FORECAST UPDATES

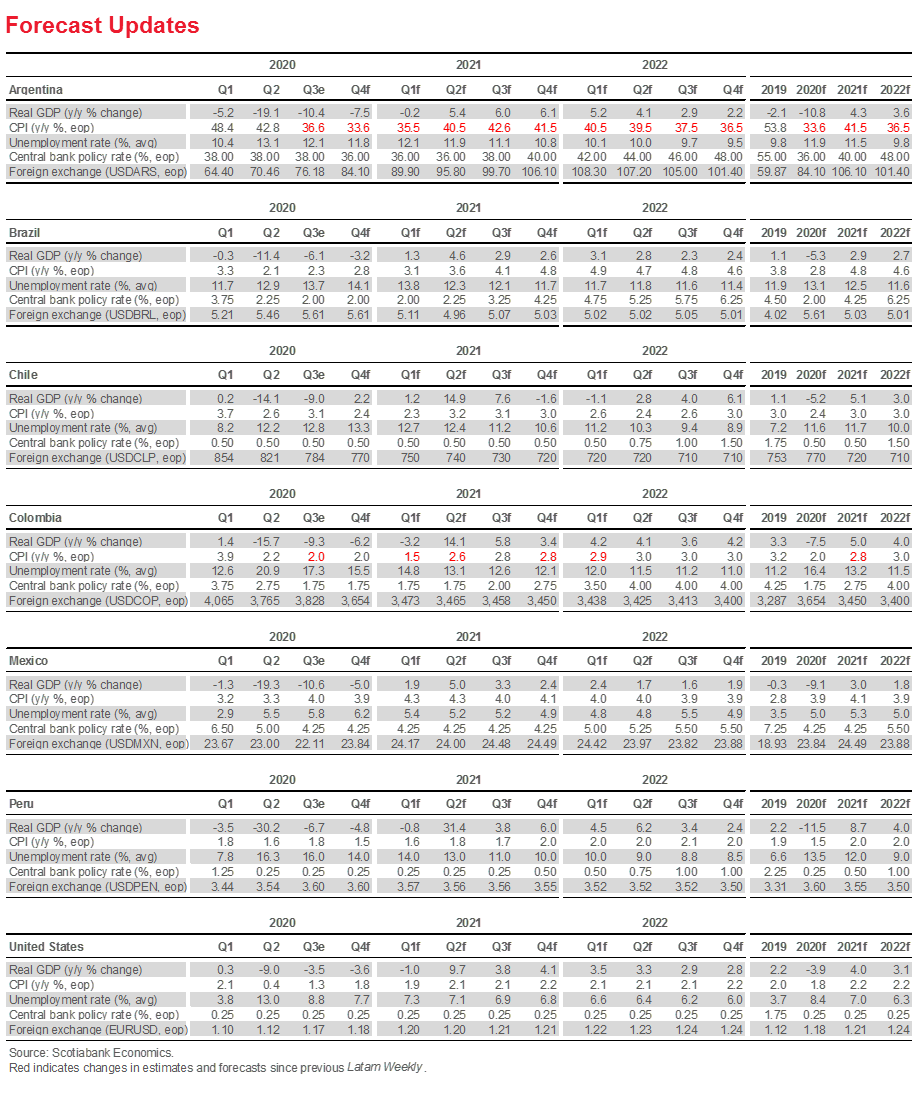

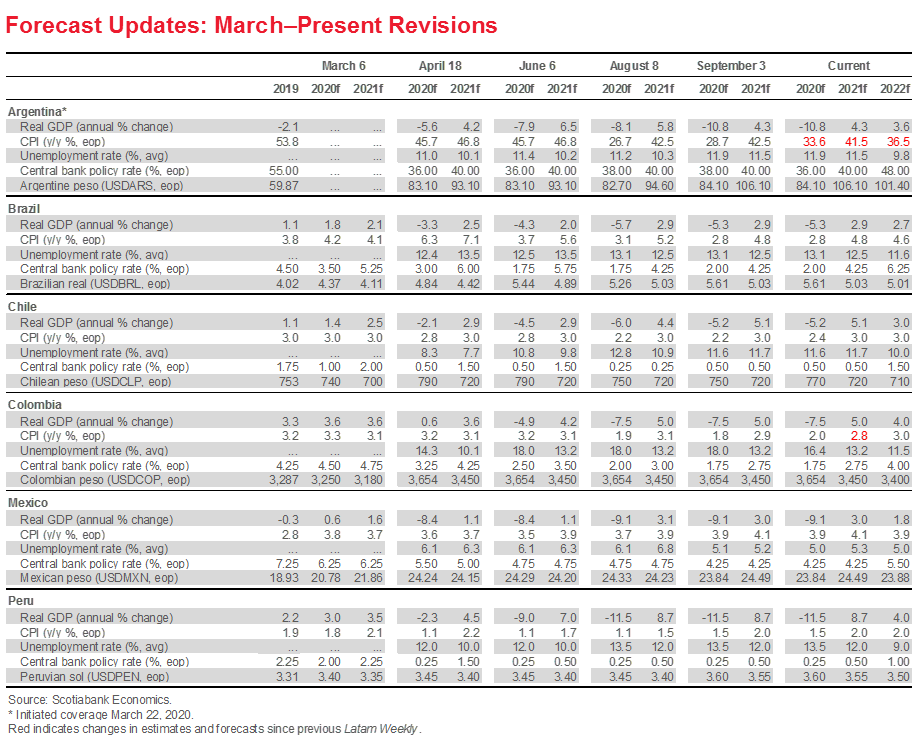

After comprehensive updates at the beginning of October, our forecasts are nearly unchanged in this Latam Weekly. Argentina’s inflation profile has been raised a touch, reflecting an expectation of even more pass-through effects from the weakening peso.

ECONOMIC OVERVIEW

We preview central bank communications due this coming week in Colombia and Brazil, and monetary-policy decisions scheduled for November 12 in Mexico and Peru. We also look at high-frequency data from across the region for signals on the state of the Latam-6’s recoveries.

MARKETS REPORT

We provide a preview of the possible impact of the US elections on FX markets, with a focus on the USD and the Pacific Alliance’s currencies.

COUNTRY UPDATES

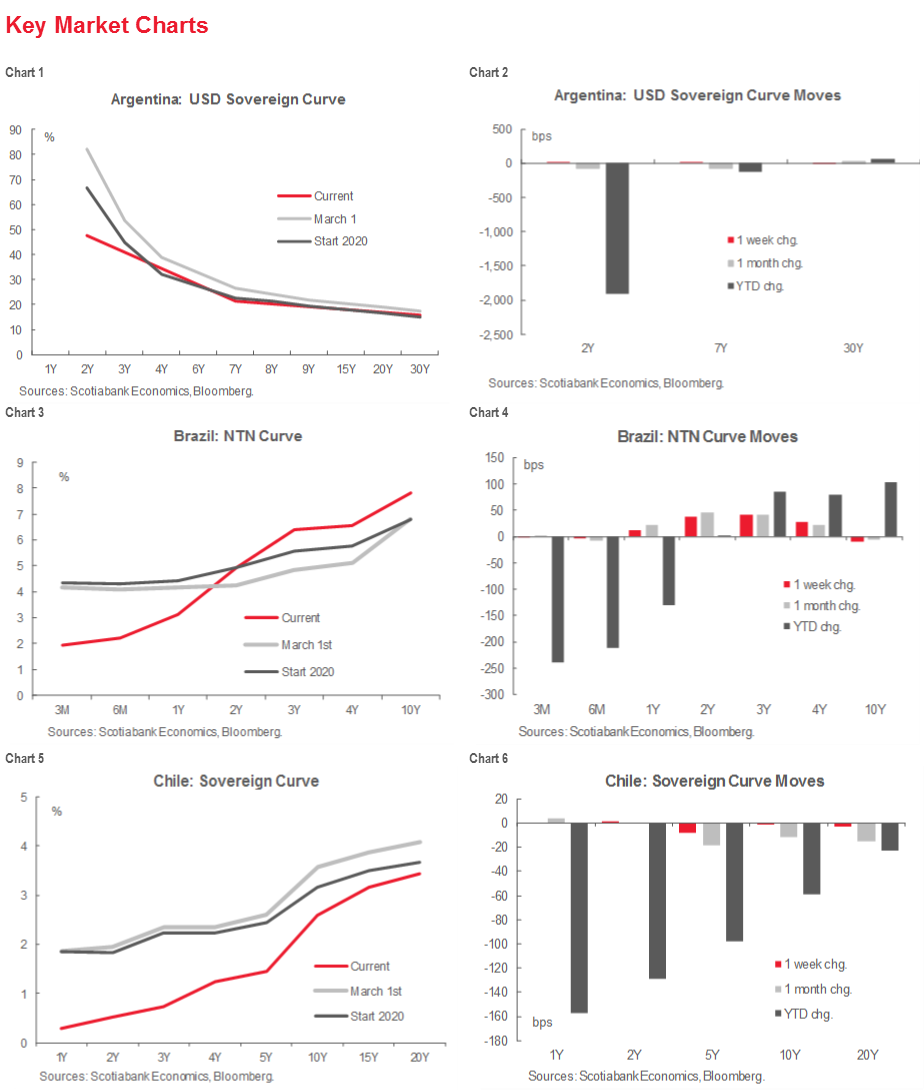

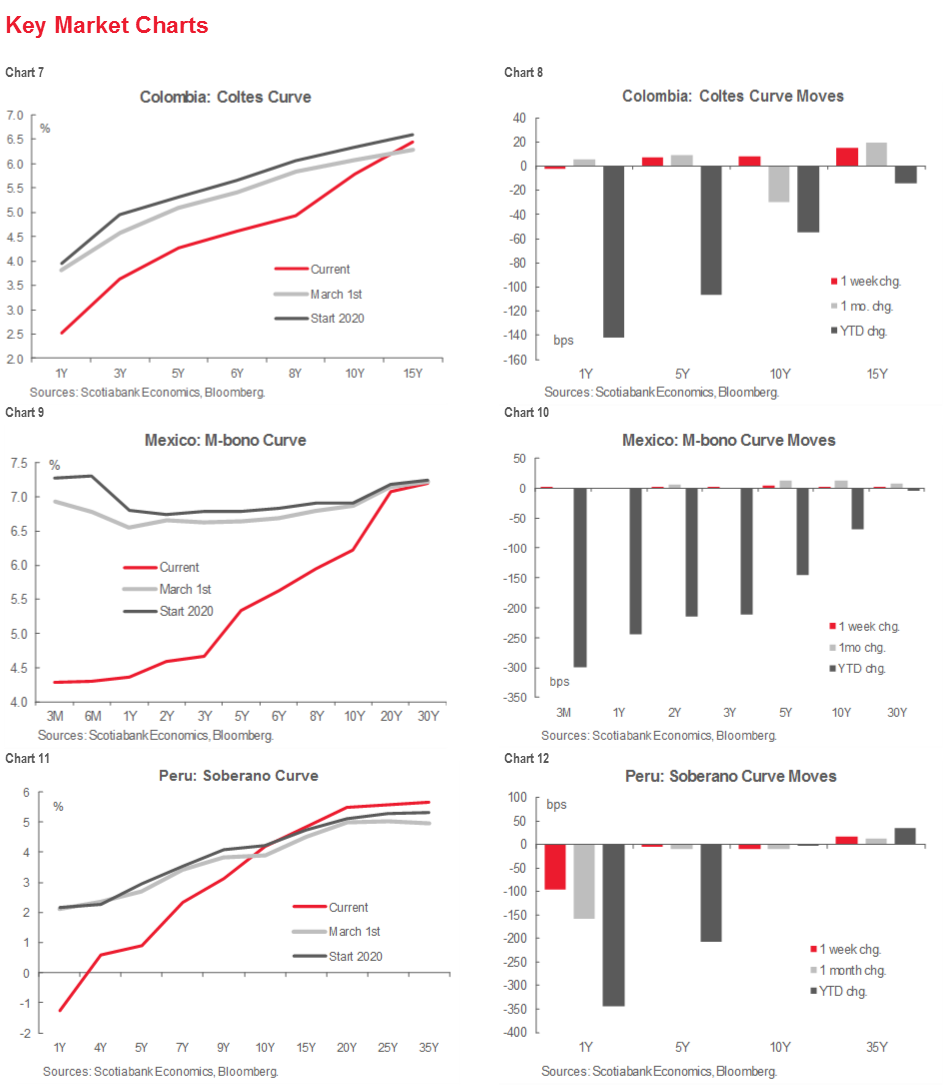

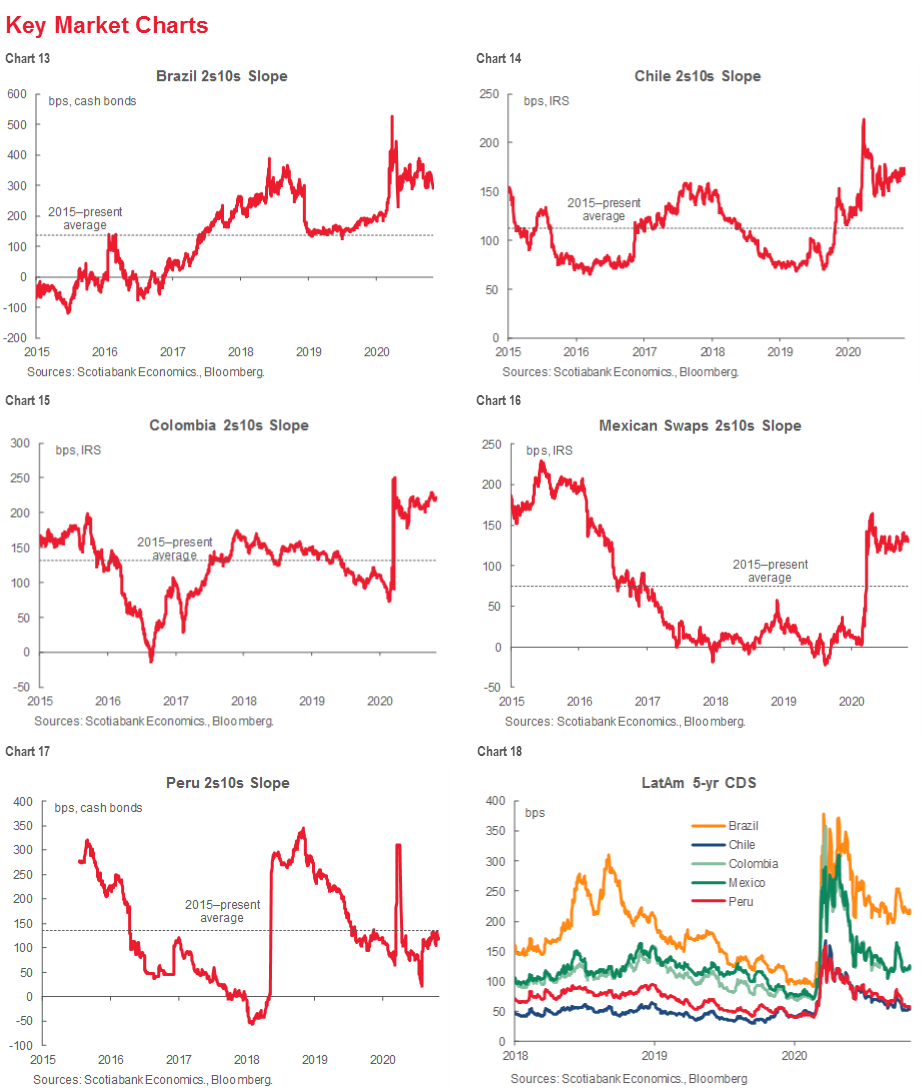

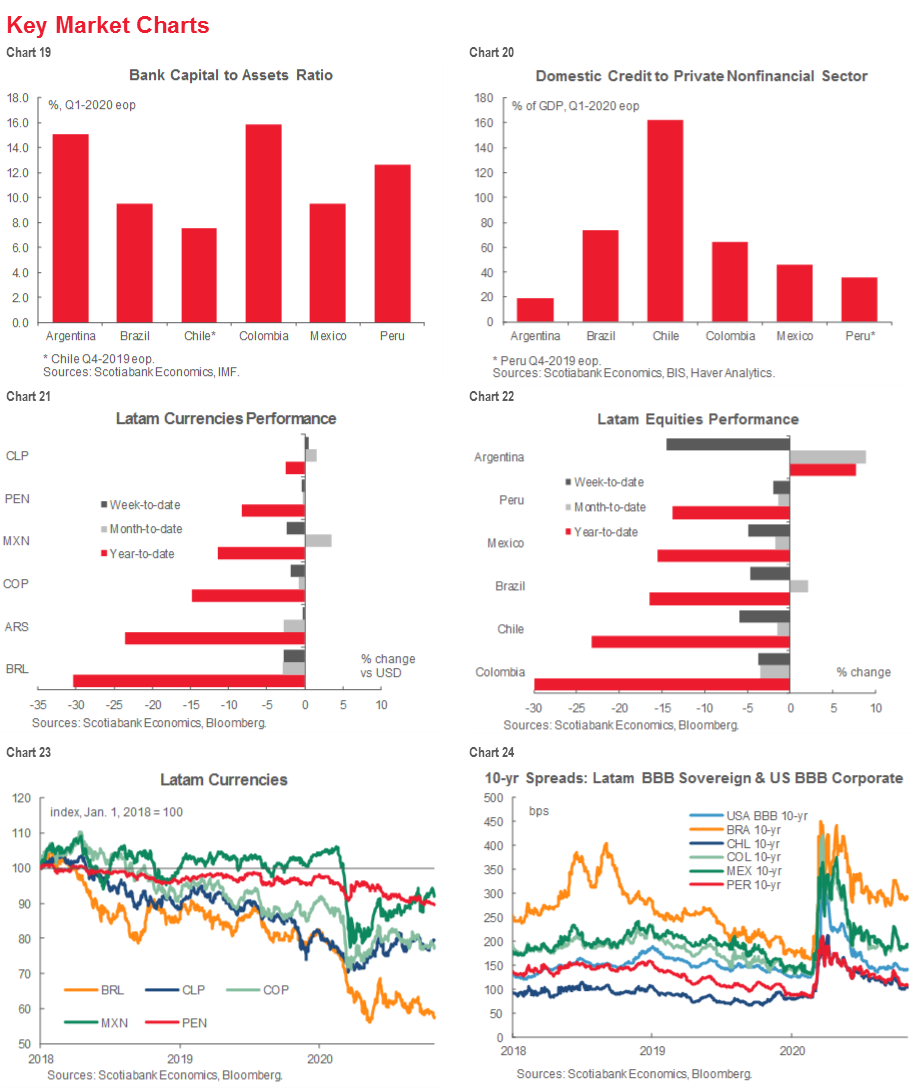

Concise analysis of recent events and guides to the fortnight ahead in the Latam-6: Argentina, Brazil, Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

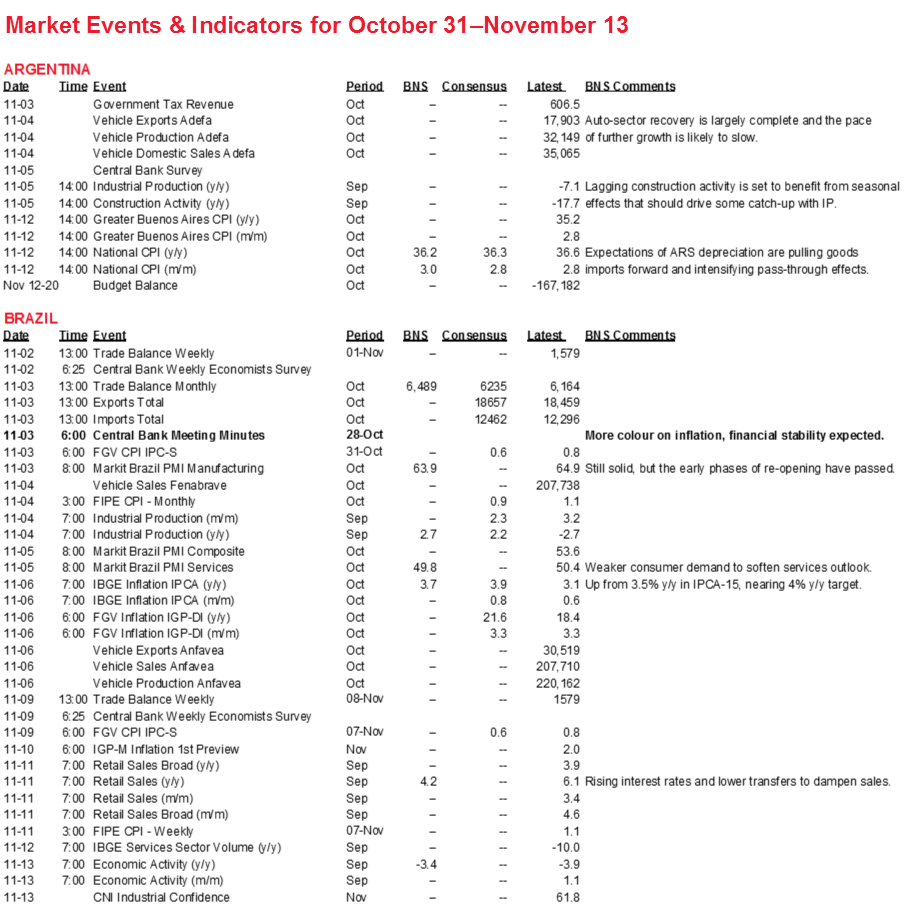

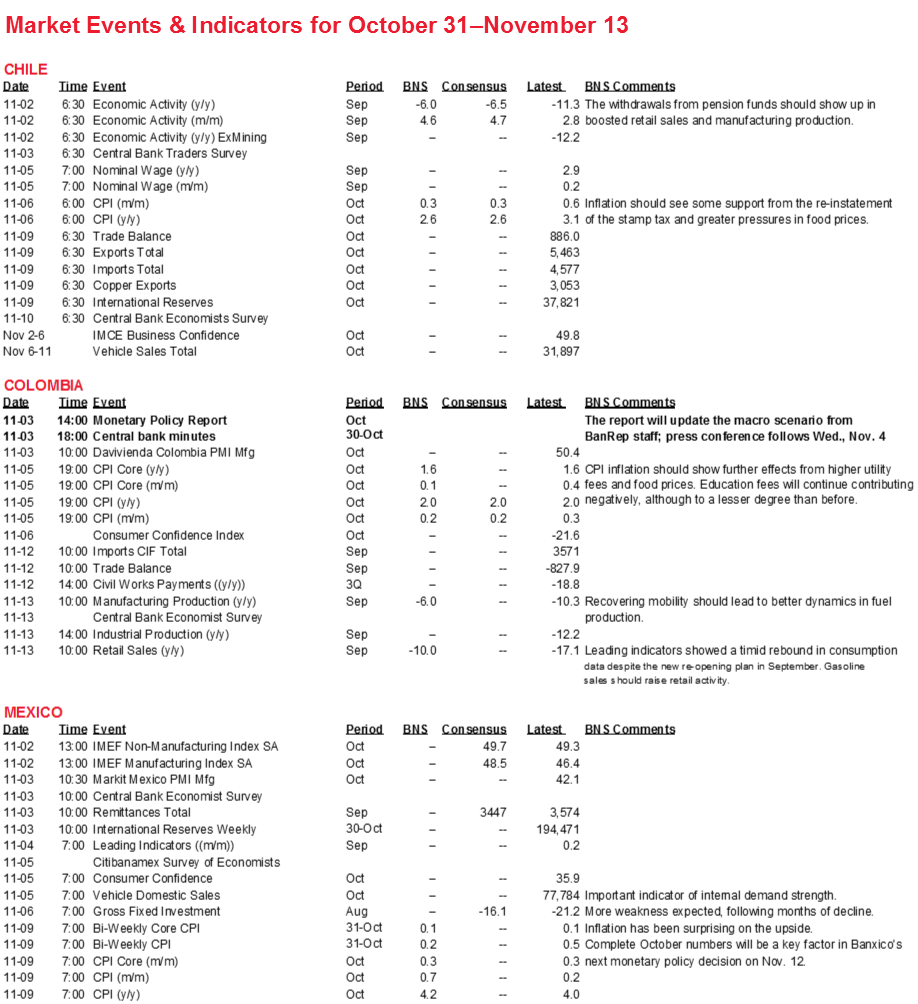

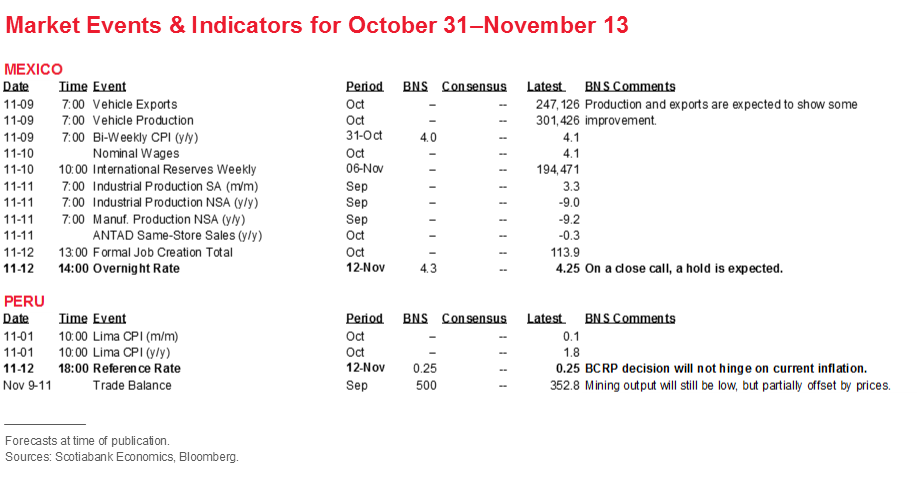

Risk calendar with selected highlights for the period October 31–November 13 across our six major Latam economies.

Economic Overview: Combing Through the Data

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

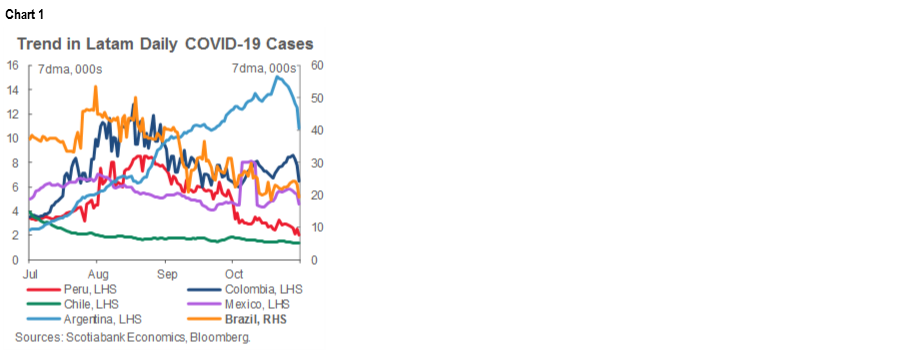

As COVID-19 fears deepened in the most of the world this past week, we saw a rare phase of the pandemic in which Latam’s numbers improved relative to the rest of the world.

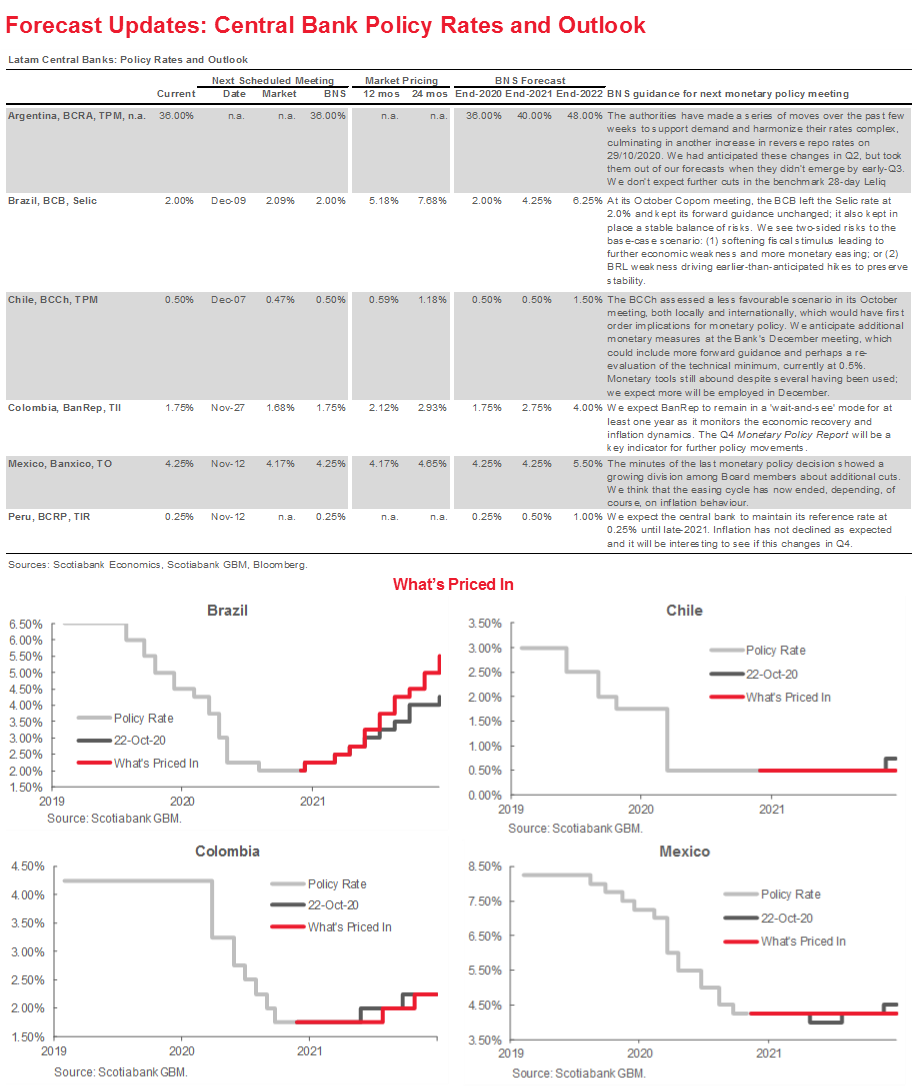

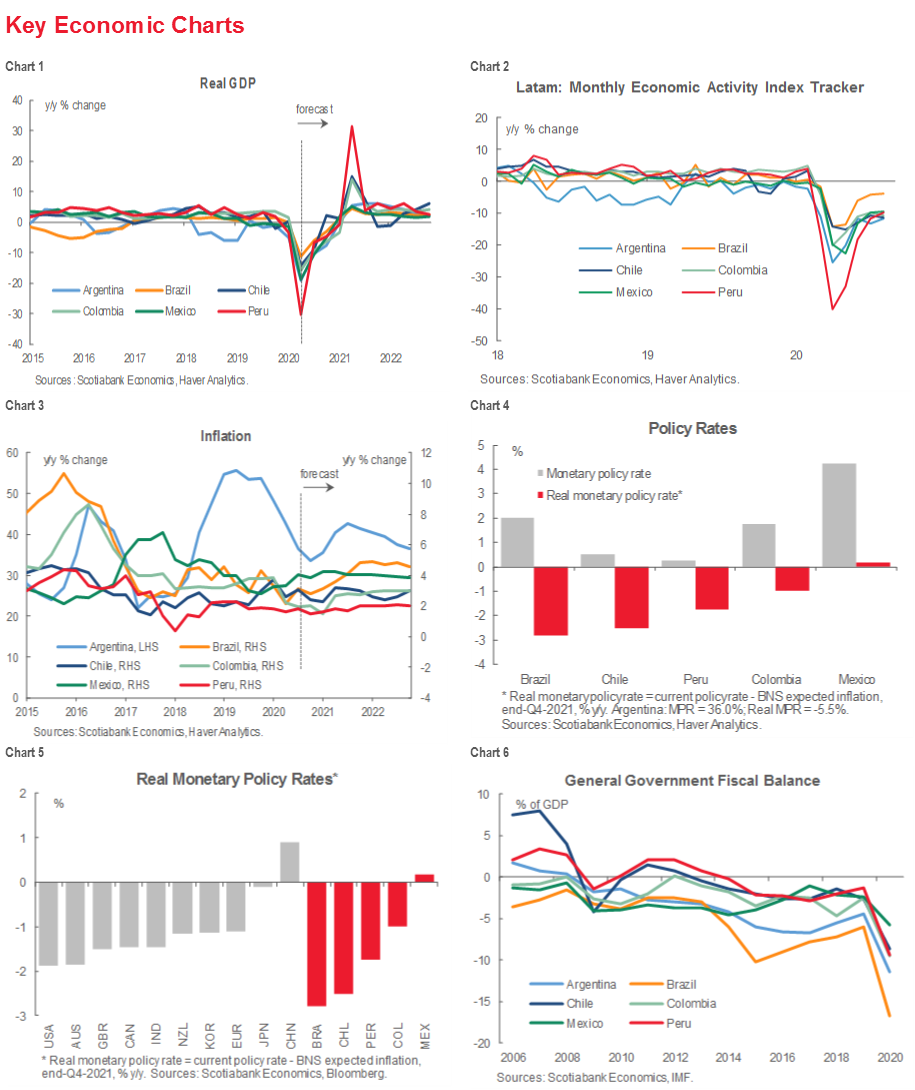

After months of cuts, we think Latam’s central banks are now all in extended holds. Minutes from Colombia’s BanRep and Brazil’s BCB should shed light on considerations for the next few months, while expected holds by Mexico’s Banxico and Peru’s BCRP, both on November 12, should extend this theme.

We look at a range of high-frequency public and proprietary data series to take the measure of the region’s recoveries and to look for signals of what lies ahead.

MARKETS AND COVID-19

During this past week Latam risk assets traded broadly in line with fears concerning rising COVID-19 numbers in Europe and the US that, in many cases, are exceeding the worst periods of the initial waves of Q2-2020. Extensive lockdowns have already begun across Europe and the UK, with more likely to follow in parts of Canada and the US. Latam FX had a tough week (table 1) amidst a broadly-based EM sell-off that has room to carry on further owing to what appears to have been long positioning built over previous weeks. The BRL, MXN, and COP were amongst the worst performers across the entire EM FX complex. Nevertheless, Latam currencies weren’t able to provide a sufficient shock-absorber for the region’s equity markets that also saw strong sell-offs (table 2). In Argentina, the Merval’s drop received a further kick from the authorities’ moves to clamp down on the parallel ARS market.

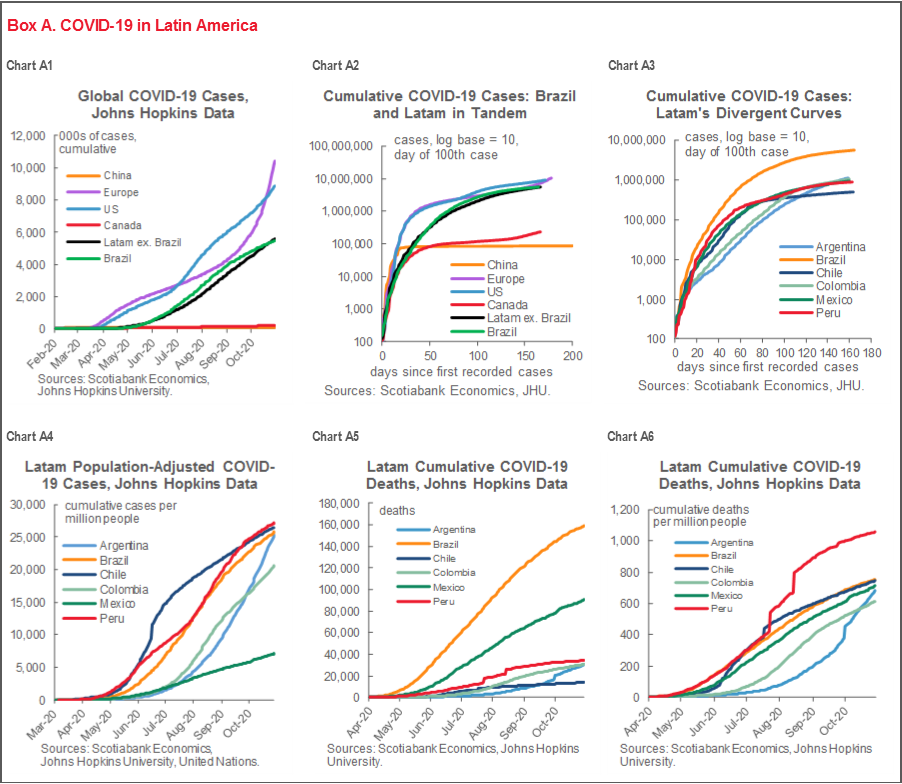

It’s sadly ironic that Latam got swept up in COVID-19-induced risk-off sentiment as even Argentina showed progress over the last two weeks in slowing the contagion (chart 1). With the worsening of the pandemic in Europe, the US, and Canada over the last fortnight, Box A’s charts A1 and A2 paint a rare COVID-19 picture in which Latam has been improving relative to the rest of the world. Still, despite Argentina’s recent success in starting to bend its COVID-19 curve, charts A3 through A6 trace how much its situation has deteriorated over the last two months compared with its regional neighbours. Chart A4’s per capita case numbers also underscore how little testing his happening in Mexico: its exceptionally low cumulative cases per million people—at less than a third of any of its neighbours—appears to be a testament to how few cases are being identified.

For perspective, even after all the economic damage this year has seen, Chile’s copper exports in September inched above their 15-year monthly average—a solid sign that the global economy is bruised, but not broken (chart 2). Dr Copper isn’t ready to write off this patient yet.

FORECASTS: STEADY

After comprehensive updates at the beginning of October, our forecasts are nearly unchanged in this Latam Weekly. We revised our inflation path for Argentina in light of the even stronger-than-expected damage to the ARS in the blue-chip swap market, which is set to intensify pass-through effects, particularly as import demand has stepped up as Argentines scramble to access dollars at the cheaper official rate. We now see sequential inflation averaging 3% m/m over the coming quarters. In contrast, our team in Bogota fine-tuned its inflation outlook, edging end-2021 headline inflation down from 3.0% y/y to 2.8% y/y.

MACRO DATA & CENTRAL BANKS

Inflation dominates macro data across the next two weeks in Latam. Price increases are expected to have picked up during October in Brazil (Nov. 6), Mexico (Nov.9), Argentina (Nov. 12); held steady in Colombia (Nov. 5); and pulled back a bit in Chile (Nov. 6). Peru leads the region’s October inflation prints on Nov. 1, but countervailing forces leave us low conviction on how Lima’s prices evolved in the month. See the Market Events & Indicators risk calendar at the back of this report for more details.

The week ahead sees the arrival of minutes and a quarterly MPR in Colombia, and minutes from Brazil. Rate decisions come the following week, both on November 12, from Mexico’s Banxico and Peru’s BCRP, where holds are expected. Detailed considerations are sketched out below.

Colombia. Following the Board’s unanimous decision to hold the benchmark interbank rate at its record-low of 1.75% at its meeting on Friday, October 30, the BanRep is scheduled to publish the minutes of the meeting on Tuesday, November 3 at 18:00 ET (henceforth moved from 14:00 ET to allow simultaneous releases in Spanish and English) following the release of its latest quarterly Monetary Policy Report at 14:00 ET.

The unanimity of the decision underscored a forward-looking message of rate stability after the 4-3 split decision that resulted in the last -25 bps cut at the previous September 25 meeting. That minority had preferred to keep the policy rate at 2.00%, and the ensuing minutes showed they were driven by concerns about the pandemic and public debt under additional easing.

In the Board’s October 30 statement, members noted that inflation expectations have risen, while fiscal measures, the new re-opening plan, and low interest rates should help the economic recovery. Nevertheless, the Board continued to eschew explicit forward guidance, noting that while the 1.75% policy rate keeps policy “expansive”, it is “prudent to maintain its current posture while waiting for new information on shocks and the evolution of variables that affect policy reactions.”

The minutes may shed some light on the Board’s views on how long it expects to keep its policy rate on hold and the considerations that will dominate its assessment of new developments over the coming months as it remains in data-dependent mode. Our team in Bogota doesn’t expect headline inflation to reach the BanRep’s 3% target until Q4-2021 (see Forecasts Table,

p. 2). Consequently, the first hike from the BanRep is forecast for late-Q3-2021.

Brazil. The BCB will publish the minutes from the October 28 Copom meeting on Tuesday, November 3. The Copom unanimously decided to hold the Selic rate at its record-low of 2.00% for a third meeting in a row.

There had been some cause to think that the Copom might change its tune given that DI yields widened between September 16 and October 28, but at this past Wednesday’s meeting the Copom stood firm on the messages that it has issued a month earlier. It reiterated its forward guidance that it does not “intend” to implement a reduction in the extent of monetary stimulus unless inflation returns to its target, currently 4% y/y, but dropping to 3.75% in December 2021 and 3.50% in December 2022, over the relevant policy horizon. The Copom further noted that it perceives the current level of stimulus as appropriate and that it would not adjust it so long as additional previously identified conditions continue to be met: inflation expectations stay below target for the relevant policy horizon, growth remains subdued, the fiscal stance is unchanged, and longer-term inflation expectations are still anchored.

As a result, the minutes may provide some additional colour on two key issues. First, it will be interesting to see the Copom members’ reflections on the market response to their recent communications. More specifically, it will be particularly insightful to glean any additional detail on the Copom’s discussion of Brazil’s fiscal stance and prospects for adjustment and reform. Second, it will be useful to reset our impression of members’ views on the outlook for inflation after the recent upturn in headline IPCA readings.

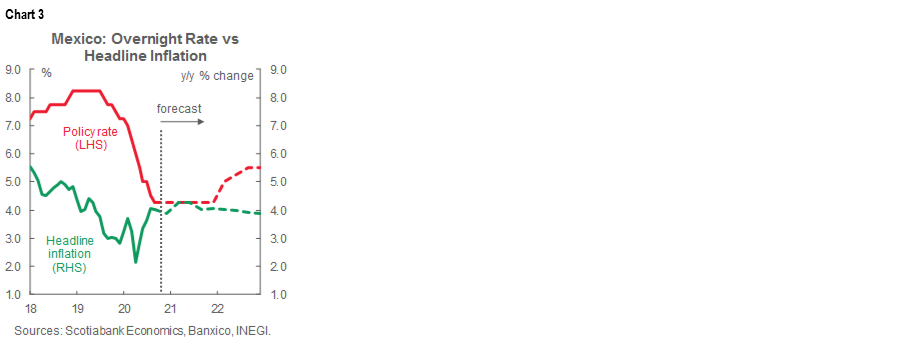

Mexico. The Banxico Board’s next monetary policy meeting is scheduled for Thursday, November 12 and it is expected to be another finely balanced decision. In a close call, our team in Mexico City expects the Board to hold the target rate at 4.25%, thereby ending its easing cycle (chart 3).

At its last rate meeting on September 24, the Board voted unanimously to cut its target rate for an eleventh time, by -25 bps to the current 4.25%, for a total of -400 bps in easing this cycle. Although in line with consensus, analysts had expected a divided Board owing to risks from inflation, growth, and financial markets. In its statement, the Board emphasized three key points: (1) the balance of risks for inflation remains uncertain, but the Board anticipated that headline and core inflation will stay around 3% y/y over the next 12 to 21 months; (2) the balance of risks to growth is skewed downward, a point on which our forecasts concur (see tables on pp. 2 and 3); and (3) global economic activity is recovering, but advanced-economy central banks are likely to keep their policy stances accommodative.

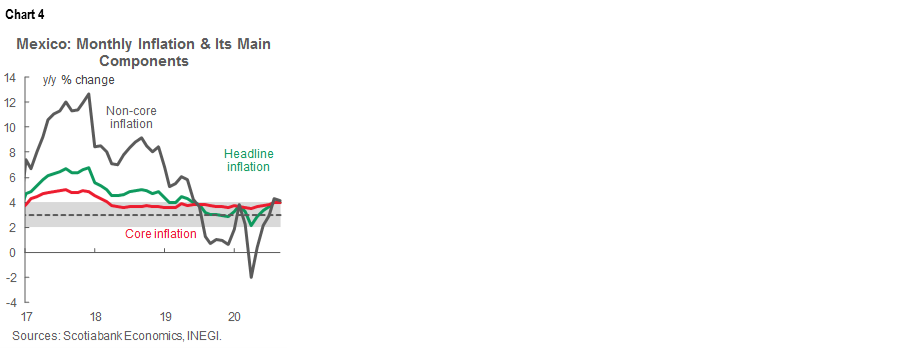

In the meeting’s minutes, published on October 8, we saw evidence of more varied views than was suggested by the Board’s unanimous vote. In fact, it appears that three of the Board’s five members noted at least some equivocations on the need for another cut in the reference rate. With inflation still above the 4% upper bound of Banxico’s target range (chart 4), we expect the Board to keep its benchmark policy rate unchanged at its November 12 meeting.

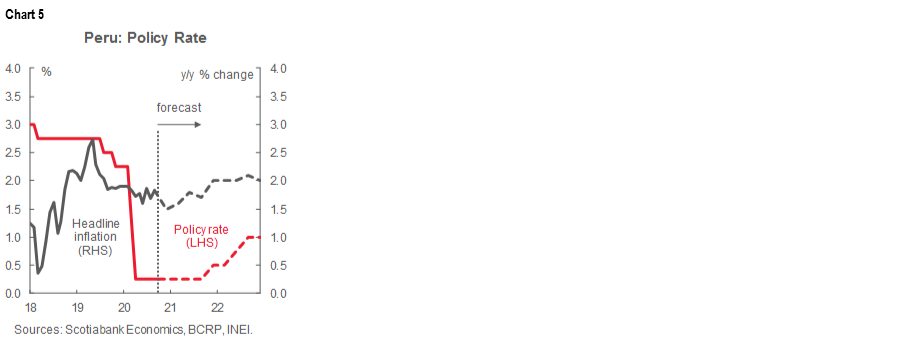

Peru. The BCRP’s Board is next scheduled to meet on monetary policy on Thursday, November 12, and along with what is likely to be a unanimous view amongst analysts, we expect the headline policy rate to be held at 0.25%, where it has been since early April (chart 5).

In the statement from its October 7 meeting, the Board’s main messages remained unchanged from previous meetings. It held to its commitment to maintain its expansive monetary stance for a “prolonged” period of time with a bias toward the implementation of greater stimulus, if it were to become necessary, through measures other than further cuts in the policy rate. That said, our team in Lima does not have the impression that the BCRP is preparing new instruments. Instead, the Bank is focused on providing liquidity through existing channels and managing PEN volatility, some of which is being driven by intermittent political strife between Congress and the Executive.

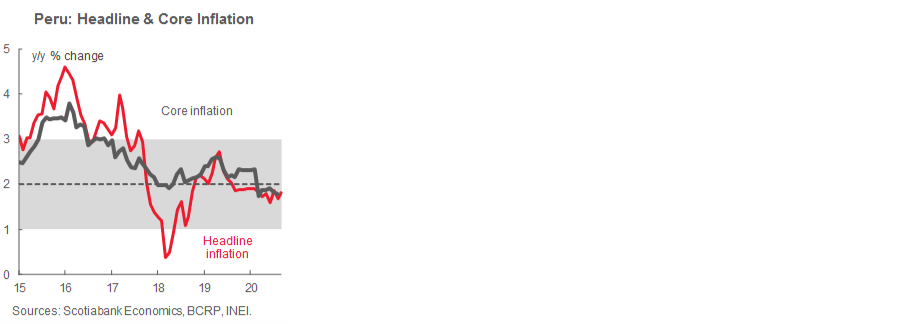

October’s inflation reading, out on November 1, will be the key remaining input for the BCRP. October prices should determine whether inflation will come down into the end of the year in line with weak domestic demand, as both we and the BCRP expect, or whether weaker-than-projected disinflationary forces allow it to remain around September’s 1.8% y/y level.

CHARTING THE REGION’S RECOVERIES

Since March, we’ve periodically reviewed a range of high-frequency and non-standard public and proprietary indicators to chart the economic impact of the pandemic in Latam as closely to real time as possible. Here, we bring together a collection of our favourite cross-country touchpoints to generate a fresh mosaic of Latam’s still progressing recoveries.

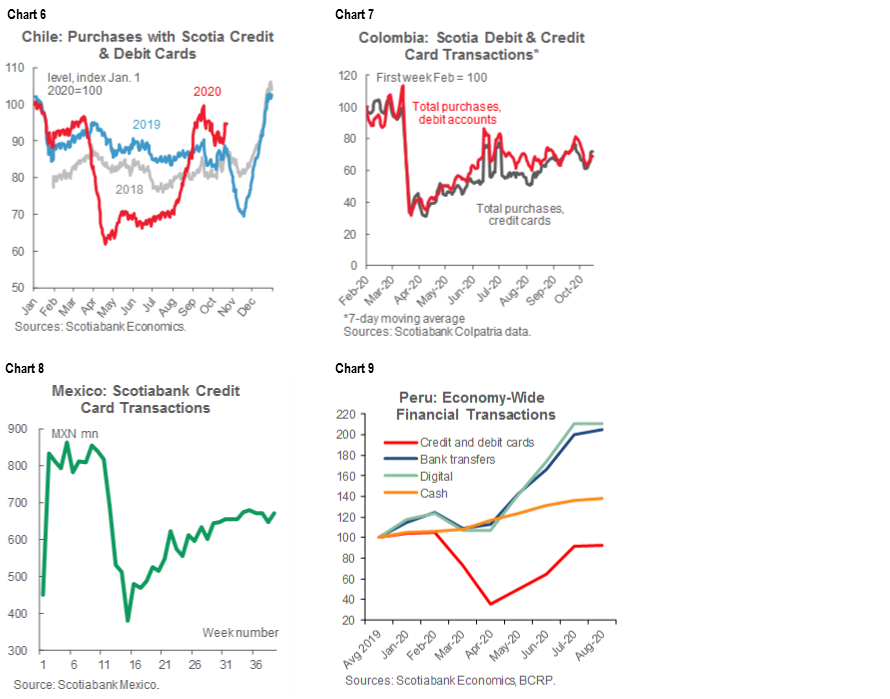

Transactions volumes. Looking at Scotia proprietary data, credit and debit volumes at current at 95% of their January 2020 levels in Chile (chart 6), 6.9% higher than in October 2019 during the civil unrest, owing in part to fiscal stimulus and pension withdrawals. In Colombia, VAT holidays spiked Scotia card transactions in June and July, but volumes currently stand at 69% of February levels (chart 7). Scotiabank Mexico’s card weekly card volumes were at 78% of February’s numbers as of end-September (chart 8). Meanwhile, in Peru, the accelerated re-opening has lifted finance-system-wide card transactions to 93% of average volumes in 2019 (chart 9), while wire and digital transfers are up 205% and 210%, respectively, over 2019’s averages.

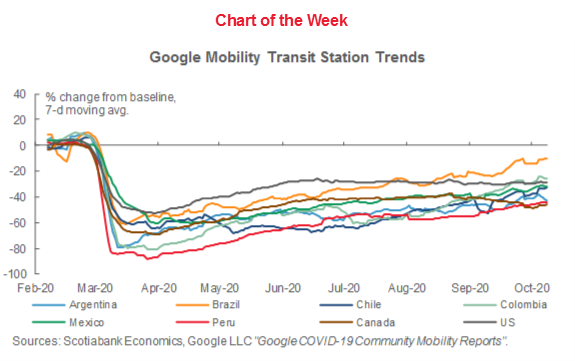

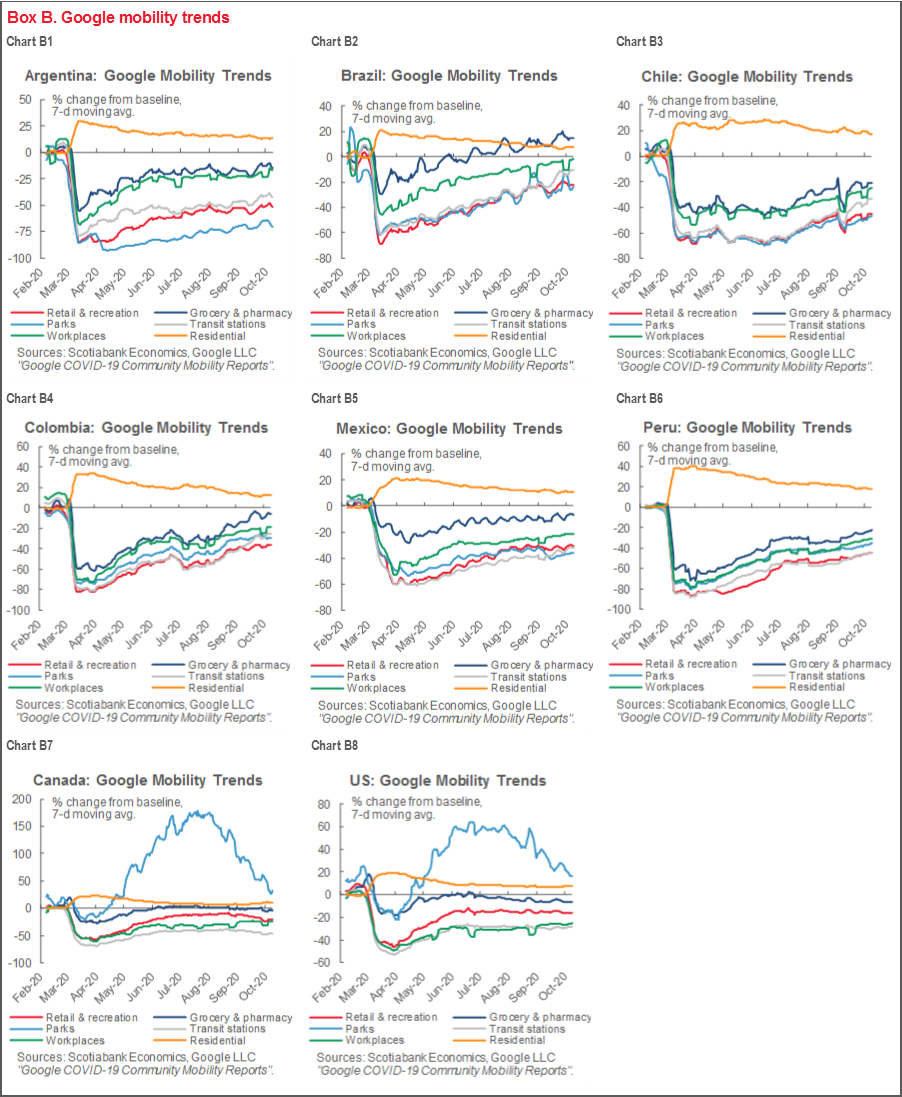

Mobility trends. According to Google mobility data, Latam transit usage to October 23 was down -31% compared with the region’s early-2020 averages (chart of the week, p. 1), better than Canada (off -46%) and only a shade weaker than the US (down -29%). Visits to grocery stores were, on average, down -9% in Latam versus the start of the year (chart 10), again only a bit softer than Canada (-3%) and the US (-7%). Brazil is the outlier, where spotty contagion control measures and loosened lockdowns mean grocery-store visits are up 15%. Detailed individual country mobility data are provided in box B for the Latam-6, plus Canada and the US. While Canadians and Americans have balanced more time at home with many more visits to parks (chart B7 and B8), a trend that has tapered off only as autumn has arrived, Latin American park visits are still down by an average of -40% compared with the beginning of the year. Perhaps this will change as summer arrives in the southern hemisphere, but it points to a possible unexploited avenue by which social cohesion could be enhanced if and as lockdowns are extended.

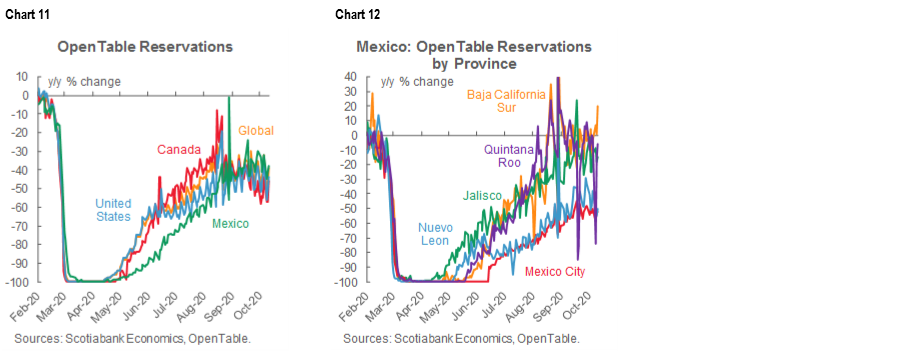

Open table reservations. As of October 28, Mexican OpenTable bookings were down -38% y/y while global bookings were down -39% y/y, with a -46% y/y drop in Canada and a -44% y/y decline in the US (chart 11). Mexico’s numbers were helped by tourist zones that have seen reservations firm up: while Mexico City and Nuevo Leon (Monterrey) were both off by about -50% y/y, tourists looking for a break from quarantines lifted reservations by 20% y/y in Baja (Cabo San Lucas), and held reservations to declines of only -15% y/y in Jalisco (Puerto Vallarta) and -6% y/y in Quintana Roo (Cancun), as shown in chart 12.

Power. Argentina energy demand was down only -1.4% y/y at end-September (Box C, chart C1). Brazil power demand was actually up 3.9% y/y in late-October (chart C2), while Mexican demand was down only -0.3% y/y (chart C5). Compared with early-2020, Colombia energy demand is down -5.2% (chart C4) and Peruvian demand is off about.-3.9% (chart C6). Chile’s year-on-year comparison is complicated by 2019’s social unrest, but power demand in late-October was 8% higher than in the 2012–18 average for the same month. See box C for detailed individual country charts.

Markets Report: US Election Preview—Potential Impact in FX markets

Tania Escobedo Jacob, Associate Director

212.225.6256 (New York)

Latam Macro Strategy

tania.escobedojacob@scotiabank.com

Shaun Osborne, MD & Chief Currency Strategist

416.945.4538

Foreign Exchange Strategy

shaun.osborne@scotiabank.com

With contributions from Brett House.

Price action in currency markets over the next week—and possibly beyond—will be heavily dependent on developments around the Tuesday, November 3 elections in the US.

We believe that the USD is at risk of broadly weakening in the case of a Biden victory while it may initially strengthen on a Trump second term before resuming a downward trajectory.

From a medium-term perspective, a Biden presidency would mean a more amenable stance toward additional fiscal stimulus.

For Latin America, the relationship between the US and the Pacific Alliance (Chile, Colombia, Mexico, & Peru) does not seem to be subject to material changes under either presidential candidate.

In an environment that is broadly favourable for EM assets, we see more value in MXN and COP, while we would be more neutral in CLP and PEN, where we think there is a local bias for higher political and credit premiums in the medium term.

USD: CHANNELLING THE US ELECTIONS

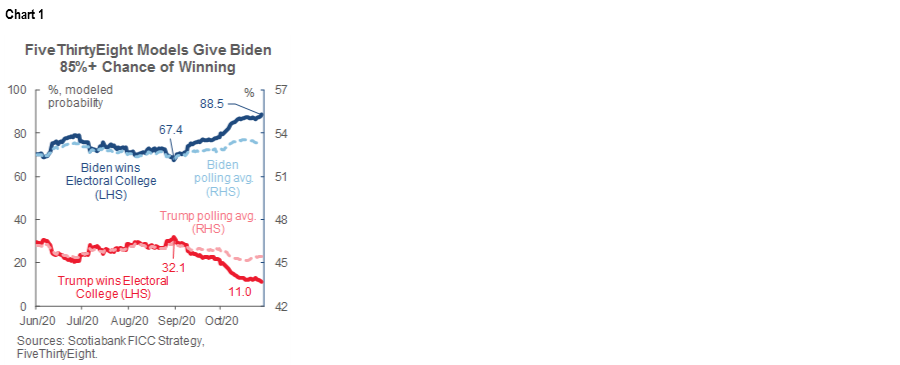

Price action in currency markets over the next week—and possibly beyond—will be heavily dependent on developments around the November 3 elections in the US. Barring declaration of a clear victory on election night (or soon thereafter) for either candidate, the USD looks set to maintain a better-bid tone. Election polls and models give former Vice-President Biden a clear lead over President Trump (chart 1), yet markets remain on edge owing to a possible repeat of former Sen. Clinton’s surprising defeat in 2016. In addition, the record-breaking number of early voters implies that there could be delays in vote counts that may mean a winner is not declared for weeks.

Beyond the election, we believe that the USD is at risk of broadly weakening in the case of a Biden victory while it may initially strengthen on a Trump second term before resuming a downward trajectory. A clear win for former VP Biden would confirm the market’s tilt toward this scenario and take off the table the lingering veil of risk-aversion that remains owing to the comparatively slight odds of a Trump victory.

From a medium-term perspective, a Biden presidency would likely mean a more amenable stance toward additional fiscal stimulus. However, Democratic control of both houses of Congress would be imperative for the passage of a new aid bill that would respond to climbing COVID-19 numbers and provide support to risk assets. In a scenario where the Democrats fail to take control of the Senate, the USD should still continue on a weakening path as the global economic backdrop gradually improves—but without the additional risk-on boost from fiscal aid.

If Trump is declared the victor, the USD is liable to strengthen as the odds of a sizable stimulus package fade in relation to a Biden win. The USD would also catch a bid from risk-off fears that a re-elected Pres. Trump may be emboldened in his protectionist pursuits. Republicans have resisted calls for a large aid package as they pivot to a more fiscally conservative stance. Given the close link between the Canadian and US economies, the CAD is likely to under-perform its key peers amid an ensuing softer economic outlook in the US and Canada. Trade tensions with China would continue while the White House turns its protectionist cannons against the European Union, which would threaten the EUR. The ratification of the USMCA may provide the MXN and CAD some insulation against new bilateral trade scuffles, but the Trump Administration’s re-imposition of steel and aluminum tariffs on Canada in August 2020 implies that trade deals with the US are no longer checks on the whims of the White House.

IMPLICATIONS OF THE US ELECTION FOR PACIFIC ALLIANCE FX

The relationship between the US and the Pacific Alliance (Mexico, Colombia, Chile and Peru) does not seem to be subject to material changes if either presidential candidate succeeds in his bid for office. Hence, we think Latam assets will move in line with broad risk appetite and the USD trends described under the scenarios above.

Markets, however, have a fresh memory of what happened to Mexican assets during and following the 2016 US elections, when the Mexican peso lost 30% from its highest level that year to the weakest point reached just after the US Presidential inauguration ceremony in January 2017. MXN was by far the worst performing EM currency during that period and has carried that additional risk premium persistently since then (chart 2). The spike in volatility seen in MXN going into and during the aftermath of the 2016 US elections also exceeded that of its peers (chart 3), which resulted in a decision by the Banco de Mexico to intervene directly in the market by selling USD spot and by participating in the NDF market for the first time in its history (see here for Banxico’s announcements).

As we approach the US presidential election on November 3, concerns about what could happen to the Mexican currency this time around have emerged, keeping investors on the sidelines. We think that the 2016 presidential run was very specific in terms of the content of the Republican campaign and what it put at stake regarding commercial and immigration ties between Mexico and the US. The fact that the final result of the election was not clearly anticipated by the polls made the market reaction more abrupt, especially for Mexican assets.

But things have changed since 2016 and the effects of the US campaign and election on the MXN will likely be less violent and closer to what we saw in previous elections (see our detailed analysis of the peso’s reaction to past US votes in the September 5 edition of the Latam Weekly here). Key reasons why 2020 is not 2016 redux include:

- One of the most feared potential outcomes of the 2016 election—the disintegration of NAFTA—has been avoided and a new trade agreement, the USMCA, has been approved by the three countries;

- On immigration, diplomatic negotiations seem to have reached an equilibrium, with Mexico taking some additional measures to contain flows of people within its borders;

- The Mexican Administration has set as a priority the maintenance of a close and healthy diplomatic relationship with the US and has, so far, ignored most US statements on controversial topics, such as the border wall; and

- Former Vice-President Biden’s campaign platform is, in our view, less likely to create an environment of confrontation with Mexico. Instead, it is likely to focus more on domestic issues such as the health care system, income re-distribution, and clean energy infrastructure.

With less of an MXN-specific shock expected in this election, we think the currency should behave more in line with overall risk sentiment. With markets focusing intently on the battle for the White House (and Congress), uncertainty may provide the USD with a little support. In the longer run, however, broader global economic and monetary policy settings are likely to have more influence on the USD’s direction than who wins the election. In short, we think the USD may benefit somewhat from precautionary positions ahead of the election—even more so considering the accumulation of USD short positions in recent weeks—but that, in the end, the excess liquidity available in the global financial system will remain a strong support for risk assets, including EM currencies, over a longer horizon.

In an environment that is broadly favourable for EM assets, we tactically see more relative value in MXN and COP and would be more neutral regarding CLP and PEN where we think there is a local bias for higher political and credit premiums in the medium term. We should note that our Strategy team’s relative tactical view in favour of the MXN is at odds with the macro fundamentals-based depreciation in the Mexican peso forecast by Scotiabank Economics’ team in Mexico City (see forecast tables on pp. 2 and 3). While we have a clear consensus on the current state of and prospects for the Mexican economy, our Strategy team sees signs that this relatively tough outlook is largely priced into the MXN and that we may see some episodic bouts of relative peso strength.

COUNTRY UPDATES

Argentina—Talks Isn’t Cheap Anymore

Brett House, VP & Deputy Chief Economist

416.863.7463

brett.house@scotiabank.com

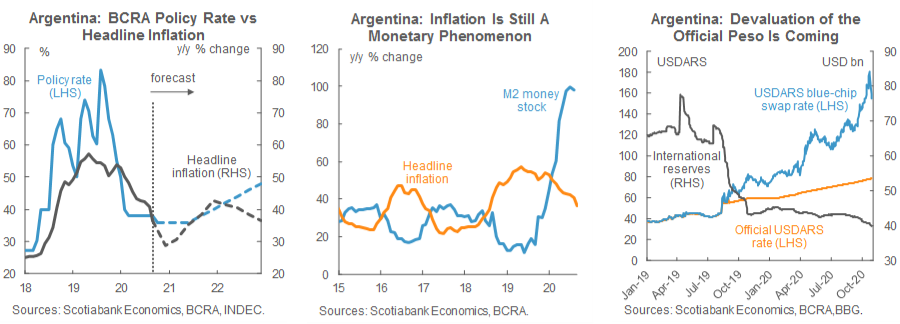

On Thursday, October 29, the BCRA once again raised its reverse repo rates for the third time in the last few weeks, increasing the 1-day rate from 30% to 31%, and lifting the 7-day rate from 33% to 34.5%; it kept the benchmark 28-Leliq rate on hold at 36.00% after two 100 bps cuts concurrent with earlier adjustments to the reverse repo rates. The moves bring the BCRA’s complex of policy rates more closely into alignment and raise the potential return on ARS-denominated deposits. The authorities continue to hope that this will boost demand for pesos, but it’s hard to see this happening when real rates are low to support economic activity (first chart), the monetary base is set to push inflation up (second chart), and the parallel FX market implies that a devaluation of the official ARS is inevitable (third chart).

Efforts by the authorities this past week to get local brokerages to limit trades in the blue-chip swap market aren’t likely to have a lasting effect; instead, they’ll fuel ongoing demand for dollars in the coming weeks. Former Economy Minister Domingo Cavallo argued in an interview Friday, October 30, that unification of the peso markets would be unproductive and that a devaluation was “unnecessary”. He proposed that the official market should be reserved for “essential” commercial activity while the parallel market could be allowed to float. It’s hard to see how this would bring about anything other than a crowding out of the official market and only slightly delay a devaluation that is coming anyway.

In other magical economic thinking, Argentina’s IMF Executive Director, Sergio Chodos, this week contended that a simple rollover of the country’s USD 44 bn outstanding to the IMF “remains the base case for negotiations”, but he conceded that “a slightly different program size could come up”. As we’ve noted in previous reports, the economy is so far off-track from the projections in the IMF’s March 2020 DSA that a larger arrangement is now a given—which can only make the Fund negotiations tougher than they were already set to be.

The fortnight ahead is dominated by real-economy data for the auto sector in October (Wednesday, Nov. 4) followed by industrial production and construction activity (Thursday, Nov. 5) numbers for September; but the bigger attention-getter will be October inflation, out on Thursday, November 12. After a 2.84% m/m print in September, we expect inflation stay around 3.00% m/m through the end of the year and into 2021, higher than the 2.50% m/m average we previously forecast for Q4-2020. This would bring year-end inflation in at 33.63% y/y, nearly 5 ppts higher than the 28.70% y/y we forecast in our October 18 Latam Weekly and Global Forecast Tables. We project monthly inflation to persist around this rate through to Q3-2020 before beginning to slow when, we hope, stabilization measures begin to be taken under a credible IMF-supported adjusted program.

Brazil—Rising Interest Rates and Softening Government Support Could Take Some Wind out of Consumers’ Sails

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

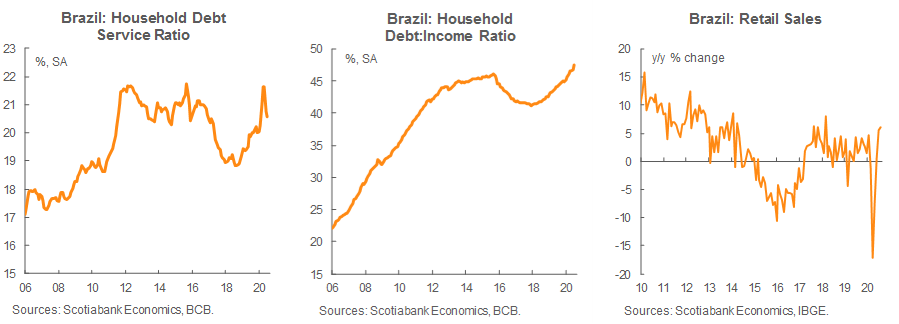

Over the last few months, we’ve been surprised by the speed of the recovery in Brazilian consumer demand, likely because we underestimated local governments’ capacity to deploy effectively fiscal stimulus to offset the COVID-19 shock. In short, state and municipal governments in many parts of the country stepped in to supplement the federal government’s efforts and to fill gaps. The BCB’s aggressive rate-cutting cycle has also helped to support household demand. The decline in local interest rates freed up about 100 bps of consumers’ disposable income in mid-2020 as the debt-service ratio fell from 21.6% to 20.6% (first chart). Importantly, this drop in consumer debt service burdens came at a time when the ratio of household debt to income has been rising (second chart). In the event, the short average reset time of Brazilian household debt, combined with aggressive Selic rate cuts, has given consumers a boost through better cash flow and more disposable income, a boost that they have deployed.

In this regard, the BCB Copom’s pledge in its forward guidance to keep rates low for a prolonged period could help soften the blow to consumers from declining government support measures, which we are set to see taper progressively more quickly through Q4-2020 and into 2021. However, if—contrary to the BCB’s signals—domestic market rates continue to rise as they have been doing (2-year DI rates are up about 100 bps since September), domestic consumption should soften as 2020 draws to a close. Rising interest rates are an especially important consideration in the outlook for consumer demand given Brazil’s rising household debt-to-income ratio.

As of August, retail sales were not only recovering strongly from the COVID-19 shock, they were up 6.1% on a year-on-year basis (third chart). However, we expect a bit of a softening from September onwards owing to a combination of two events: (1) the gradual reduction of the government’s cash transfers to households, and (2) rising market interest rates. We don’t expect spending to fall off a cliff, but we do anticipate that the combination of these two factors will lead to a softer retail sales print for September, which we project at 4.2% y/y, down from 6.1% y/y in August.

As the year gets closer to its end, we are increasingly concerned that external demand could slow due to the re-introduction of tougher social distancing measures in Europe and elsewhere due to the spike in COVID-19 cases, but it is still early to quantify how serious this potential new headwind will be. For now, we are holding off on making any forecast revisions. We look forward to the BCB Copom’s minutes from its October 28 meeting, scheduled to arrive on Tuesday, November 3, for more colour on its assessment of the economic outlook. We expect October manufacturing and services PMIs to pull back a bit from solid September prints. Meanwhile, headline inflation is forecast to accelerate from 3.1% y/y in September to 3.7% y/y in October, just below the current 4% y/y target that is set to be reduced to 3.75% y/y in December.

Chile—A Fragile Recovery; Employment Improves, but Still has a Wide Gap to Close

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

Chile just passed a busy week in terms of political developments and economic releases. In the plebiscite held on Sunday, October 25, Chile’s citizens approved by wide margins a re-write of the country’s 1980 constitution through a popularly elected assembly. The relatively high participation rate at 50.9% was a pleasant surprise. Preliminarily, it appears that there was strong turnout amongst first-time voters, which implies an increased interest in politics among young people. Among the 78% who chose to reform the constitution and the 79% who voted to do so through a 100%-elected convention, a wide diversity of views and groups are represented. This indicates that the election of members to the Constitutional Assembly on April 11, 2021 will be critical in determining whether there is likely to be a set of coalitions that would allow the Convention to reach the two-thirds majority required to approve a new constitutional draft and send it to voters for review in a mandatory plebiscite in early-2022. If the draft receives more than 50% of votes in the 2022 poll, it would become Chile’s new constitution; if not, the 1980 constitution would remain valid. All in all, the streets should be dramatically calmer in the coming weeks, although some small groups of protesters may continue to raise proposals for inclusion in the drafting of the new constitution in public demonstrations.

On Tuesday, October 27, the proposal for a second withdrawal of pension funds was approved in the Constitutional Committee of the Chamber of Deputies. Following this endorsement, the bill must be discussed by the entire Chamber of Deputies. If it is approved there, then later it will have to be ratified by the Senate in order to become law. The Government has expressed its opposition to this bill, arguing that it would reduce future pensions, on average, by 23%. It is estimated that about 2 million people withdrew all of their funds from the pension system under the first window a few months ago; this second withdrawal would leave a total of about 4 million people without pension funds.

In the central bank’s minutes, released on Friday, October 30, which correspond to the meeting of October 15, the Board recognized a less favourable economic scenario since the last monetary policy meeting. Although fiscal support and the withdrawal of funds from the AFPs generated a positive impact on private consumption, their effects were temporary and have not generated relevant traction in job creation. Demand for loans has begun a gradual slowdown in all its segments; growth in the external sector, which showed signs of recovery in September, has started to slow down again with very weak imports; additionally, job creation has been timid, while wages account for still extremely weak domestic demand. We anticipate additional monetary stimulus measures at the central bank’s next meeting in December. These new measures could take the form of more stimulative forward guidance on the policy horizon and could even lead the BCCh to re-evaluate the “technical minimum” level of the monetary policy rate.

In employment data released on Friday, October 30, the unemployment rate stood at 12.3% in the quarter between July and September, down from the 12.9% result in the previous moving quarter. The decline was explained by a somewhat greater improvement in employment than in the size of the labour force. However, this phenomenon should be reversed in the coming months when a greater inflow to the workforce begins. This would keep the unemployment rate high (above 10%) for several quarters, unless employment begins to gain traction along with more investment. For now, we do not see things going this way, as investment is recovering slowly and job creation remains relatively insufficient for the size of the employment gap.

The fortnight ahead will bring some important data and events. First, on Monday, November 2, we will receive the monthly GDP data for September. After the sectoral data released on Friday, October 30, which showed a positive surprise in manufacturing, a rise in retail sales as expected, and a decline in mining, we estimate monthly GDP would be down in annual terms by -6% y/y. September should have been the last month with a significant impact in consumption coming from the withdrawal of pension funds and the fiscal measures to support household incomes. On Friday, November 6, we will get the inflation print for October. We expect a monthly variation of 0.3% m/m, explained by the re-instatement of the stamp tax and greater pressures on food products. With this, annual inflation would reach 2.6% y/y. Finally, we will monitor the discussions in the Chamber of Deputies on a second withdrawal of pension funds. The following two weeks will be key in these deliberations. The Government could bring the matter to the Constitutional Court if the bill is approved.

Colombia—Policy Rate Analysis from the Reaction Function’s Point of View

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@co.scotiabank.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@co.scotiabank.com

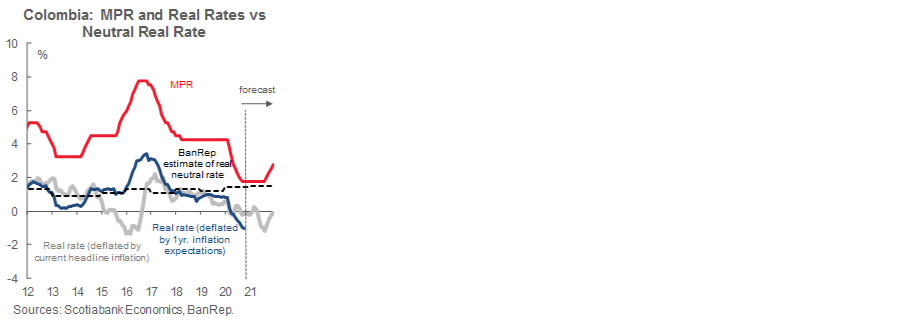

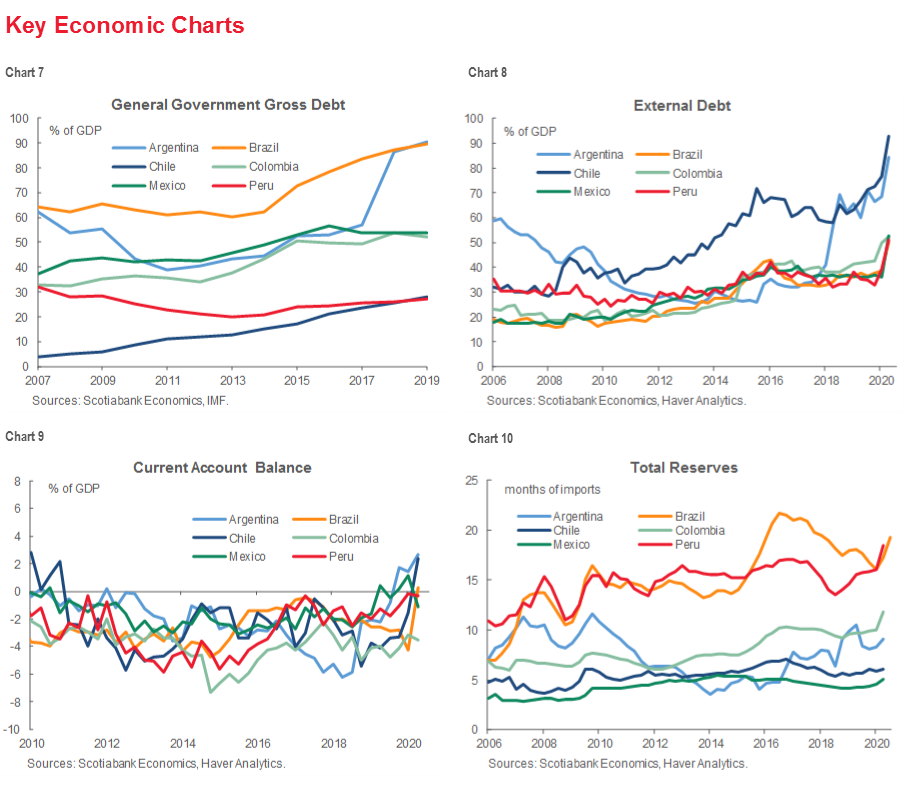

A conventional reaction function under an inflation targeting (IT) framework has three key factors that central banks look at in order to determine the appropriate policy rate: the neutral interest rate, the inflation gap, and the output gap. The Colombian central bank (BanRep) has been characterized as one of the most conventional IT banks in the region, even in the face of 2020’s COVID-19/oil price shock. This means that, although the current situation forced BanRep to cut its policy rate by -250 bps, it did so at a more gradual pace than its peers and—in terms of level—Colombia continues to have some of the highest nominal and real policy rates in the region (see Key Economic Charts section, chart 5). According to our own calculations, 1.75% is the lowest nominal policy rate at which the BanRep would be comfortable to enter into a wait-and-see-mode in the midst of still-high uncertainty.

On the inflation gap, headline inflation and core inflation measures found a bottom in August, and in September showed a small rebound to levels close to 1.9% y/y for both numbers; meanwhile, inflation expectations continue to point to a normalization by the end of 2021 at levels a bit below the 3% target. Thus, although inflation has given us signals that the policy rate should be on the expansionary side, if inflation expectations are right, there is not much room to continue with the easing cycle.

In the output-gap arena, it is clear that the 2020 recession needs a highly expansionary policy rate to help the recovery of economic activity. Lower rates reduce saving incentives due to a very low opportunity cost between savings and consumption; they also help investment since lower interest rates make it easier to invest in the real sector with lower funding costs.

However, interest rates that are too low also create perverse incentives that increase inflation via unsustainably high consumption expenditures and boost unproductive investment due to cheap funding costs. So, what is the level at which BanRep can boost the economy without lowering rates so far that instabilities are created, as Hernando Vargas, BanRep’s chief economist, has warned? The answer starts with potential output. In our estimation, the COVID-19 shock cost Colombia about 5% of its stock of capital; therefore, a good chunk of the GDP lost due to the recession is not immediately coming back, which means that monetary policy cannot help on this front. According to BanRep’s calculations, potential output growth this year and the next will be -2.6% y/y and 1.6% y/y, respectively. As a result, we project that the BanRep’s expansionary stance should continue in 2021, however, gradual normalization should start by H2-2021 since the ongoing recovery in economic activity should start to narrow the output gap by that point. In the meantime, as discussed in previous Latam Weekly reports, the BanRep is likely to remain very active in keeping liquidity in the system to prevent instabilities.

Finally, according to BanRep staff, the neutral real interest rate is 1.4%, which means that Colombia currently has a very expansionary monetary stance (chart). In fact, the current nominal policy rate, 1.75%, is -0.22% in real terms if we deflate it with current inflation, but even more negative if we use 1-y inflation expectations (about -1.05%).

All in all, from the perspective of the reaction function, we don’t see more room for the BanRep to continue the easing cycle under the base line scenario that involves an inflation normalization by 2021 and a gradual recovery in economic activity. Therefore, we expect BanRep to continue to hold its policy rate at 1.75% in a wait-and-see mode in anticipation of developments in prices and the real economy. In fact, at the October meeting (Friday, October 30) the BanRep ended its easing cycle in a unanimous decision that guided toward stability for the near future.

Mexico—Bouncing back

Mario Correa, Economic Research Director

52.55.5123.2683 (Mexico)

mcorrea@scotiacb.com.mx

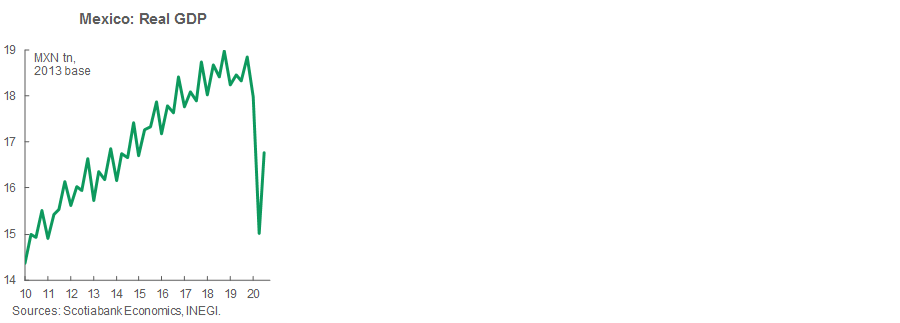

In the first advance, preliminary data on Q3, real GDP grew by 12.0% q/q as the economy recovered some of the ground lost due to the COVID-19 pandemic. This is good news, but it should be taken with the appropriate perspective. First, the rebound was naturally expected as economic activities reopened and—given the order of magnitude of growth rates—differences between expected and observed results should be taken with caution. Second, in Q3 the production level recovered only 40% of Q2’s losses and got back only to 2014 levels (chart). Third, there is a clear dichotomy in the pace of growth in the economy. On the one hand, manufacturing activities are presenting a fast rebound, pulled by external demand, mainly from US industrial activity, which is propelling Mexican exports. On the other hand, internal demand continues to show signs of weakness, as private consumption and investment have been affected not only by the pandemic, but also by a negative business environment due to controversial decisions on public policy. As a result, the services sector is recovering at a much slower pace of 8.6% q/q in Q3 versus 22.0% q/q in the industrial sector. In coming quarters, economic recovery in Mexico will depend on exports, which are performing well due to the US economic recovery—and on private consumption from households and investment from firms, both of which have presented weak readings. It is worth noting that a new confinement to contain the spread of COVID-19 is not being contemplated owing to concerns about the economy. If another lockdown proves necessary, then our forecasts will need another significant, negative adjustment.

Inflation presented a new surprise on the upside in the first half of October, posting a 0.54% 2w/2w result while the consensus average was 0.46% 2w/2w. The surprise came mainly from the energy sector—which saw prices rise by

3.72%, while in the previous year they increased by only 3.09% in the same period—and also in fruits and vegetables, whose prices increased by 2.77%, an unusually high reading for this period. Core inflation was relatively tame in this fortnight, increasing only 0.14% 2w/2w. General inflation reached 4.09% y/y, while core inflation posted a 4.00% y/y reading—both at uncomfortably high levels when compared with the official target of 3.0% y/y. These results are likely to tilt the balance on Banco de Mexico’s Board in favour of a pause in the next monetary policy decision on November 12.

The trade balance recorded a new strong surplus in September at USD 4.4 bn, which brought trade to a total surplus of USD 21.8 bn over the last 4 months, which is highly unusual for the Mexican economy. Total exports grew 3.7% y/y in September, mainly driven by manufacturing exports, which grew 4.3% y/y. The pace of total imports growth showed significant improvement, increasing by USD 3.3 bn between August and September, which was mainly explained by the intermediate goods component, suggesting that a faster pace of internal production obtained in September. Total imports are still -8.5% below a year ago.

There was also a marginal improvement in the unemployment rate, which edged down to 5.1% in September from 5.2% in August. Retail sales grew 2.5% m/m in August, but remained -10.1% below the level reached a year ago. Direct bank financing to the private sector weakened again in September, falling -2.0% y/y in real terms after a -1.7% y/y decline in August.

Finally, Pemex presented its Q3 financial results, with a net profit of 1.4 bn pesos that contrasts with the loss of 606.6 bn pesos in the first half of the year. Balance sheet performance remains a cause for concern. Total assets contracted by 12.9 bn pesos from the end of 2019 to September 30, while total liabilities increased by 522.9 bn pesos, resulting in a negative change in equity of 535.8 bn pesos. In US dollars, Pemex equity reached negative USD 110.3 bn in Q3.

During the coming two weeks, we will have the next monetary policy decision by Banco de Mexico on November 12. Since the minutes of the last meeting indicated a divided Board—with three out of five members expressing at least some doubts about the need for another cut in the reference interest rate—and inflation remained above the 4% y/y threshold in the first half of October, it is likely that the Board will keep the rate unchanged. Over the next fortnight, we will also receive the Banco de Mexico survey of economic expectations results for October, remittances for September, investment and internal private consumption for August, and inflation and auto industry figures for October.

Peru—COVID wanes, the elections race begins to warm-up, and the economic recovery remains tepid

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Daily COVID-19 contagion, hospitalization, and mortality rates have dropped markedly over the past few weeks. However, news from the rest of the world and the fear of a second wave continue to unnerve health authorities, who refuse to lift travel, capacity, and concentration restrictions even as they open up more segments of the economy.

Meanwhile, the pace of the recovery has slowed. We expect September GDP to remain down by -8% y/y, which is not much of an improvement over the -9.8% y/y recorded in August. This strains our -11.5% full-year forecast a bit, although not enough to change it yet as we see signs of a sharper improvement in Q4. The agroindustry is particularly strong, with 20% export volume growth in August. At the same time, mining, which was struggling to get out of COVID-19’s shadow, apparently has finally done so in October, with reports of healthy recent output gains. The third leg to the table is public sector investment, which is also showing hopeful signs of a vigorous improvement in Q4. Perhaps the most pleasant surprise comes from the real estate and home construction market. September was the third consecutive month in which home sales surpassed pre-COVID-19 levels. As proof that this was not a data distortion, cement sales soared 10% y/y in September, and mortgage loans in September rose for the first time since February. In sum, the third quarter recovery has been exasperatingly slow, but the fourth quarter holds promise of an acceleration.

By the time this report is published, inflation for October will have been released. The month is key in determining whether inflation begins to slide towards our full-year forecast of 1.5% y/y, in line with weak domestic demand, or continues hovering around 1.8% y/y. Either way, it seems clear that the BCRP will maintain its policy rate at 0.25%. In fact, the BCRP seems focused more on the FX market, and on the cacophony coming from Congress concerning pension funds, than on domestic price management. The FX rate has been pushing against the historical high range of USDPEN 3.60 to 3.65 for some time and could gather force if resistance is punctured. Since this could unnerve both businesses and public opinion, the BCRP has been intervening just enough to provide some stability without reversing the overall trend.

The political front seems to have settled down. Congress will be debating yet another bill for the impeachment of President Vizcarra in early November. The odds appear to favour Vizcarra overcoming this challenge once again. However, his image has suffered with the successive allegations of corruption. At the same time, however, even as Congress has focused its attack on Vizcarra personally, it has become more receptive to working with the Ministry of Finance and the BCRP. This will not be enough to prevent Congress from continuing to embrace populist initiatives, but it could help take some edge off many of these proposals. Meanwhile, public and political attention is turning from the congressional-executive boxing match to the electoral racetrack, as potential candidates jockey for space on presidential tickets and parliamentary lists.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.