EXECUTIVE SUMMARY

- Ongoing military actions in Iran have increased the likelihood of broader regional conflict and raised the probability of future oil supply disruptions, pushing oil prices higher in early trading.

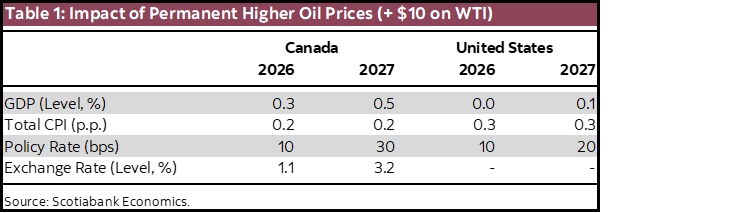

- Because the ultimate path of oil prices remains highly uncertain, we provide model-based rules of thumb simulations for a persistent $10/bbl increase in WTI. Canada would likely benefit from a positive terms of trade shock (GDP +0.5% in year two, CPI +0.2 p.p.), while the U.S. would see a small net gain driven by investment in the shale sector (GDP +0.1% in year two, CPI +0.3 p.p.).

- Key uncertainties include the duration of the shock, the possibility of a weak CAD-oil correlation, and the potential tightening of financial conditions—each of which could materially alter the economic impact.

Heightened geopolitical risk in the Middle East has materially increased the probability of a broader regional conflict. Ongoing military operations in Iran have introduced significant uncertainty for global energy markets, elevating the risk of future supply disruptions. While the initial market reaction reflects a “fear premium,” the persistence and magnitude of the price surge will ultimately depend on whether physical supply is impaired.

Given the fluid environment, we are providing model-based rules of thumb to help assess the potential macroeconomic implications of a sustained oil price shock for the United States and Canada.

MACROECONOMIC IMPACT: MODEL SIMULATIONS

Table 1 summarizes the estimated impact of a $10/bbl increase in WTI that persists for at least two years, based on the Canada-U.S. Scotiabank Macro Model. The model incorporates both the first round effects of higher oil prices and the endogenous monetary policy response that typically offsets part of the shock. The results scale approximately linearly; for example, a $20/bbl shock would generate roughly double the impacts shown below.

Canada: Terms of Trade Shock

As a net energy exporter, Canada benefits from an improvement in its terms of trade when oil prices rise, but the transmission channels differ in strength:

- Income & Investment: Higher oil prices represent a sizeable nominal income transfer into Canada. Energy sector profits and investment rise, supporting employment and eventually household spending. These gains are partly offset by a squeeze on real disposable income; higher gasoline prices act as a regressive tax, reducing discretionary purchasing power. On balance, real GDP increases by 0.5% in year two.

- Inflation & Policy Response: Total CPI rises by 0.2 p.p., though core inflation remains relatively contained. Stronger domestic demand still generates some price pressures, prompting the Bank of Canada to increase the policy rate by roughly 30 bps than otherwise.

- Currency Appreciation: Stronger demand for Canadian dollars leads to a CAD appreciation of about 3%, dampening imported inflation but weighing on non‑energy exports.

United States: Investment Sensitivity and the Net Exporter Pivot

Traditionally, the U.S. economy reacted negatively to increases in oil prices because higher energy costs reduced household purchasing power. However, this dynamic has changed since the U.S. became a net exporter of oil. The net macroeconomic effect is now slightly positive (+0.1%) though still modest:

- Investment Sensitivity: While higher oil prices lead to higher production costs, U.S. shale investment responds strongly to price signals. Higher oil prices raise energy sector capital spending, supporting employment and household income.1 However, higher energy costs simultaneously erode household purchasing power, partly offsetting the gains.

- Inflation & Monetary Policy: CPI inflation is more sensitive to fuel prices in the U.S., rising 0.3 p.p. The Federal Reserve is expected to tighten policy modestly—20 bps above baseline—to contain the inflation impulse.

KEY UNCERTAINTIES & RISK CONSIDERATIONS

- Temporary vs. Permanent shock: The rules of thumb above assume a persistent increase in oil prices. However, if the military operations do not result in a significant reduction in oil production or any material disruption to global oil trade, the price impact would likely be much more temporary, and the corresponding effects on economic activity would be considerably smaller and shorter lasting. For example, an oil price increase lasting only two quarters would generate less than half of the reaction shown in table 1 again.

- The CAD Disconnect: The CAD–oil relationship has weakened in recent years, especially during supply driven price spikes. If geopolitical stress triggers a global flight to safety into the USD, CAD may fail to appreciate. In that scenario, the positive impact on Canadian GDP could be ~20% larger than stated in table 1 again, but inflation pressures would also be stronger.

- Financial Conditions and uncertainty effects: A geopolitical shock of this magnitude often leads to a widening of credit spreads, equity market volatility and economic uncertainty effects. If financial conditions tighten sharply, the contractionary effects could significantly dampen the positive terms-of-trade gains in both countries, and even result in a negative overall impact on the U.S. economy. In contrast however, a flight to safety would push yields lower and ease financial conditions, providing some support to U.S. economic activity.

1 This is consistent with empirical estimates from Gervais (2019), which show that oil supply shocks generated a significant increase in U.S. business investment.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.