ECONOMIC OVERVIEW

- A mostly quiet week ahead ends with a flood of macro data in Latam and the G10 on Friday, with key activity readings out of Chile, Banxico’s quarterly report, Eurozone CPIs and U.S. PCE, and Canadian GDP all on tap.

- Market optimism built on a dovish read of Fed speakers at Jackson Hole will now have to contest with (or build off) the start of 50% U.S. tariffs on India on Wednesday, and the end of de minimis tariff-free treatment for U.S. imports on Friday. Nvidia’s results on Friday will also be key for trends in global equities.

- In today’s report, the team in Mexico discusses the latest Banxico meeting minutes that point to further rates cuts while our colleagues in Colombia highlight the domestic economy’s strength that is nevertheless centred on informal sectors with narrower benefits for public revenues.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia and Mexico.

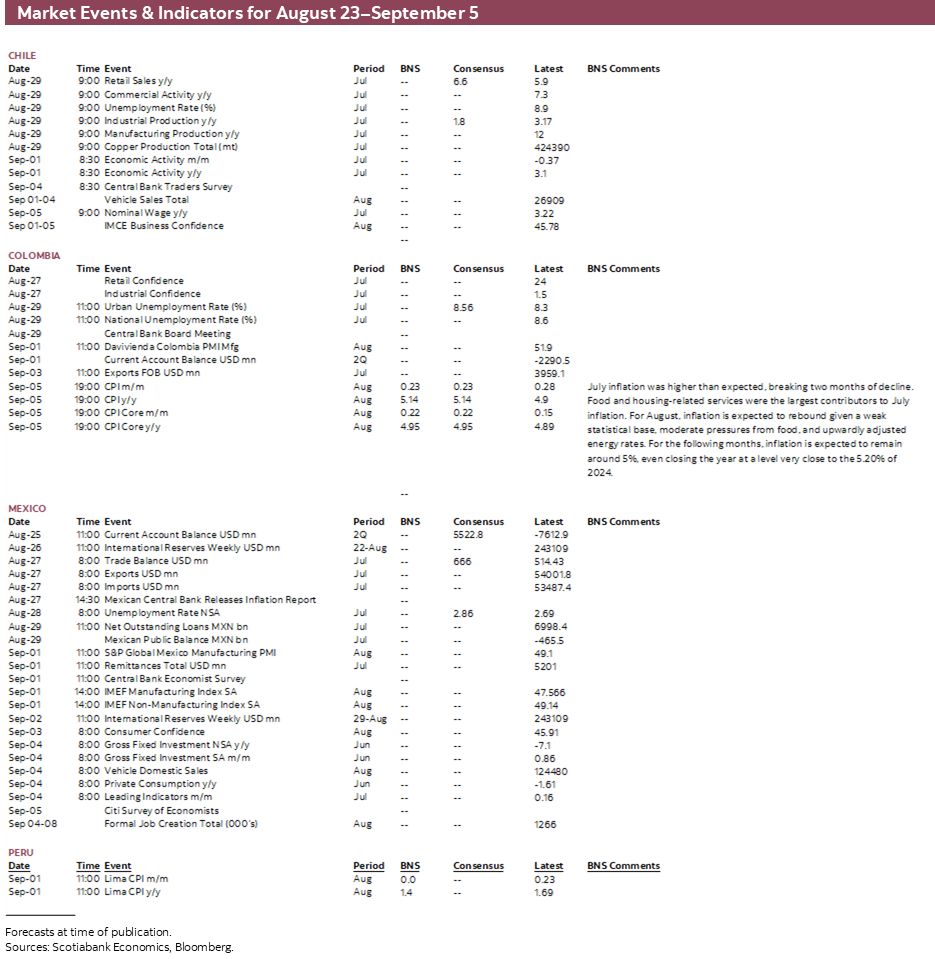

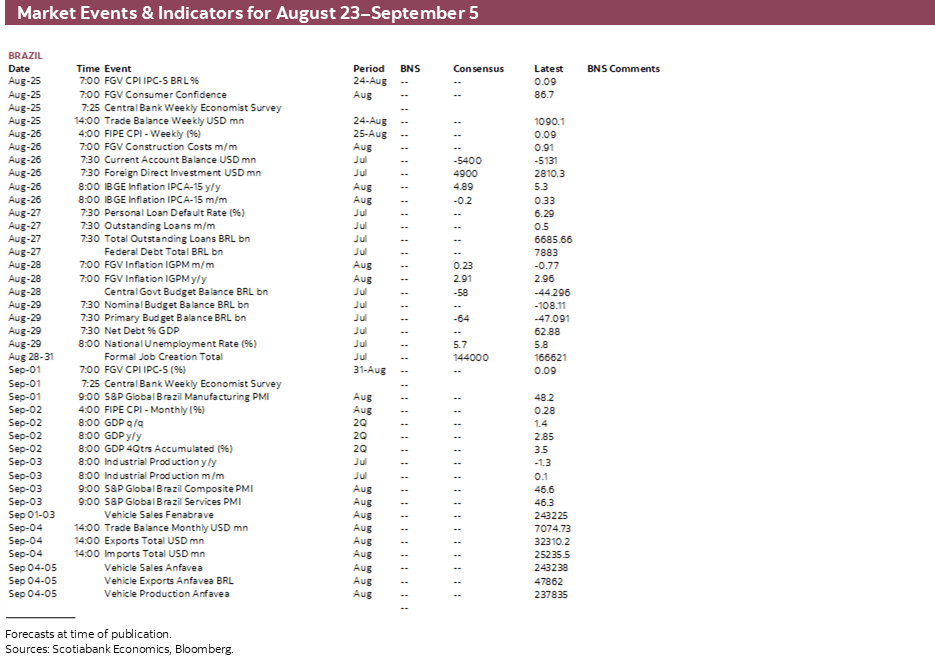

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period August 23–September 5 across the Pacific Alliance countries and Brazil.

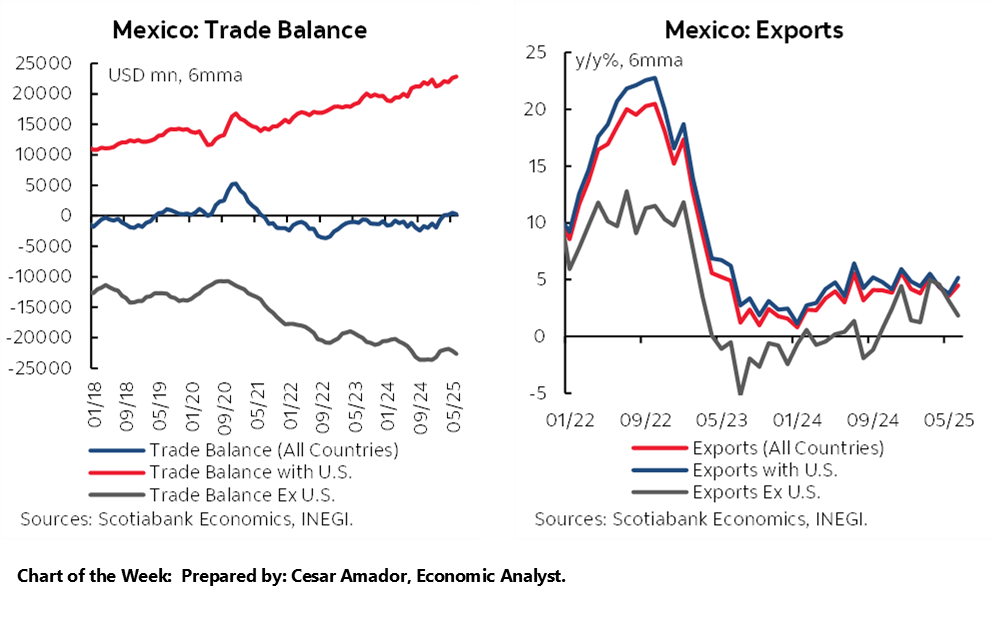

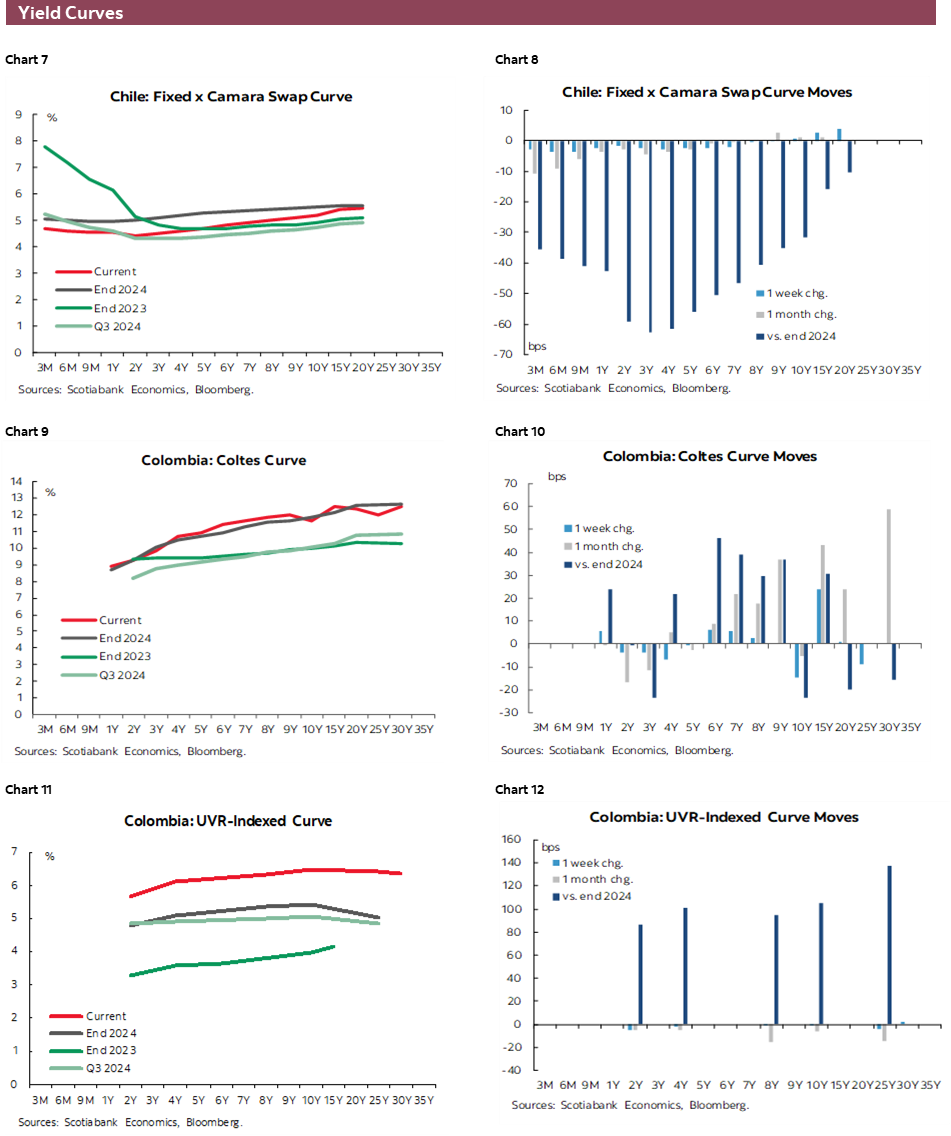

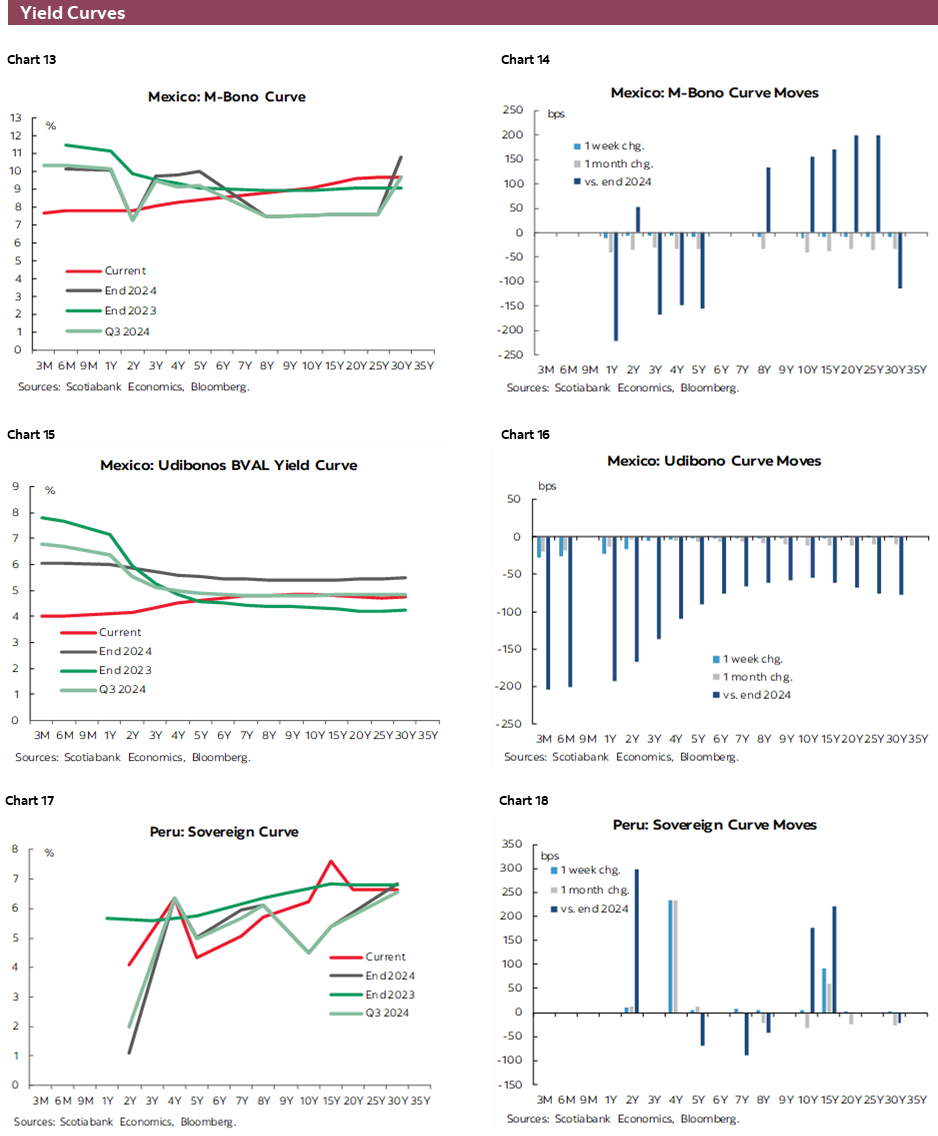

Chart of the Week

ECONOMIC OVERVIEW: TRICKY FRIDAY

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- A mostly quiet week ahead ends with a flood of macro data in Latam and the G10 on Friday, with key activity readings out of Chile, Banxico’s quarterly report, Eurozone CPIs and U.S. PCE, and Canadian GDP all on tap.

- Market optimism built on a dovish read of Fed speakers at Jackson Hole will now have to contest with (or build off) the start of 50% U.S. tariffs on India on Wednesday, and the end of de minimis tariff-free treatment for U.S. imports on Friday. Nvidia’s results on Friday will also be key for trends in global equities.

- In today’s report, the team in Mexico discusses the latest Banxico meeting minutes that point to further rates cuts while our colleagues in Colombia highlight the domestic economy’s strength that is nevertheless centred on informal sectors with narrower benefits for public revenues.

Markets are heading into the weekend with rebuilt optimism that the Federal Reserve will soon resume rate cuts, helping to lift trading sentiment that was largely downbeat through most of the week with risk on offer due to a lack of tailwinds in the lead-up to the Jackson Hole summit and Powell’s (eventually more dovish than expected) speech on Friday. Canada’s move to remove retaliatory tariffs on some U.S. imports was also a positive development on the trade front, but we’ll still watch whether the U.S. goes ahead with scheduled 50% tariffs on India on Wednesday and the end of de minimis tariff exemptions on Friday.

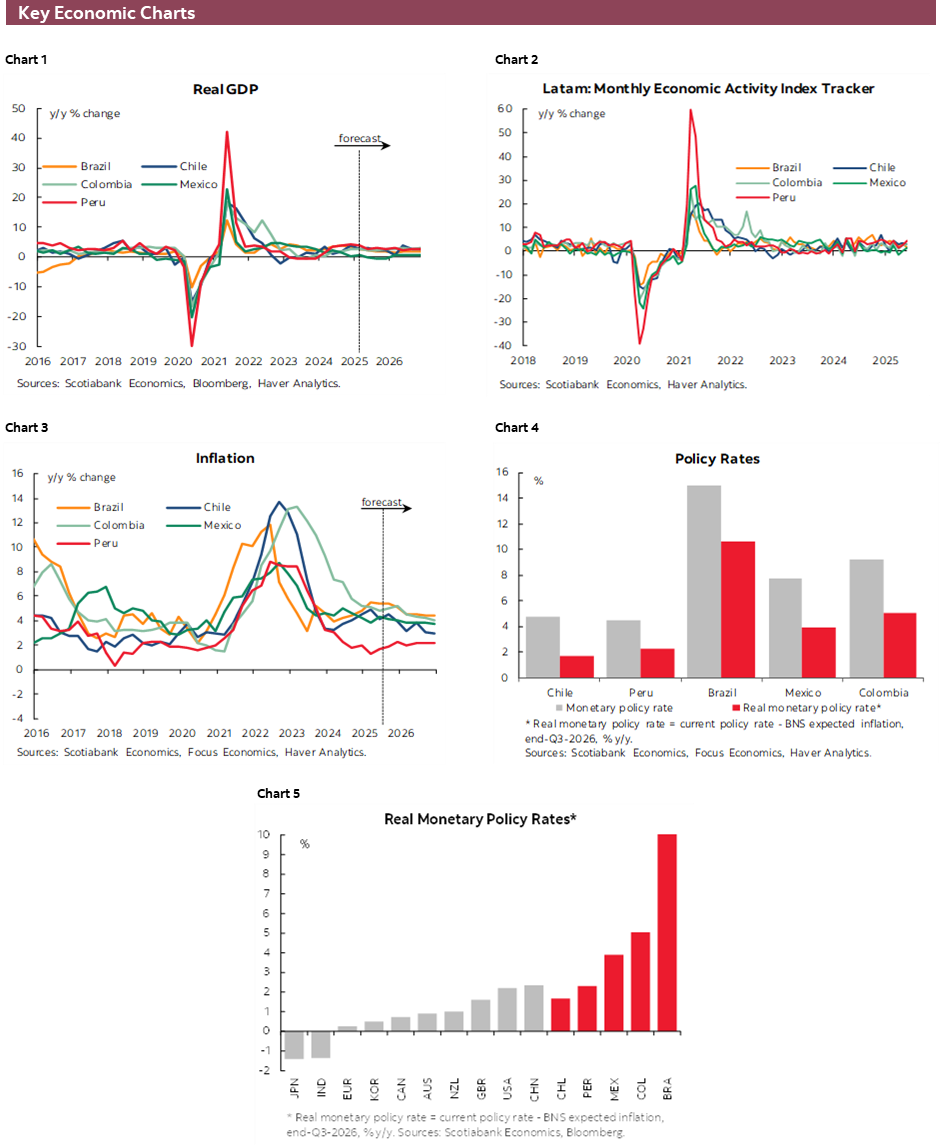

In Latin America, Thursday’s surprise resignation of Chilean FinMin Marcel shook up local markets that have since somewhat calmed but may remain cautious in the near-term for what Grau, his replacement, may imply for the 2026 budget plan—with an eye on the first round of presidential elections in mid-November. On the flip side, 2Q growth data were solid, in contrast to Peru’s which while strong left some to be desired in the details (see Latam Daily).

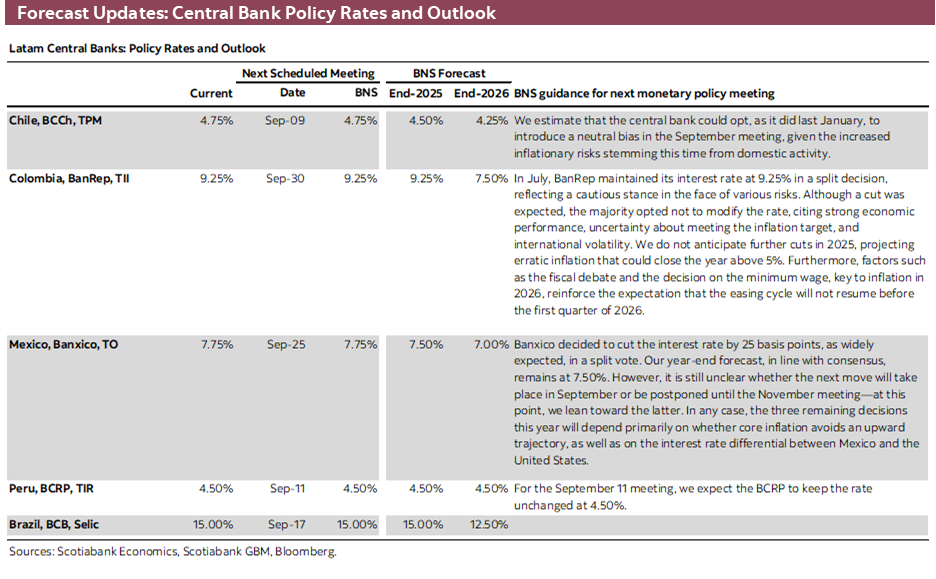

Mexican data, from soft retail sales to downside surprises in June’s economic activity and mid-August inflation (see here), combined with a more dovish feel to Fed speakers throughout the week, have firmed expectations for another rate cut at Banxico’s September announcement. In today’s report, the team in Mexico discusses the latest Banxico minutes. Although the minutes touched on the discussion of recent core merchandise inflation pressures, most in the board seem inclined to continue quarter-point moves which opens some downside risk to our 7.50% year-end call for Banxico’s policy rate. Next Friday’s quarterly report will provide more clarity on the path for rates.

Next week is shaping up to be a quieter one as far as on-calendar events are concerned in Latam and the G10, especially over the first half of the week, with busier Thursday and Friday schedules closing out the month. Briefly, in the G10, Friday’s U.S. PCE and German, French, Italian, and Spanish HICP, and Canadian 2Q GDP are the highlights, joined by U.S. durable goods orders and the second release of 2Q GDP, and RBA and ECB meeting minutes earlier in the week. Markets also await Nvidia’s results on Wednesday. The U.K. is closed on Monday for holidays.

In Latam, Chile’s INE has its usual once-a-month flood of macro figures on Friday, with retail sales, manufacturing/industrial production, commercial activity, copper output, and unemployment rate data on tap. That same day Banxico will publish its quarterly report, after Wednesday’s international trade and Thursday’s unemployment rate figures out of Mexico. Colombia has only jobless rate data on tap while BanRep officials hold a non-rates-setting meeting, both on Friday, while Peru takes it easy with an empty schedule. Brazil’s mid-month CPI readings on Tuesday are expected to show headline inflation falling below 5%, possibly lifting market bets on the BCB starting cuts before year-end.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Consumption Rebounds as the Government Advances its Debt Strategy

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

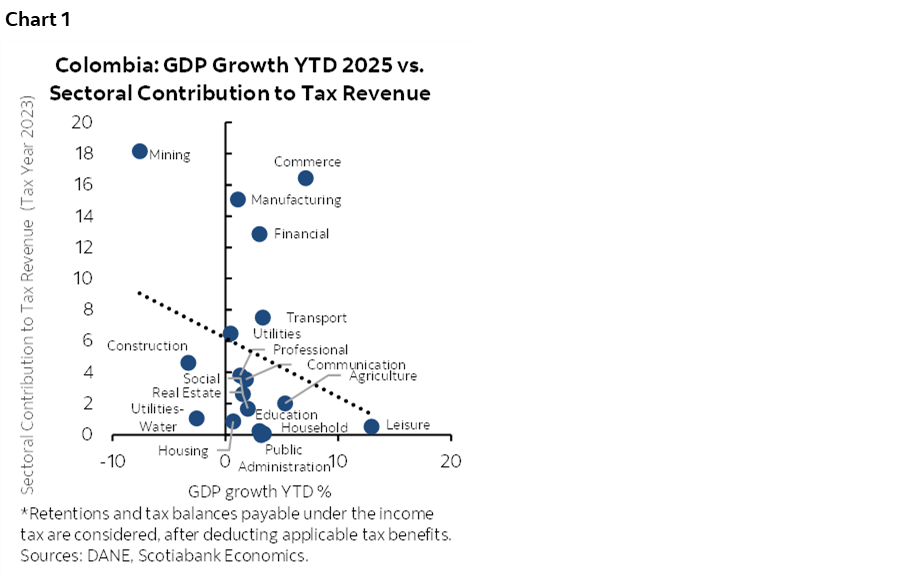

Last week, second-quarter GDP figures were released, confirming the momentum of domestic consumption (see here). The economy is estimated to have grown 2.1% y/y (2.5% y/y seasonally adjusted), driven by both private and public spending, with positive impacts on sectors such as retail and entertainment.

The published data reveal disparities in Colombia’s economic performance, particularly in two areas: the potential sectoral composition of tax revenue and the economy’s growth potential. This year, economic momentum has been driven by sectors with low tax contributions, contrasting with the contraction in industries such as mining and construction, which are key sources of fiscal revenue (chart 1). This trend may pose an additional risk, as growth is increasingly concentrated in informal segments with limited impact on tax collection.

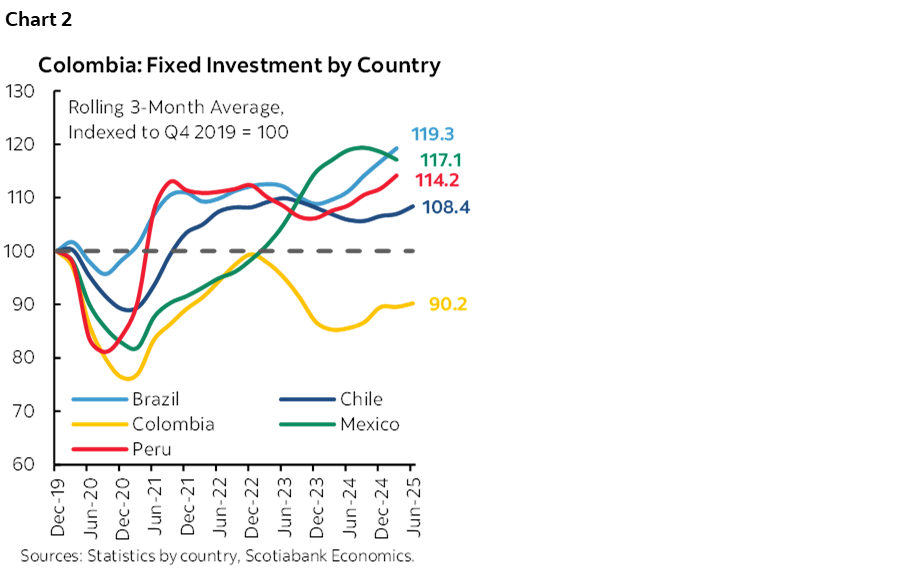

On the other hand, fixed investment remains sluggish, affected by contractions in sectors such as construction and mining, as evidenced by comparisons to other countries in the region (chart 2). Relative to pre-pandemic levels, Colombia shows a lag of nearly 10%, with investment rates between 16%–17% of GDP, below the historical average of 22%. According to estimates from the central bank, this loss in productive capacity may have reduced potential growth by approximately one percentage point, from an average of 3.5% before the pandemic to 2.6% today.

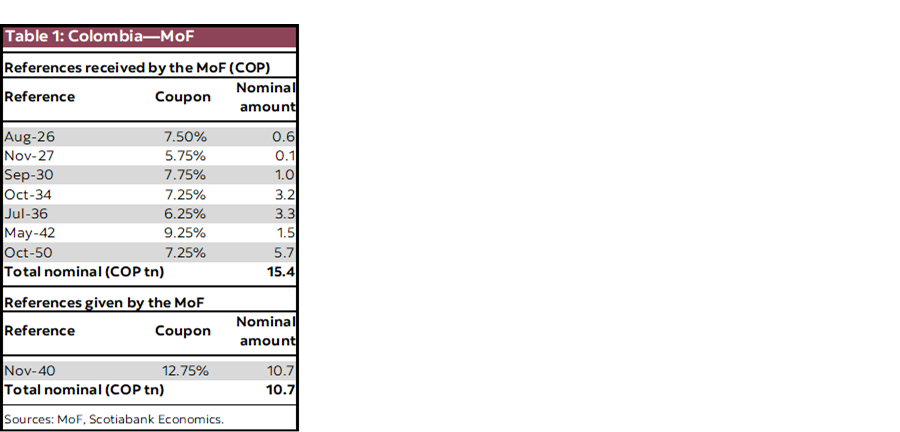

Meanwhile, the Ministry of Finance continues to advance its debt strategy aiming to reduce interest burdens and improve debt-to-GDP indicators. During the week, the fifth public debt swap was announced for COP 27 tn, in which Public Credit repurchased COP-denominated securities worth COP 15.4 tn at high discount rates, and in exchange issued new COP-denominated bonds maturing in 2040 (table 1). Additionally, US $2,958 bn in external bonds were repurchased.

As a result of the operation, the nominal balance of domestic public debt fell by COP 4.8 tn, while external public debt decreased by COP 11.8 tn. However, this reduction is temporary, as the government plans to issue new external debt in other currencies. So far this year, debt management operations have totaled COP 63.4 tn and have led to a reduction of COP 24 tn in the domestic debt outstanding (equivalent to 1.3% of GDP, comparable to a tax reform). Meanwhile, markets remain cautious amid rising refinancing and liquidity risks.

Mexico—Banxico Minutes Reinforce Outlook for Further Rate Cuts Amid Mixed Inflation and Growth Signals

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Banxico’s monetary policy meeting minutes revealed a Governing Board largely inclined to repeat 25 basis point rate cuts at least once more during the three remaining meetings of the year. Broadly speaking, the members’ arguments revolve around three key themes:

1. The recent inflation path, which, despite recent upticks, remains below pandemic-era levels.

2. Slack conditions and weak economic momentum, which continue to support lower inflationary pressures.

3. The relative monetary policy stance, particularly the interest rate differential with the Federal Reserve.

In this context, several members see space to continue with rate adjustments in upcoming meetings. Moreover, recent developments may support this view:

1. Lower-than-expected inflation in the first half of August,

2. Weak Q2 GDP growth, and

3. Powell’s comments hinting at potential rate cuts.

However, Deputy Governor Heath dissented, arguing that upward revisions to core inflation forecasts suggest its persistence has been underestimated. He also noted challenges in consolidating a downward inflation path, recommending greater caution until clearer progress toward the 3.0% target is observed.

We partially agree with his arguments, especially given the highly uncertain environment. Therefore, we maintain our year-end forecast for Banxico’s rate at 7.50%, though we acknowledge a high probability of additional cuts.

Additionally, the minutes highlight comments on the Mexican economy, which grew 0.6% quarter-over-quarter in Q2 (seasonally adjusted), below the initial 0.7% estimate. Some members noted external demand showed some expansion, possibly due to the front-loading of exports to the U.S. in response to tariff policy changes. Investment remains on a negative trend, while consumption—though resilient—faces challenges amid a slowing labour market.

On inflation, the latest reading supports the Board’s dovish stance: headline inflation in early August surprised to the downside at 3.49% vs. 3.63% expected. Most of the decline was due to a double-digit drop in fruit and vegetable prices, but core inflation also eased slightly from 4.26% to 4.21%.

Within core inflation, goods slowed to 3.97%, while services rose to 4.43%. One member attributed the deterioration in goods to a lagged effect of peso depreciation earlier this year; another linked it to early purchases amid global trade disruptions. A third noted that services inflation reacts more slowly, so economic weakness is not yet fully reflected. Regarding non-core inflation, one member warned that its decline is highly reversible in the short term. Most agreed that U.S. trade policy has created uncertainty around inflation expectations.

On the monetary policy, some arguments for further cuts focused on the rate differential with the U.S. One member saw room for more easing due to the peso’s recent appreciation. Another emphasized that both economies are in different phases of the cycle, and the current differential is above the historical average.

In contrast, another member—likely Heath—argued that the upward bias in inflation risks could delay convergence to the 3% target until Q3-2026. He also noted that U.S. economic resilience and higher-than-expected inflation have strengthened expectations of more moderate Fed cuts, limiting Mexico’s room for easing. In this context, the comments reinforced expectations of a Fed rate cut in September, though uncertainty remains about the timing and magnitude of future moves.

Based on the minutes and Friday’s GDP data, we reaffirm our expectation of a 25 basis point cut at Banxico’s September meeting, likely with a split vote. However, future decisions will depend on clearer signs of a sustained decline in core inflation and the Fed’s stance for the rest of the year. For now, we maintain our year-end forecast at 7.50%, with a dovish bias, given the improved inflation risk balance and the uncertain environment that could negatively impact both the domestic and global economy.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.