- Peru: BCRP holds as expected for third consecutive month

- Mexico: Banxico minutes with little guidance on the policy rate path

Overnight trading was quiet with the USD and US yields moving in relatively narrow ranges after yesterday’s choppiness on the PPI data. The USD may be on the verge of clawing back some of its recent losses as some of the key currencies break key psychological levels and/or near overbought territory; at least that could augur for a slowing of its depreciation against the likes of CAD, EUR, GBP, and CHF. For that, however, rate cut expectations by year-end may need to be reduced further.

Crude oil is roughly unchanged but holding a solid near 2% gain for the week, extending the OPEC-cut-motivated rally. Copper is around 0.5% higher, while iron ore picks up marginally (up 3.2% and 0.8% for the week, respectively).

The MXN is the worst performer overnight, coming off sub-18 pesos trading during yesterday’s session as the big figure area stands as decent support for the cross since early-March. Yesterday’s Banxico minutes (see below) had limited impact on the currency.

The main event of the Latam day will be the BCRP’s presser following yesterday’s rate hold (see below) at 13ET. The bank made but a minor adjustment to its statement that more clearly suggests that the current policy rate of 17.75% is its terminal rate. We’ll look for officials to elaborate on guidance later today.

Colombian manufacturing/industrial production and retail sales data at 11ET round out the session on the data front while we also await the results of the latest BanRep economists’ survey. Today’s macro data will help refine expectations for next Tuesday’s release of monthly economic activity data for the month where a softening from the surprising 5.9% y/y expansion in January is expected.

Global markets will centre their attention on the release of US retail sales data at 8.30ET followed by the results of the April U Michigan consumer sentiment survey at 10ET, with swaps pricing positioning for a final 25bps increase from the Fed in May.

—Juan Manuel Herrera

PERU: BCRP HOLDS AS EXPECTED FOR THIRD CONSECUTIVE MONTH

The board of Peru’s central bank (BCRP) kept its key interest rate at 7.75% on Thursday, in line with the market consensus and with our forecast, confirming the pause mode for the third consecutive month after 18 months of hikes. In its statement, it reiterated that it keeps its options open to changes in any direction in the future—specifying that this decision does not necessarily imply the end of the interest rate hike cycle. However, unlike the previous statement, it replaced the text of making “additional changes” with making “changes” to monetary policy, if necessary. The new text accommodates more to the possibility that the interest rate has already reached its terminal level at 7.75%.

The statement kept its concerns about the macroeconomic effects of social unrest. GDP was affected for this reason during 2023-1Q, which led the BCRP to reduce its inflation forecast from 2.9% to 2.6% for all of 2023, materializing the deterioration of indicators and expectations about the economy, which until March they remained in pessimistic territory, although without fall in a recession.

In March, year-on-year inflation accumulated 22 months outside the target range, surpassing the previous record. Inflation fell slightly in March, although the monthly data exceeded market expectations. The BCRP, like us, expected a visible drop in inflation beginning in March, which has not materialized yet. The BCRP attributes this behavior to transitory effects on inflation due to supply restrictions of some foods and the rains derived from Cyclone Yaku. The BCRP forecast that the downward trend in year-on-year inflation will continue in the coming months with a return to the target range in Q4-2023, with a forecast of 3% inflation for the year-end, although the BCRP acknowledges an upward bias in its forecast. Our inflation forecast remains at 5.00% by end-2023.

The statement does not yet give clear signals of how long the interest rate can remain at the current level. Twelve-month inflation expectations are key. In March they remained stable at 4.3%, but still well above the target range (between 1% and 3%). April inflation is expected to reflect the break that should have been seen in March, so we see the possibility of inflation falling below 8% in April. Our base scenario considers that key rate will remain stable in this level for a long time, at least at 3Q-2023.

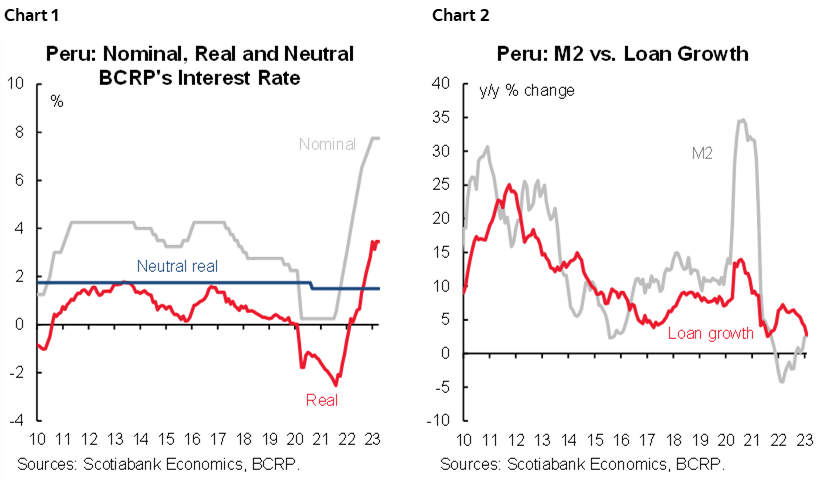

The decision to hold the policy rate could have seen the monetary policy stance is already tight enough to deepen economic weakness. The real interest rate kept stable at 3.45% (chart 1), remaining above its neutral level (1.50%) for the eighth consecutive month. Liquidity growth in soles (M2, chart 2) accelerated from 2.4% to 2.7% in February, remaining in positive territory for the sixth consecutive month, while, on the contrary, credit expansion slowed down also for the sixth consecutive month, going from 4.1% in January to 2.8% in February.

The BCRP statement indicated that the outlook for global economic activity points to a moderation, although global risk remains due to restrictive monetary policy in advanced economies and ongoing global conflicts. Regarding the previous statement, it left aside the impact of inflation on consumption, and included among his concerns the uncertainty of upward pressures on the prices of energy commodities.

—Mario Guerrero

MEXICO: BANXICO MINUTES WITH LITTLE GUIDANCE ON THE POLICY RATE PATH

Yesterday, Banxico released the minutes to its March monetary policy meeting, where it delivered a 25 bps hike, to 11.25%, reaching a new record high. In the communiqué, they stated that they have been monitoring different national and international economic indicators, as well as the development of the recent banking crisis in the United States, which has been the focus of attention in international financial markets. Within this, the Board considered that the Mexican banking sector remains solid and with sufficient liquidity given the current regulations.

On the other hand, although this latest decision was unanimous, some board members noted that the rate is already restrictive enough to address inflation, which has remained well above from the central bank's target. Although inflation has begun decelerating, what is worrying is the core component, which does not seem to be easing, standing at 8.09% y/y, with pressures in merchandise (10.12%) and services still on the rise (5.71%). On the non-core side, agriculture (7.24%) and energy (0.16%) have already taken a downward trend, supporting the overall deceleration. The Board mentions that it will be necessary to continue monitoring the indicators, as several of them remain strong.

The MXN has continued to appreciate, but with significant volatility. It has also benefited from the nearshoring effect, derived from the tensions between the US and China. Another relevant factor has been the limited effect of the banking crisis on the Mexican financial sector, despite the fact that banks listed on the Mexican Stock Exchange have suffered considerable losses in market capitalization.

The document noted Deputy Governor Irene Espinosa's dissenting opinion on the central bank's communication strategy. In particular, Espinosa pointed out that the forward guidance in the statement reinforces a very short-term, partial and incomplete view, as it omitted to communicate that "they anticipate that the monetary stance will have to remain in restrictive territory for two years to achieve the convergence of inflation to the 3.0% on-time target".

As we have mentioned before, we believe that it is better for the Banxico to provide conditional guidance rather than forward guidance, as forward guidance as a price taker may risk losing credibility. In an environment of high uncertainty, it may be better to provide forward guidance subject to the expected downtrend in inflation.

Following the last two monetary policy announcements, where the bank surprised on the upside in February with a 50 bps hike and in March delivered an expected 25 bps hike—although without explicit forward guidance on the monetary policy horizon—we noticed a wider consensus among analysts regarding rate expectations. In this sense, the Citibanamex Survey shows a wide range of responses regarding the year-end rate, ranging from 10.0% to 12.0%, with a median of 11.38%. This implies that a majority of analysts now expect Banxico to start its cutting cycle before 2024, while others expect the hiking cycle to end above 11.50% and remain unchanged for the rest of the year. For our part, we maintain our expectation that the cutting cycle will begin in early 2024.

—Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.