- Ottawa may soon invite Canadians to invest alongside it. The proposed Canada Strong Fund is expected to be paired with a retail-accessible sleeve that would give households a direct stake in the federal government’s growth ambitions.

- The idea is novel. It could broaden participation in nation-building assets, allowing Canadians to share more directly in the upside of the domestic growth agenda and giving them a greater sense of agency in the nation’s future.

- But the bar should be higher than patriotic packaging. The policy test is not only whether Canadians can be encouraged to buy in. It should be whether the design solves a legitimate policy failure or market gap.

- One possibility is that domestic capital is undervalued in a more polarized world. Global markets should respond to Canada’s investment demands, but capital allocation may not fully align with national priorities at a time when strategic resilience, domestic ownership, and supply security carry greater weight.

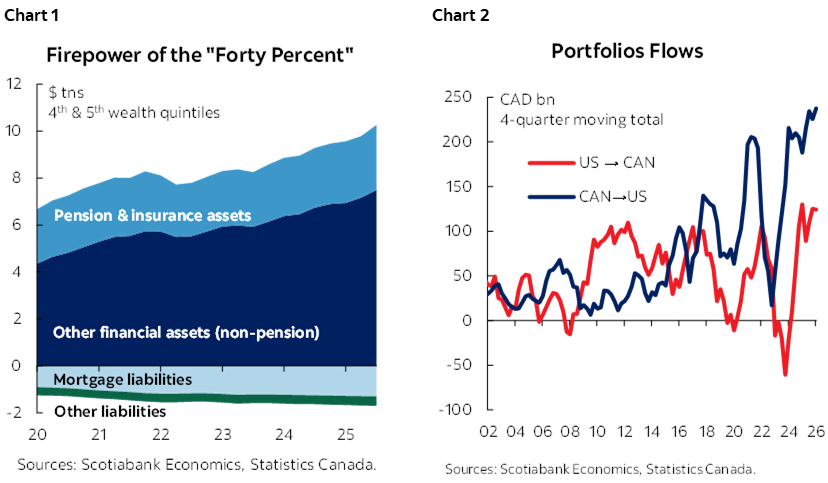

- Households are often overlooked in this mobilization story. Aggregate balance sheets look constrained because they are housing-heavy, but disaggregated data show substantial financial capacity among higher-wealth households. The top 40% of households hold $7.4 tn in non-pension financial assets (chart 1).

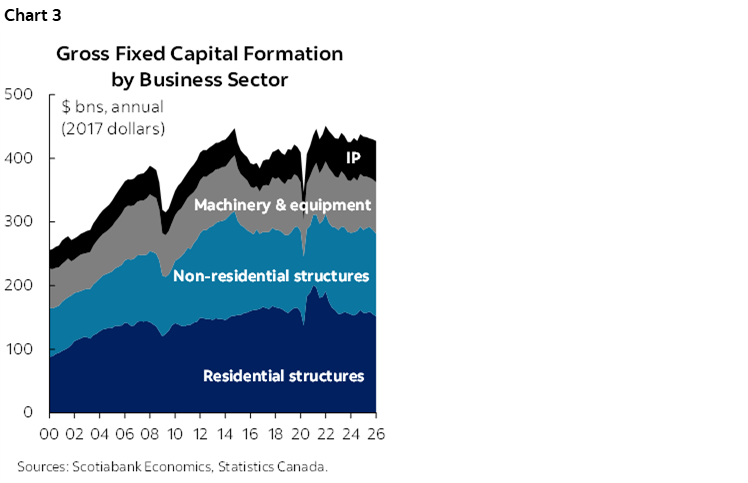

- Mobilizing that capital also depends on the channels available to households. Much of Canada’s investable surplus flows abroad—particularly to the United States—as many households have fewer practical ways to access diversified, productivity-enhancing Canadian assets at home (chart 2).

- Even as balanced exposure to long-duration assets has historically delivered higher risk-adjusted returns over the long run, investor education and discipline may not fully internalize those gains—particularly the value of dampened volatility—especially when a run of exceptional public market gains may anchor expectations.

- Any retail sleeve should expand access without diluting investment discipline. Measured exposure to new nation-building projects may provide the upside, but a stabilizing core of mature infrastructure would likely be needed to make the proposition investable for households.

- Patient capital also needs the right savings architecture. The government has not indicated whether the retail sleeve would be tax-favoured, but Canadian savings behaviour suggests incentives matter if the objective is to mobilize household capital into long-duration domestic assets.

- The policy test is disciplined access. Done well, it gives households a credible way to invest in Canada’s productive base. Done poorly, it shifts too much risk back onto taxpayers.

- The answer is not obvious, but the policy test should be.

THE TRILLION DOLLAR PLAN

The federal government has embarked on a deliberately ambitious investment agenda. In Budget 2025, the Carney government set a goal of mobilizing a trillion dollars of investment over the next five years. Ottawa would leverage over $450 bn (cash basis) under its new capital framework to crowd in the balance from private players and, to a lesser extent, other orders of government.

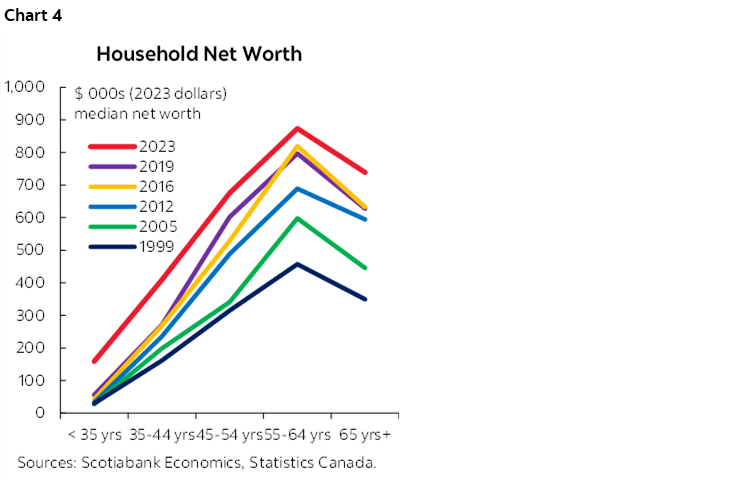

This would represent a meaningful step-up in investment if successful. With annual business capital formation currently running near $600 bn (current dollars), this roughly implies investment growth on the order of 15–20% per year. Yet in real terms, investment has been largely stagnant in recent years—barely covering depreciation, let alone supporting a growing labour force (chart 3). As Scotiabank has previously noted, the scale of this ambition is audacious, but it is also the only durable path to lifting living standards for Canadians.

The plan’s early architecture is constructive. The government has moved quickly to improve the investability of the domestic landscape through wide-ranging regulatory and policy reforms. By its own estimates, the emerging nation-building project pipeline—currently standing at 15 projects—could unlock roughly $126 bn in new investment, alongside another 7 transformative strategies. There should also be positive spillovers from NRCan’s $637 bn inventory of long-horizon natural-resource projects.

The ambition is clear. The harder question is whether Canada can attract and mobilize the kinds of capital that best align with its long-term investment objectives.

A MOBILIZATION MANDATE

This agenda will take capital. In open markets, investment demand should attract supply, and foreign capital should remain a key part of the mix. It brings scale, discipline, and expertise. Federal officials are actively courting investors abroad.

But not all capital is the same. When domestic investment needs exceed national saving, foreign inflows can fill the gap. Modest current-account deficits are not inherently problematic, but their causes and consequences matter. In Canada’s case, they reflect deeper structural vulnerabilities, including persistent fiscal shortfalls, housing-heavy capital allocation, and eroding external competitiveness.

The Build Canada agenda raises the stakes. If investment ambitions rise materially without broader mobilization of domestic capital, Canada could face larger external financing needs during the build-out phase, with more of the upside accruing to foreign owners. In a more fragmented world, the source, terms, and ownership of capital should carry greater weight. That raises the premium on putting Canadian capital to work at scale.

Ottawa is moving in this direction. Earlier measures target pension and other long-horizon institutional capital, including greater private participation in federally owned airports, adjustments to prudential settings to avoid unduly constraining business lending, and more deliberate use of federal and Crown balance-sheet capacity.

The Canada Strong Fund, along with its potential retail sleeve, would add further tools to that mobilization mix—and bring households squarely into the policy frame.

UNTAPPED FIREPOWER

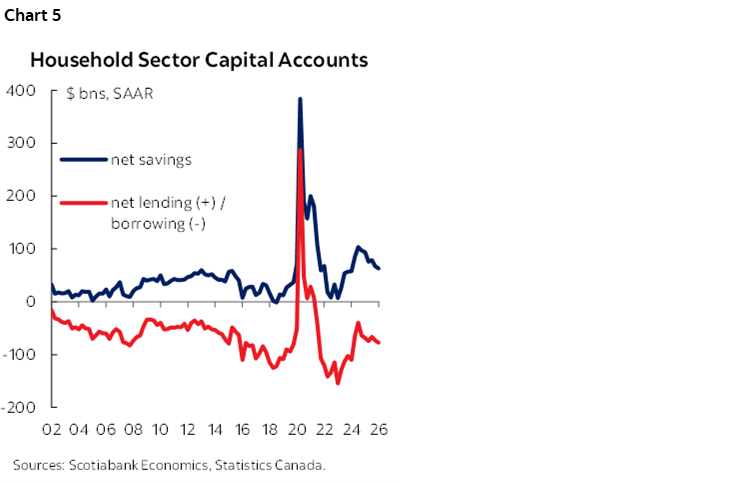

Households have until now been largely absent from Canada’s capital-mobilization playbook. A “Buy Canada” response is showing up in pocketbook choices, including staycations and local-first spending. But the dominant macro household narrative remains one of pessimism and constraint. Noting that Canadians have never been wealthier is a political non-starter (chart 4).

The sector accounts help explain part of the disconnect. Household saving—measured as disposable income minus current consumption—is positive. But once the acquisition of non-financial assets, primarily housing, is netted out, the sector flips into net borrower status (chart 5). High housing costs crowd out the very saving that could otherwise be channeled into more productive investment—reinforcing why housing affordability is central to the broader growth agenda.)

Disaggregation tells a different story. Higher-wealth households run persistent financial surpluses and act as net lenders. A simple liquidity proxy—non-pension financial assets net of liabilities—shows the top two wealth quintiles comfortably above the bar, with these 40% of households holding a combined $7.4 tn in non-pension financial assets (chart 1, front).¹ Market gains have added a couple of hundred billion to these balances each quarter—albeit with volatility—as equity markets have buoyed asset prices.

Much of this investable surplus migrates abroad. Canadians are buying north of $200 bn in foreign portfolio assets annually, predominantly US exposure, while reciprocal foreign purchases of Canadian assets are smaller despite the larger US investor base. This is not unusual in open markets, where capital follows risk-adjusted returns. (It is also consistent with a current account deficit financed by other offsetting gross inflows.)

None of this argues against diversification or openness. But it raises a policy-relevant question whether Canada’s current intermediation channels make it easier for households to access foreign exposure than a diversified slice of Canadian productive assets at home. And relatedly, does Canada's savings architecture give suitable households a credible way to go long on Canada.

GOING LONG

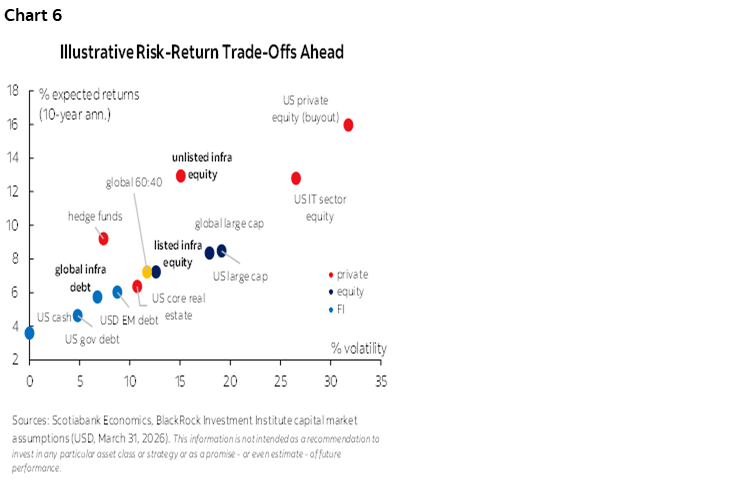

The case for expanding household access to long-duration assets—such as infrastructure, real estate, private credit, and growth equity—is straightforward on paper. Public markets are a thinner channel for broad wealth creation as listings decline, concentration rises, and short-horizon approaches deliver less diversification (chart 6). Longevity risk—and policy failures tied to aging preparedness—only strengthen the case for longer-horizon planning.

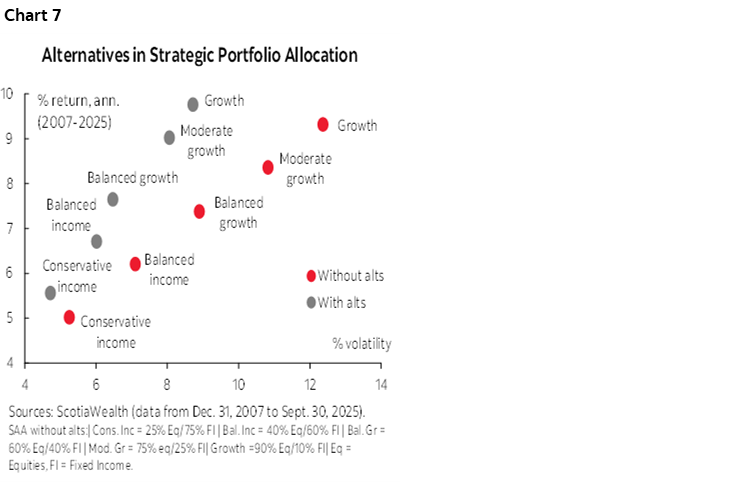

Past market performance supports diversified and measured exposure. Scotia’s Balanced Growth portfolio, for example, delivered 40% higher risk-adjusted returns between 2007 and 2025 when a portion of capital was reallocated from equities to alternatives within a diversified mix. A combination of lower volatility and higher returns drove the improvement, with even larger gains for more growth-oriented portfolios (chart 7).

Long-horizon investing is already embedded in Canada’s institutional ecosystem. Pension funds and high-net-worth investors hold material exposure to alternative assets to capture illiquidity premia and dampen cycle volatility, with allocations ranging from roughly 10% to more than 50% among some larger institutional investors. Retail investors, by contrast, remain concentrated in liquid public products, with alternatives representing only a marginal share of managed retail assets.

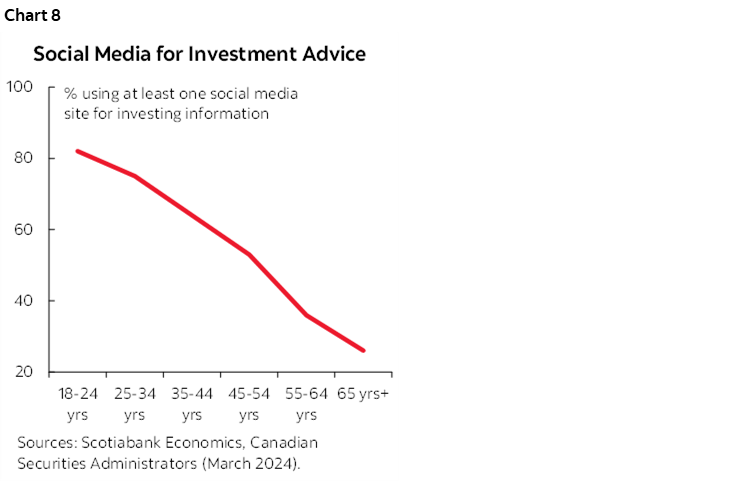

Access alone does not guarantee suitability. Liquidity is an imperfect measure of risk, but it becomes critical when investors expect to redeem their money more quickly than the underlying assets can be sold. Recent strains in private credit markets illustrate how quickly confidence can erode when liquidity terms, underwriting standards, and product complexity are not well understood. These risks are more acute in retail segments where investor knowledge is uneven, advice quality varies, and social-media-driven financial guidance is gaining influence (chart 8). The majority of retail investors in Canada continue to score low on investor knowledge, according to the 2024 CSA Investor Index, even as a third of young Canadian retail investors hold crypto assets.

The implication should not be “no access,” but disciplined access. Any expansion should be scaled cautiously with structures that align investor horizons with asset duration, redemption terms, disclosure, advice standards, and plain-language framing. Canada also has to do a much better job at building financial literacy at much earlier ages and horizons.

BUILDING THE BRIDGE

The proposed Canada Strong Fund retail sleeve could give households a practical way to invest in Canada’s long-term growth story. The Fund’s anticipated underlying asset base—energy systems, infrastructure, major natural resource developments, defence-related capacity, and other nation-building equity investments—could give households exposure to tangible Canadian assets with long-term economic value.

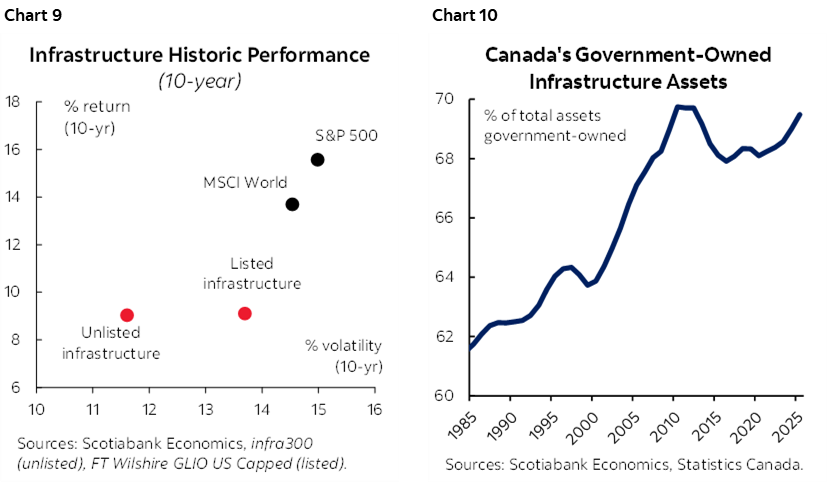

The key is turning nation building projects into an investable proposition rather than a symbolic savings vehicle. Global infrastructure assets—public and private—have proven their value as portfolio ballast, even if recent equity strength has distorted near-term comparisons (chart 9). A sensible structure would pair measured exposure to new nation-building projects with a stabilizing core of mature infrastructure assets backed by contracted or regulated cash flows. That structure could support more stable returns while capturing some upside. Asset recycling could further deepen the pool of investable assets given the large share of government-owned assets (chart 10). The government has hinted in this direction though only a small share sits on federal books.

The asymmetric risk-sharing promise also raises the stakes for the asset mix. Ottawa has signaled that Canadians would share in the upside while receiving downside protection. If protection is tied mainly to a narrower, inherently riskier pool of new-build projects, the cost could land back on the federal balance sheet. A seasoned infrastructure core would help anchor the sleeve, making any protection more credible and reducing the risk of taxpayer-backed losses.

The policy case also points to a potential role for incentives. The government has not indicated that the retail sleeve would be tax-favoured. But the UK experience, as well as Canadian savings and investment behaviour, suggests that incentives may be needed if the goal is to encourage households to hold long-duration assets rather than treat the sleeve as another short-term savings product.

Canada’s existing savings architecture is informative in this regard. RRSPs, pension plans, and locked-in accounts show that households will accept long-term constraints when the tax and savings incentives are clear. TFSAs, while highly successful, often function more like flexible liquidity vehicles, which may make such a structure less suited to illiquid or semi-liquid assets without additional design features.

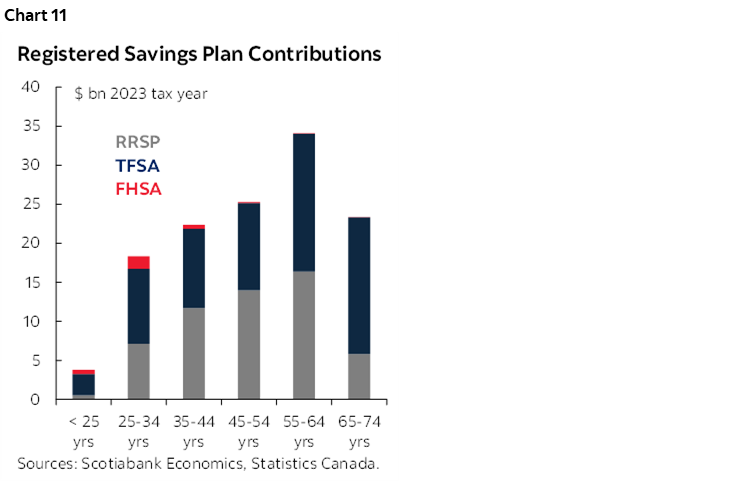

The opportunity could also scale quickly. As Canada’s build agenda enters a capital-intensive phase, registered plans already operate at scale, with large and recurring annual contributions (chart 11). Targeted, time‑limited measures such as incremental contribution room or enhanced tax treatment could ease early‑adoption frictions, while early‑withdrawal penalties could reinforce longer holding horizons. Even modest incremental room for qualifying long-duration domestic assets—taken up by a subset of higher-capacity households—could redirect tens of billions in annual flows. While small relative to national needs, these flows would compound over time.

Finally, the case for a government-backed retail sleeve is not demand alone but a clear market gap. It would channel household capital into long-term domestic assets and expand access where private markets fall short. The goal should be to catalyze participation, not displace private solutions.

OWNING TOMORROW

Canada’s challenge is not raising more capital—it is mobilizing the right capital on the right terms. A retail sleeve in the Canada Strong Fund could help if it gives households disciplined access to productive domestic assets while keeping risks transparent and appropriately allocated. Done well, Canadians become owners—not just taxpayers—in the country’s next phase of growth. Done poorly, it is simply patriotic packaging for risk.

1 The middle quintile enjoys a net financial surplus but flips to a deficit when pension assets are excluded, while the second-lowest quintile's net worth (all assets) is tied up in housing with more limited financial assets of all type.

Box 1: UK’s Long Term Asset Fund (LTAF)

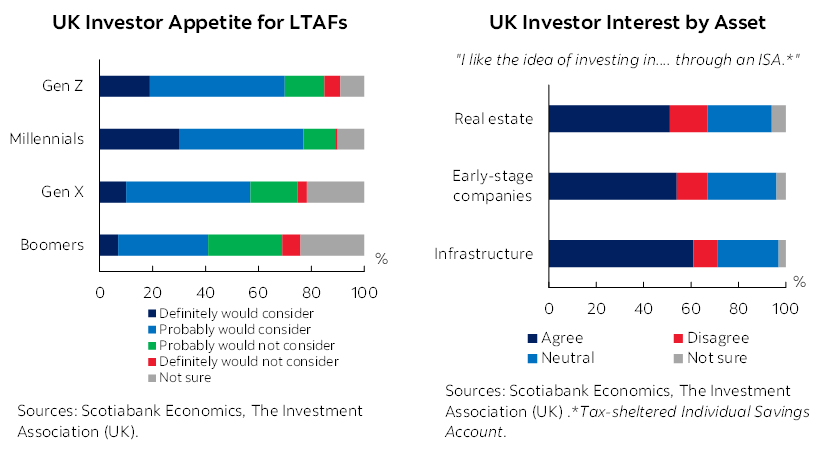

The UK’s Long Term Asset Fund (LTAF) offers one model of enabling retail access with safeguards. LTAFs are regulated vehicles designed for illiquid assets such as infrastructure, real estate, and private credit, with explicit liquidity‑management tools so that redemption terms reflect the underlying assets. Since mid‑2023, roughly 25 LTAFs have launched (~£7.3 bn AUM). Policy changes are expected to support further growth as LTAFs become eligible within tax‑advantaged Individual Savings Accounts this year.

Survey evidence suggests demand exists when offerings are clearly framed: nearly 60% of UK investors report interest in “going long for local” if opportunities are attractive, with particularly strong appetite among younger investors along with a clear preference for infrastructure exposure. Nevertheless, it is still early days and the UK Investment Association ISA barometer underscores the importance of clear communications, investor education and adequate safeguards in its long-term success.

Box 2: Other Potential Ideas to Mobilize Domestic Savings Towards the Build Canada Agenda

A contribution from Scotia Global Asset Management

A broader set of policy options could be explored to mobilize domestic capital. The ideas below are intended as thought‑starters rather than recommendations, recognizing that outcomes will hinge on design choices—particularly around incentives, risk‑sharing, safeguards, market integration and administrative feasibility. Some may overlap with the federal government’s proposed retail product, where details remain under consultation.

1. Reframe existing savings vehicles

- Rebrand the TFSA as a Tax‑Free Investment Account (TFIA) to better reflect its intended role as an investment—not merely a savings—vehicle, and to counter the tendency for a large share of balances to remain in cash or near‑cash instruments.

- Such a reframing could modestly shift behaviour toward longer‑horizon deployment without changing the underlying tax treatment.

2. A Canada First Tax‑Free Infrastructure Account (public‑markets variant)

- A registered account focused exclusively on publicly listed Canadian companies and government‑issued instruments tied to energy, infrastructure, defence and broader industrial capacity. Potentially higher contribution room and incentives for longer hold periods could help scale investment.

- By limiting eligibility to public markets, this approach would favour transparency, liquidity, and familiarity for retail investors and advisors, while still creating a dedicated channel for long‑term domestic investment.

3. A modern infrastructure‑focused savings bond

- Reintroduce a Canada infrastructure savings bond, carefully informed by the experience of the former Canada Savings Bond program, which was wound down amid waning investor interest and high administrative costs—underscoring the need for any new initiative to be competitively priced, operationally lean, and clearly differentiated from existing retail products.

- A re‑imagined approach could emphasize longer maturities, optional inflation protection, and incentives that reward holding to maturity, while leveraging the Canada Infrastructure Bank to link sovereign issuance to portfolios of CIB‑vetted and de‑risked projects—providing tangible project linkage and credibility without re‑creating the cost and complexity challenges of earlier efforts.

4. Reinvigorate flow‑through shares for long‑duration capital

- Refocus flow‑through share incentives on recycling capital over time, rather than on short‑term tax benefits tied to initial issuance.

- Preferential tax treatment could be conditioned on extended holding periods and reinvestment into subsequent eligible Canadian projects, reinforcing continuity of patient capital.

5. Purpose‑built long‑term asset funds for retail investors

- Establish a regulated long‑term asset investment fund structure, overseen by securities regulators, allowing private savings to access diversified pools of eligible Canadian energy, resource, and infrastructure assets.

- Time‑limited and declining tax incentives could help overcome early‑adoption frictions, while strict alignment of asset duration, redemption terms, and disclosure standards would be central to retail suitability.

6. Encourage the repatriation of Canadian capital

- Introduce a targeted, tax‑deferred pathway for rolling foreign holdings into eligible Canadian assets, subject to caps and safeguards.

- Such an approach would encourage, rather than compel, portfolio rebalancing toward domestic investment while preserving diversification.

Taken together, these ideas share a common objective of incentivizing broader capital mobilization through channels accessible to more Canadians. They differ in design, risk profile, and target investors—differences that warrant careful deliberation. Any approach should weigh potential welfare gains against fiscal cost, potential demand, market effects, and the risk tolerance and readiness of retail investors, with an emphasis on aligning product design to investor capacity while supporting long‑term domestic capital formation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.