- Tensions in the Middle East are generating significant uncertainty for the global economy. Even if the present ceasefire holds, higher oil prices are likely to persist.

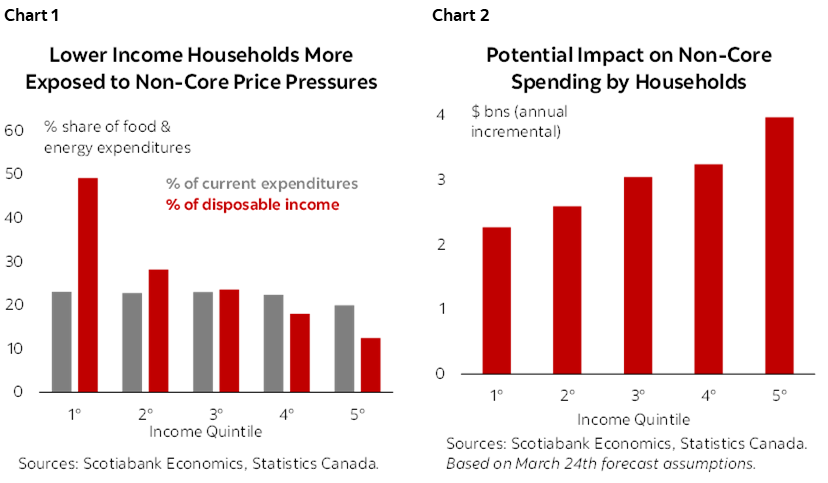

- Canada’s net energy exporter status should help offset macro headwinds, but higher energy prices impose important distributional costs. Lower income household spending is disproportionately skewed towards essentials with limited flexibility to absorb price shocks and lower lifts from wage income (chart 1).

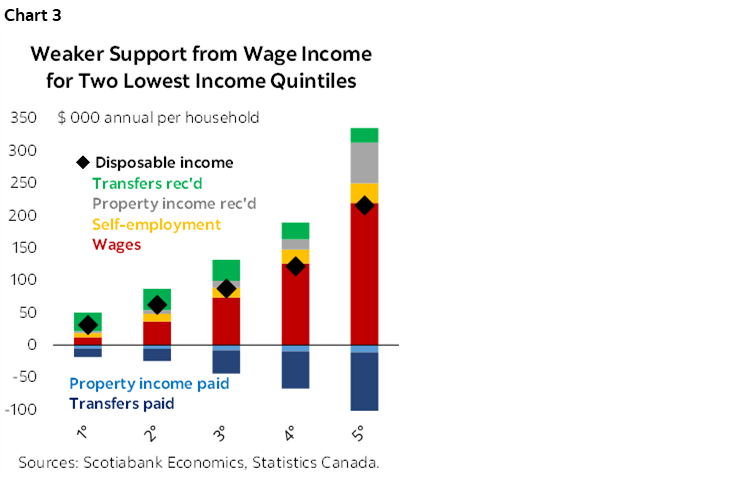

- A sustained increase of US$10 per barrel in WTI could result in an additional $1 bn in annual expenditures on food and energy for Canada’s two lowest income quintiles. Under our current economic projection—where the conflict drives up CPI by roughly one ppt relative to a pre-war baseline—this would equate to an incremental price shock totaling $5 bn for these households (chart 2).

- The macroeconomic context does not call for a broad-based stabilization effort given the broader tailwinds from the terms-of-trade shock, but there is a reasonable case to provide targeted relief to those least able to cope with the immediate impacts of the price shock. Even offsetting in full the impact on those bottom income quintile households would not materially change the growth and inflation outlook.

- Canada is well placed to respond with targeted fiscal support. Inflation-driven revenue gains and an existing delivery channel—the GST Groceries and Essentials Benefit—give the federal government scope to provide timely, well-targeted relief but should do so within its broader fiscal framework that would still balance the operational balance within three years.

- Going forward, indexing targeted transfers to essentials could improve resilience and policy coherence. Linking GST rebate payments to food and energy inflation could help protect vulnerable households, improve timeliness, and reduce risk of policy missteps, while complementing monetary policy by addressing distributional effects of energy price shocks.

THE AGGREGATE

The economic consequences of the conflict in Iran remain highly uncertain. Although tensions have eased for now with the tentative ceasefire, elevated oil prices are likely to persist. The impacts will vary around the world, reflecting each region’s energy dependence, trade exposure, and underlying economic fundamentals.

Canada’s status as a net energy exporter puts it in a comparatively strong position. The country stands to gain from a positive terms-of-trade shock, which could boost national income through increased revenues in the resource sector and an improved trade balance. These advantages should help counterbalance the adverse effects stemming from broader uncertainty and tighter financial conditions. As detailed in our latest forecast update, these offsetting forces leave the net impact on growth broadly neutral, but inflation is expected to run about one percentage point higher this year than in our pre-war baseline.

The geopolitical context is nevertheless highly volatile and unpredictable. To help navigate this uncertainty, we earlier outlined simple rules of thumb: each sustained US$10/bbl increase in WTI is estimated to raise Canada’s CPI by roughly 0.2 percentage points, largely through non-core components such as energy and food.

THE PROBLEM WITH AVERAGES

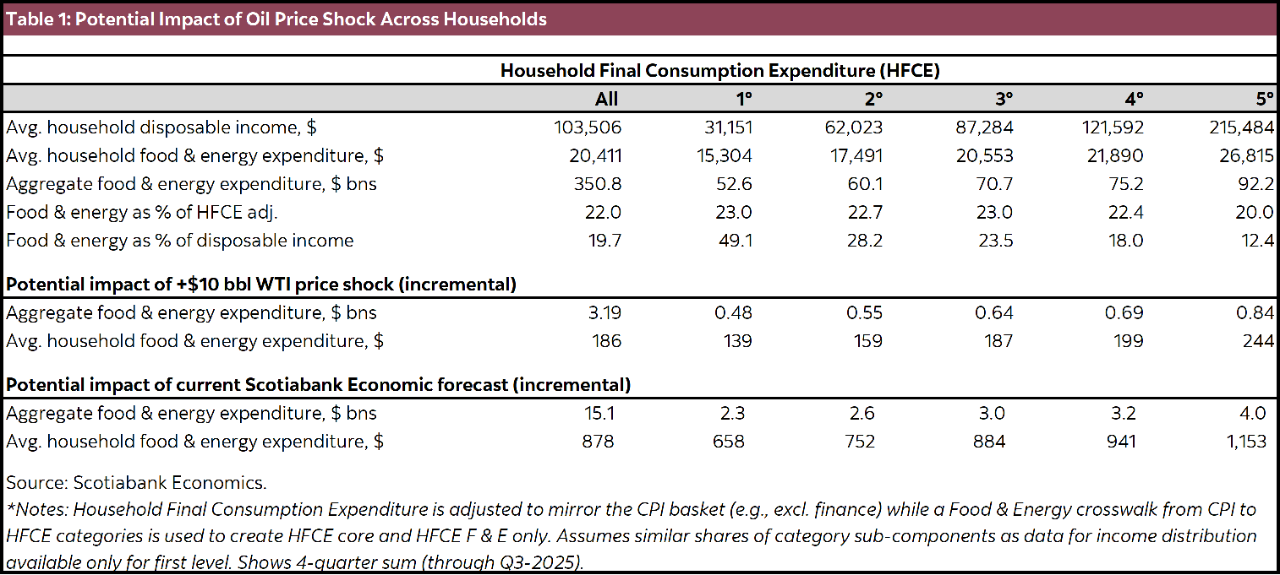

Although Canada’s net gains from higher oil prices skew positive, they conceal meaningful distributional pressures. Higher energy and food prices disproportionately burden lower‑income households. While essentials make up only a slightly larger share of their consumption basket (~23%), the regressive impact is stark relative to disposable income where the lowest quintile spends almost half of disposable income on food and energy versus under 20% for the average household leaving limited flexibility to adjust. The lowest two income quintiles face heightened vulnerability with wages making up less than a quarter of total income for the lowest group, and under half for the second lowest (chart 3).

Applying our oil shock sensitivities across households can put an order of magnitude to that impact. Each sustained $10/bbl increase in oil price shock could drive an incremental $1 bn hit in food and energy costs to Canada’s lowest two income quintile. Each sustained 0.2 ppt rise in CPI—primarily in non-core items—would translate into an extra $3 bn spent annually across all households. For those lowest income quintiles, this incremental $1 bn would translate into an additional ~$150 per household (table 1).

Scaling these estimates to our latest forecast suggests a total impact of about $5 bn for those two lowest quintiles. These approximations are highly stylized as they do not account for behavioural changes or demand elasticity—though these would be relatively low for essentials—rather these rules of thumb are intended to inform the debate.

TO RESPOND OR NOT RESPOND

Prime Minister Carney has indicated he is weighing options to offer consumer reprieve. From a broader macroeconomic perspective, the current context does not call for a broad-based stabilization program. The economy continues to operate in excess supply and uncertainty persists, but the nature of the current oil price shock should be directionally supportive. There is however merit in considering targeted support to those least able to cope.

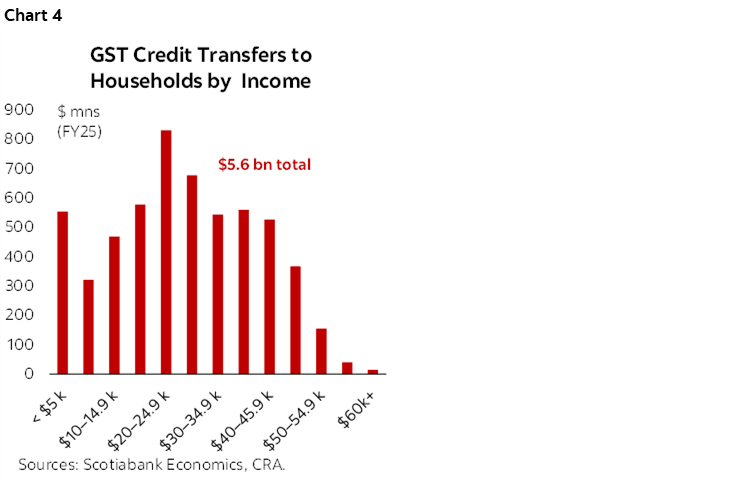

The federal government already has an established mechanism to administer timely and targeted relief. The GST rebate—recently rebranded as the GST Groceries and Essentials Benefit—is a refundable tax credit delivered as a cash transfer to low‑ and modest‑income households on a quarterly basis. Last year, $5.6 bn was transferred to lower income households (chart 4).

This transfer was recently enhanced. In January, the PM announced a one-time $3.1 bn top-up to the GST Groceries and Essentials Benefit which is expected to reach households “no later than June”, alongside a 25% increase for five years. These measures, however, pre‑date the Iranian conflict and were designed to respond to the disproportionate burden of essentials price inflation on lower‑income households arising from pandemic era supply chain disruptions and the war in Ukraine (chart 5). At the same time, the repeal of the federal fuel charge has likely left the lowest two income quintiles worse off—by roughly $3 bn on net—as redistribution of the fiscally neutral levy was highly progress.

Given the current landscape of forward-looking risks and persistent price pressures, the federal government could reasonably undertake additional targeted support without undermining its macro or fiscal position. According to Scotiabank Economics’ modelling, even at the extreme—a near-term transfer that fully offsets non-core price inflation for the bottom two income quintiles—would have a near negligible macro impact, even with a high marginal propensity to consume. A one-time boost in government transfers (in the range of $5 bn) would increase GDP by less than 0.1%. While low income recipients are likely to spend more of the extra cash, even doubling the multiplier would still leave effects marginal. And with the economy expected to remain in excess supply for the foreseeable future, this small boost could even be beneficial from a macro standpoint.

Overall, the bandwidths around the impact of such an additional top-up would not materially alter the overall growth or inflation outlook but could meaningfully enhance the resilience of households at lower incomes. The government is also poised to benefit from increased revenues driven by the positive nominal GDP shock (and a stronger hand-off into 2026). Finance Canada sensitivities, for example, suggest a positive 1 ppt GDP inflation shock could bolster net revenues by about $2.3 bn the first year. They should however undertake any additional spending (outside a full-blown crisis) within the context of the current fiscal framework that would balance the operational balance within three years.

There are some calls for cutting gas taxes with several European countries temporarily suspending fuel levies. While such measures are broad‑based and highly visible—and would offer some near‑term relief to low‑ and middle‑income households, who spend a larger share of their income on transportation—they are also regressive, delivering the largest benefits to higher‑income households with greater fuel consumption. They also blunt price signals, weakening incentives to conserve fuel or switch to alternatives. More importantly, once implemented, fuel tax cuts tend to be politically difficult to unwind.

TO DEBATE OR NOT DEBATE

In an increasingly shock-prone world, the government could shore up the responsiveness of this tool by indexing it to essentials. Namely, the GST rebate quarterly payments could be indexed to transparent, publicly-available measures of food and energy price inflation. This would allow the rebate to adjust mechanically as these essential prices rise or fall. Properly designed, it could function as an automatic stabilizer, reducing the need for ad‑hoc political intervention during energy and food price spikes. In a volatile geopolitical landscape, a rules-based mechanism that households can depend on could help improve resilience.

A potential drawback is that automatic stabilizers are designed to cushion cyclical swings whereas rising commodity prices reflect positive terms‑of‑trade developments that support aggregate income and consumption. Broad‑based transfers that rise mechanically with oil prices, risk amplifying the consumption cycle, working against the stabilizing intent. However, because the GST rebate is tightly targeted to lower‑income households such a measure may help offset distributional impacts without materially amplifying procyclicality. Some may also contend that it further increases the labour tax wedge; however, this issue is most effectively addressed within the framework of comprehensive tax reform that takes into account broader policy objectives. Moreover, given the cyclical and temporary nature of the incremental support, the impact on work incentives would likely be limited.

Such a mechanism could also strengthen complementarity between fiscal and monetary policy. By delivering targeted transfers to low- and middle-income households, fiscal policy can address the distributional consequences of rising energy costs—something monetary policy is ill-suited to do. This would allow the Bank of Canada to focus on aggregate macroeconomic dynamics and keeping inflation expectations anchored, with less concern about the distributional effects of energy price shock and/or of its own policy actions.

A SMOOTHER PATH FORWARD

This does not diminish the ongoing necessity of making investments that foster sustained economic growth while maintaining fiscal discipline. An effective fiscal framework should offer the flexibility to adapt throughout the business cycle, with automatic stabilizers playing a key role in mitigating cyclical fluctuations and reducing the risk of policy missteps. Given the unique characteristics of the current shock, alongside the federal government’s robust fiscal position and inflation-driven revenue gains, there should be capacity to provide timely, targeted support that is proportional, targeted, temporary, and firmly rooted in economic principles within the current fiscal framework. Against a highly uncertain outlook ahead, there should be serious consideration to calibrating the tool automatically to the landscape to ensure that support is deployed swiftly and effectively precisely when the most vulnerable Canadians need it most.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.