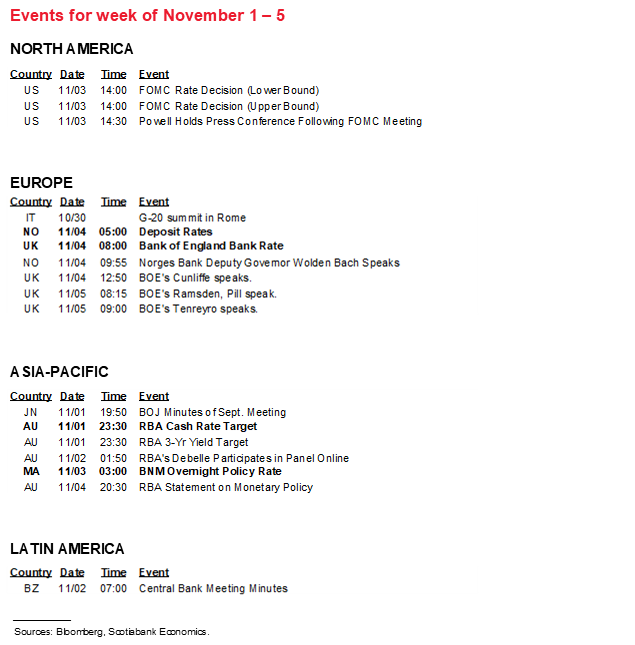

Next Week's Risk Dashboard

• US nonfarm payrolls and wages likely to accelerate

• Canadian jobs downside, wages upside?

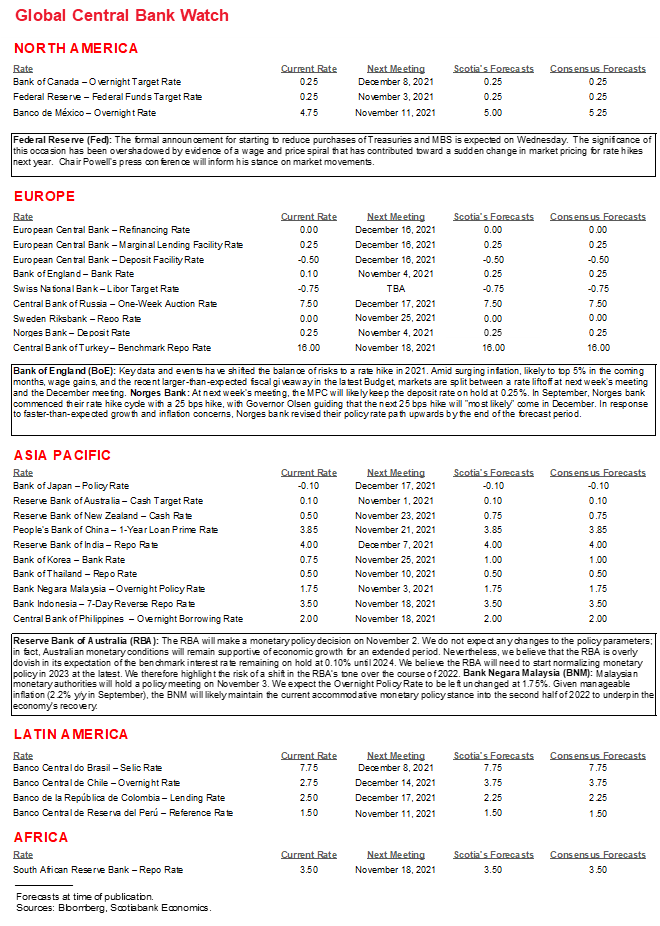

• Federal Reserve: no longer just about the taper

• Bank of England: you started it!

• RBA: Ummm…about that yield target…

• BoC: Macklem’s second chance

• Norges Bank: Little mystery here

• Ditto for Bank Negara

• OSFI may ease up

• Ontario’s fiscal update

• Other macro

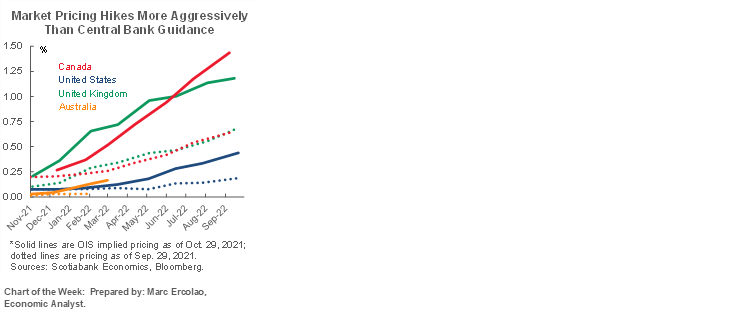

Chart of the Week

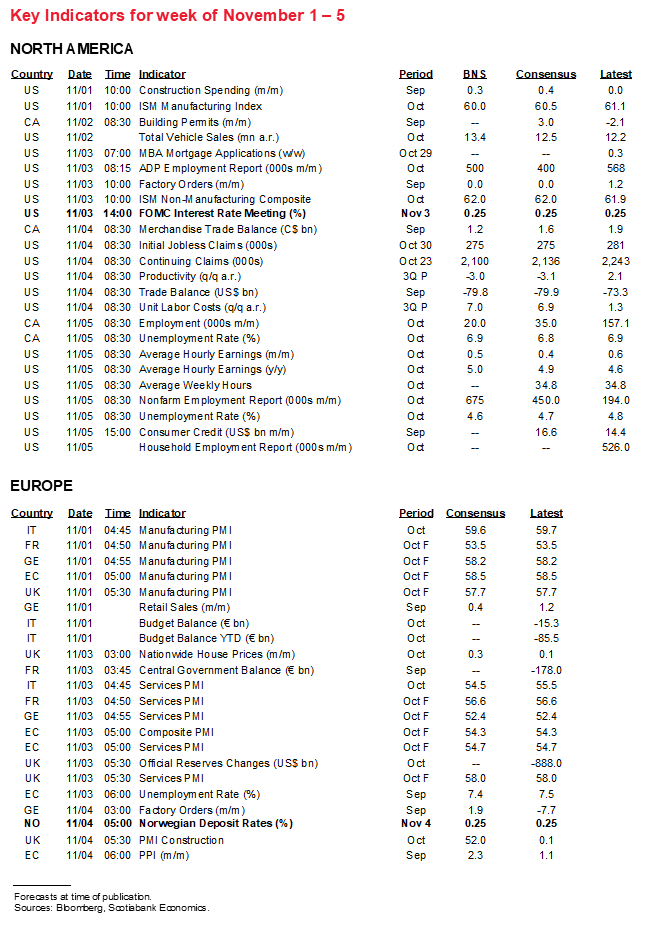

US JOBS AND WAGES—UP, UP AND AWAY?

Friday’s labour market readings for October are expected to post an acceleration of job growth and faster wage gains. I went with a nonfarm payroll gain of 675k with wage growth accelerated to 5%.

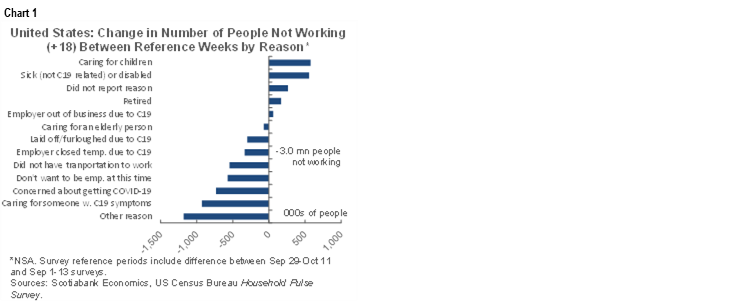

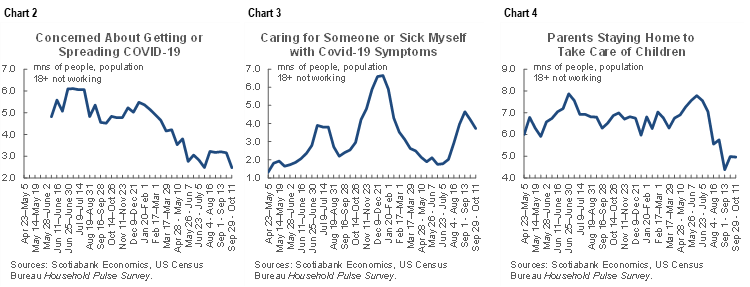

As the Delta variant’s grip subsided, it appears that more Americans became more comfortable with accepting jobs among the vast number of vacancies. To help inform this view, chart 1 shows the results of the latest Household Pulse Survey produced by the US Census Bureau. A section of the survey asks respondents to provide reasons for not working over an almost two-week interval. We can explore how the answers shifted between proxies for the nonfarm reference periods in September and October and use these responses as proxies for changes to re-engagement with the labour force. That worked reasonably well the prior month when payrolls increased by only 194k (Scotia 250k, consensus 500k) and so we’ll test our luck again with a similar approach this time by going with a strong rebound of 675k in October. That’s because of the large declines in the numbers of people who said they were not working into October across multiple COVID-19 related categories (chart 2–4).

As for wages, there is little doubt that the US labour force is on the upswing. Month-over-month annualized average hourly earnings are rising at an accelerating pace and so is the overall Employment Cost Index (chart 5). That should drive rapid growth in unit labour costs— productivity adjusted wages—when we get that figure on Thursday for Q3.

CANADIAN JOBS AND WAGES—LIKELY TO UNDERPERFORM THE US THIS TIME

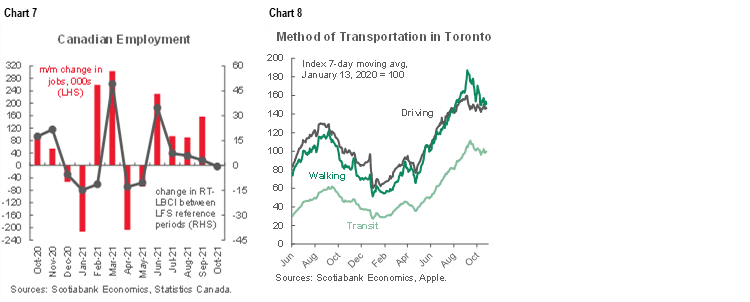

Whereas Canada’s pace of job gains outshone the US pace in September, the opposite is likely to happen in October. The US is emerging from a worse rise in new COVID-19 cases than the magnitude that hit Canada (chart 6). I went with a modest gain of 20k and an unchanged unemployment rate.

There could even be further downside risk given the connection between Statistics Canada’s Real-Time Local Business Conditions Index and monthly job changes (chart 7). Part of this index is based upon multiple mobility readings. Chart 8 shows one such example of how mobility as a proxy for economic activity has recently taken a step back, although there isn’t enough history to tell how much of this is normal at the end of summer vacation season and when the kids go back to school.

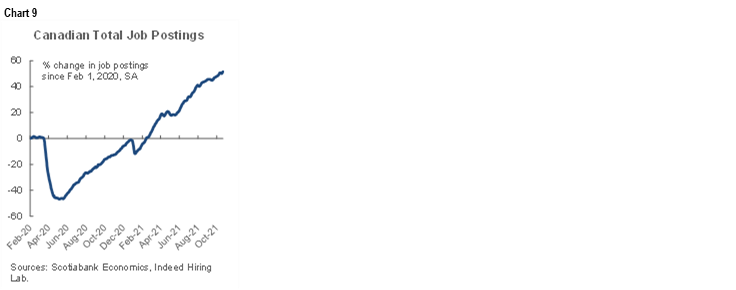

Still, any cooler employment gains would not be for lack of available openings (chart 9).

Whereas the evidence on wage inflation recently appears to be more compelling stateside than in Canada, there is also nascent evidence of such pressures in Canada that the October reading will further inform.

BANK OF CANADA—MACKLEM’S SECOND CHANCE

Fresh off his recent performance (recap here), Bank of Canada Governor Macklem has another opportunity to push back on market pricing for rate hikes starting in January when his interview with Radio-Canada airs at 11amET on Halloween. If he doesn’t do so, then the week might end that way in any event if there is a downside surprise in Canadian jobs.

Still, must it be the case that the Bank of Canada delivers what the markets have priced? The BoC’s forward rate guidance says they won’t hike until sometime between April and September and the latest GDP figures and their implications for spare capacity might reinforce this view (here).

It might also be useful to remind markets of times when the BoC has indeed surprised market pricing (chart 10). The chart shows times when one-month CDOR has changed by 15bps or more (to signify a material shock to market pricing) in the days leading up to policy rate decisions. There have been nine such occurrences over about the past twenty years. To the extent to which history is a guide, the BoC has tended to avoid surprising markets the vast majority of the time, but there is enough of a sample of occasions when it has to merit caution toward market pricing. The path toward the January and April meetings and developments across data and events will further inform the risk to market pricing.

FEDERAL RESERVE—IT’S NO LONGER ABOUT THE TAPER

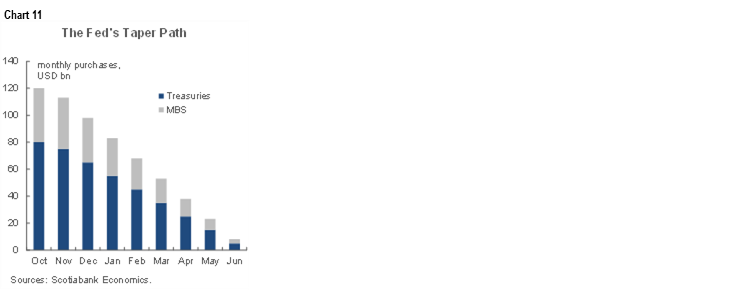

The Federal Reserve is widely expected to announce the start of its tapering plans for Treasury and MBS purchases from the respective starting points of $80B/month and $40B/month. The policy statement arrives on Wednesday at 2pmET and will be followed by Chair Powell’s press conference at 2:30pmET. There are no forecasts or dot plots due again until the December meeting.

Chart 11 shows our assumed taper path through to ending the purchase program by around next June. Recall that the FOMC set up a taper as soon as the November meeting when it said in September (recap here) that “a moderation in the pace of asset purchases may soon be warranted.” The word “soon” is the Fed’s code language for signalling something imminent. They also said that while no decision had been made on the pace of reductions at that meeting, they would nevertheless aim to end purchases “around the middle of next year.” Such guidance was reinforced in the minutes to that meeting (here).

During the press conference following the September meeting, Chair Powell said that “it would not take a knock-out jobs report to meet the test, only a reasonably good report.” Powell’s appearance on an October 22nd panel generally reaffirmed that the September payrolls report was indeed good enough to proceed with tapering.

There may be greater risk around how the Fed views inflation dynamics in light of the recent sharp acceleration of wage pressures as the heretofore missing link in the debate over sustainable wage pressures. The press conference will be monitored for questioning around how Chair Powell views the recent market moves that have brought forward pricing for Fed rate hikes to next summer. He is likely to indicate something along the lines of what others such as Governor Waller have indicated in that they would prefer a gap between ending purchases and commencing rate hikes but, should inflation persistently surprise higher, they will take needed action as the time approaches.

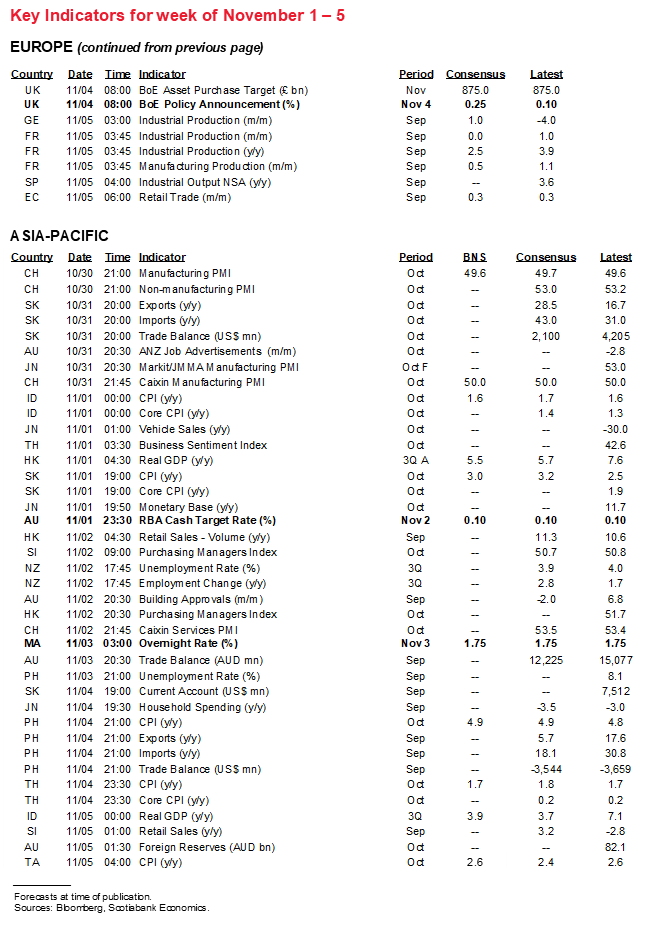

BANK OF ENGLAND—YOU STARTED IT!

One theory for the rates sell-off is that when Governor Bailey mused aloud about the possibility of a rate hike and central bankers had their IMF-World Bank meetings they decided to set off in herd like fashion away from stimulus measures and this lit up the front-ends of global yield curves. Bailey may get his chance to calm things back down. Markets and economists are divided on whether the Bank of England will begin to raise Bank Rate at Thursday’s meeting. It’s almost a 50–50 split among economists in the Bloomberg consensus in terms of a hold at 0.1% and a small 15bps hike to 0.25%. OIS markets have most of a 10bps hike priced and a 25bps increase priced for the December 16th meeting. For my two cents I think they go now and end the purchase program on target by year-end.

Forward guidance will also be key and centered around fresh forecasts for growth and inflation that may revise down growth in the nearer term and raise inflation. Having learned from the experiences at the ECB and the Bank of Canada, it is possible we hear a more forceful message from Governor Bailey if he feels market pricing for further rate hikes over 2022 is getting ahead of itself.

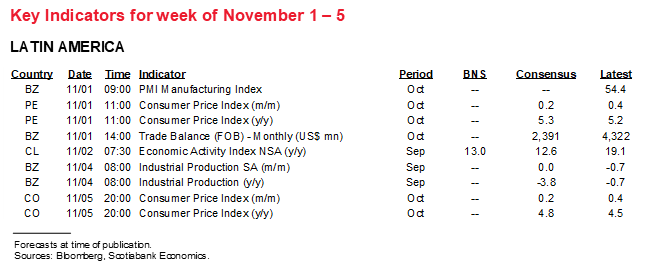

RBA—UNDER THE BUS

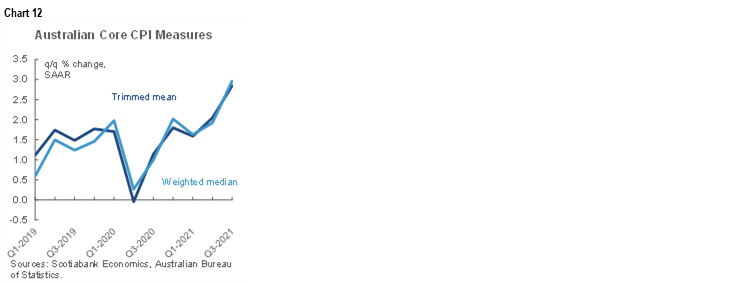

The RBA’s policy communications on Tuesday suddenly became more interesting due to two recent developments. One was the upside surprise to Australia inflation readings that has put significant upward pressure upon trimmed mean and weighted median central tendency gauges especially when judged properly as quarter-on-quarter annualized rates of change (chart 12).

Second is that when it had the chance to lean against sharp upward movements in bond yields, it passed on doing so to end this past week and thus did not repeat the intervention it led the prior week. As a consequence to higher inflation and the RBA’s recent benign neglect, the RBA’s 3-year yield target of 0.1% is being massively overwhelmed as the yield ended the week at 1.2% (chart 13). This has spawned speculation toward whether the RBA may abandon the target. It is likely to push back on the pace of rate hikes that have been factored into markets with OIS markets now expecting the cash rate to rise to about 1% in about a year’s time and closer toward 2% within two years.

Now if only all of them would lift a page from the Norges Bank’s playbook then forecasting policy decisions would be so much simpler. Mind you, more boring too. In any event, no one expects the central bank to change its deposit rate on Thursday because, well, it said after hiking to 0.25% in September that “the policy rate will most likely be raised further in December.” Forward guidance may be of greater importance after the prior meeting raised the projected path to 1.1% by the end of next year and 1.5% the year after (chart 14).

Bank Negara Malaysia is also expected to stay on hold on Wednesday at an overnight policy rate of 1.75%.

OTHER—CANADIAN BANKS AND LIMITED RELEASES

Canadian bank watchers will want to keep an eye on expected developments this week. Thursday’s speech by Office of the Superintendent of Financial Institutions’ Peter Routledge is expected to outline the regulator’s priorities and agenda (2pmET). Key will be possible guidance on the relaxation of bank capital restrictions. Canada has been somewhat of an international laggard on the issue to date. That would tee up bank earnings season that kicks off on November 30th through December 3rd.

Canada updates trade figures for September on Thursday. They will help to further inform tracking of the Bank of Canada’s Q3 GDP growth forecast of 5.5% that faces downside risk following the monthly GDP figures for August and September this past week. For a reminder of the tracking issues go here.

US releases will be followed primarily in terms of what they may reveal about the state of the job market ahead of Friday’s payrolls. Monday’s ISM-manufacturing report could weaken if it follows regional surveys lower and in light of ongoing supply-side challenges, but watch the prices and employment gauges. Wednesday’s ISM-services report arrives just ahead of the Fed and is expected to hold firm given the reopening on the services side, but watch the hiring gauge more closely in this one given the dominance of service sector jobs. ADP payrolls earlier that morning will play a similar role in terms of informing nonfarm payroll expectations but it’s often rather out there in terms of reliability. US vehicle sales are expected to modestly rebound based upon advance industry guidance.

New Zealand’s Q3 jobs and wages (Tuesday night ET) are expected to make further progress with wages continuing to accelerate.

CPI reports will land across Asia-Pacific (South Korea, Philippines, Indonesia, Thailand, Taiwan) and Latin American (Peru, Colombia and Brazil) markets and I’ll write about those in daily notes throughout the coming week.

European releases will be fairly light and focused primarily upon Germany which updates retail sales during the week, plus factory orders (Thursday) and industrial production (Friday) all for September and following the prior round of disappointments.

ONTARIO’S FISCAL UPDATE

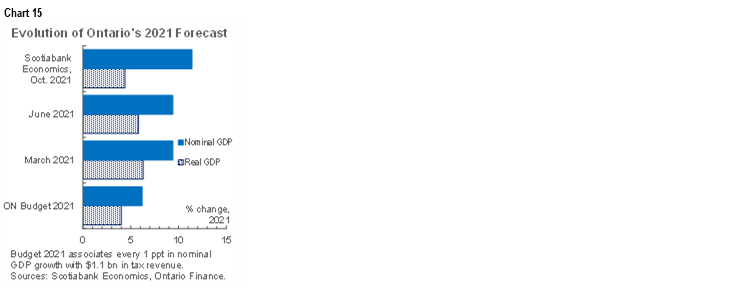

Despite recent downgrades to the economic outlook, the fundamentals suggest an improved fiscal path for Ontario in its mid-year Economic Outlook and Fiscal Review—set for publication on Thursday. A stunning $22 bn narrowing versus forecast in the province’s FY21 deficit provides a strong handoff for FY22, even if some health spending is pushed forward into this year. Inflation gains to date also leave nominal output—which anchors revenue forecasts—on pace to far exceed the 6.2% advance budgeted for calendar 2021 (chart 15). Recall that at budget time, the province pencilled in a $33 bn shortfall and linked every 1 ppt in nominal GDP growth with $1.1 bn in tax revenues for this fiscal year. On that basis, current private sector nominal output growth forecasts in the 10–11% range could generate another $4–5 bn in tax receipts. Yet semiconductor shortage-related auto production cuts spurred a 25% (q/q ann.) international export plunge in Q2; an uncertain outlook on this front may prompt new fiscal prudence. And with a pre-election budget set for the spring, there will be a natural inclination to “under-promise, over-deliver” on the bottom line this time.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.