ECONOMIC OVERVIEW

- Between now and Friday, the Fed, ECB, BoE, BCB, Banxico, BCRP, SNB, Norges Bank, and PBoC will all meet and decide on policy, with recent inflation optimism prompting a sharp rally in global rates markets that has gone mostly unchallenged by officials—which partly fueled greater declines in yields.

- Among the key central banks announcing policy next week, only the BCB and BCRP are expected to move their benchmark rates, and it’s unlikely that they deviate from expected respective 50bps and 25bps cuts.

- As for Banxico, the doves in the board may firm up guidance for an earlier (February) rather than later (March) start to rate reductions. The Fed and ECB will be looking to push back against the quick increase in cuts pricing; the BoE may be more comfortable.

- Colombia retail sales and industrial production, Peru monthly GDP, the BCCh’s dual traders and economists surveys, and Brazilian CPI are the Latam data highlights. Chileans vote on the new Constitution text on the 17th. Elsewhere, US CPI and retail sales, UK GDP, Chinese retail sales, industrial output, and investment, and global PMIs data await.

MARKET EVENTS & INDICATORS

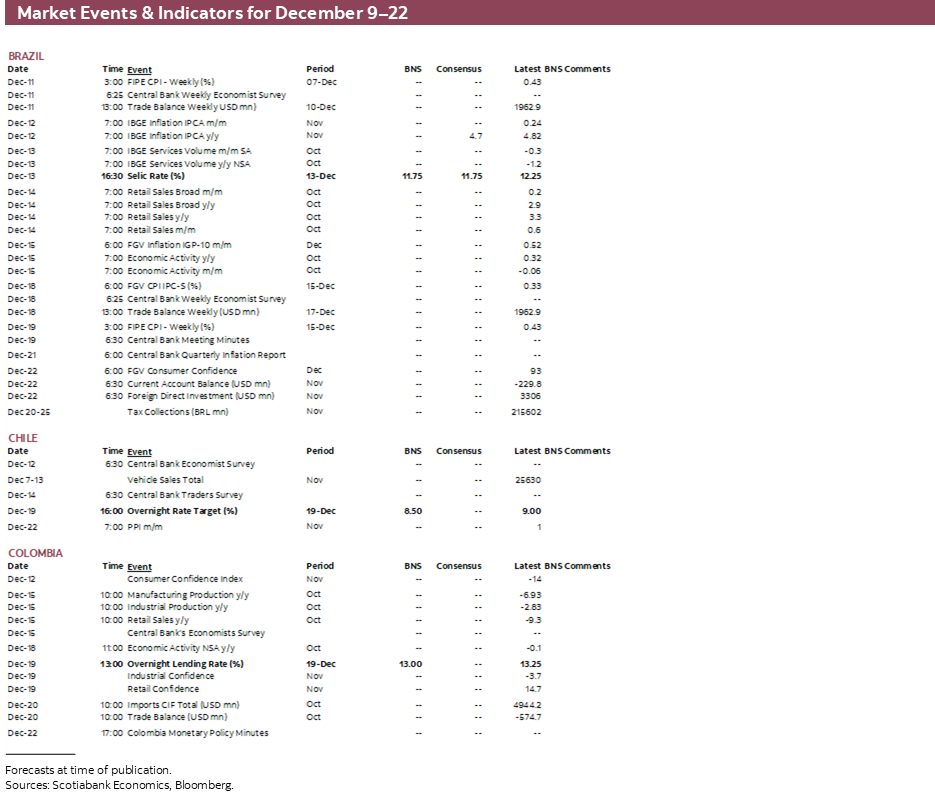

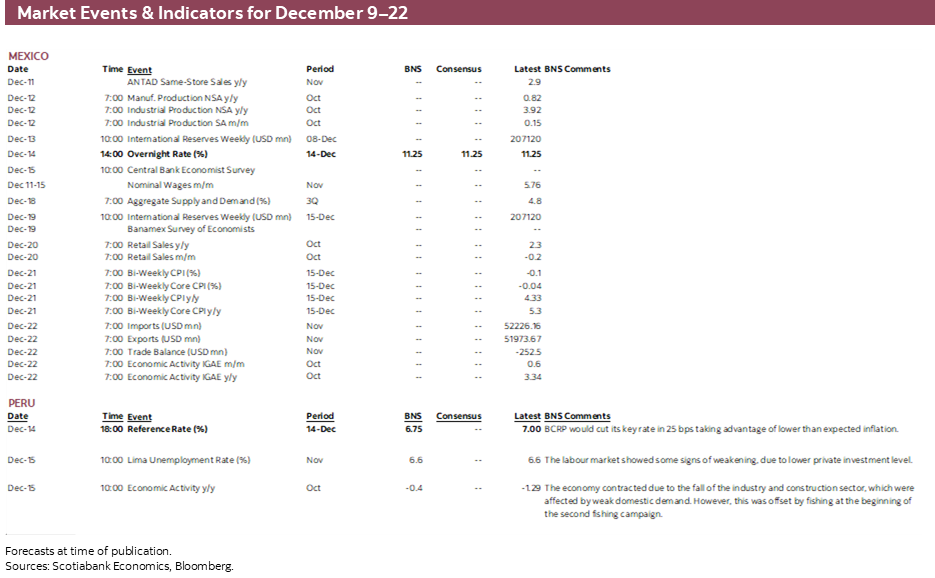

- A comprehensive risk calendar with selected highlights for the period December 9–22 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: CENTRAL BANKS PARADE

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Between now and Friday the Fed, ECB, BoE, BCB, Banxico, BCRP, SNB, Norges Bank, and PBoC will all meet and decide on policy, with recent inflation optimism prompting a sharp rally in global rates markets that has gone mostly unchallenged by officials—which partly fueled greater declines in yields.

- Among the key central banks announcing policy next week, only the BCB and BCRP are expected to move their benchmark rates, and it’s unlikely that they deviate from expected respective 50bps and 25bps cuts.

- As for Banxico, the doves in the board may firm up guidance for an earlier (February) rather than later (March) start to rate reductions. The Fed and ECB will be looking to push back against the quick increase in cuts pricing; the BoE may be more comfortable.

- Colombia retail sales and industrial production, Peru monthly GDP, the BCCh’s dual traders and economists surveys, and Brazilian CPI are the Latam data highlights. Chileans vote on the new Constitution text on the 17th. Elsewhere, US CPI and retail sales, UK GDP, Chinese retail sales, industrial output, and investment, and global PMIs data await.

This week, the BoC’s and the RBA’s as-expected decisions with little surprises quietly kicked off the last round of central bank decisions of 2023. Between now and Friday the Fed, ECB, BoE, BCB, Banxico, BCRP, SNB, Norges Bank, and PBoC will all meet and decide on policy, after recent inflation optimism prompting a sharp rally in global rates markets that has gone mostly unchallenged by officials, which partly fueled greater declines in yields.

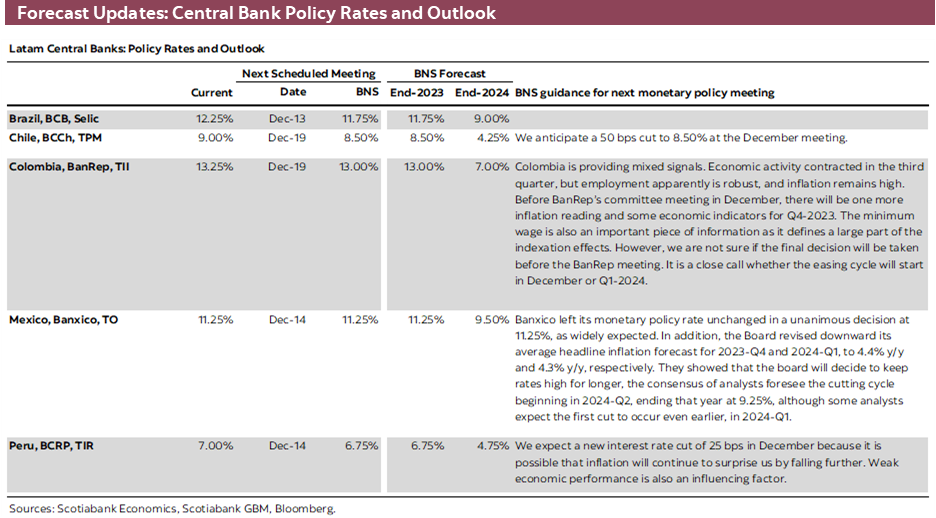

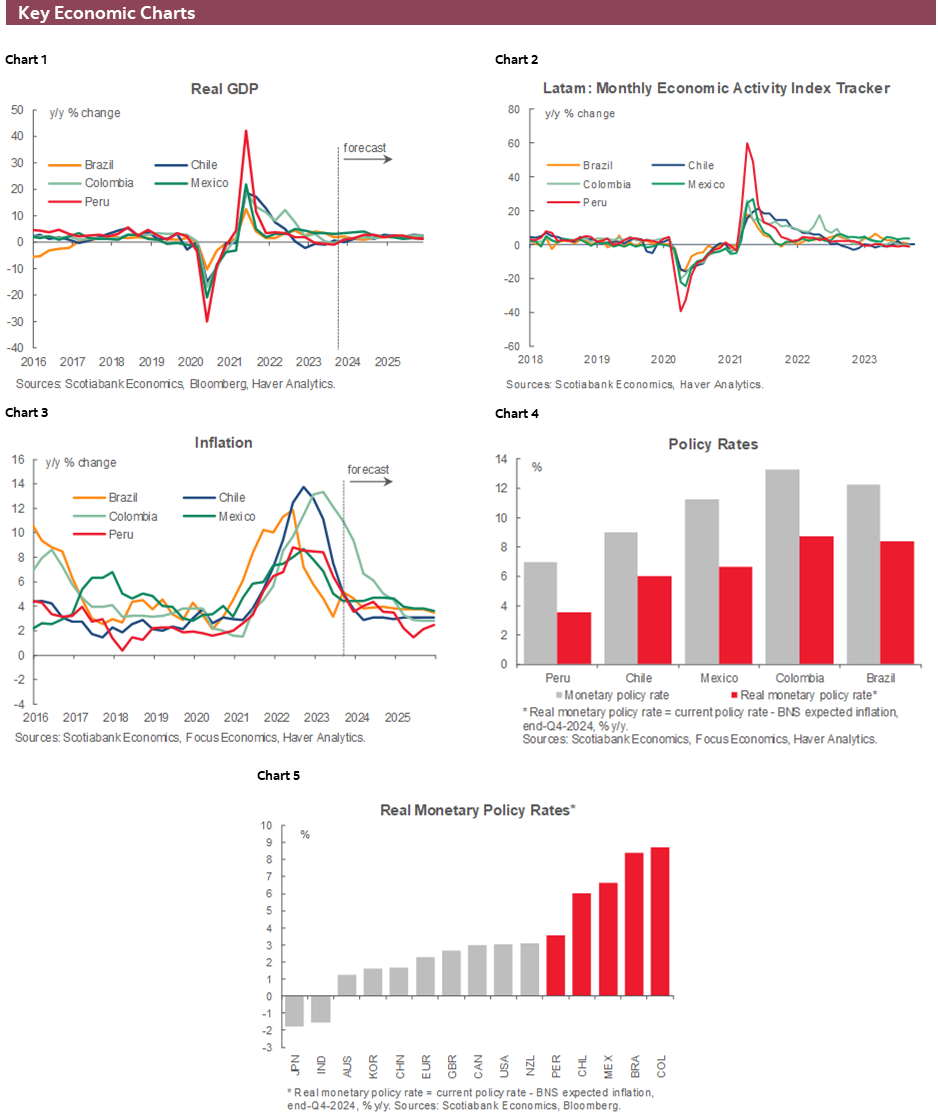

Among the key central banks announcing policy next week, only the BCB and BCRP are expected to move their benchmark rates, however. What’s more, there’s only some very slight uncertainty around the possible size of the BCRP’s cut (25 or 50bps) while the BCB is on a clearly laid-out 50bps schedule. November inflation data out on Tuesday and services volumes figures out on Wednesday ahead of the BCB’s decision are unlikely to materially change their guidance.

Throughout the week, we will preview the Latam central banks’ decisions in our Latam Daily reports. We see the BCB cutting the Selic rate 50bps to 11.75% (and another 50bps will very likely follow in February). November inflation data out on Tuesday and services volumes figures out on Wednesday ahead of the BCB’s decision are unlikely to materially change their guidance; October economic activity data closes out the week.

The BCRP looks on track to continuing its easing cycle at a 25bps pace—despite a solid November inflation miss (see here) and a weak economic performance. The day after the decision, we’ll get October GDP data that we expect will show a 0.4% y/y contraction in output due to weakness in manufacturing and construction industries against a boost from the second fishing season of the year (first one in May was cancelled); unemployment data are also out on Friday.

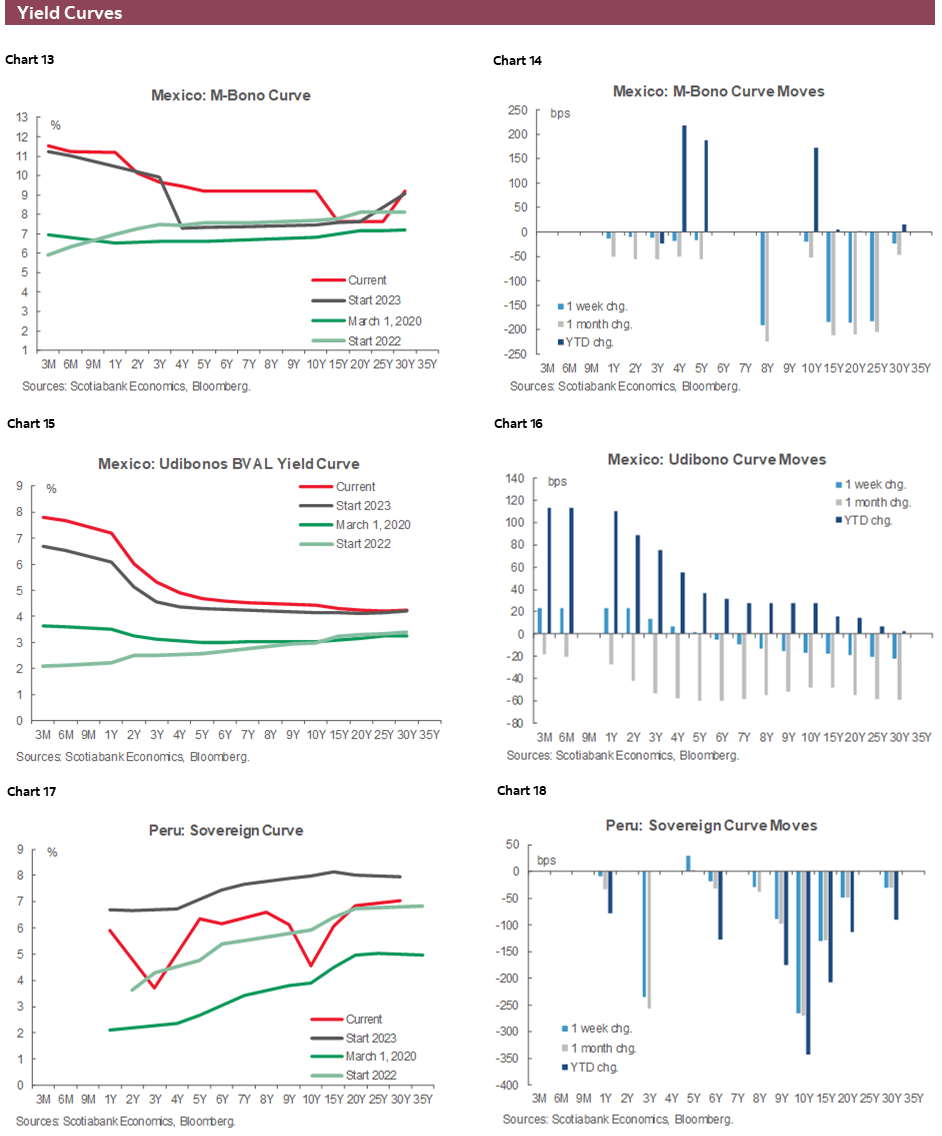

As for Banxico, the doves in the board may firm up guidance for an earlier (February) rather than later (March) start to rate cuts; at the margin, the deceleration in core inflation in November would support their view (see here). Mexican industrial production figures scheduled for a Tuesday release (markets closed for holidays) and Banxico’s economists survey on Friday should be an afterthought. We’re also watching what happens at Movimiento Ciudadano regarding who will represent them in next year’s presidential elections after Garcia dropped out to return to the Nuevo Leon governorship. On the topic of politics, Milei’s presidency in Argentina begins Sunday, the 10th.

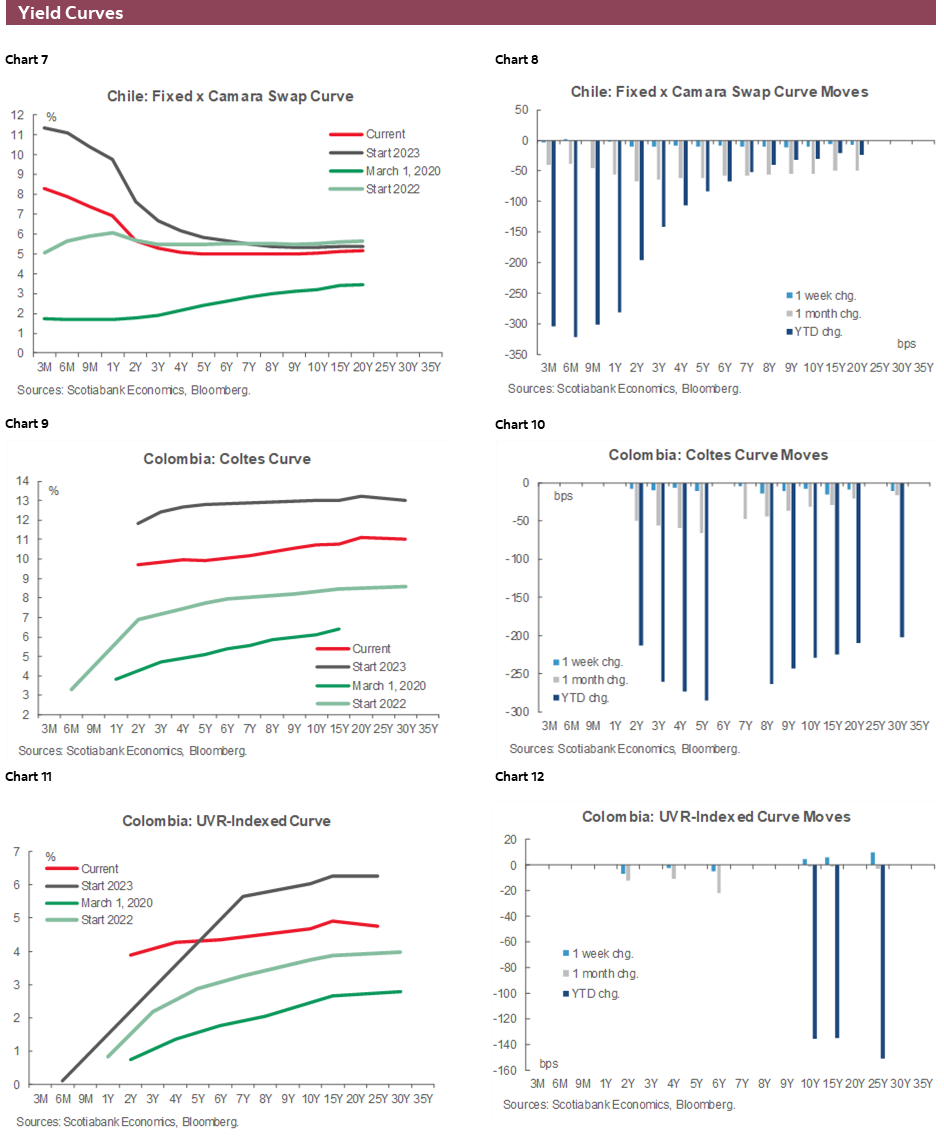

It will be BanRep’s and the BCCh’s turn the following week, on the 19th, coming after an intriguing BoJ announcement in the early hours that same day. In the case of the BCCh, November’s CPI print massively beat expectations (see here), which has led the team to revise their expectation to a 50bps reduction versus a 75bps forecast before the data. It’s likely that other analysts feel the same way—and maybe also consider changes to their projections for the January 31st decision—in the results to the BCCh’s economists and traders surveys out on Tuesday and Thursday, respectively. Recall that on the 17th, Chileans will vote on whether to approve or reject the new Constitution text; before the polls blackout period, there was no statistical certainty about which option will be the most popular.

There’s still some uncertainty around whether BanRep will begin its cutting cycle in December, more so after inflation data surprised to the upside (see here), though for now we think they will, by 25bps (but it’s a close call). We get data for manufacturing/industrial production and retail sales, and the results of BanRep’s economists survey on Friday, followed by monthly economic activity on the 18th, to help us narrow our view.

Of the remaining central banks meeting next week, some like the Fed and ECB could push back against what may be overextended cut bets in markets (~110–120bps and ~130–140bps by end-2024, respectively), while the BoE may be a bit more comfortable with market expectations (~80bps by end-2024) and not have to sound as hawkish (though it should consider itself lucky). Markets and economists are fairly confident the next SNB move will be a cut, in March, but are slightly prepared for a would-be surprise Norges Bank hike next week (Norwegian inflation out on Monday, too). The PBoC is not expected to shake things up on Friday. We also get a lot of data from outside Latam next week: US CPI on Tuesday; the BoJ’s Tankan survey, UK GDP, US PPI and IP on Wednesday; New Zealand Q3 GDP, Switzerland CPI, and US retail sales and import/export prices on Thursday; and a flood of global PMIs and Chinese retail sales, investment, and industrial production on Friday.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.