ECONOMIC OVERVIEW

- The week ahead brings economic activity data out of Peru, Brazil, and Colombia, though data for the first two may be somewhat stale while in Brazil we’d rather pay close attention to the expected release of the government’s fiscal framework proposal. Social unrest headwinds continued in February in Peru so Saturday’s GDP print should also be taken with a grain of salt before a stronger March reading.

- The balance of information for Colombia shows that the country saw a moderate economic slowdown in the first quarter. The team takes stock of developments in inflation and monetary policy, and discusses the slow advance of social reform negotiations.

- We have little to look forward to in the case of Chile and Mexico, but the team in Santiago has modified its forecasts to show a smaller reduction in the BCCh’s policy rate by year-end—whose meeting minutes are out on Thursday. In the case of Mexico, our economists discuss the (small) implications of the Iberdrola power plants sale as retail sales data are an afterthought for markets that are looking ahead to H1-Apr CPI the following week.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

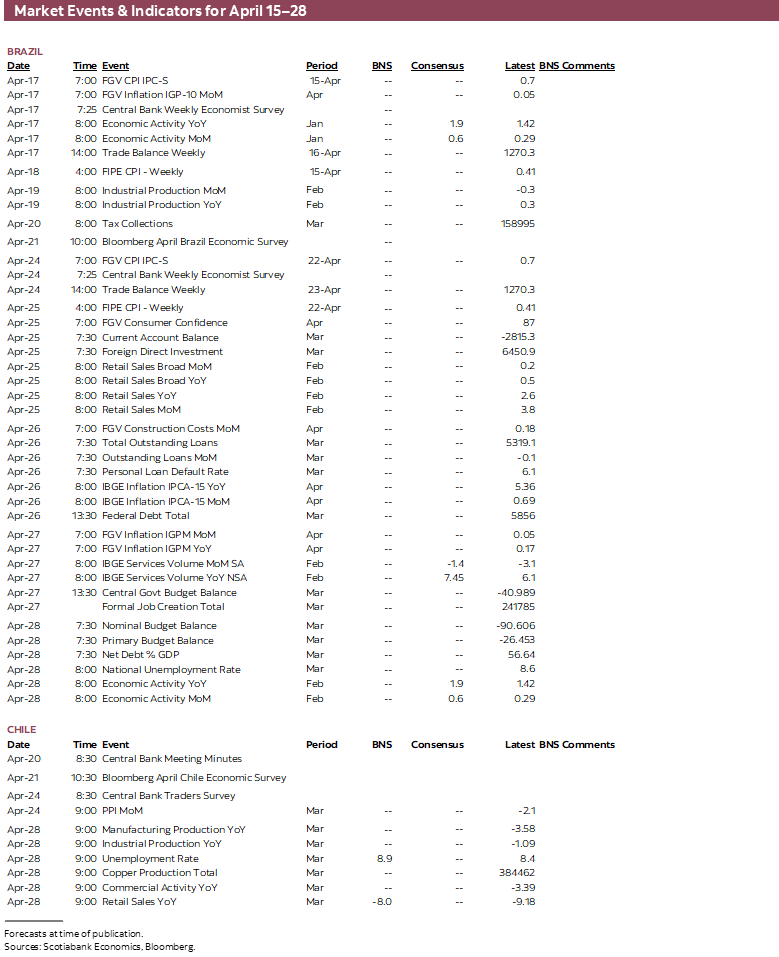

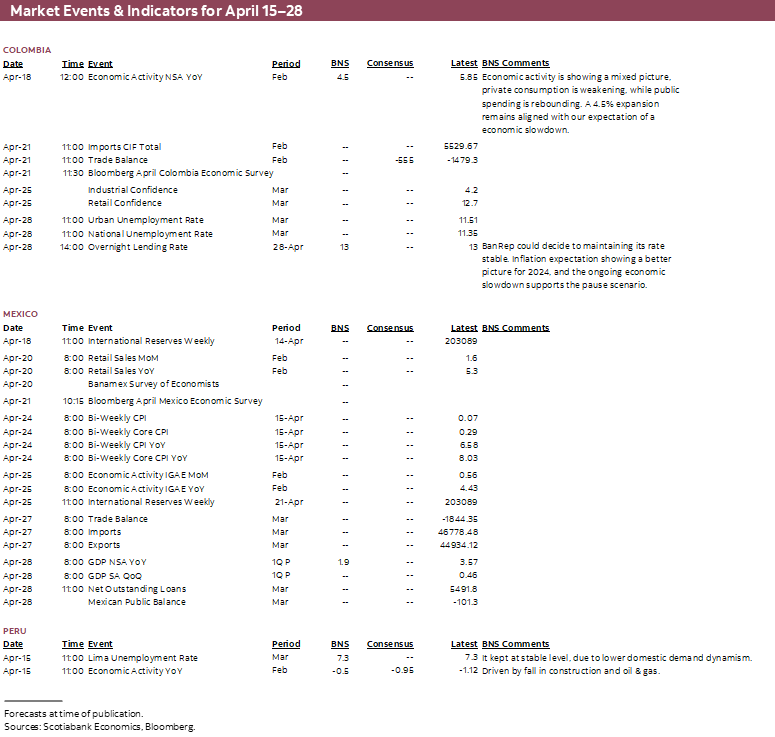

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period April 15–April 28 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: ECONOMIC ACTIVITY DATA; BCCH FORECAST CHANGE

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- The week ahead brings economic activity data out of Peru, Brazil, and Colombia, though figures for the first two may be somewhat stale while in Brazil we’d rather pay close attention to the expected release of the government’s fiscal framework proposal. Social unrest headwinds continued in February in Peru so Saturday’s GDP print should also be taken with a grain of salt before a stronger March reading.

- The balance of information for Colombia shows that the country saw a moderate economic slowdown in the first quarter. The team takes stock of developments in inflation and monetary policy, and discusses the slow advance of social reform negotiations.

- We have little to look forward to in the case of Chile and Mexico, but the team in Santiago has modified its forecasts to show a smaller reduction in the BCCh’s policy rate by year-end—whose meeting minutes are out on Thursday. In the case of Mexico, our economists discuss the (small) implications of the Iberdrola power plants sale as retail sales data are an afterthought for markets that are looking ahead to H1-Apr CPI the following week.

We’re looking ahead to a relatively quiet Latam week, with already some of the more notable data out over the weekend rather than during the trading week. Peru publishes a couple of key figures—unemployment rate and monthly GDP—on Saturday in what are the only major releases in the country until CPI data on May 1st. The economic activity print may also be somewhat backward-looking, as February data will reflect lingering, though more muted, disruptions from protests, and our Lima economics team believes a slightly negative to no growth print is the more likely result. March output data may be impacted somewhat by adverse weather, but preliminary figures for the month (mining, public investment) point to a solid return to y/y growth in Peru.

Brazil’s data and events calendar may offer a bit more than its regional peers, with economic activity figures out on Monday, though data for January looks even more stale than Peru’s. What may be more interesting is the results of the weekly BCB survey out that same day to see if economists changed their view on the end-2023 policy rate (last seen at 12.75%). The survey comes on the heels of the slight miss in March inflation earlier this week that saw an increase in year-end rate cuts pricing in markets. On the political front, continued (slow) progress on fiscal framework plans and the debate of the proposal to be put forth by Fin Min Haddad (now expected on Monday) will remain key items to watch.

In Mexico, retail sales data for February is but an afterthought as traders are unlikely to alter their views too much on this, with the release of H1-April CPI around the corner, on the 24th; another soft print then could see markets settle on expecting only one final 25bps increase next month. On a related note, the Citibanamex survey results on Thursday could also show a lower terminal rate forecast, with projections leaning just in favour of a rate cut before the end of the year. Banxico’s minutes published yesterday provided little guidance on the policy rate path (see Latam Daily). In today’s weekly, Eduardo Suárez writes on the announcement of the sale of Iberdrola plants in Mexico with some implications for private participation in the country’s power sector—though the move itself should have no impact on installed power generation capacity.

Colombia’s DANE will publish economic activity index data for February on Tuesday. The January gain of 5.9% y/y greatly surpassed economists’ estimates (Bloomberg median at 2.5%) but we see the economy continuing on a slowing trend on weakening private consumption. BanRep meets two weeks from today, when we see an unchanged policy rate at 13.00%. In today’s weekly, the team takes stock of economic and inflation developments in the first quarter, and discusses the very slow progress in social reform negotiations.

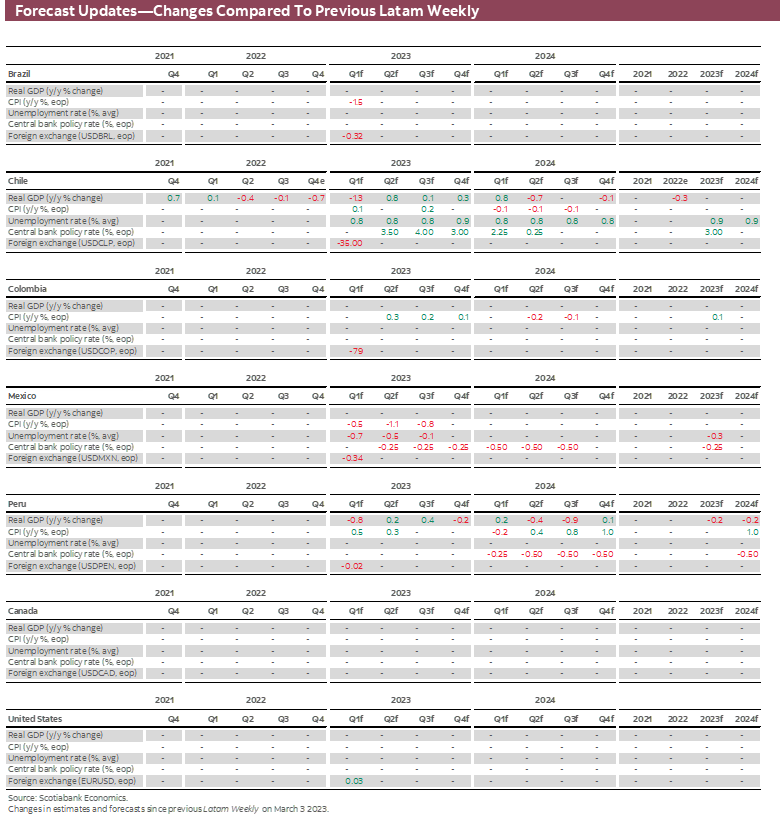

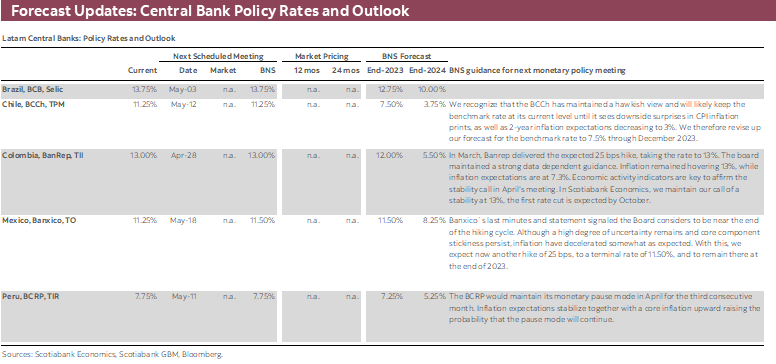

Lastly, Chile’s schedule has limited releases of consequence with the exception of Thursday with the minutes to the most recent BCCh decision in early-April that saw the bank stick to a relatively hawkish message pushing back against cut expectations. Our economists in Chile have pushed back the timing of the first projected rate cut to the final meeting of the quarter (in June), with a 25bps reduction then. See the Chile section for a more detailed overview of the new forecast—which leaves annual GDP growth and year-end CPI inflation projections unchanged.

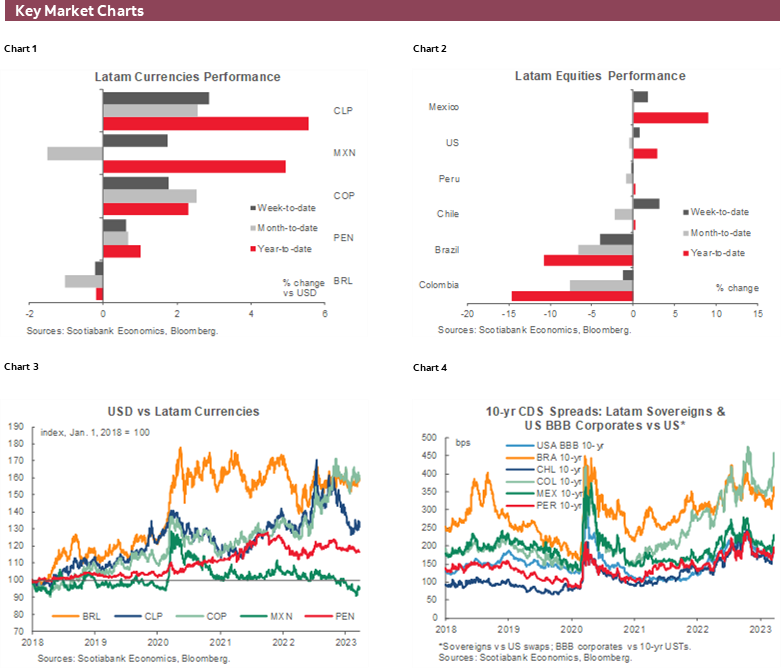

There is also not too much that catches the eye from a US data standpoint next week but global markets are due to pay close attention to comments by Fed officials ahead of the start of the bank’s communications blackout next Saturday. Rates pricing in markets is favouring a 25bps rate hike, though only assigning around 65–70% odds to it with no additional increases beyond this point. Latam currencies have certainly been no strangers to the broad moves in markets over the past month or so as markets look ahead to the end of the Fed’s hiking cycle, with the COP, BRL, and MXN, in particular, recording solid gains against the USD. There is a clear risk, however, that markets may be overestimating the Fed’s shift to a rate cutting stance this year and with it, a partial reversal of recent currency gains may be in store—though the Latam FX continue to offer appealing rates.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Returning to Macro Equilibrium Amid Stalling Credit Flows

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

WE REVISE UPWARDS OUR PROJECTION FOR THE BENCHMARK RATE IN 2023; UNCHANGED IN GDP AND CPI FORECASTS

In early April, the Central Bank of Chile (BCCh) kept the benchmark rate unchanged at 11.25% and maintained a neutral bias regarding future rate movements, indicating that it will keep policy at its current level until the process of inflation convergence to 3% is consolidated. In our view, the monetary policy strategy should be opting for waiting for clear signs of a deceleration in core inflation before initiating the normalization process.

We recognize that the BCCh has maintained a hawkish stance and is likely to keep the benchmark rate at its current level until it sees downside surprises in CPI inflation figures, as well as 2-year inflation expectations falling to 3%.

Taking the above into account, we revise upwards our forecast for the benchmark rate to 7.50% in December 2023 (from 4.50% in our last scenario), which is consistent with our forecast for GDP growth and inflation this year.

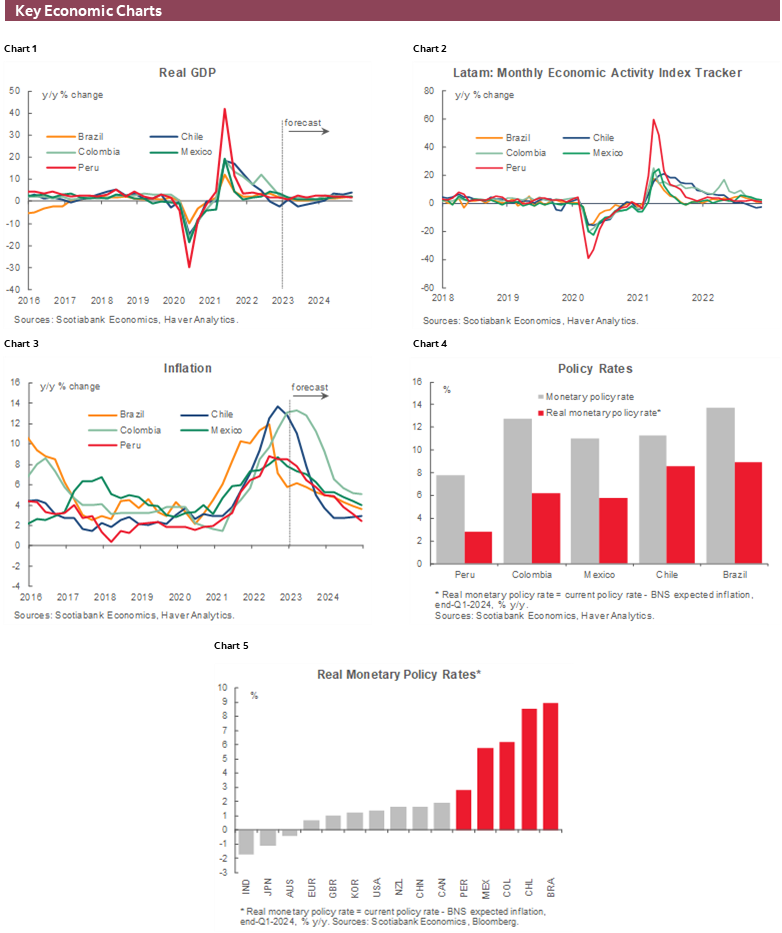

In this context, we continue to forecast a mild recession in 2023 with a GDP contraction of 0.8%. In the short term, we forecast a GDP contraction of between 0.5% and 1.5% y/y in March, followed by negative y/y figures until June. On the CPI front, we continue to forecast headline inflation of 3.7% y/y in December 2023, driven by lower tradable goods inflation and weakness in private consumption, along with the strength of the Chilean peso (CLP) in real terms.

Overall, the good performance of CLP has been explained by good news on the political front, with a constitutional process with sufficient restrictions limiting the room for extreme proposals and the government seeking broad agreements on structural reforms. Looking ahead, we see the likelihood of right-wing parties gaining more than 3/7 of assembly members at the May 7 elections increasing, which would give them sufficient numbers to block extreme proposals.

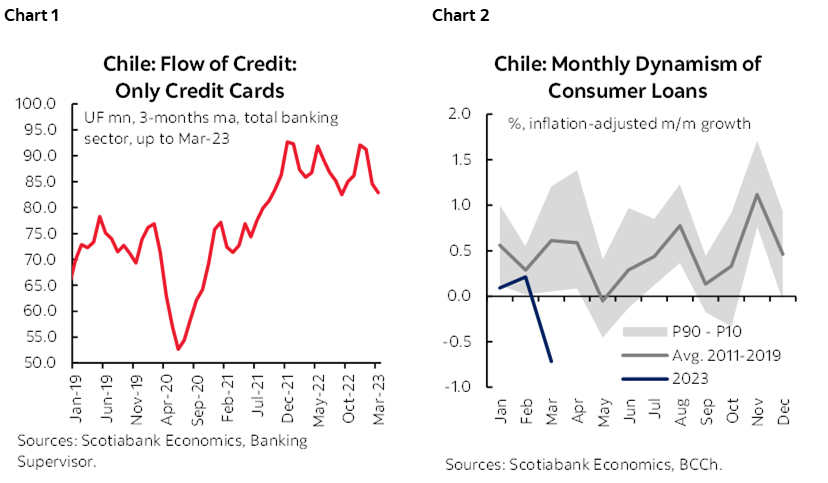

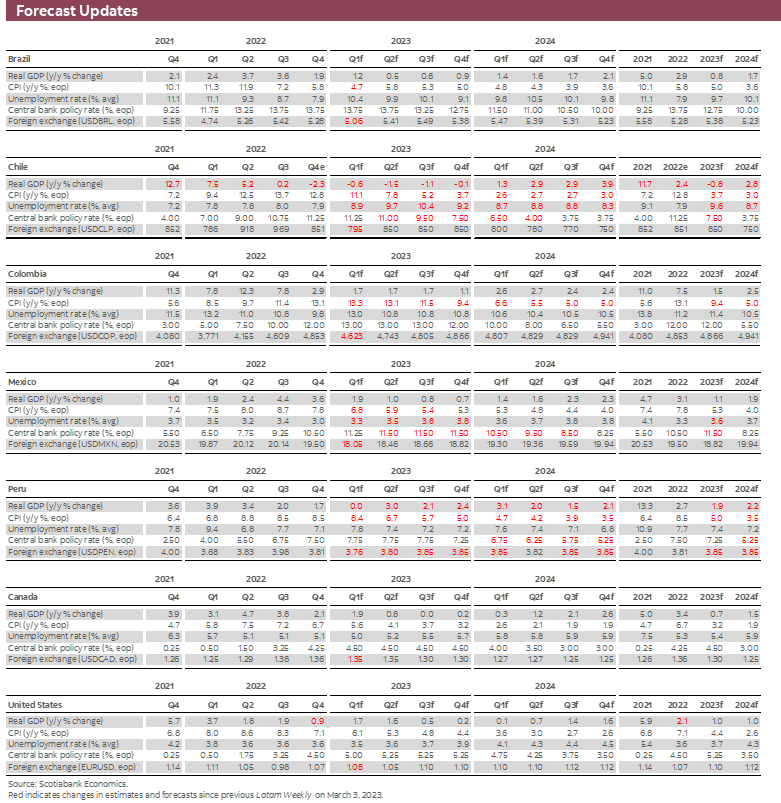

PRIVATE CONSUMPTION LANDS AT A SUSTAINABLE LEVEL AS CREDIT FLOW STAGNATES

In its latest Monetary Policy Report, the BCCh warned about an acceleration in the flow of consumer credit card loans, for which it only used statistics from the Metropolitan Region. We do not agree with this view.

Private consumption has returned to a sustainable level in recent months, and we see no signs of recovery, but rather of stabilization at low levels. Although we observed increased usage of credit cards amid tight credit conditions, much of the increased activity was explained by tax and travel payments in March. In addition, consumer lending fell sharply in March in inflation-adjusted terms. In summary, we observed flat credit flow at the national level and even a slowdown at the margin (charts 1 and 2).

Colombia—Taking Stock of the First Quarter

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Santiago Moreno, Senior Research Analyst

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

The first quarter has ended and Colombia's macroeconomic balance shows a moderate economic slowdown due to weaker private consumption, partially offset by more dynamic regional public spending that coincides with the pre-electoral season. Inflation hasn't reached a strict peak yet. However, it is transitioning to a plateau of around 13.3%, and one-year-ahead inflation expectations are hovering at 7%, which has been at least encouraging for the central bank to slow down its hiking cycle. At its latest meeting, the central bank delivered a 25bps rate hike to 13.00% in a unanimous vote, maintaining a data-dependent approach. Minutes revealed two groups within the board, one group emphasizing that cumulative rate hikes are contributing to an economic slowdown, and the other group is concerned about still-high inflation expectations and potential future volatility.

On the political front, negotiations for social reforms are taking longer than expected. Unlike the fiscal reform debate, traditional political parties have laid out red lines regarding the government's strategies to achieve social goals this time around—the health reform is struggling to find enough support. National Development Plan debates are dropping requests for special powers for the president. The labour reform also faces headwinds since it proposes significant increases in labour costs, which could act against a reduction in informality. The only reform that hasn't raised significant political concerns is the pension reform which, in broad terms, is meeting some social targets such as increasing the coverage to the vulnerable elderly population with a subsidy that will be financed by current fiscal income. It also seeks to eliminate the competition between existing sub-systems and limit the size of pension subsidies to high-income people, which could be an opportunity to impulse voluntary savings that currently account for less than 2% of GDP. The big question mark concerns technical items and the regulatory framework of the public savings fund proposed in the pension reform. However, it is not an issue that will be resolved soon. From a fiscal perspective, the pension reform is seemingly favourable as it reduces uncertainty around pension liabilities. The labour reform doesn't have a direct fiscal impact, in theory. In contrast, the health reform's fiscal income assessment is not yet known.

With only nine weeks left in the current congressional legislature session, we assign a low probability to the approval of the ambitious political package. Were something to get approved, it would likely be greatly watered down. In that context, we anticipate a more conciliatory tone will be taken by the government.

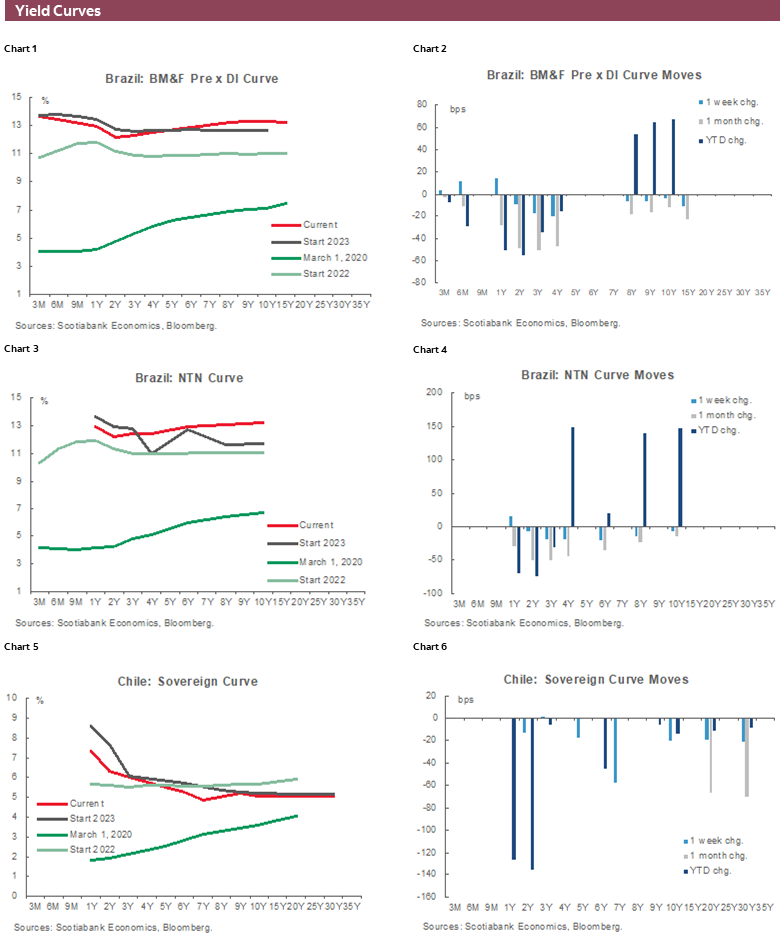

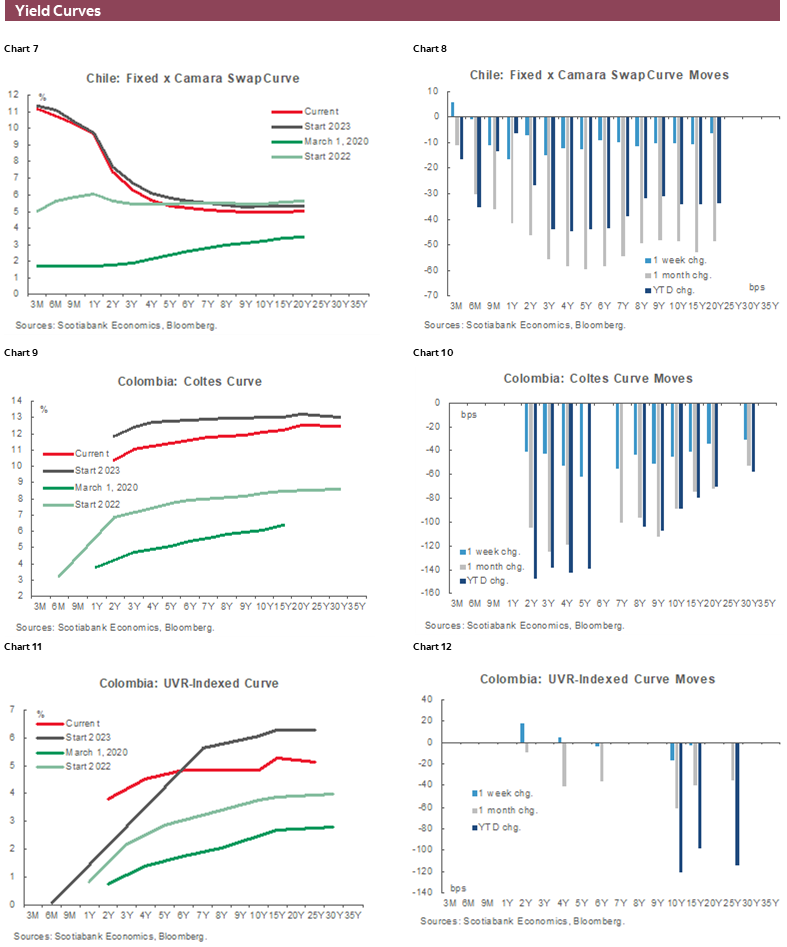

In markets, international trends and a reduced domestic risk perception have led to an improved performance of local assets. In the first quarter, the Coltes curve fell significantly, while the USDCOP is now trading below the 4,500 pesos mark. In the case of the exchange rate, seasonal flows due to tax payments from corporations are contributing to its appreciatory trend. However, this temporary effect is expected to vanish in the coming weeks. Our forecast for the cross remains stable at around 4,750 to 4,900 by year-end; we assume that the currency is still pricing a risk premium from international developments, and a firming of the "higher for longer" stance at the Fed could trigger a stronger dollar in the medium term.

Mexico—New Twist in the Mexico-North America Power Sector Struggle

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

President López Obrador announced that Spanish company Iberdrola would sell 13 plants in Mexico (12 combined cycle and one wind farm) to Mexico Infrastructure Partners (MIP, a private infrastructure fund), in turn financed by the Fonadin (a Mexican Government infrastructure fund structured within development bank Banobras) for close to USD5.9bn.

There is still uncertainty about the structure of the deal, and how the responsibilities between Fonadin and MIF would be split, but the details that have emerged so far suggest this deal could be similar in structure to the PIDIREGAS (Proyectos de Infraestructura Productiva con Impacto Diferido en el Registro de Gasto) of the past. There have been reports that the financing of the deal is primarily contributed by the Mexican public sector through the Fonadin, as well as MIP, making the acquisition a form of Public-Private Partnership. However, reports also state that the operation would fall to CFE rather than private players, differing somewhat from PIDIREGAS employed in the past.

PIDIREGAS were a mechanism developed in the 1990s to allow Mexico to access larger amounts of resources in the aftermath of the 1994 crisis, by opening the sector to private sector participation and having a deferred impact on public finances. Their use was primarily in the energy sector, and roads, but even education was contemplated. This mechanism allowed private players to operate projects, which would be financed with a public sector guarantee and where, after a period, the assets would end up as public sector assets. However, in past uses of PIDIREGAS, private players often operated the assets. For public finances, the PIDIREGAS counted as “contingent liabilities” (as the actual cost to public finances were variable), with only the looming amortizations counting as part of the public sector borrowing requirements (PSBR).

The transaction between Iberdola-MIO / Fonadin has no impact on the installed power generation capacity in Mexico, and is essentially a negative FDI flow, compensated by the flow from the acquisition by the Fonadin / MIP. The impact on the power generation capacity in Mexico is neutral, as assets are simply changing hands. Interestingly, close to a week after announcing the sale of assets in Mexico, the Spanish company committed a similar amount of investments into Brazil (US$5.8bn). However, one positive implication from the transaction could be a modest thawing of the government’s appetite for private participation in the power sector, particularly if it means that going forward the use of PIDIREGAS will widen the resources available to finance power sector development.

If this is indeed the case, there are a few factors to consider:

- The use of PIDIREGAS can, on the margin lead to a decreased transparency in public accounts (they can be considered contingent liabilities as opposed to debt, and their cost to public finances is tougher to model due to potential project structure complexity).

- They also tend to have a higher cost than public debt (i.e. mbonos, cetes, etc), and would hence likely make the development of the power sector costlier.

Peru—A Ray of Greater Stability is Starting to Break Through Peru’s Cloudy Skies

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

In Peru, there is a growing sensation that things are slowly returning to normal. A hot, muggy and humid normal, in any event, given the ongoing El Niño and consequent rains, which, however, should not have any really significant impact on the economy in 2023. More importantly, social protests are turning into more a memory than a day-to-day reality, and heretofore urgent issues such as early elections, presidential impeachments or other major disruptive political events, are no longer dominating the political agenda, allowing the government to dedicate its energies to more normal state management activities. Two recent examples of this are the initiative to transfer PEN209mn for emergency relief following the heavy rains and landslides along the Northern coast, and the recent proposal sent to Congress for the creation of a National Infrastructure Authority, which would reportedly seek to expedite 1,800 infrastructure projects.

Looking forward, early indicators point to better growth after a dismal January–February. Furthermore, we expect inflation to begin to decline in earnest (finally!) beginning in April.

Let’s begin with inflation. Early price indicators for April point to an inflation trend of under 0.3% for the month. Yearly inflation is, then, tracking 7.6% to 7.8%. To be sure, it’s still early in the month, but should the trend continue, and there seems to be no reason why it shouldn’t, then 12-month headline inflation would fall comfortably below 8.0% for the first time since March 2022.

Regarding February GDP, to be released on Saturday, April 15, our bias is that growth is more likely to be slightly negative than positive. February was an atypical month, however, as violent protests continued and rains were beginning. Construction growth appears to have been particularly hard hit, given the double-digit decline in cement sales. Mining was also affected by roadblocks at a few locations.

March should be quite a bit more hopeful, when data come out in a month’s time. For now, we have initial figures of double-digit mining growth, fairly robust public investment, and a more normal evolution of most domestic demand components, which should take March GDP comfortably above 1.0%, and perhaps closer to 2.0%.

Barring a significant surprise for February GDP, we are comfortable with our full-year 2023 GDP growth forecast of 1.9%, which already incorporates the impact of the Q1 political turbulence.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.