- Our base case remains that we expect little change on the CUSMA front. While a full breakdown of negotiations and termination of the agreement remains a low probability event, its occurrence would be negative for both economies and would push Canada into a recession under the more severe scenario.

- Using Scotiabank’s integrated U.S.–Canada macro model, we consider two stylized scenarios representing progressively more severe trade disruptions. The model ensures internal consistency and captures bilateral trade flows and the endogenous monetary and fiscal policy responses that partially offset the drag from higher trade barriers.

- In this note, we assess the macroeconomic consequences of a potential failure to ratify CUSMA, the most consequential near-term risk facing the Canadian economy.

- The Bank of Canada might face pressure to ease monetary policy pre-emptively in the case of a failure to ratify, but high uncertainty around negotiations supports a prudent approach until clearer signals emerge.

The future of CUSMA is the single most consequential macro uncertainty facing the Canadian economy this year. The agreement’s review process presents three potential pathways: (1) ratification, in which the three countries agree to extend the agreement for another 16 years; (2) non‑ratification, under which the agreement would remain in force but only until its scheduled expiry in 2036, subject to annual reviews; or (3) termination, whereby any country could withdraw with six months’ notice under Article 34.6. The last involves significant legal hurdles and political costs, making the possibility of the U.S. unilaterally withdrawing very unlikely.

It is difficult to predict the future outcome of the review.1 The recent ruling by the Supreme Court of the United States (SCOTUS), which held that IEEPA does not authorize the U.S. president to apply tariffs, adds a new level of uncertainty. The decision introduces a new legal dimension and considerations to any scenario that sees the U.S. imposing new tariffs outside the CUSMA framework.

We view termination as a low probability event. However, the downside of such an outcome—for Canada, Mexico, and, to a lesser extent, the U.S.—is unambiguously high impact.

In this note, we map out the macro fallout on the Canadian and U.S. economies should CUSMA fully lapse. The analysis relies on simulations from Scotiabank’s integrated U.S.–Canada macro model, which embeds bilateral trade channels and general equilibrium feedback effects. Our conclusion is clear: a failure to ratify CUSMA would negatively impact the U.S. economy and push Canada into a recession.

TWO CUSMA SCENARIOS

As mentioned, there is a wide spectrum of possible outcomes to the 2026 review. Our baseline assumption aligns with a benign scenario whereby CUSMA is ultimately ratified or extended with limited adjustments that do not materially shift the macroeconomic trajectory. This view reflects the fundamental reality: the agreement is mutually beneficial, and much of the recent U.S. rhetoric appears aimed at strengthening its bargaining position rather than signaling an intention to dismantle the deal.

Still, uncertainty surrounding the review process warrants analysis of more adverse outcomes as a complete breakdown in negotiations cannot be ruled out. To capture the range of potential macroeconomic impacts, we consider two stylized scenarios representing progressively more severe trade disruption following a failure to ratify. In both scenarios, we assume the post-CUSMA regime starts in the third quarter of this year, in line with the six months’ notice requirement:

Scenario 1: Disruptive but Contained

CUSMA fails and the U.S. applies a 10% tariff on goods currently exempted under CUSMA—10% being the minimum tariff rate the U.S. had applied on all trading partners using IEEPA, and the initial global levy it later implemented in response to the SCOTUS decision to strike down tariffs under IEEPA. The existing Section 232 U.S. tariffs on steel, aluminum, and autos remain in place. The effective additional tariff rate on total Canadian exports, not just those destined for the U.S., rises to ~8%. Note that these estimates reflect only the incremental tariff burden since January 2025, not the total tariff rate currently paid on Canadian exports to the world.

Scenario 2: Severe Fragmentation

CUSMA fails and the U.S. broadly applies the current tariff rate applied to non-CUSMA compliant goods today: 35% on all applicable Canadian imports, with energy and potash at 10%. Section 232 tariffs remain the same. The effective additional tariff rate on total Canadian exports increases to ~15%.

Throughout this note, we assume Canada and Mexico would maintain their bilateral framework even in the event of a U.S. non-ratification; we treat a complete collapse of the agreement among all three parties as a low-probability tail risk. We also assume that there are no additional retaliatory tariffs by Canada’s and Mexico’s governments beyond those already embedded in our baseline While this is a reasonable assumption purely based on economic considerations, political considerations might lead to some form of a retaliatory response, increasing uncertainty about economic conditions in a failure-to-ratify scenario. A stronger retaliatory response will put upward pressures on domestic costs and prices, tightening the monetary policy stance, and amplifying the negative economic impacts.

All results are generated using Scotiabank’s U.S.–Canada macro model, which features explicit bilateral trade flows, and the full propagation of shocks through output, labour markets, incomes, consumption, and investment. The model ensures internal consistency across transmission channels: weaker exports reduce GDP, which softens employment and household income, depressing consumption and overall demand. Policy responses—monetary and fiscal—are captured endogenously, mitigating but not fully offsetting the drag from higher trade barriers.

Other impacts of a failure to ratify or prolonged renegotiation that are not explicitly captured in our model include, but are not limited to (see our Mexico team’s earlier note for a detailed discussion on qualitative considerations):

- Sector-specific disruptions due to rules of origin tightening and potential regulatory disputes. Autos, agriculture, energy, forestry, and other highly integrated manufacturing sectors are particularly exposed.

- Addition of non-trade chapters, like migration and security, which would be particularly relevant for Mexico.

- Increased administrative and financial costs stemming from new customs procedures.

- Broader non-tariff barriers to trade, including lack of protocol and certification standards.

- Second order effects, such as a potential expansion of bilateral trade between Canada and Mexico should their trade ties with the U.S. deteriorate. While this could provide some benefits, it would not fully offset the broader additional negative impacts described above.

TRANSMISSION MECHANISMS OF THE TRADE SHOCK

A CUSMA breakdown would hit both the Canadian and U.S. economies through several transmission mechanisms. Four channels matter most: collapsing trade flows, weaker productivity, confidence effects, and tariff-driven inflation.

- Lower trade volumes. The immediate consequence of higher tariffs is a sudden rise in the cost of cross-border trade. Canadian exporters face weaker U.S. demand as their goods become less competitive overnight. This gradually pulls down export volumes by over 1% in Scenario 1 roughly one year after the collapse of the agreement, and almost 4% in Scenario 2. Exporters investment projects are postponed or cancelled, and they also cut their payroll. Job losses erode household incomes and dampen consumption. This channel accounts for the bulk of the GDP decline in Canada across both scenarios. Lower exports spill quickly into the whole economy through reduced demand by export-oriented industries for labour and other production inputs. Note that the exchange rate depreciates by about 1% in Scenario 1 and 1.5% in the severe scenario, reflecting lower demand for Canadian assets. There is a risk that the depreciation will be larger, especially in a disorderly financial market adjustment. This would act as a shock absorber and reduce the impact on the Canadian economy.

- Weaker productivity. Dismantling integrated North American supply chains forces both economies into less efficient production structures. Capital is stranded, labour is underutilized, and firms are pushed toward higher cost domestic substitutes, hence leading to higher prices paid by businesses and households.

In the model, we capture this as a negative supply side shock that lowers potential output over time. The negative response of potential GDP reflects the fall of investment and an exogenous shock to total factor productivity partially calibrated using the BoC GEM model developed at the Bank of Canada and the IMF.

- Confidence effects. The current uncertainty about CUSMA negotiation’s outcome is negatively impacting our baseline economic outlook through reduced confidence for households and businesses. We can reasonably assume this uncertainty will abate once the post-negotiation regime is known. Nevertheless, we assume uncertainty about future economic and income conditions will stay elevated during the transition to this new tariff regime. This amplifies the short- to medium-term negative economic impacts by reducing household and business expenditures.

- Inflation passthrough and rising costs. Tariffs lift import prices directly (and indirectly through higher input costs), raising inflation, cutting real incomes, and pushing policy rates higher in the U.S. This channel is especially powerful under Scenario 2, where U.S. inflation rises by 0.3 pp. Canada avoids direct impact on inflation from these additional tariffs because we assume no retaliation to those. But second round passthrough matters: higher U.S. prices bleed into Canadian import costs, partially offsetting domestic disinflation from weaker demand.

Our model coefficients are estimated with historical data. Therefore, the reported impacts reflect estimated historical relationships between economic and financial indicators considered in the model, including how they reacted to past changes in effective tariff rates. But these effective tariff rates—and their changes—were modest until very recently. It is thus possible that larger-than-historical changes in tariff rates like those assumed in both alternative post-CUSMA scenarios discussed here could trigger non-linear effects in either direction.

There is thus meaningful uncertainty around how confidence levels and financial variables would behave under these scenarios. For instance, a stronger tightening in risk premia or a sharper decline in confidence than assumed could occur, which would amplify reported impacts. On the other hand, a sharper-than-estimated depreciation of the exchange rate would reduce the decline in exports and GDP. On balance, we view these two sources of uncertainty as broadly offsetting but still increasing the range of possible estimated impacts.

MACROECONOMIC IMPACT

The failure to ratify would be negative for both countries, lowering economic activity and likely leading to higher prices. The following are the details of our simulations results.

Canada

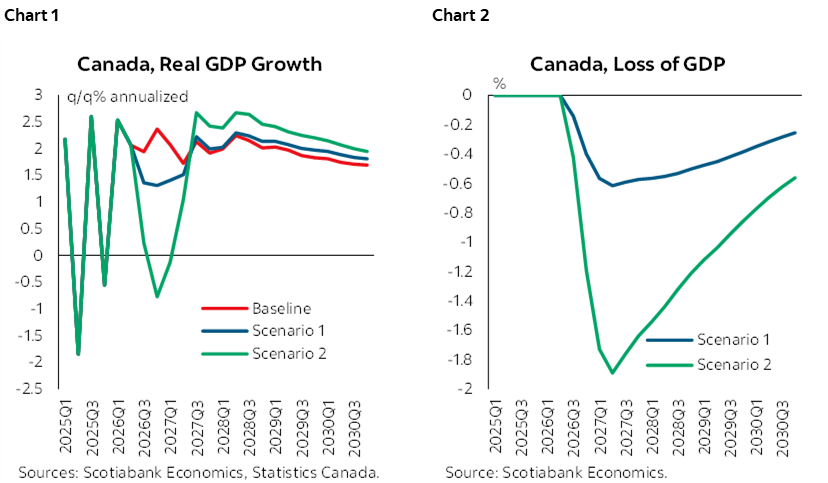

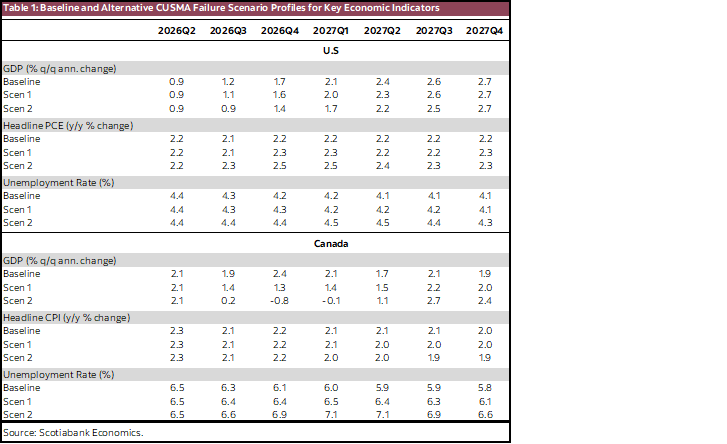

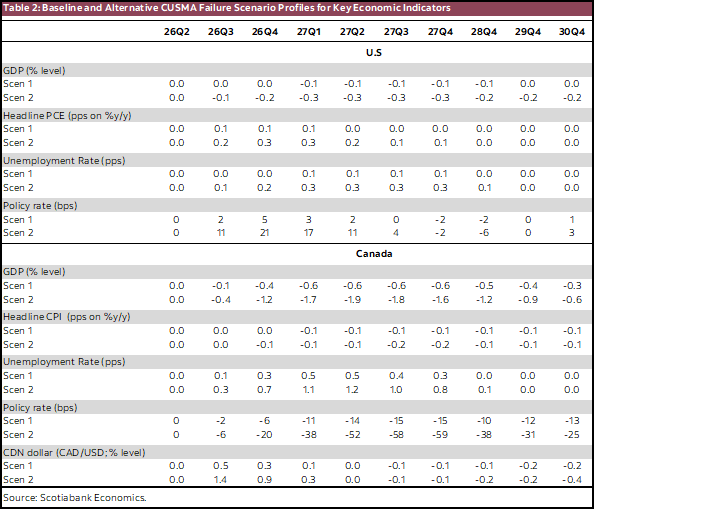

Relative to a renewal with minor changes scenario, real GDP falls by 0.6% under Scenario 1 and 1.9% under Scenario 2 roughly one year after the collapse of negotiations. The decline is driven primarily by collapsing trade flows and retrenchment in investment and household spending (charts 1 and 2).

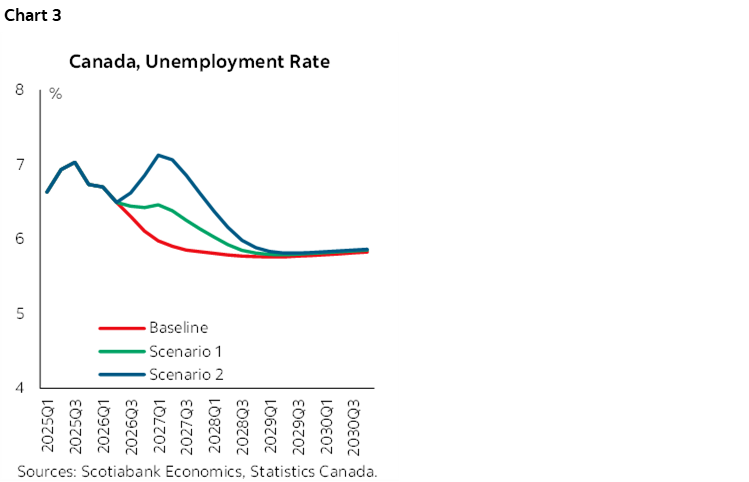

The labour market deteriorates materially: layoffs push the unemployment rate to a peak of 6.5% in Scenario 1, 0.5 p.p. above the renewal scenario, versus a peak of 7.1% under Scenario 2, 1.1 p.p. above renewal (chart 3).

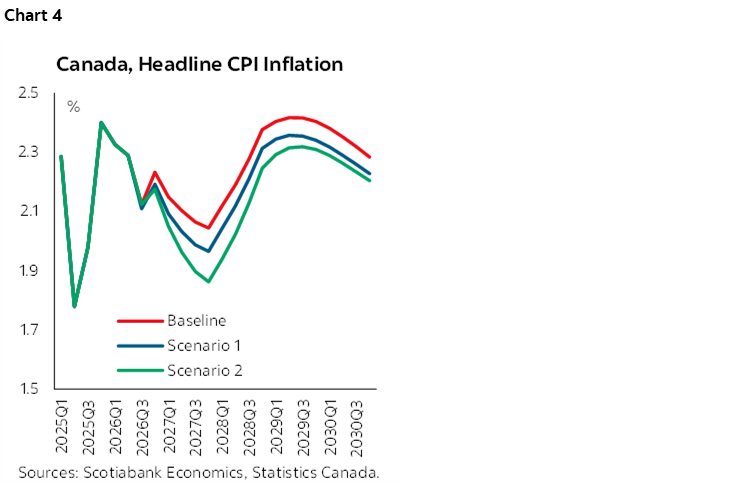

Inflation in Canada is largely unchanged in both scenarios. Higher U.S. inflation offset the disinflationary impulse from weaker domestic demand (chart 4).

The Bank of Canada delivers 50 bps of easing in the severe scenario, reflecting the buildup of economic slack. This helps mitigate the decline in demand. Automatic fiscal stabilizing effects—captured by our fiscal policy equations—also contribute to ease the negative impact on GDP.

United States

The U.S. economy is not immune. Higher import costs with the resulting weakening in productivity, reduce GDP by 0.3% in the severe scenario. As well, lower equity markets dampens household spending and amplifies the macro hit (charts 5, 6 and 7).

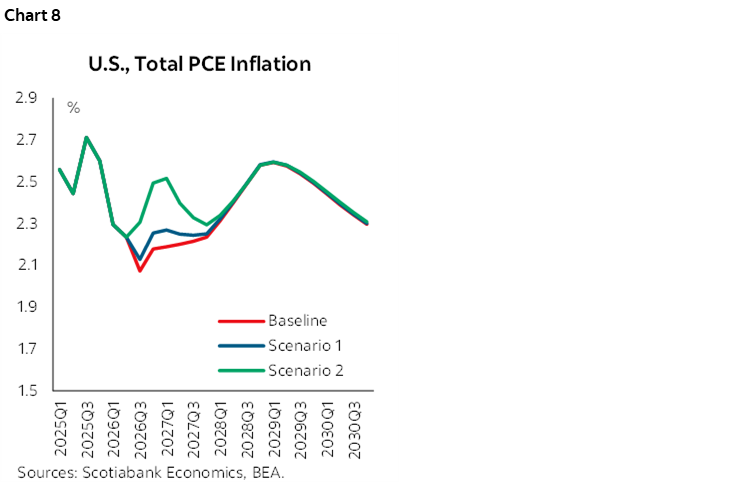

Even if some of the tariff shock is absorbed through profit margins, U.S. core goods inflation rises sharply especially under the severe fragmentation scenario. Under this scenario, PCE inflation increases by 0.3 pp2 (chart 8), forcing the Federal Reserve to briefly raise its policy rate by 25 bps. Because the need for tighter monetary policy is not persistent in our modelling, the Federal Reserve might look through the temporary tariff‑induced inflation and focus on supporting economic activity instead.

CONCLUSION

Overall, Scenario 1 represents a meaningful but manageable setback: growth slows—without becoming negative—and the damage is contained in trade exposed sectors. Scenario 2, by contrast, is a genuine macro event; the most significant North American trade disruption in decades. The combination of steep tariffs and productivity losses drives Canada into a deep recession and leaves the U.S. facing higher inflation and weaker growth. Uncertainty around these outcomes has direct implications for monetary policy in the near term, especially in Canada. Since a full termination or prolonged and messy renegotiations would constitute a very bad outcome for the economy, the Bank of Canada could ease pre-emptively. This would cushion the blow if the worst-case scenario materializes, but it carries the risk of over-easing—for example, if an agreement is ultimately smoothly reached, if the Canadian government retaliates with its own tariffs (pushing inflation higher), or if it instead responds with additional fiscal stimulus.

Given these risks, and the wide spectrum of possible outcomes, the most prudent course remains patience until clearer signals emerge from the review process, consistent with our baseline assumption.

1 See our Mexico team’s analysis on the most likely scenarios, ranging from benign, whereby the agreement is ratified mid-year, to adverse, whereby the framework remains in flux beyond the end of 2026. The analysis also highlights the considerations surrounding a partial renegotiation that could include revisions to rules of origin, sector-specific provisions, or the potential addition of non-trade chapters.

2 This is the resulting rise in inflation accounting for the rise in policy rate and does not fully reflect underlying inflation pressures from increased tariffs which are exceeding this projected 0.3 pp rise.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.