- Mexico: Inflation accelerated less than expected in November

Markets in Asia and so far in Europe have taken to reversing US-session moves on Thursday, leaving US yields higher across the board while crude oil stages a modest recovery that is on somewhat weaker footing in Europe; only US equity futures are looking flattish, at writing. We’re all waiting a few hours until the release of US NFP at 8.30ET where the median economist is expecting a 183k rise in jobs vs the 150k reported in. Watch wages growth and the unemployment rate, as well, and be wary of unpredictable U Mich survey results at 10ET. Today, Chile, Colombia, and Peru markets are closed for the holidays, so these markets will likely open abruptly to whatever moves result from today’s US data. There’s no major data of note out of Brazil nor Mexico today.

Treasurys are offered across all maturities, seeing the belly underperform, in contrast to more clearly bear steepening gilts and EGBs that partly reflect a post-Europe sell-off in the US long-end yesterday. Crude oil is up 1.5% as some bottom-fishing emerges but not enough to erase a 5% decline tracked for the week. Iron ore is up 1.1% and copper is up 0.8%. SPX futures are little changed (maybe some marginal losses in Nasdaq given rise in yields) while ESX and FTSE post solid gains of 0.8% and 0.6% that have, for the most part, taken place during European dealing rather than taking the US’s cue.

With a shakier mood in overnight trading, we have currencies ceding a bit of ground to the USD, but the MXN +0.4% and the CAD +0.2% are among the top performers today. The former is coming back from the mid-17s area that it reached yesterday but the peso’s gain on today still leaves it down 1.2/3% on the week as the worst major currency this week after the NOK (down 1.7%) and the CLP (down 1.7/8%, despite the stronger inflation data yesterday, see here).

In Mexico, political risks continue ahead of next year’s elections as AMLO readies electoral, national guard, and judicial reforms for February. Instead of waiting for the possibility that Morena’s coalition gets a 2/3rds qualified majority that would permit constitutional reforms in the 2024 elections, the Pres seems to be taking advantage of the fact that Movimiento Ciudadano has split from the (very loose) congressional opposition. Were the whole of the MC to join Morena’s alliance, this bloc would have a qualified majority in the Senate, but not in the Lower House. Still, we do not know who (if at all?) will run for the MC in 2024 after Garcia returned to the Nuevo Leon governorship. This was after he was (very briefly) replaced by a state opposition candidate—which was what put the MC over the edge to divorce its ‘allies’ in the national legislature.

We got Colombian inflation data after the close yesterday, so local markets will be unable to react to it until Monday given holiday closures today. The data came pretty much in line with expectations in headline terms (10.15% vs 10.17% medina) but the core reding exceeded estimates and surprisingly accelerated to 10.61% from 10.51% (vs 10.39% median). Note, however, that Colombia’s main ‘core’ index only excludes food while keeping energy prices. The 5%+ m/m rise in electricity costs drove a large part of this beat, but rents also accelerated and added to ex. food inflation. CPI excluding food and regulated prices fell 0.3ppts to 9.00% y/y.

Our economists in Colombia see that, all in all, headline inflation continues its gradual while core inflation sends mixed signals. The year-to-date appreciation of the COP has helped on the tradable goods inflation front, but non tradable components, especially rent fees, continue to show indexation effects, and regulated prices remain a big impediment for the convergence of inflation to target. November CPI has something for both sides of BanRep’s board. will give arguments to both sides of the board. Headline inflation should close 2023 below 10%, but hawks will point to persistently sticky core inflation. In their words, they “continue to think that the recent economic activity deceleration plus the current account deficit coming in well below BanRep expectations will give enough arguments to start a very gradual easing cycle and cut the benchmark rate by 25bps at the December 19th meeting, but we know that it will be a close call.”

—Juan Manuel Herrera

MEXICO: INFLATION ACCELERATED LESS THAN EXPECTED IN NOVEMBER

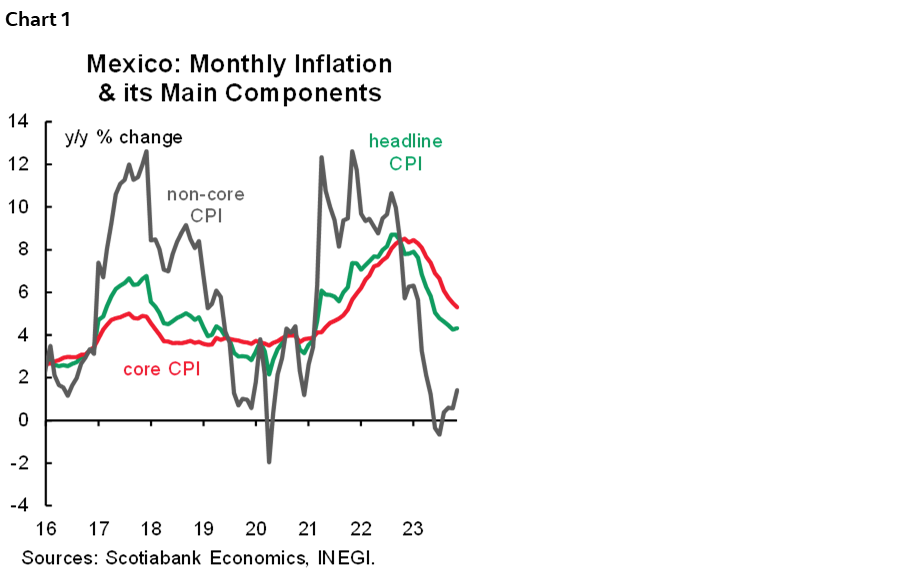

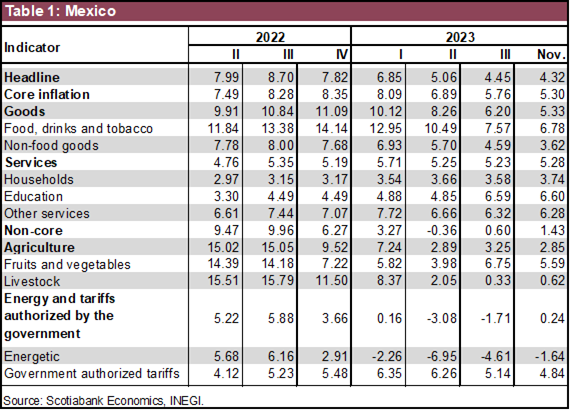

In November, inflation accelerated to 4.32% y/y from 4.26% (4.4% consensus), breaking its 13-month trend of declining (chart 1). However, core inflation moderated to 5.30% y/y from 5.50% (5.34% consensus), derived from a slowdown in both merchandise to 5.33% (5.64% previously), and services 5.28% (5.34% previously), see table 1. The non-core rose 1.43% y/y from 0.56%, with energy and government rates rising 0.24% (-0.35% previously), and agriculture 2.85% (1.62% previously). In its monthly comparison, headline inflation rose to 0.64% m/m (0.38% previously, 0.72% consensus), core inflation had a smaller increase of 0.26% m/m (0.39% previously, 0.30% consensus), with a greater pace in goods and services. Finally, the non-core accelerated to 1.81% m/m (0.34% previously).

The trajectory of non-core inflation is meeting our expectations related to upward risks for next year (chart 1), since in previous statements we mentioned that the abnormally low prints in non-core items have supported headline inflation to decelerate faster, however this might not be the case in the short term. We believe that this behaviour will continue in the coming months, leading to inflation remaining above 4.0%.

As for the core inflation, stickier dynamics remain as the main upside risk in the outlook (chart 1 again). Particularly, services have shown a strong persistence of high levels and cost pressures represent another important risk as wages continue to increase above inflation. For the next year, we expect economic activity to continue with significant increases within the first half of 2024 adding to the risk of stickiness in inflation.

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.