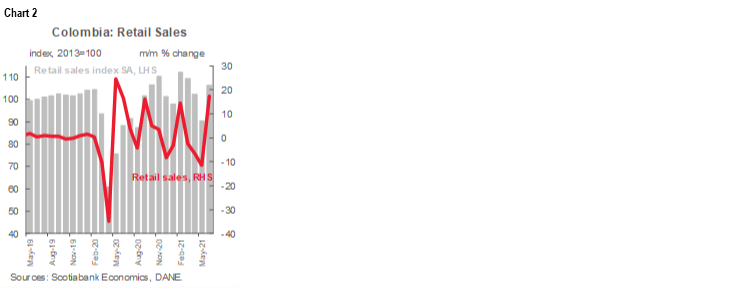

Retail sales

Retail sales expanded by 24.7% y/y, well above the expected 20.6% in Bloomberg’s survey and our 19.4% y/y estimate. Compared to pre-pandemic levels (June 2019), retail sales are now 7.1% higher. In H1-2021, retail sales increased by 4.3% relative to pre-pandemic (H1-2019). Total retail sales, excluding vehicles, increased by 17.3% m/m seasonally adjusted in June (chart 2), showing a rebound that is mainly explained by increased mobility, as large cities allowed a broad reopening and nationwide strike eased.

On a year-over-year basis, two-thirds of the increases were registered in vehicles for household use (92.4% y/y), (non-car), vehicles and motorcycles (93.0% y/y), and gasoline (26.5% y/y). It is worth noting that gasoline demand in June is just 1.5% below pre-pandemic levels. In a reflection of life during a pandemic, the best performing lines were vehicles for household use (30.9%), (non-car), vehicles and motorcycles (20%), computers for domestic use (48.7%). Additionally, DANE underscored that 2.6% of total retail sales excluding vehicles were through on-line channels.

Other relevant indicators:

DANE also published services sector data, showing that in H1-2020, the major lags in the recovery area in the film and TV production sector (-65.2% compared to pre-pandemic levels), while the best performers are postal services (17.6%) and development of IT systems and data processing (8.2%).

In addition, DANE data show that hotel occupation stood at 36.1% in June, the highest level since the pandemic began. In fact, 22.3 ppts were explained by leisure travelers, similar to pre-pandemic trends (25.5%), while hotel occupation for business travel lags as it contributed 11.7 ppts (compared to the pre-pandemic contribution of 18 ppts).

All in all, June’s activity data exceeded our expectations. The fact that major cities lifted restrictions significantly boosted activity levels. However, the labour market remains a concern as employment in the H1-2021 remains 4.6% below pre-pandemic levels in manufacturing and 4.3% below in retail sales. On Tuesday August 17, DANE will release the Q2-2021 GDP. Our expectation remains that it will show growth of 16.9% y/y, but we think the risks are skewed to the upside despite impacts from the nationwide strike, as the June rebound was stronger than expected. Either way, we reaffirm our view that the central bank (BanRep) will begin moving its hiking cycle by September 2021 with gradual adjustments of 25 bps.

—Sergio Olarte & Jackeline Piraján

PERU: CENTRAL BANK RAISES RATE AT 0.50% REACTING TO HIGHER INFLATION AND INFLATION EXPECTATIONS

I. Central bank raises rate at 0.50% reacting to higher inflation expectations

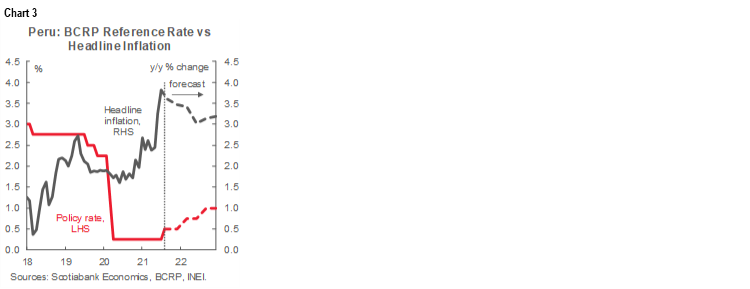

At its monthly meeting on Thursday, August 12, the Board of Peru’s central bank (BCRP) raised its key interest rate by 25 bps to 0.50% from its historical low of 0.25% (chart 3). While the decision was not widely expected by the market consensus, it is not surprising since the BCRP had already changed its narrative, opening the door to this possibility. There were also signals that raised the probability of a rate hike in that direction. The BCRP’s reference rate had been at 0.25% since April 9, 2020, following the onset of the pandemic.

The BCRP statement emphasizes that the real monetary policy rate remains at historical lows, going from -2.35% in July to -2.50% in August after the decision. The Board indicated that it will remain attentive to new information on inflation expectations and the evolution of economic activity “to consider, if necessary, modifications in the monetary policy position”, a wording that has been used in interest rate hike cycles in the past.

In July the Board had changed its future orientation from being “strongly” expansive to just expansive and abandoned its commitment to continue providing additional stimulus as needed, showing that the BCRP was preparing for future tightening, in line with other emerging market central banks.

II. Inflation continues to rise

Inflation picked up again in July, driven by higher costs of inputs and imports, going from 3.3% y/y in June to 3.8% y/y in July, above the limit of the BCRP target range (between 1% and 3%) for the second consecutive month, reaching the highest rate since February 2017. Inflation also exceeded the BCRP’s forecast of 3% for year-end. The BCRP considers that inflation will remain temporarily above the target range. Core inflation rose from 1.9% y/y to 2.1% y/y in July, exceeding the 2% y/y target for headline inflation for the first time in 16 months. The BCRP statement emphasizes that trend inflation indicators remain around the midpoint of their target range.

The BCRP’s most recent survey on inflation expectations 12 months forward is rising, from 2.6% y/y in June to 3.0% y/y in August, reaching the upper limit of the target range. The BCRP affirmed its view that inflation will return to the target range in the next 12 months as the effects of transitory factors on inflation (FX, international fuel and soft-commodities prices) are reversed and economic activity will still be below its potential level. Regarding the latter, the BCRP pointed out that expectations about the economy remain pessimistic.

Our 3.5% y/y inflation forecast for year-end has an upward bias, owing to persistent upward pressure on input and import costs. Inflation expectations are already beginning to reflect this bias, leading the BCRP to react earlier than we expected, so our benchmark interest rate forecast also has an upward bias for the remainder of the year, considering that decisions would continue to be made by a BCRP board headed by Julio Velarde. In its statement, the BCRP stopped mentioning the monitoring it had been carrying out on liquidity-generating operations, increased its overnight deposit rate by 20 bps (from 0.15% to 0.35%) and raised the rate on direct reporting transactions and loans of monetary regulation (from 0.50% to 1.00%).

Monetary expansion slowed in June, for the sixth month in a row, to a rate of 5.3% y/y, similar to the growth rate of loans (5.1% y/y), which seems to have stabilized around 5% (chart 4).

The BCRP’s statement confirmed that it will continue to take actions to mitigate the volatility of the financial markets in the context of uncertainty. In the FX market, the BCRP has injected USD 1.2 bn of liquidity so far in August, despite which the USDPEN exchange rate reached a record of 4.11. BCRP FX intervention in the year to date has been at record levels, totalling USD 12.1 bn, of which USD 6.1 bn was conducted via spot sales, USD 3.9 bn through derivatives, and USD 2.1 bn in dollar repos.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.