- Iran war lifts oil prices and uncertainty, but baseline macro impact remains contained. We assume tensions ease around mid‑year, with oil prices remaining elevated through Q3 before gradually easing. While the net macro impact on Canada is broadly neutral due to offsetting forces, oil prices remain the key source of uncertainty and skew inflation risks to the upside.

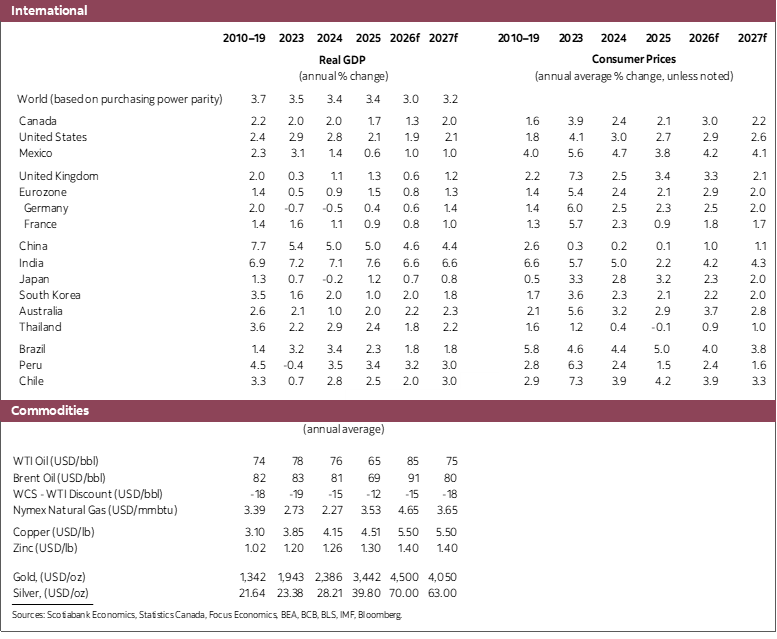

- US growth slowing, inflation risks constrain Fed easing. US activity continues to decelerate as labour markets soften and equity market support fades. We expect growth to average 1.9% in 2026 before improving modestly in 2027. Higher oil prices and sticky inflation pressure lead us to expect a cautious Fed, delivering one rate cut this year and one in 2027 before pausing around 3.25%.

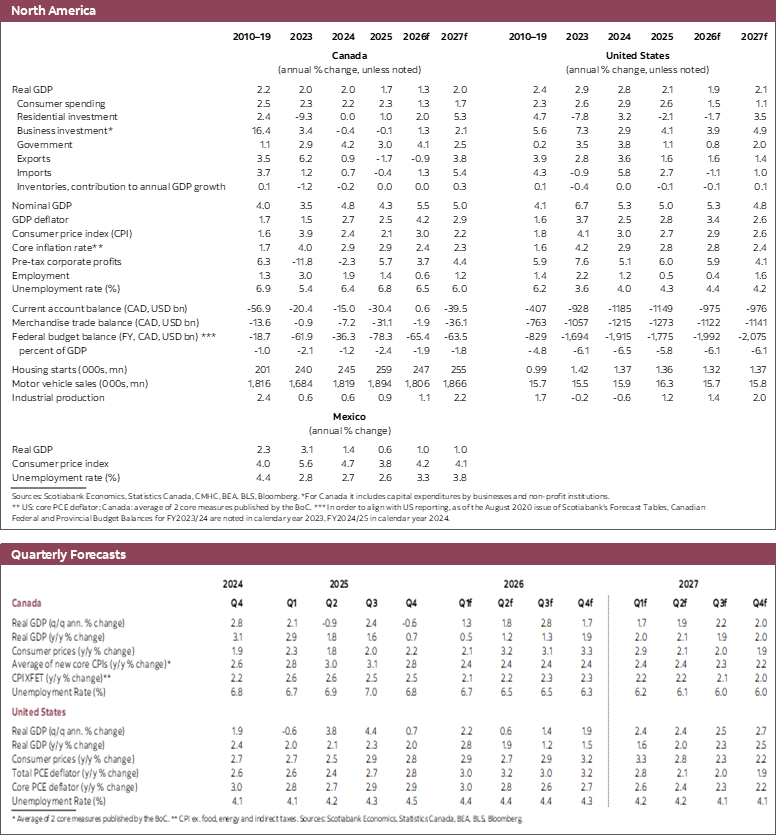

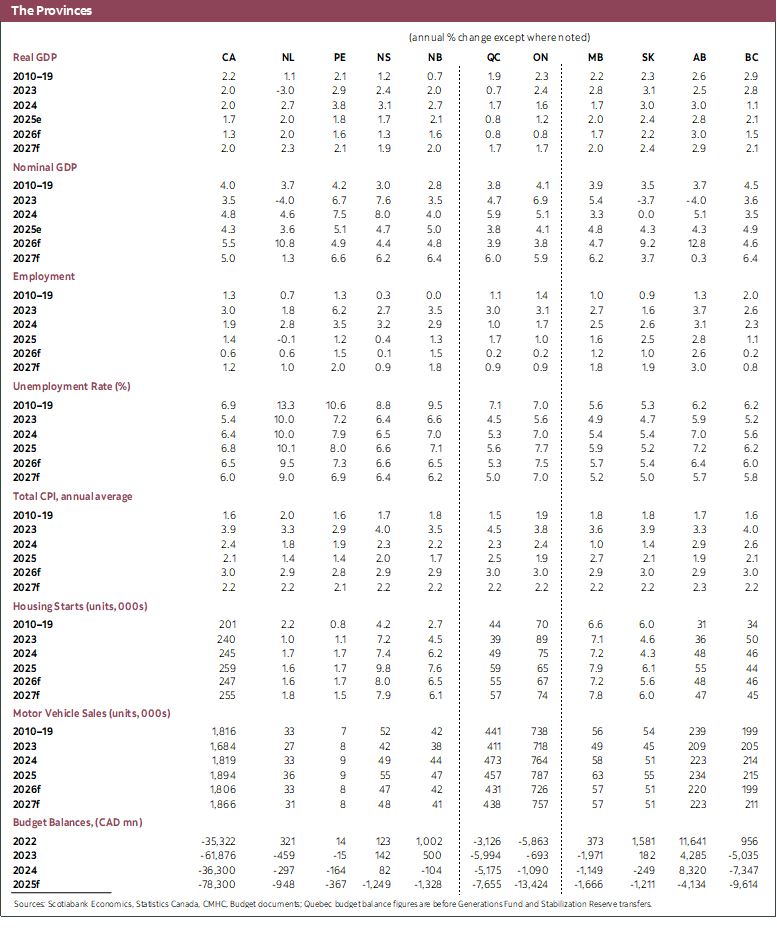

- Canada hits a soft patch in early 2026, but recovery remains intact. We now expect weaker growth in early 2026, with average GDP growth revised down to 1.3% for the year, reflecting soft labour and trade data at the start of the year. Growth is projected to rebound to 2.0% in 2027, supported by fading trade headwinds, lagged rate cut effects, fiscal support, and a recovery in exports.

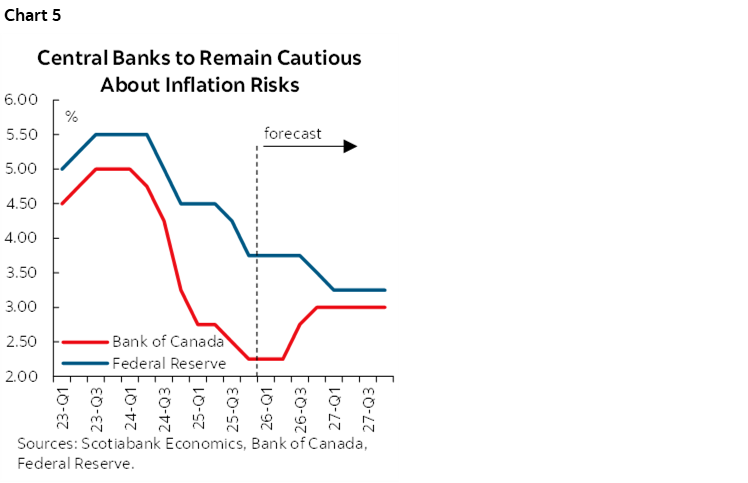

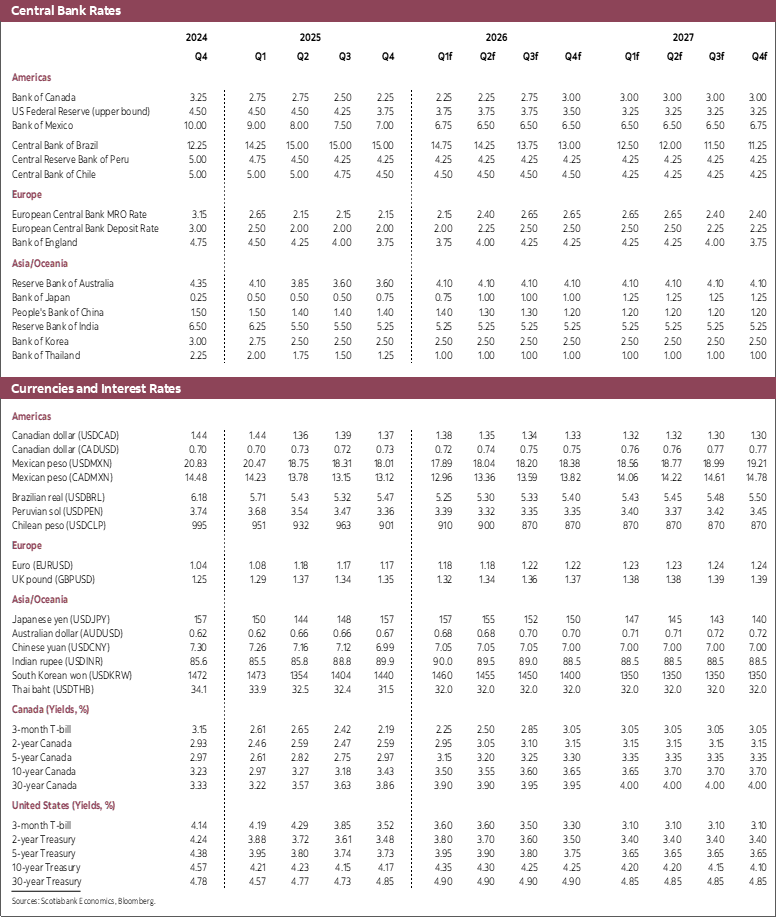

- BoC retains a tightening bias amid asymmetric inflation risks. While near-term activity has softened, higher oil prices tilt inflation risks upward. We expect the BoC to remain on hold in the near term, but to begin removing monetary stimulus later this year, hiking three times in the second half of 2026.

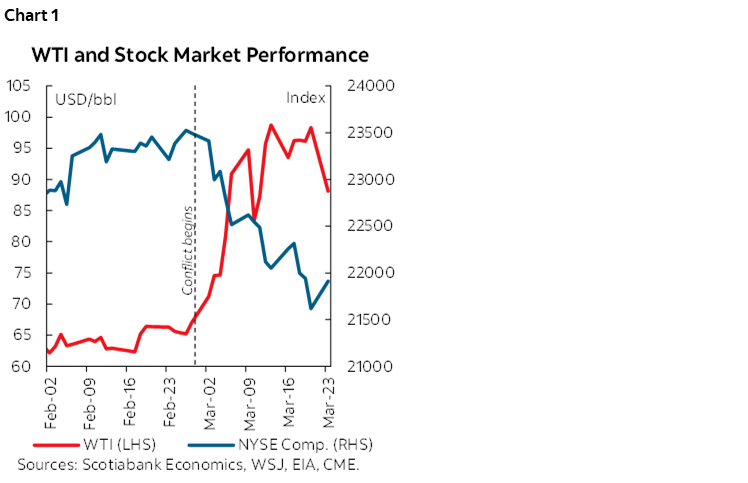

Oil prices have jumped sharply following the outbreak of the Iran war, pushing benchmark prices well above the assumptions in our January baseline (chart 1). This adds a major new layer of uncertainty to the outlook, given the wide range of possible paths for the conflict—spanning its duration, potential disruptions to supply and transportation, regional spillovers, and longer-term structural effects.

Our March baseline assumes tensions ease around mid-year, but oil prices remain elevated for longer. This is a baseline assumption rather than a call on the timing of a resolution. Under this profile, oil prices stay high through Q3 before gradually easing, albeit to levels above those previously assumed. On net, we judge the macro impact of the Iran war on Canada to be broadly neutral, reflecting significant offsetting forces, which we discuss in more detail in an In Focus box. That said, oil prices remain the single most important source of uncertainty around the forecast.

Stripping out war-related effects and recent market volatility, the US economy has evolved broadly as expected. Activity continues to slow alongside a gradually weakening labour market. In Canada, GDP growth in 2025Q4 matched expectations, but weaker-than-expected trade data and soft Labour Force Survey prints in January and February point to a weaker start to 2026. This marks a clear loss of momentum and weighs on the near-term growth outlook.

Despite this, growth dynamics over the forecast horizon remain broadly consistent with our January view. In the US, we continue to expect growth to slow as household spending cools in line with softer labour market conditions. In Canada, growth should recover after a weak first half of 2026, supported by fading trade headwinds, the lagged effects of past rate cuts, and continued support from government spending and investment.

While the baseline outlook for both economies is little changed, higher oil prices clearly skew inflation risks to the upside—especially in the US. We continue to expect the Federal Reserve to deliver one rate cut this year and one in early 2027, but with greater caution given elevated inflation risks. The Bank of Canada also remains focused on inflation, though it must balance these concerns against weakening incoming data. Against this backdrop, we expect the BoC to raise rates three times this year.

TRADE POLICY AND IRAN CONFLICT WEIGH ON US OUTLOOK

The US outlook remains broadly unchanged relative to January. Equity markets strengthened early in the year, partly offsetting the more recent sell‑off linked to the Iran conflict. Meanwhile, the Supreme Court decision on IEPPA tariffs and the subsequent temporary global levy are expected to have limited macro effects. Any modest gains from slightly lower effective tariff rates are likely to be offset by elevated trade policy uncertainty, as new investigations are launched and the global levy approaches expiry later this year.

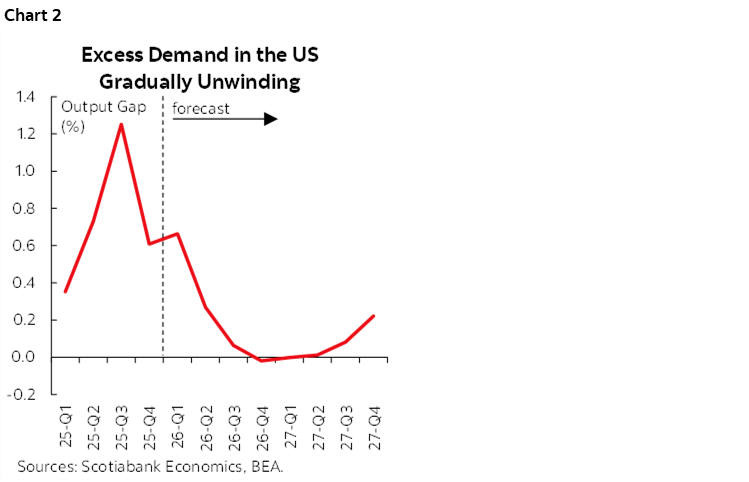

Against this backdrop, we continue to expect US growth to moderate, averaging 1.9% in 2026 before edging up to 2.1% in 2027, with the output gap—the percent deviation of GDP from its potential level—closing in 2026 (chart 2). Elevated interest rates, a softening labour market, and tighter financial conditions should increasingly weigh on activity. The resilience of the US economy has relied heavily on strong equity markets; with equity prices now softening amid geopolitical uncertainty and concerns over more persistent oil-related spillovers, this source of support is fading, pointing to a more visible slowdown ahead.

Household spending is expected to slow materially over the coming year. Consumption growth is projected to decelerate from 2.6% in 2025 to 1.5% in 2026 and 1.1% in 2027, reflecting softer labour market conditions and pressure on real incomes from higher energy prices. Business investment—particularly in technology-related sectors—has been a key growth driver in recent years, but momentum is expected to fade in 2026 as firms turn more cautious amid slowing demand.

In the near term, higher oil prices are expected to push headline CPI inflation to around 2.9%. Core PCE inflation is expected to remain in the upper-mid 2% range through 2026, easing only gradually to around 2.4% in 2027. This slower growth path is unlikely to be enough to return inflation to target. While tariff-related cost pressures have eased somewhat following the Supreme Court’s ruling on IEPPA tariffs, there is still pressure in the pipeline. Moreover, even before accounting for the recent rise in energy prices from the conflict in Iran, underlying domestic price pressures remain sticky, reflecting solid wage growth and elevated input costs.

Although the baseline US outlook is largely unchanged, inflation risks now loom larger for monetary policy. We expect the Federal Reserve to proceed cautiously, continuing its gradual easing cycle with one rate cut this year, and one early next year bringing the federal funds rate to 3.25%, where it is then expected to remain. Persistent inflation above target, combined with higher oil prices and other rising costs, is likely to limit the scope for faster easing. In this environment, the Fed is likely to err on the side of caution to avoid having to reverse course should inflation re‑accelerate.

CANADA: SOFT PATCH IN EARLY 2026, RECOVERY STILL ON TRACK

Canadian GDP growth in 2025Q4 came in as expected, with domestic demand slightly stronger than anticipated, but that strength has not carried into the new year. Recent data point to a weaker start to 2026, with broad-based softness in the Labour Force Survey in January and February and a very weak January trade report, signaling slower aggregate demand. We now expect GDP growth in 2026Q1 to undershoot earlier expectations but still progress at about potential’s pace. While part of this weakness likely reflects temporary factors and volatility, the overall growth profile for 2026 has deteriorated, with average growth now expected at 1.3%.

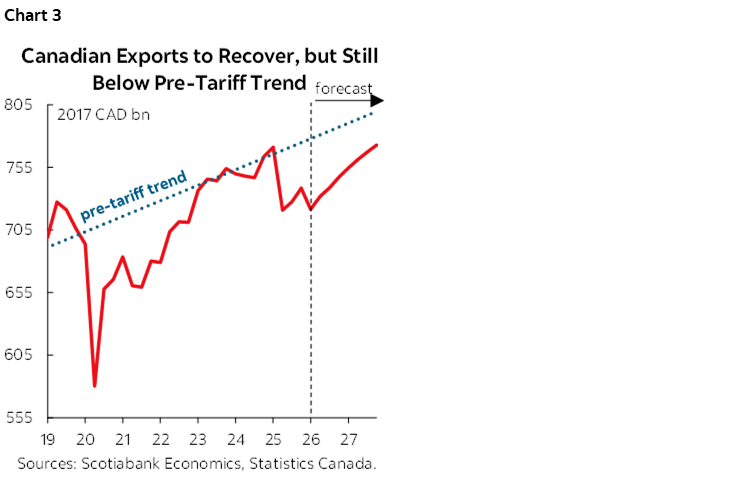

That said, several forces should support a recovery later in the year and into 2027. The drag from trade tensions is fading, past rate cuts are still feeding through, and government spending and investment initiatives will be supportive. After this early-year soft patch, growth is projected to accelerate to 2.0% in 2027. Domestic demand should rebound as confidence improves and fiscal support gains traction—not only through higher public spending, but also by supporting private investment. Exports are also expected to recover after a temporary pullback in Q1; while levels are likely to remain below pre-tariff trend, export growth should strengthen going forward (chart 3).

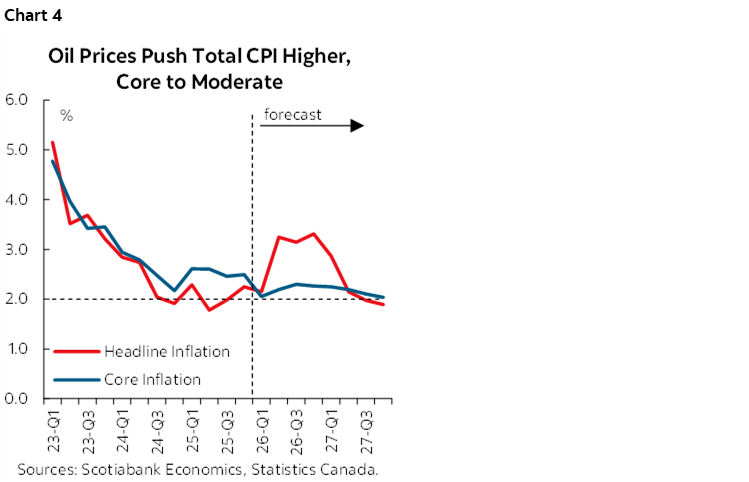

As for the US inflation, Canadian inflation dynamics in the near term will be heavily influenced by developments related to the Iran conflict. Higher energy prices are expected to push headline inflation to around 3.2% in 2026Q2 before inflation gradually converges back toward the 2% midpoint of the Bank of Canada’s target band over the course of 2027. With the economy operating below full capacity in recent quarters, excess supply has been weighing on core inflation (chart 4). However, elevated oil prices will continue to push input costs higher, tilting inflation risks to the upside even as demand cools.1

Against this backdrop, the Bank of Canada faces a familiar tradeoff. While near‑term growth has softened, we view the slowdown as temporary and do not expect the BoC to react to it. We also don’t expect it to react to the direct impact of higher oil prices on headline inflation, but the shift in the balance of inflation risks argues for caution—particularly given uncertainty around the persistence of the oil shock. A further deterioration in the conflict would likely require a more restrictive policy response to ensure inflation expectations remain well anchored. 2

We therefore expect the BoC to begin gradually removing monetary stimulus and move toward a more neutral stance by year‑end. Consistent with this view, we expect the Bank to remain on hold in the near term—until CUSMA renegotiations are resolved—before hiking three times in the second half of this year (chart 5).

RISKS

The outlook is subject to several important risks, with the most pertinent being the duration and intensity of the hostilities in Iran and surrounding regions, alongside a number of domestic risks in Canada and the US.

- Two-sided risks around oil prices. There is significant uncertainty surrounding the implications of the Iran conflict, and we see risks as broadly two-sided. Central banks, however, should be particularly alert to the risk of a further escalation. Additional disruptions to oil production or transportation would likely push commodity prices higher, increase financial market volatility, and place upward pressure on inflation expectations. This would represent a material upside risk to headline CPI inflation.

- Upside risk from additional US fiscal stimulus. Further fiscal support remains a key upside risk for the US economy, particularly if defense spending rises more than currently assumed amid a prolonged Iran conflict. In addition, proposed household transfers could provide further support to consumer spending if implemented. Taken together, a larger-than-expected fiscal impulse would complicate the inflation outlook and could materially alter the Federal Reserve’s policy path.

- Risk that Canadian economic weakness proves more persistent. Recent softness in Canadian activity may extend beyond a temporary soft patch, reflecting the lagged effects of tariffs and elevated policy uncertainty. In this scenario, the recovery in growth would be weaker than assumed, inflation pressures would ease more quickly, and interest rates would likely settle at lower levels than in our baseline.

- Breakdown of CUSMA negotiations. A full breakdown in CUSMA negotiations remains a low probability event but would represent a significant downside risk. Such an outcome would be negative for both economies and would likely push Canada into recession, given its high exposure to trade with the US.

1 In a previous note, we argued that rising costs act as an amplifier of upside inflation risks. In this context, the sharp increase in oil prices further tilts the balance of risks to the upside.

2 As Deputy Governor Sharon Kozicki noted in her latest speech, the longer a supply shock persists, the stronger the required policy response. In particular, inflation expectations could become de‑anchored if inflationary pressures are left unaddressed.

IN FOCUS: IMPACT OF IRAN WAR ON OUR ECONOMIC OUTLOOK

The escalation of the conflict involving Iran introduces a new layer of uncertainty for the global economy. While there is a high level of uncertainty around the development of the conflict our base case assumes a relatively quick resolution to the conflict, but that instability will remain in the region, leading to a persistent risk premium on oil prices. As such, we assume WTI to remain elevated in the near term, with a gradual normalization over the rest of this year. We expect oil prices to remain higher than pre-conflict projections over the rest of our forecast horizon.

For Canada and the US, the economic implications of this conflict operate through three main distinct channels:

- Higher Oil Prices: A Terms-of-Trade Shock. The most immediate channel is through energy prices. The conflict has pushed oil prices higher amid concerns about supply disruptions and increased geopolitical risk premia. For commodity exporters such as Canada, and recently the United States, this represents a positive terms-of-trade shock. Higher oil prices raise the value of exports relative to imports, increasing national income and improving corporate revenues in the energy sector. This effect typically boosts investment, fiscal revenues, and income in oil-producing regions. That said, higher energy prices also act as a tax on consumers through higher gasoline and transportation costs, partially offsetting the positive income effect.

- Tighter Financial Conditions. The conflict has already been associated with a decline in equity markets (see chart 1) and widening credit spreads, tightening financial conditions. Lower asset prices reduce household wealth and dampen business investment. These effects are negative for economic activity partially offsetting the income gains associated with higher commodity prices.

- Confidence Effects. Finally, geopolitical events that threaten income prospects often lead to deterioration in household and business confidence. While survey data have not yet fully reflected these developments, we estimated that oil supply shocks are associated with negative confidence effects in our model.

A SMALL NET IMPACT, BUT LARGE UNCERTAINTY

Overall, we assess the net impact of the Iran war to have a small impact on both Canadian and US economies, but this masks large offsetting forces. It’s worth noting that the magnitude of these forces are large, and the balance of effects is highly sensitive to the persistence and magnitude of oil price increases and financial market stress. Should either move materially beyond current assumptions, the net impact on growth could shift meaningfully in either direction.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.