- Persistently high oil prices with sensitive inflation expectations are an important macro risk. With the 2022 episode still fresh, a renewed oil price surge comes at a time when inflation expectations are more sensitive, raising the risk that shocks may carry larger and more persistent effects than in the pre‑COVID period.

- We assess the risk of prolonged geopolitical conflict involving Iran combined with an endogenous credibility framework. Embedding time‑varying credibility in our macro model, we allow expectations to evolve with inflation outcomes, capturing how a sustained oil shock can weaken the BoC’s inflation anchor and alter price‑setting behaviour.

- Expectations are the key amplifier. We find that the central bank credibility is still below its historical average, making the current situation fragile. If the Middle East conflict drags on and credibility slips further, inflation would become more persistent and rises more sharply, requiring materially tighter policy.

- Loss of credibility is costly. In a prolonged shock, de‑anchored expectations could push inflation up to ~2pp above baseline, force aggressive rate hikes (+140bps), and trigger a significantly deeper economic slowdown.

The renewed surge in oil prices has brought back a familiar concern; that inflation could once again slip out of control. With the 2022 episode still fresh in mind, both markets and households are highly sensitive to price shocks. Shocks that would have been relatively benign in the pre‑COVID period may now carry much greater weight.

Our baseline remains that oil prices eventually normalize, allowing inflation to gradually converge back to target. But the risk scenario is becoming increasingly relevant for the Canadian economy: one in which oil prices remain elevated for longer, sustaining cost pressures and, crucially, testing the resilience of inflation expectations.

WHERE DOES THE BOC CREDIBILITY STAND?

When inflation is close to target, firms and households place substantial weight on the central bank’s objective and temporary shocks have limited and short-lived effects. But when inflation persistently deviates from target, credibility of that anchor weakens, and persistent shocks lead to very different inflation dynamics. So before turning to the scenario analysis, we must first evaluate where the credibility of the central bank’s target stands, because the starting point matters.

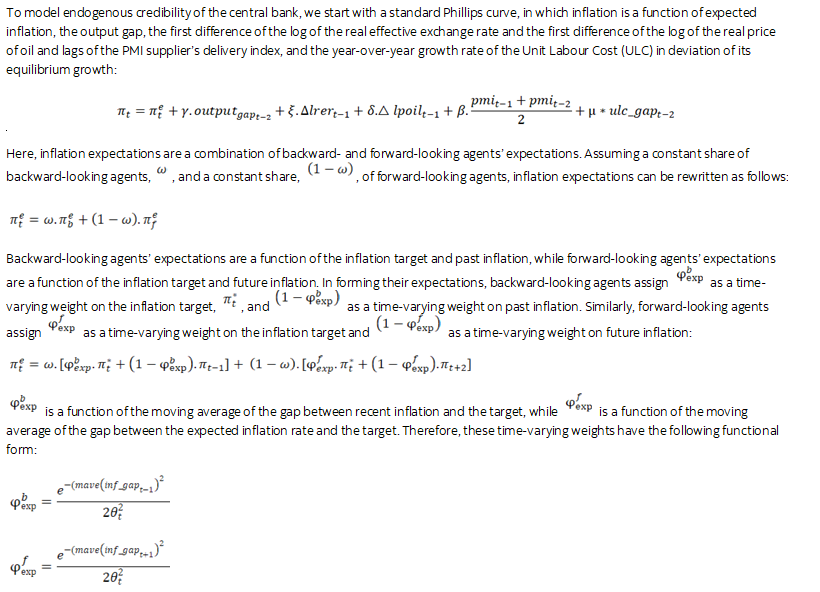

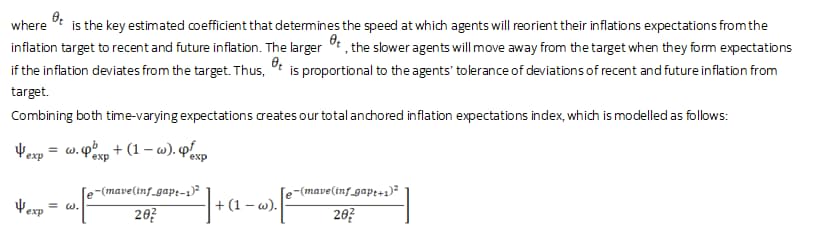

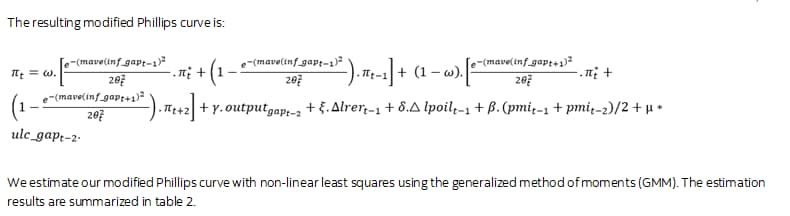

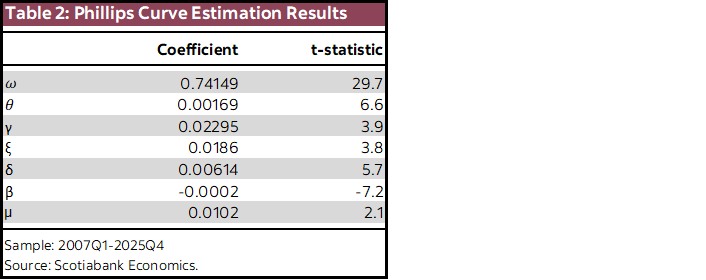

To evaluate the state of the central bank’s credibility, we rely on a modelling framework, used in previous work, embedded in our macro model that mimics endogenous credibility. In this setup, agents form expectations as a combination of the inflation target, recent inflation, and expected future inflation. The key feature is that the weight on the central bank’s target varies over time with inflation outcomes and expectations. As past and expected inflation moves away from target, firms place less weight on the target and increasingly rely on observed and expected inflation when setting prices. This shift makes inflation more backward-looking and more persistent, less self-correcting and more sensitive to ongoing shocks. See Appendix A for modeling details.

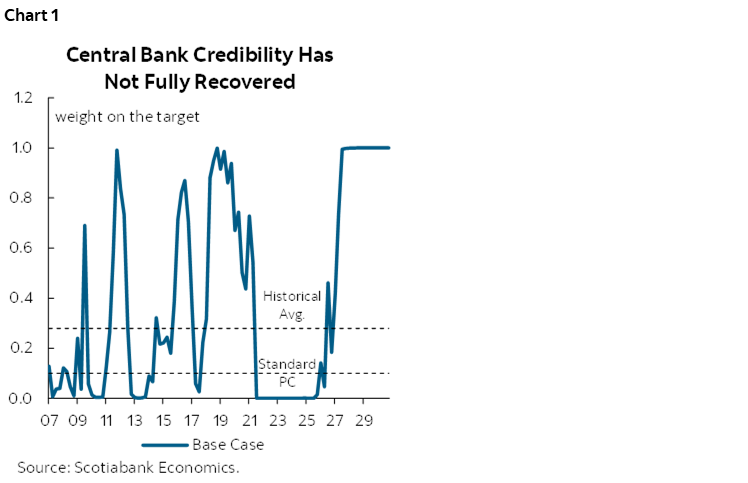

Chart 1 illustrates this mechanism through the weight placed on the inflation target over history, which we interpret as a proxy for the central bank’s credibility. At a high level, the index captures how much confidence agents place in the central bank’s ability to deliver on its target based on recent and expected inflation outcomes.

Unsurprisingly, this measure deteriorated sharply during the pandemic period, as inflation rose well above target and remained elevated. The longer inflation stayed high, the more agents adjusted their behaviour, gradually placing less weight on the 2% anchor.

More recently, inflation has come down significantly, but core inflation has been slow to fully return to target, leaving the central bank credibility still below its historical average. That said recent incoming data, including the April CPI print, point in the right direction, and we expect progress on core inflation to continue which should allow credibility to rebuild completely in the near term.

Still, the current starting point remains fragile. This leaves the inflation process more exposed to renewed shocks than in a fully anchored regime. In particular, in an environment where households are highly sensitive to visible price increases—especially gasoline and food—a sustained rise in energy prices could once again weigh on expectations. This is what we explore next.

WHAT COULD GO WRONG?

A prolonged geopolitical conflict involving Iran would tighten global oil markets for an extended period and generate significant supply chain disruptions. But even if oil prices do not rise further and instead remain elevated for a prolonged period, the implications for inflation could still be substantial. Beyond the direct impact on inflation, the persistence of the shock amplifies its indirect effects. Elevated fuel and transportation costs push up production costs across a wide range of sectors, from manufacturing to services. Since firms cannot absorb these cost increases indefinitely, they ultimately pass them on through higher prices. In other words, temporary shocks can be absorbed, but persistent shocks tend to alter behavior.

Another key mechanism operates through inflation expectations. When expectations are well anchored, firms broadly trust the central bank’s target and tend to look through small, temporary deviations in inflation. The degree of this so-called “rational inattention” is beneficial, as it allows central banks to guide inflation back to target following transitory shocks. However, when shocks are large and persistent, well-anchored expectations can no longer be taken for granted, especially since the credibility of the BoC has not yet fully recovered, as shown in chart 1 again.

The 2022 episode provides a clear illustration. As inflation surged, measures of expectations began to drift, forcing central banks to respond more aggressively to regain control. In the case of a persistent shock, such as one in which conflict in the Middle East drags on, these pressures could re-emerge. While we don’t think a repeat of 2021–2022 is the most likely scenario since the economy is currently in excess supply and fiscal policy is not as stimulative as it was, it is still an important upside risk. To assess the magnitude of the potential issue, we turn to a scenario analysis of a more prolonged conflict combined with a modeling device designed to capture endogenous changes in the central bank’s credibility.

ALTERNATIVE SCENARIO: PERSISTENTLY ELEVATED OIL PRICES AND SUPPLY CONSTRAINTS WITH UNANCHORED EXPECTATIONS

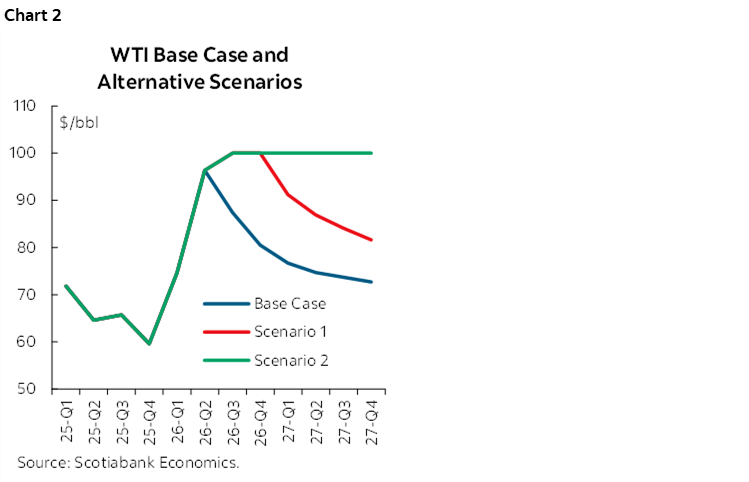

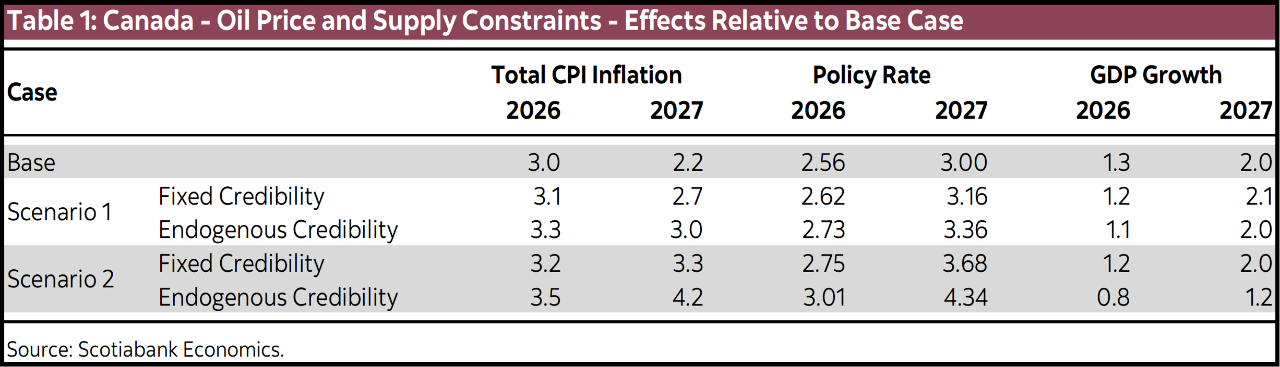

To quantify the upside risk to inflation, we construct scenarios built on three common pillars. In Scenario 1, we assume (1) oil prices remain elevated at $100 through the end of 2026; (2) supply chain frictions persist, as proxied by continued pressure on delivery times; and (3) central bank credibility is endogenous, allowing inflation expectations to de-anchor. Scenario 2 extends the same three assumptions, but over a longer horizon, with elevated oil prices and supply bottlenecks persisting through the end of 2027. Chart 2 shows the three oil price (WTI) scenarios.

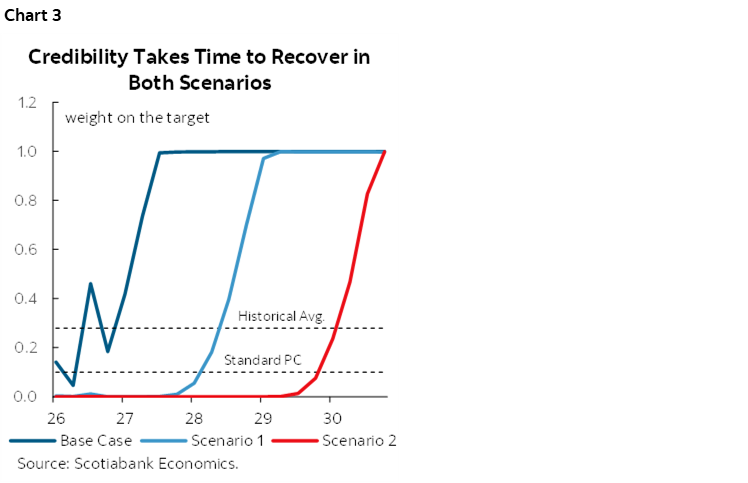

The inflation expectation de-anchoring mechanics is critical here. Rather than assuming that expectations are well anchored, we allow them to evolve endogenously using the framework described above (chart 3). This mechanism becomes particularly relevant in these alternative scenarios since energy prices play an important role in shaping inflation expectations. Households observe gasoline and food prices frequently and tend to extrapolate these movements into broader inflation beliefs. As a result, expectations are especially sensitive in an environment of persistently high oil prices. If households and firms come to believe that elevated inflation will persist, those beliefs can feed directly into wage demands and pricing behavior.

LOST CREDIBILITY = MORE PERSISTENT INFLATION, DEEPER ECONOMIC DOWNTURN

The simulation results point to a clear asymmetry in inflation dynamics, one that hinges critically on whether expectations remain anchored.

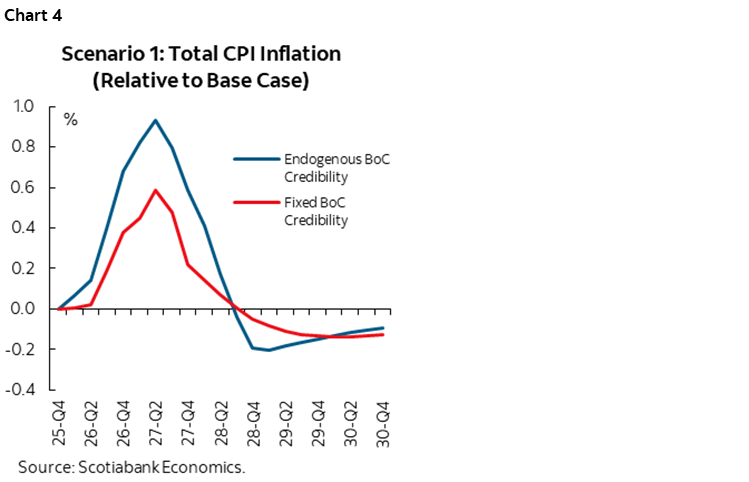

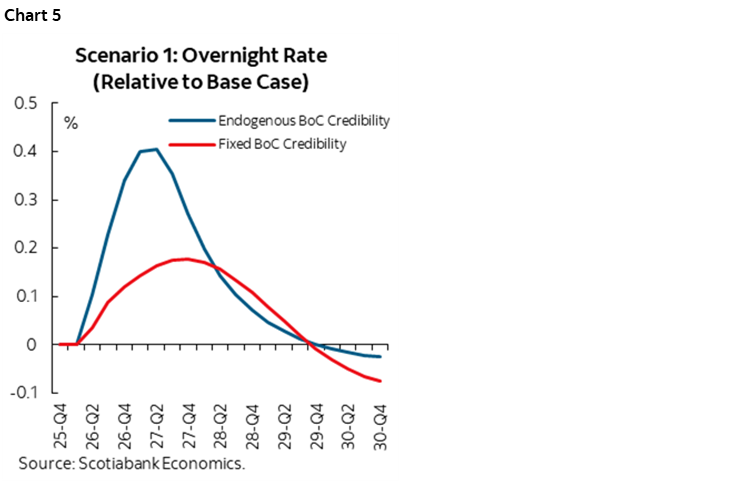

In the first scenario, the oil shock pushes inflation higher by roughly 0.6% above the base case, if expectations remain well anchored (chart 4), reaching 3.1% in 2026 and 2.7% in 2027 (table 1 shows the impact of the scenarios on the dynamics of the main macro variables). The impulse remains generally contained; firms and households continue to use the inflation target as their reference point, limiting second-round effects. In that environment, the BoC retains the flexibility to “look through” part of the shock. The result is only a modest tightening of monetary policy, with rates increasing by a limited amount to stabilize inflation over time (chart 5).

The picture changes materially once credibility starts to slip. In the case where credibility is endogenous and inflation expectations begin to de-anchor; inflation increases by 1% and is more persistent, reaching 3.3% in 2026. The key issue is that the inflation process itself changes: firms no longer price off the central bank’s target, but instead increasingly rely on observed and expected inflation. At that point, the central bank loses a key stabilizing channel; it can no longer rely on credibility to do part of the work. Restoring that credibility requires a much more forceful response; the policy rate needs to rise by roughly 40 bps to bring inflation back under control. The policy rate in this case is 3.25% on average in 2027.1 The central bank will regain its credibility by the end of 2027.

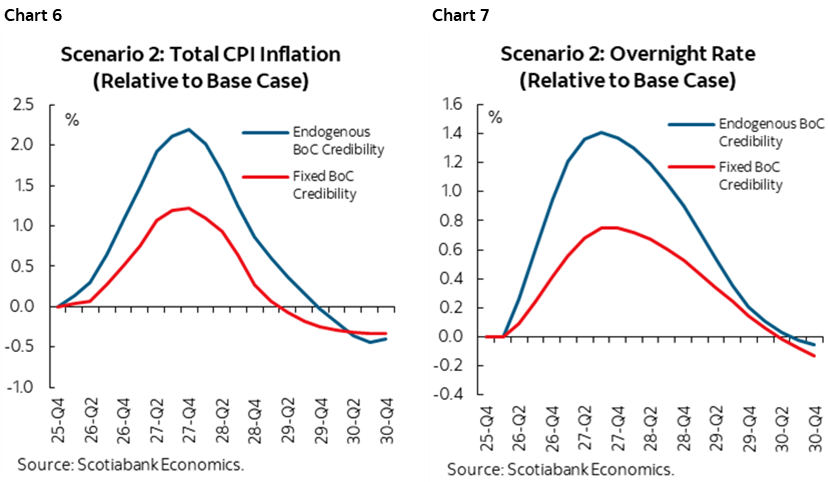

The problem becomes significantly more acute in a prolonged shock environment. In the second scenario, when oil prices remain elevated through 2027, the inflation impulse compounds (chart 6). With a loss of credibility, inflation response peaks at 2% above the base case, reaching 4.2% in 2027, and the policy response becomes significantly more aggressive, with rates rising by 140 bps above the base case (chart 7). This would bring the policy rate at 4.25% on average in 2027.1 In this case, the central bank only gets its full credibility back at the end of 2029.

THE COST OF DISINFLATION RISES SHARPLY

One of the key results from these simulations is that once expectations de-anchor, the economic cost of bringing inflation back down increases materially.

When credibility is intact, part of the disinflation process comes “for free”; agents expect inflation to return to target, which helps anchor price setting even as shocks hit. This shows up clearly in the simulations. The impact on the economy of the scenario with fixed credibility is small; higher oil prices provide some income support to the Canadian economy via the terms of trade, but it’s largely offset by persistent supply chain disruptions, and the small monetary tightening.

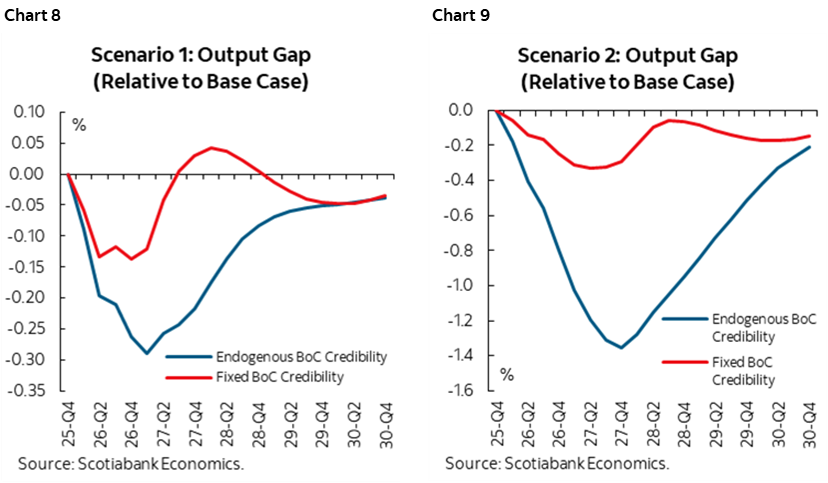

But when the anchor weakens, disinflation has to be engineered through demand destruction, i.e. weaker growth, softer labour markets, and a larger output gap. Simulations show the level of output would need to drop by 0.3% to bring inflation back to target (chart 8). This is twice as much as in the fixed credibility case, for the same oil shock. The effect is dramatically more pronounced in the second scenario where oil prices remain elevated until the end of 2027 (chart 9), with output falling by 1.4%. GDP growth would be significantly lower at 0.8% this year and 1.2% in 2027 in that case. Put differently, the economy has to endure a much deeper slowdown to generate the same disinflation outcome.

BOTTOM LINE

The key message is that a more persistent oil price profile can quickly become destabilizing if expectations are not well anchored. This is precisely why a risk management approach is essential in situations like this. Acting early and communicating clearly the commitment to controlling inflation can help prevent expectations from drifting in the first place, avoiding the need for a strong downturn in economic activity to regain control of inflation. Credibility, once lost, is definitely costly to rebuild.

1 The monetary policy rule in these simulations remain the same in both cases. However, in an optimal policy setting, the central bank would likely put more weight on inflation deviations knowing that inflation expectations can de-anchor. This would mean an even more reactive policy rate, and tighter policy rates.

APPENDIX: PHILLIPS CURVE WITH ENDOGENOUS CREDIBILITY

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.