- The reduction in the Domestic Stability Buffer is equivalent to a quasi monetary easing.

- We estimate that the reduction in the Domestic Stability from 3.5% to 3% could have roughly the same impact on economic activity as a 25 basis point decline in the Bank of Canada’s policy rate.

Regulatory policy changes often fly under the radar of most Canadians. Yet, changes in the regulatory landscape can have meaningful impacts on the economy when they impact the availability of credit. Last week, the Office of the Superintendent of Financial Institutions (OSFI) lowered the Domestic Stability Buffer (DSB) from 3.5% to 3.0% in a move designed to provide greater flexibility for the six largest banks to deploy capital. While this policy change focuses on the supply of credit to the economy, it is analogous to a drop in the Bank of Canada’s policy rate that stimulates the demand for credit. We estimate that the reduction in the DSB provides roughly the same amount of stimulus as a 25 basis point cut in the Bank of Canada’s policy rate assuming that there is an ability to fund asset growth and that there is demand for the resulting increase in supply of credit. Given our view that the Bank of Canada (BoC) will need to raise its policy rate late this year, this regulatory change may need to be considered by the BoC as it sets its policy rate.

BACKGROUND FOR OSFI’S DECISION

The Office of the Superintendent of Financial Institutions regulates and supervises all federally regulated financial institutions. It sets a broad range of regulations impacting many aspects of the Canadian financial system and ensures that these are respected. For banks, a key regulation concerns the amount of capital banks must hold against assets. The DSB is one layer of capital Canada’s six largest banks must hold. The DSB is reviewed twice a year by OSFI, in June and December. The DSB was last modified in June 2023 when it was raised to 3.5%. The DSB now stands at 3.0%.

Changes in bank capital ratios have a direct impact on the supply of credit. A lower capital ratio frees up capital and can lead to asset growth for banks, while a rising capital ratio does the opposite. As a result, changes in capital ratios impact the economy in a very tangible way. A decline in the DSB will raise economic activity, and this is expressly noted in OSFI’s decision: “These adjustments will enable Canada’s largest banks to aid the Canadian economy’s adaptation to shifting dynamics in technology, trade, and geopolitics with opportunities in segments such as defence and security, critical infrastructure, resources and artificial intelligence.”

ESTIMATING THE MONETARY POLICY EQUIVALENT OF CHANGES IN CAPITAL RATIOS

Depending on the direction of change, a modification in the capital ratio can impact economic growth by raising or lowering the supply of credit available to finance household and business spending and ultimately put upward or downward pressure on inflation. In contrast to changes in regulatory capital, movements in policy rates impact the demand for credit and impact growth and inflation. In this sense both policies impact the economy through different, but critical financial channels.

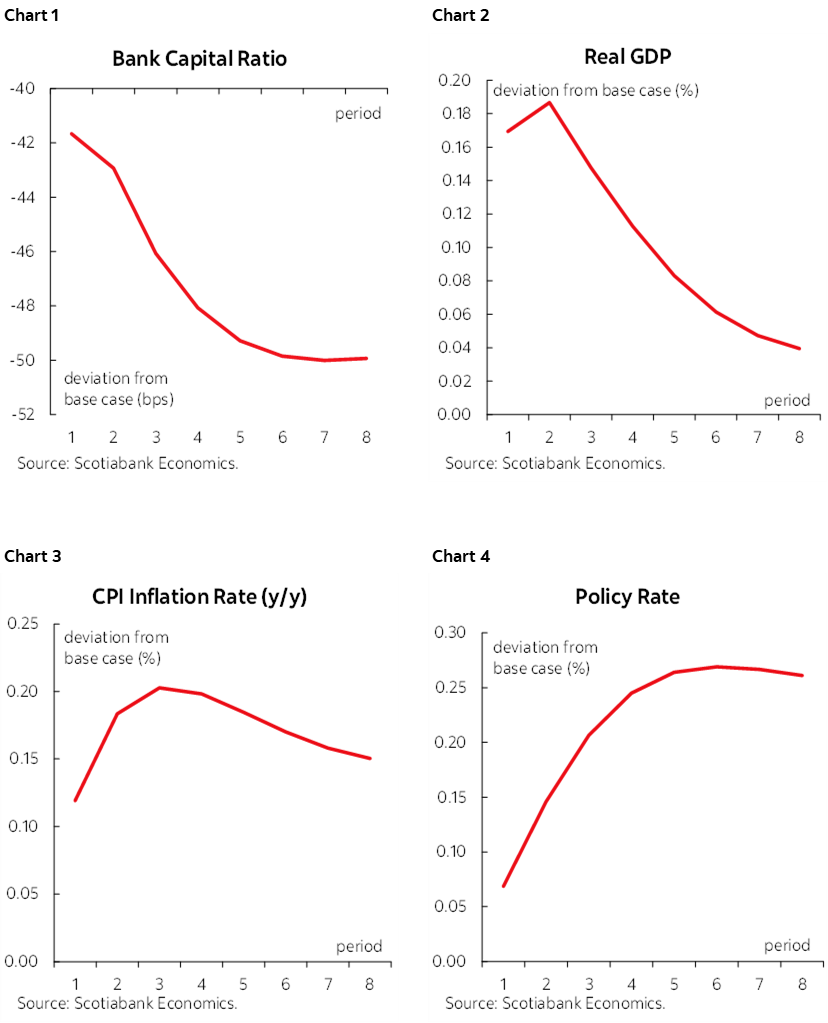

We used a series of alternatively specified structural vector auto-regression (SVAR) models to identify the impact of changes in capital ratios on the economy and policy rates. These are described in Appendix 1. These SVARs show a clear, sizeable, and rapid impact of changes in capital ratios on economic activity and eventually inflation and the policy rate (see charts 1 to 4 on page 2). This suggests that a 50 basis point decline in bank capital ratios is equivalent to a peak impact of a 25 basis point decline in the Bank of Canada policy rate. From a timing perspective, most of the impact on growth happens in the first two quarters while the impact on policy rates peaks about 5 quarters after the change in capital ratios.

A key challenge in mapping changes in the capital ratio to policy rates is the impact of credit demand to a change in credit supply. While our empirical approach suggests that past changes in capital ratios have had an impact on economic growth through higher credit demand, it is possible that this impact may be lower in present circumstances given the level of uncertainty currently impacting the economy (concerns about the review of CUSMA, the impact of the war on spending power, and general uncertainty regarding future potential actions of the U.S. President). Moreover, liquidity is currently scarce, and that may limit a bank’s ability to fund asset growth even if they have the capital space to do so. Because of this, it is perhaps best to think of our results reflecting an upper-bound of the impact. Nevertheless, the general point holds: a lower DSB is equivalent to a quasi easing in monetary policy.

IMPLICATIONS FOR MONETARY POLICY

Regulatory policy can have an indirect impact on monetary policy through two key channels. These policies can alter the supply of credit to the economy through a variety of regulatory decisions. If impactful enough, this can at times influence central bank policy. Regulatory policy can also impact the transmission mechanism by modifying the financial system’s response to changes in central bank policy rates.

Our results suggest that the positive economic impacts of the change in the DSB may need to be considered by the Bank of Canada as it sets its policy rate going forward.

APPENDIX 1: STRUCTURAL VAR APPROACH

To analyse the impact of a change of bank capital ratio regulation on the economy we use a structural VAR approach (SVAR). This empirical approach analyses the interaction between macroeconomic and financial variables among each other and across time. Our main SVAR model includes the following variables in this order:

i) The first difference of the bank capital ratio

ii) The first difference of the log of real Canadian GDP

iii) The first difference of the Bank of Canada core inflation (i.e. (Trim CPI+Median CPI)/2, Y/Y)

iv) The first difference of the nominal policy rate

v) The first difference of the log of the real bilateral Canada/US exchange rate

Since we are interested in measuring the impact of a permanent change of bank capital regulation by OSFI we use long run restrictions to identify the structural shocks of the model. Also, given that the permanent component (trend) of the Bank capital ratio reflects only the changes of regulation, and is therefore exogenous to the other variables in the long run, we insert this variable first in the ordering of the VAR. Akaike, Schwarz and Hannan-Quinn lag length selection tests all select one lag for the SVAR which is not surprising given the small size of our sample (2008Q2–2026Q1).

Results show that a permanent decrease in the capital ratio of 0.5 percentage point increases GDP by about 0.18 percent, lifts core inflation by about 0.2 percentage point and increases the policy rate by 25 basis points. Unsurprisingly, our Canada-US Macroeconomic model suggests that the Bank of Canada must temporarily increase its policy rate by 25 basis points to offset this shock.

The results are robust across a broad range of alternative specifications of the SVAR:

i) Lags selection: we also evaluated the same SVAR with two lags instead of one. Results are all qualitatively the same and the impact of a permanent change to the Bank capital ratio on macroeconomic variables are slightly bigger.

ii) Variable inclusion: we tested SVARs that also include the price of oil and/or the labour productivity, and the results are very similar.

iii) Finally, we test SVARs where we introduce the core inflation rate and the nominal policy rate in levels and the results are qualitatively the same but the impact on real GDP is somewhat larger and the effect on inflation and the policy rate a bit smaller, but the latter is still rounding at 25 basis points.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.