- Canada has been forced to revisit long-standing growth models amidst geopolitical and economic turmoil. But few files show the strain on legacy policy architecture more clearly than those meant to support Canadians as they age.

- Almost one in five Canadians is over 65 today and the age—and cost—curve will only steepen further ahead. Social infrastructure is already stretched, fiscal pressures are growing, and a fragmented policy landscape is no longer fit for a much older future.

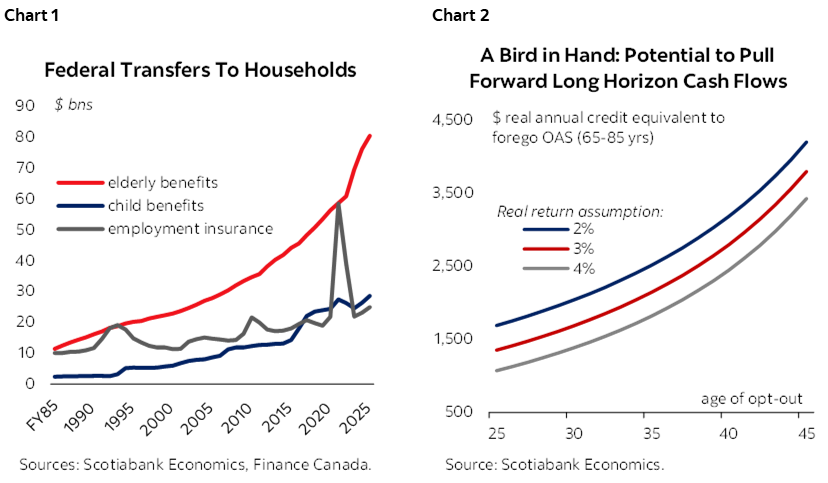

- Old Age Security is a natural place to start because it sits squarely within Ottawa’s control. OAS now represents nearly six in ten federal dollars transferred directly to Canadian households and is on track to approach $100 billion annually by the end of the decade (chart 1).

- Its broad-based structure is increasingly hard to defend as trade-offs across competing priorities— and generations—mount. Yet retrenchment is politically challenging for understandable reasons. Older households have planned around OAS even as younger Canadians increasingly doubt it will be there for them down the road.

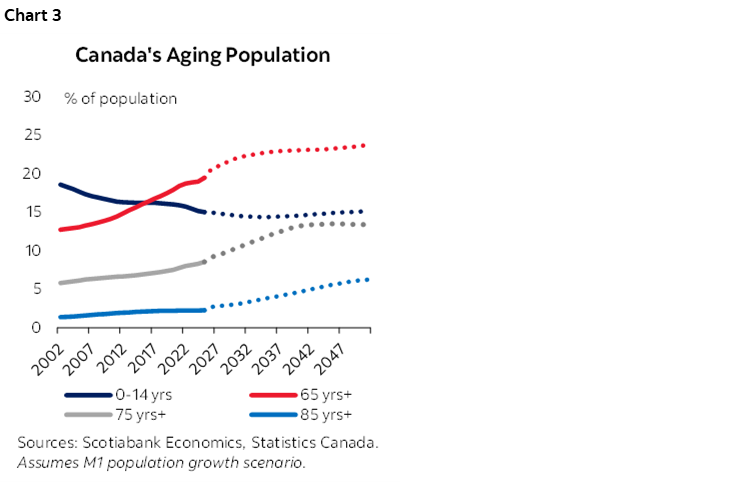

- A more productive debate could focus on bold redesign. One option is to recast OAS from a near‑universal pension at 65 into a lifecycle model that supports saving earlier and insures longevity later. Practically, this could pair earlier locked‑in retirement credits with pooled lifetime income—or mortality credits—later. This would leverage known valuation and behavioural wedges to deliver stronger outcomes over a lifetime (chart 2).

- As Ottawa develops ways for Canadians to invest alongside its Build Canada plans, OAS reform could be part of that conversation—especially where long-horizon returns would compound for younger generations but barriers still exist.

- This is only one idea to reframe the conversation. The broader imperative is a more deliberate, thoughtful dialogue on modernizing OAS in a way that lets Canadians of all ages see their own financial future in it.

AGE OF CONSTRAINT

Canada has been forced to rethink many of its policy playbooks as geopolitical turmoil upends old economic models. Governments have moved quickly on trade, investment, defence, and industrial strategy. Yet they remain remarkably complacent about the most predictable pressure of all as the nation grows older by the day.

The country has not even entered peak aging yet, but the warning signs are already pervasive. From stretched healthcare systems to fragmented home and long-term care to uneven retirement readiness in an age of longevity, Canada is ill-prepared for the much more resource-intensive phase still ahead as the Baby Boom cohort ages over the next two decades.

Intergenerational blame is unproductive. The deeper issue is perhaps the most consequential policy coordination failure of our time that spans generations. Older Canadians face a weakening late-life social contract as supports fall short precisely when they need them most, while younger Canadians increasingly doubt that the same bargain will endure for them down the road.

The required response is system-wide. Still, Old Age Security (OAS) is a pragmatic place to start as a large and fiscally significant policy framework that no longer matches Canada’s demographic realities—and one that sits squarely within federal control.

READ THE LARGE PRINT

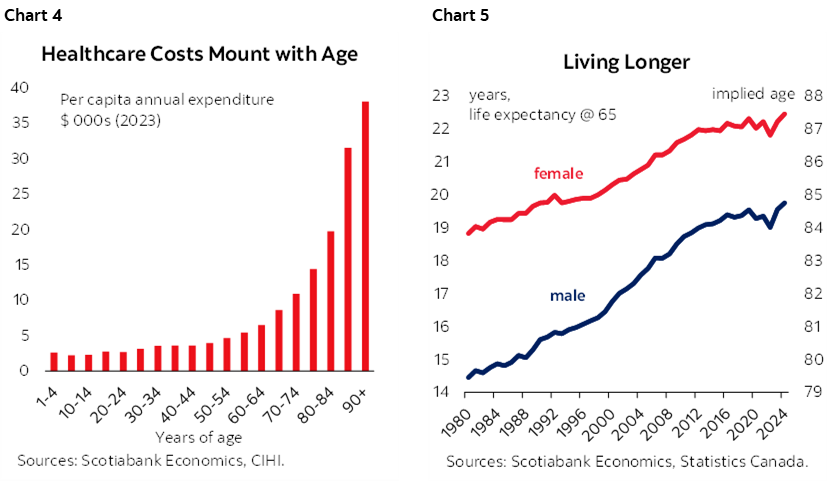

Canada is rapidly aging. Nearly one in five Canadians is already over 65, and that share is expected to hit one-quarter by mid-century. The 85-plus cohort is expected to triple over the same period as longer lives push more Canadians into advanced age. The next phase of aging will look very different—and cost much more—than the one the country is experiencing now (chart 3).

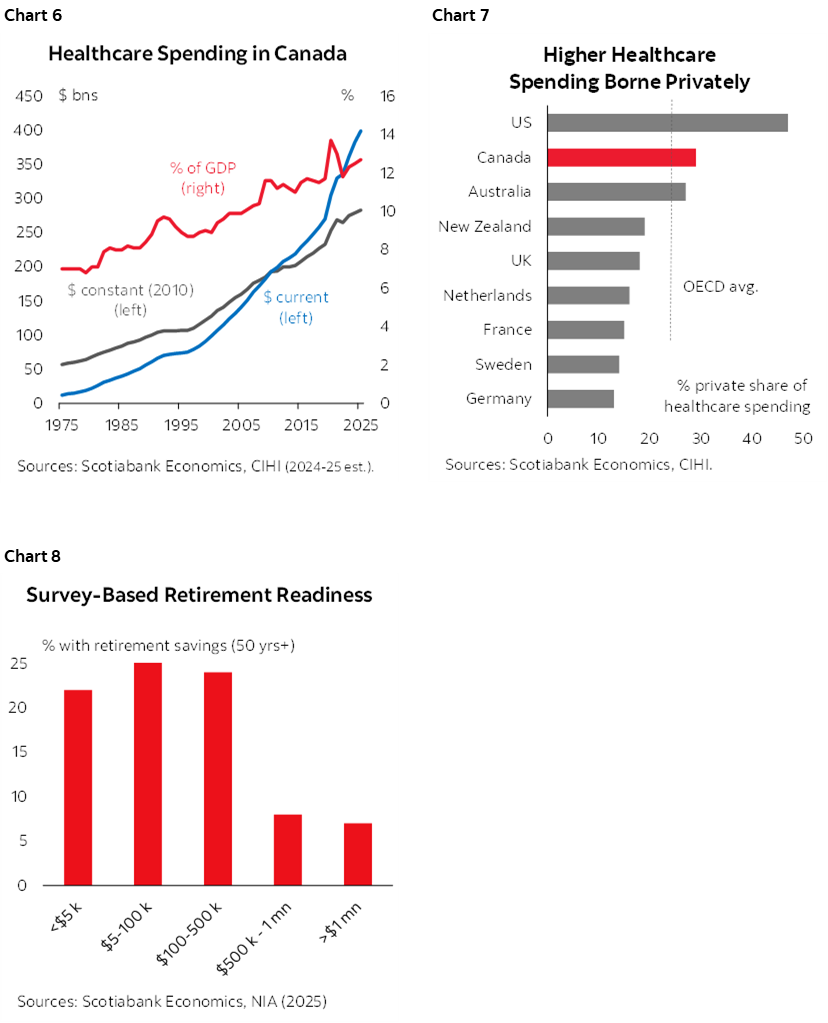

Costs are concentrated in later years. Healthcare spending on those over 85 is almost quadruple that of those in their 60s (chart 4). And while Canadians are living longer (chart 5), healthy years have not kept pace. A 65-year-old man today can expect roughly a quarter of his remaining years in less than full health. By age 85, over 90% live with at least one chronic disease—and 80% with multiple conditions. Seniors already account for nearly half of health spending in a system approaching 13% of GDP.

The strain is already visible. One in five Canadian adults lacks a regular health care provider according to CIHI, while Statistics Canada estimates roughly 600,000 Canadians report unmet home care needs. Long-term care pressures are also spilling into hospitals, where more than 6% of stays involve alternative level of care patients even as about 10% of long-term care residents could have been supported at home. These already-stretched systems will face a doubling in demand within the next five years alone according to CMA projections.

Long-term fiscal assessments likely understate the exposure. General government debt paths can look manageable under current-policy assumptions, but a meaningful share of age-related costs still sits outside public balance sheets. Scotiabank Economics has estimated that fully reflecting non-universal components such as long-term care and home care could add roughly 2 percentage points of GDP to annual spending. Much of that implicit burden sits on subnational balance sheets with recent provincial budget overruns an early warning sign.

Absent bold and coordinated course-correction, the path forward looks like a combination of muddling through with increasingly greater costs borne privately (charts 6 & 7). It does not appear most households are ready for that future (chart 8).

LAYERS OF COMPLEXITY

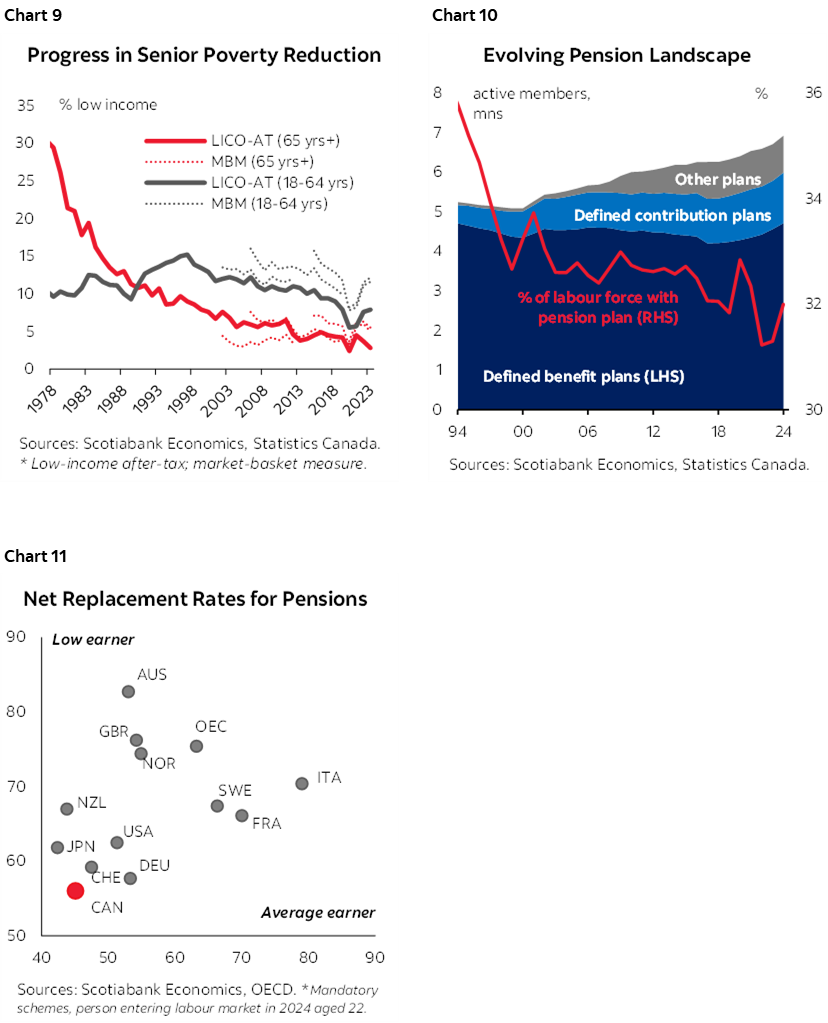

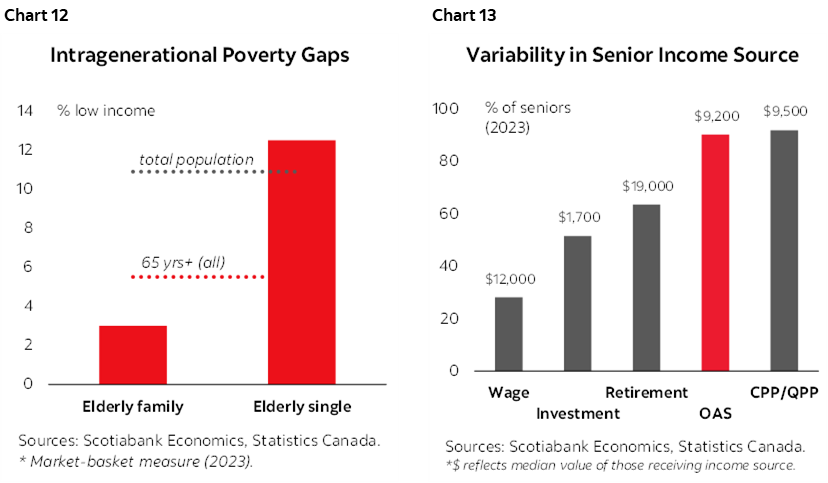

Canada’s retirement income system as a whole deserve solid marks. Its three-pillar design—a public floor, an earnings-related public pension layer, and a private savings sleeve—remains broadly sound by international standards. The CPP/QPP is fully funded and actuarially stable, OAS and its companion Guaranteed Income Supplement (GIS) have helped reduce senior poverty, and private wealth has grown through an evolution in workplace pensions and voluntary savings frameworks. Still, there are gaps including low coverage for the most vulnerable (charts 9–11).

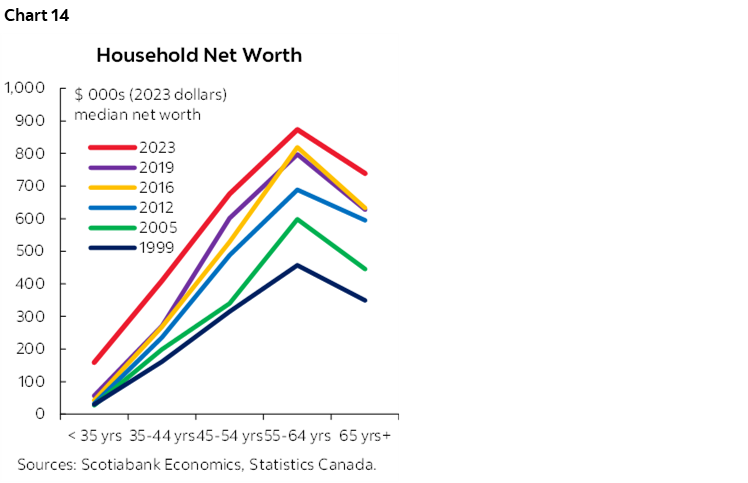

Metrics of later‑life financial security show wide variation within the senior population. In the 2023 Survey of Financial Security, the median net worth of a pre‑retirement household was about $873 k—and would look even stronger today. But outcomes diverge sharply across rooftops. A household approaching retirement with a primary residence and an employer‑sponsored pension had a median net worth of roughly $1.4 mn compared with less than $12 k for those with neither. A meaningful share of seniors still enters retirement with no private pension coverage or registered savings, and a gap that is clearly reflected in their income sources—and their vulnerability—in retirement (charts 12 & 13).

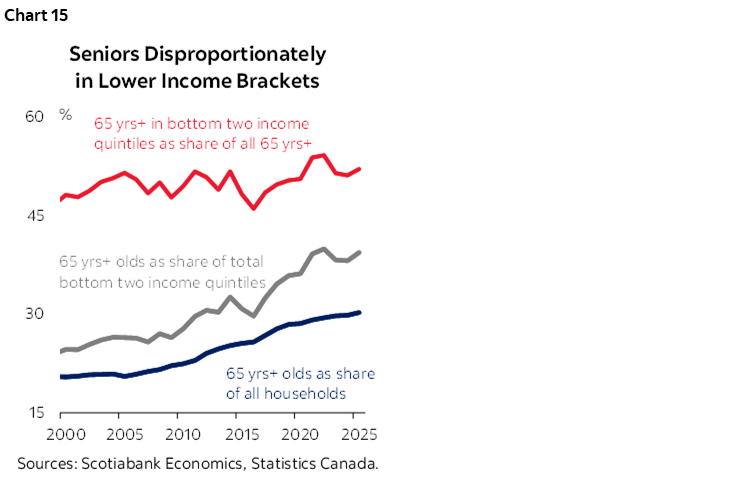

Intergenerational tensions are also rising. Younger households saw a pandemic-era boost in paper wealth (chart 14), but pessimism remains pervasive. The path to homeownership and financial security feels steeper and less certain than it did for earlier cohorts. Public debt and rising tax expectations are reinforcing those pressures, even if older households’ wealth largely reflects normal lifecycle accumulation.

The challenge is compounded by imperfect metrics. Policy still leans heavily on income-based measures of eligibility and vulnerability, even though income can be a weak proxy for financial need in retirement. Many older households actively manage income drawdown for a wide range of reasons grounded in the decumulation phase. As a result, senior households disproportionately appear in lower income brackets despite holding substantial assets. Over half of all senior households land in the bottom two income quintiles (chart 15). This can distort readings of inequality and dilute the effectiveness of policy targeting.

As Canada ages, the ability to distinguish normal lifecycle patterns from genuine economic hardship becomes more important. Otherwise, perceptions of fairness become even more volatile—and harder for policymakers to navigate—as dissatisfaction rises across the age spectrum.

BUILT FOR YESTERDAY

OAS was built for a much younger country with shorter life expectancy. In 1952, OAS kicked in at age 70. The senior population was about 7% and a 65-year-old man’s life expectancy was 78. Today, nearly 20% of Canadians are 65+ and lifespans over six years longer. This has created a growing mismatch in a program that concentrates broad support early in retirement even though the greatest risks are increasingly concentrated in later years.

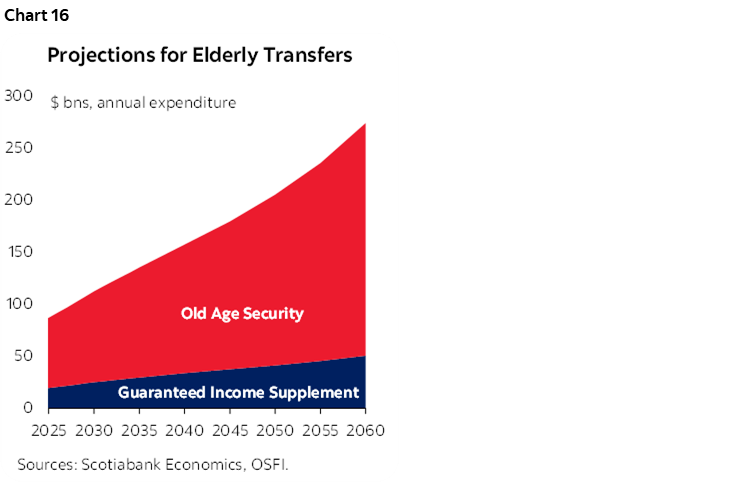

The mismatch is amplified by the scale and breadth of the program. Elderly benefits, dominated by OAS, already exceed $80 billion annually and are on track to surpass $100 billion before the decade is out (chart 16). Six in ten federal household transfer dollars now go to senior households. Gradual claw back only begins at an individual income of $95 k with full claw back at $155 k. About 7.4 mn senior households receive OAS with OSFI estimating only about 8% are affected by the recovery tax—and less than 3% subject to full recovery.

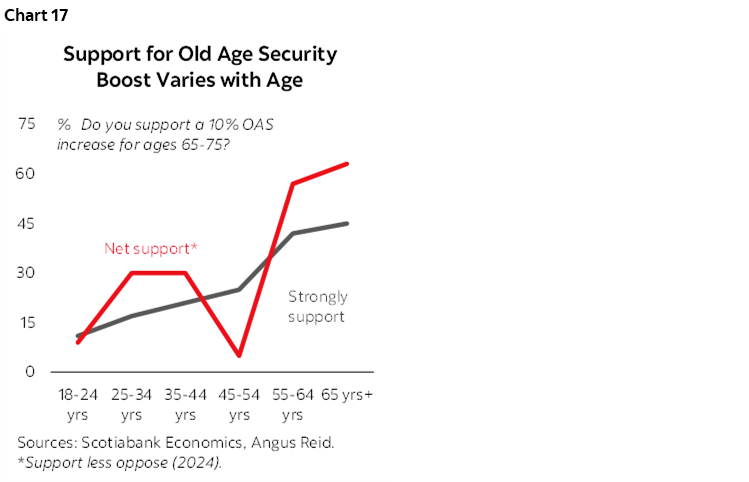

Past governments have tried to adjust OAS at the margins. In 2012, the Harper government moved to raise the eligibility age to 67 (with a decade‑long phase‑in), only for the Trudeau government to restore it to 65 in 2016. Ottawa expanded it further in 2022 with a 10% boost for those aged 75+, and pressures for additional expansion continue to surface despite polarized support across age groups (chart 17). These episodes underscore how difficult retrenchment becomes once a near‑universal benefit is embedded in household expectations.

Ottawa has tried to nudge OAS support into later life with incentives. Since 2013, seniors can opt to defer OAS to age 70 in exchange for an actuarially neutral increase of 0.6% per month—for a total boost of 36%. A majority of retirees will live longer to come out ahead yet deferral has remained modest in the low single-digits.

This safe-yet-sorry paradox is all too familiar. Retirees may hold on to assets for fear of future shortfalls, but in doing so may underspend even as they under-insure against that risk. People often prefer cash now over a larger benefit later. Pension experts* have long pushed for greater use of pooled annuities and related longevity-risk products because they can narrow the gap between the desire for protection and the cost of fully self-insuring. Despite enabling legislative changes, uptake is limited as these products remain unfamiliar and still face a range of other behavioural barriers.

The current framework is not only misaligned with modern lifecycle risk. It also does little to shape behaviour. It neither encourages earlier saving nor improves protection against late-life risk. A more pragmatic question is how OAS might be redesigned to work better across the lifecycle and across generations in an era of longer lives.

BRIDGING FOR TOMORROW

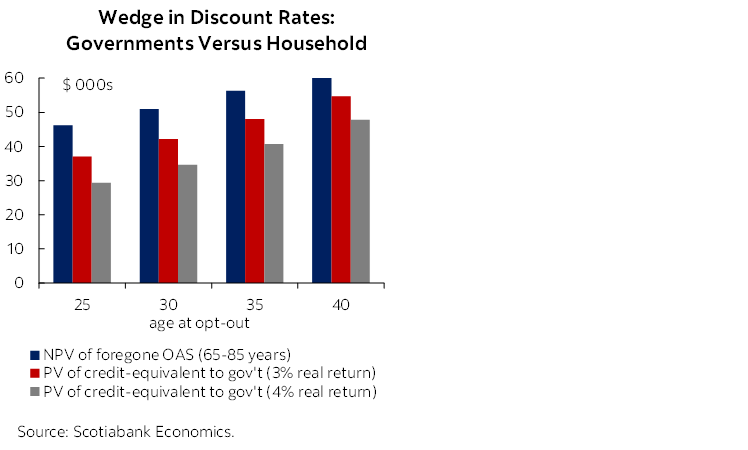

One option could recast OAS from a broad public entitlement at 65 into a model that builds private retirement assets earlier while insuring longevity risk later. Such a design could unlock value from two key wedges: a timing one between household and government valuation of future cash flows, and mortality uncertainty that can make pooled risk more efficient—and more valuable—later in life.

The logic is simple. A dollar received earlier in life can be more valuable to a household because it has more time to compound through investment, while governments can deliver equivalent future benefits at lower cost today when discounting at the risk‑free rate. (And young people today may further discount those future cash flows based on a pessimistic probability of those benefits being around decades from now.) Further along the age curve, pooled mortality risk could offer advantages (or complements) to individual savings in protecting against the potentially costlier risks that arise later in life.

Specifically, working-age Canadians could exchange a future OAS claim for annual locked-in retirement credits paid earlier in life. Those credits would flow through familiar pension-style registered accounts with individual choice preserved within established guardrails. At retirement, part of the balance could remain available for flexible drawdown, while part could convert into a pooled lifetime income product. A menu of options would be modeled on structures such as advanced life deferred annuities (ALDAs) and variable payment life annuities (VPLAs). The aim would be to support earlier asset accumulation and stronger late-life protection.

The logic may be simple, but uptake and outcomes would still depend on design. The model is most compelling for younger households with long investment horizons. Transitional design could create voluntary pathways for pre-retirement and newly retired Canadians to swap OAS claims for later longevity-pooling credits, helping build market depth and familiarity before any broader default model is applied to younger cohorts.

The design could generate welfare gains through additional channels. A more robust insurance feature could improve consumption smoothing by allowing households to spend more confidently earlier in retirement instead of underspending out of fear they may outlive savings. It could also reduce consumption distortions created by the OAS claw back framework.

Such a redesign would also reshape the fiscal profile intertemporally. Higher uptake would pull federal costs forward from outer years, even if the government’s net present liability declines. Because OAS is pay-as-you go, these claims are not explicit liabilities on Ottawa’s books today rather implicit claims on future taxpayers. At a time of rising intergenerational strain, that fiscal reshaping may be a feature, not a bug.

A BETTER DEAL FOR LONGER LIVES

Longer lives should be a gain in wellbeing, not a growing source of worry. The reforms needed are broader than OAS, but the country has to start somewhere. OAS is a practical place to begin because it was built for a different era and no longer reflects today’s demographic and socioeconomic realities. Putting redesign on the table should not be about revisiting old ideological fights. It should be framed as an opportunity to give Canadians across the lifecycle a more credible and practical financial foothold in an era of longevity—one they may judge less at the ballot box than in their own pocketbooks.

*This paper cannot do justice to depth of pension‑policy expertise in Canada. Keith Ambachtsheer and Bonnie‑Jeanne MacDonald, for instance, have been instrumental in advancing legislative reforms that paved the way for more age‑friendly pension products in Budget 2019, alongside broader work on system design and behavioural barriers. More recently, HEC Montréal researchers Philippe d’Astous and Franca Glenzer have highlighted the role of overconfidence—including in public old‑age benefits—in contributing to weaker financial decision‑making.

A BIRD IN THE HAND OVER TWO IN THE BUSH

For simplicity, assume a real, after-tax annual benefit of $6 k starting at 65 with an expected lifespan of 85. The actuarial value at age 65 of that stream is roughly $100 k when discounted at a 2% real government rate.

For a 30‑year‑old today, apply an additional 35 years of discounting to reflect their opportunity cost. On a government basis (2% real), the present value is about $51 k. On a household basis, using a 4% real market return, the indifference value is about $35 k (or $42 k at 3% real). Amortized over ages 30–64, that implies an equivalent annual credit of roughly $1,400 (or $1,700 at 3%) that would leave a rational, unconstrained individual indifferent, all else equal. As the investment horizon shortens with age, the present value rises.

These calculations rely on a few deliberate simplifications. They assume the credit is invested rather than consumed and treat the exercise as tax‑neutral, abstracting from behavioural constraints, liquidity needs, and household differences. The example is intentionally stylized: its purpose is simply to show how a valuation wedge arises when governments discount future obligations at a low risk‑free rate while households apply a higher private opportunity cost.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.