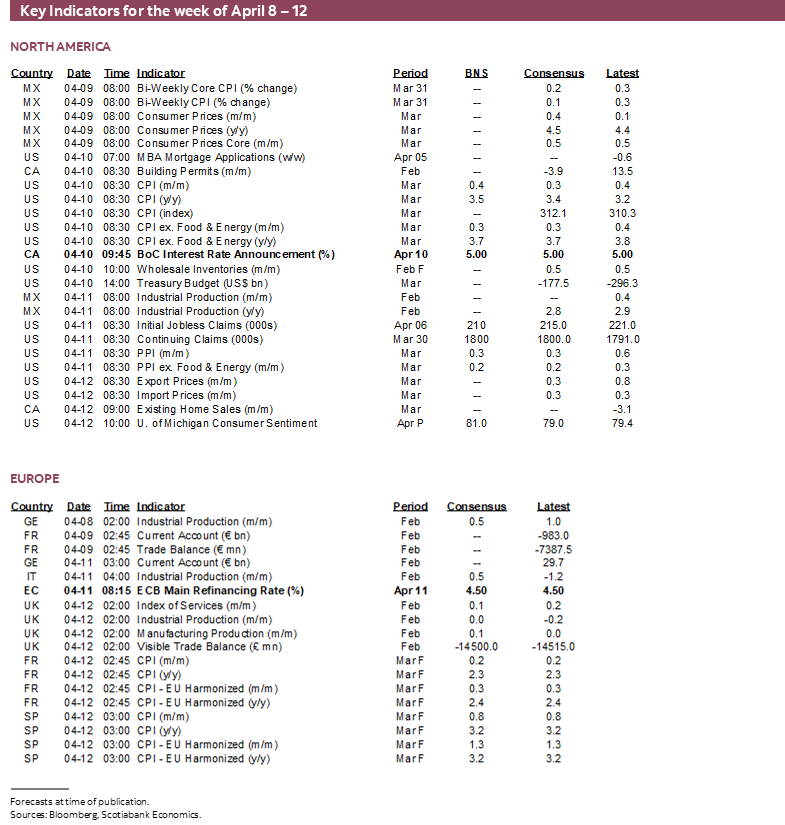

Next Week's Risk Dashboard

- Wednesday will pack a punch

- BoC: the hawkish case outweighs a dovish pivot

- US core CPI will help inform soft patch versus persistence

- FOMC minutes to further inform QT debate

- ECB: why perfectly priced for June?

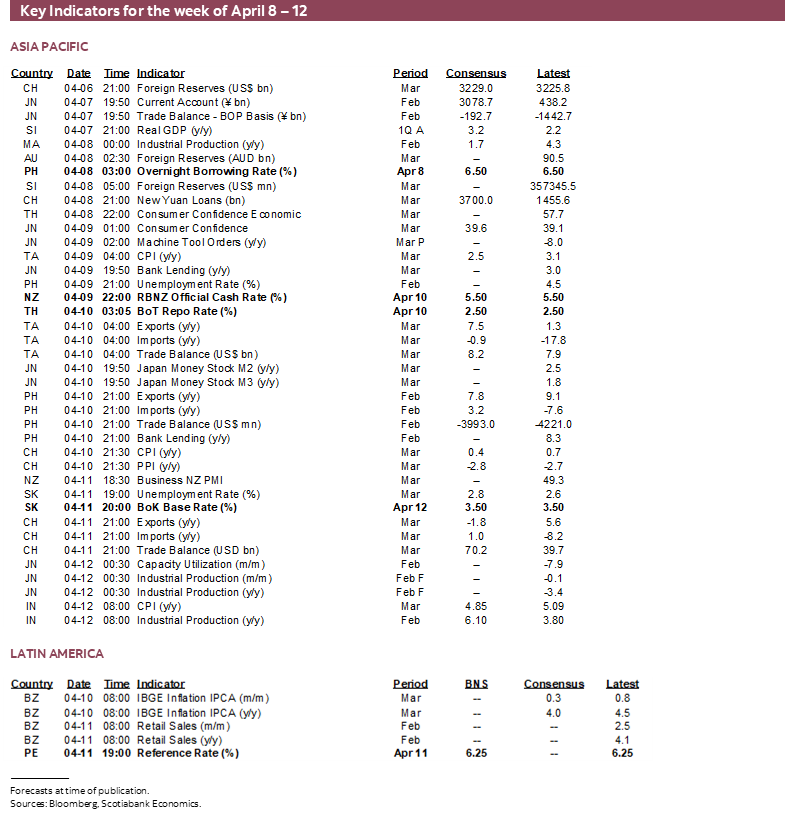

- CBs: RBNZ, Peru, BoT, BoK, BSP

- CPI: China, Chile, Mexico, Brazil, India, Taiwan, Norway, Sweden

Chart of the Week

Maybe don’t book Wednesday off. Just saying.

Three of the week’s four biggest developments will unfold on that day over less than six hours from start to finish. It starts with US CPI, then moves on to the Bank of Canada and wraps up with the FOMC minutes to the March meeting. Many of the other calendar-based developments are more likely to play backseat roles and that could also include China’s CPI reading later that evening and then the Thursday’s ECB deliberations. Several other central banks will also weigh in.

My main focus this week will be upon the BoC. While there are points to be made on both sides, I think the outcome will favour the hawks.

BANK OF CANADA—THE HAWKISH CASE OUTWEIGHS A DOVISH PIVOT

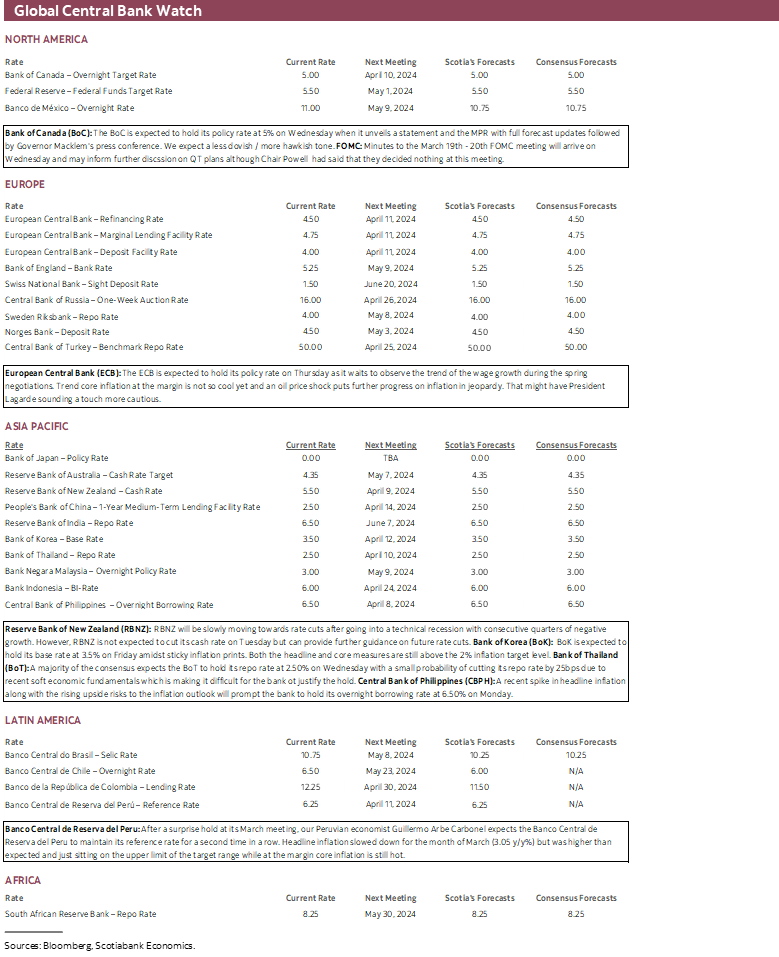

The Bank of Canada weighs in with a policy decision, statement, and full Monetary Policy Report including updated forecasts (9:45amET) and then a press conference (10:30amET) on Wednesday. No policy rate change is expected and they’ve ruled out changes to quantitative tightening for now. Key will be the bias, and on that, they should be exceptionally careful.

It’s been a tough stretch for the Bank of Canada’s forecasts. Developments since they last forecast back in January have just been too darn rosy relative to the BoC’s gloom in order to merit a dovish pivot any time soon.

The Doves’ Case

Let’s clip their wings before turning to the rest of the narrative. You could argue that the BoC will turn more dovish because of two back-to-back soft readings for core inflation, because of limited evidence that businesses’ signalled a reduction in the size and frequency of price changes going forward, because of one soft jobs report, and because they may upgrade their assessment of the supply side.

I wouldn’t and I don’t think the BoC will be of such persuasion. The jobs report was better under the hood as argued here and included evidence that wage growth remains too robust relative to the inflation target and productivity.

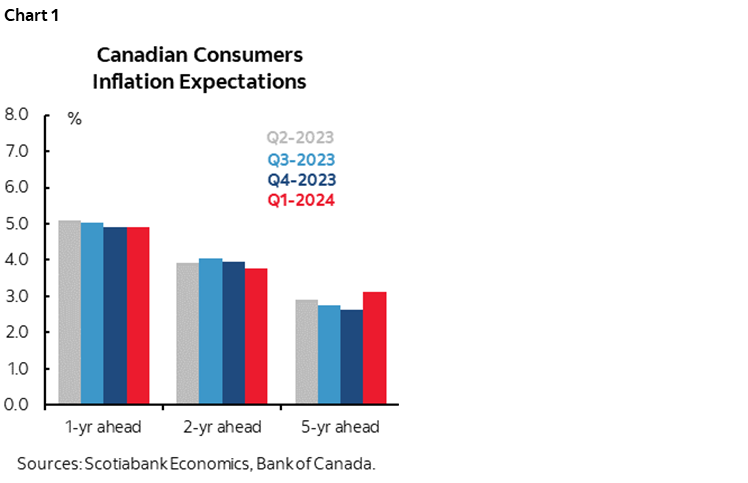

Core inflation may have had several temporary drivers to the soft patch so far this year as argued here. Business and particularly consumer inflation expectations remain too high and the backing up in long-term inflation expectations is likely to be especially disconcerting (chart 1).

The Bank of Canada is very unlikely to be swayed by one jobs report whatever one thinks happened, or two inflation reports. They’ll require much more evidence as Governor Macklem put it during the March 6th press conference when he said “…we want to see a further deceleration in core inflation in the coming months.” Note the plural reference, as opposed to the single additional month we’ve seen since his remarks.

When Deputy Governor Gravelle spoke after the next CPI report, he said it was “very encouraging” but that it’s “one number.” Technically it was two, but who’s counting. The point is that the BoC would be silly to overreact to so little data—especially in isolation of solid arguments for why bigger picture developments have added to inflation risk. It would be very surprising if the tendency were to suddenly become much more reactionary.

And on the supply side, the BoC will probably argue that the level of potential GDP is now judged to be higher than previously because of an extra year of strong population growth that is continuing even in the last monthly estimates for March. A key question, however, is whether this proves to be just a one-off.

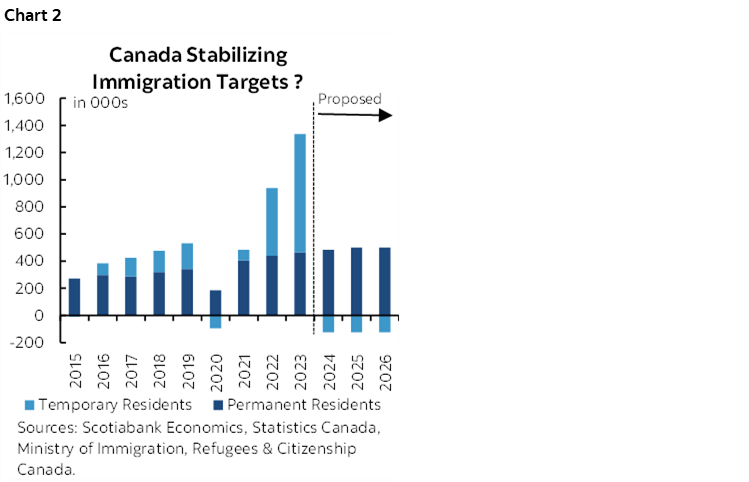

If the Federal Government succeeds in bringing down the number of temporary residents in the country by 15% from just over 2½ million at present to around 375k lower within three years, then it should have the effect of dramatically cooling population growth going forward (chart 2). They need to get the provinces on side and in turn work with educational institutions of varying repute in order to achieve this. Still, it would probably be imprudent of the BoC if they were to revise up the level of potential GDP—and hence the capacity of the supply side to absorb inflationary pressures—while ignoring the forward looking risks.

The Hawks’ Multi-Faceted Case

There is a lengthier list of reasons for why the BoC shouldn’t even hint at rate cuts any time soon.

i. Managing Markets

If they do take any step toward teeing up a cut, then they’d better have an exceptionally strong narrative. Markets are itching for an excuse to pile into the front-end and buy bonds like they’re Taylor Swift tickets. A central bank that looks through strong upside to its prior narrative that I’ll expand upon below and turns more dovish regardless would be a signal to markets that its reaction function is independent of the balanced suite of data and developments. That would be a very dovish signal and, in my opinion, policy error that could invite a response by markets to price more aggressive cuts thereafter, and to forecasters to upgrade GDP and inflation forecasts going forward and thus prolong efforts to contain the painful consequences of high and volatile inflation.

ii. Serial Upside to GDP Growth

Let’s start with GDP tracking by making two observations:

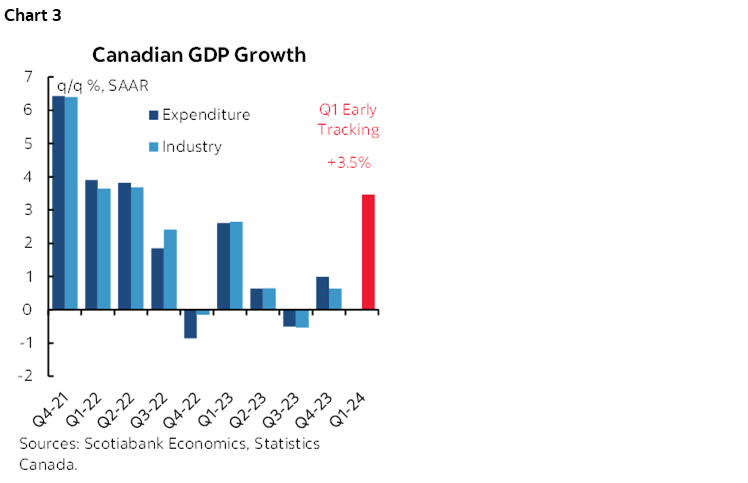

- 2023Q4: They forecast 0% q/q SAAR in the January 24th, 2024, MPR. We got 1%. Score 1 for upside. A 1% beat is nothing to spit at.

- 2024Q1: They forecast 0.5% q/q SAAR in the same January MPR. We're tracking somewhere around 3½%. There is still significant risk to this estimate given a lot of data that is yet to come, but we’re confident that the BoC will need to sharply raise its projection. Score 2 for upside.

These are very large forecast upsides as growth vaults to its strongest pace in year (chart 3). On their own, they would sharply narrow the negative output gap measure of slack in the economy. How the BoC fudges estimated potential GDP could partially offset the positive surprises on actual GDP growth.

These are serial upsides to the BoC’s serially gloomy view. They fundamentally challenge the BoC's confidence in the Canadian economy opening as much slack as they had thought at the start of the year and in 2024H1 being the worst for the economy. There are still plenty of forward-looking risks, but they have to acknowledge that the latest two quarters are evolving considerably better than they feared.

This rebound evidence also reinforces my argument throughout the past year that the BoC was too quick to take credit for dampening growth with its rate hikes and too dismissive toward other causes of soft GDP growth. There is of course some evidence of rate effects on consumption, but they were too dismissive toward the growth dampening effects of inventory shedding that shaved at times multiple percentage points off of quarterly growth starting in 2022Q4, strikes that cost many hours worked and hence production, the effects of wildfires, and considerations such as unplanned maintenance and retooling in sectors like autos, petrochemicals and mining.

iii. Fiscal Easing Cancels Monetary Easing

Once upon a time we used to beseech governments to pitch in and help central banks while steering through the Global Financial Crisis and its aftermath. Now we can’t stop them.

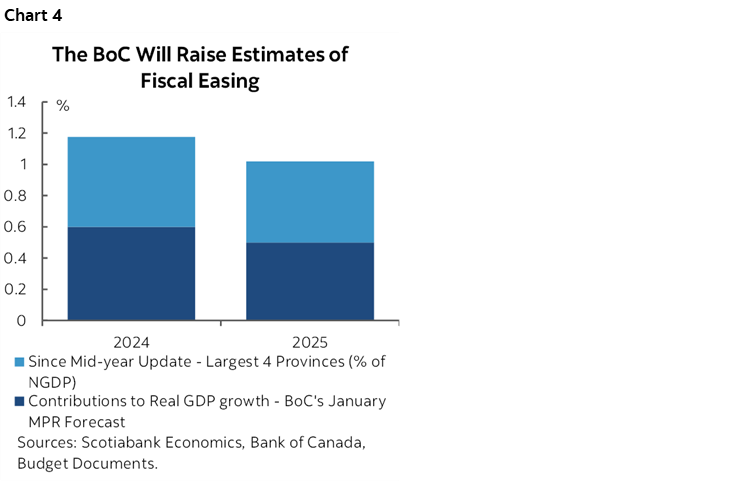

The BoC’s estimate of fiscal contributions to growth probably has to be revised sharply higher. They had figured around a 0.5–0.6 ppts weighted contribution to growth in 2024 and 2025. Without even being able to incorporate the Federal budget on the 16th and considering just the four largest provinces reveals that the contribution to growth from government spending is tracking about double what the BoC had estimated (chart 4). The Feds are likely to add to that estimate of fiscal contributions to growth and are floating expansionary components of the Budget each week in advance. Recall that Governor Macklem warned that if governments added more to fiscal easing, then it would only further complicate his job.

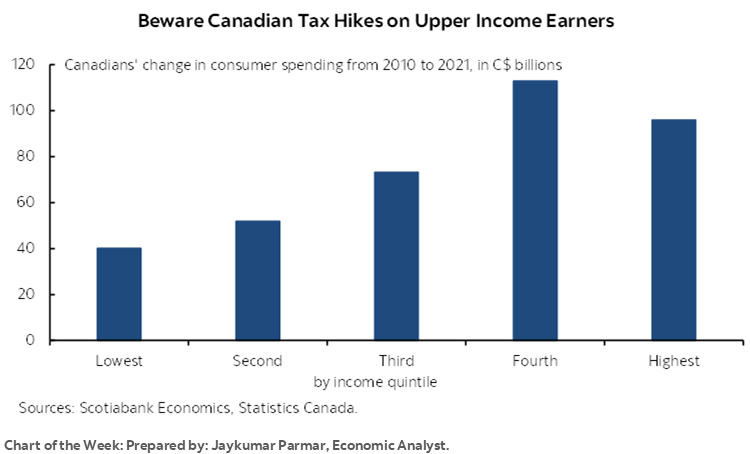

A risk is how much the Federal Government takes out of the system through tax hikes as the PM has only said that middle-income earners won’t face higher taxes. That’s probably not an unintended slip as opposed to a message to others to expect hikes. Nobody knows how they define middle income, but OECD estimates and past comments by Liberal politicians probably pegs it in a wide range from about C$50k to $140k in after-tax household income and likely toward the middle of that range.

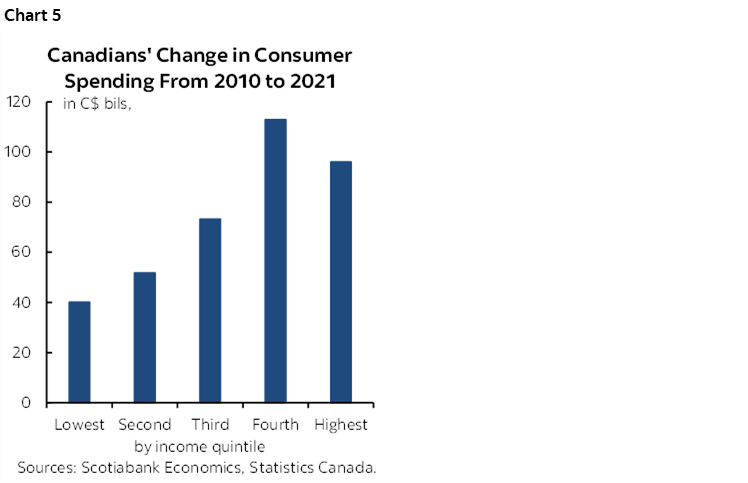

If in the quest for ‘fairness’—howsoever defined—the outcome is that upper income earners face material tax hikes, then it could dampen economic growth, given evidence that they have driven so much of the gain in consumer spending over time using the freshest available figures from Statcan (chart 5). And that’s without getting into the controversy over what is ‘rich’ especially in Canada’s most expensive cities.

Also bear in mind that fiscal policy will remain very much in play into next year’s Federal election.

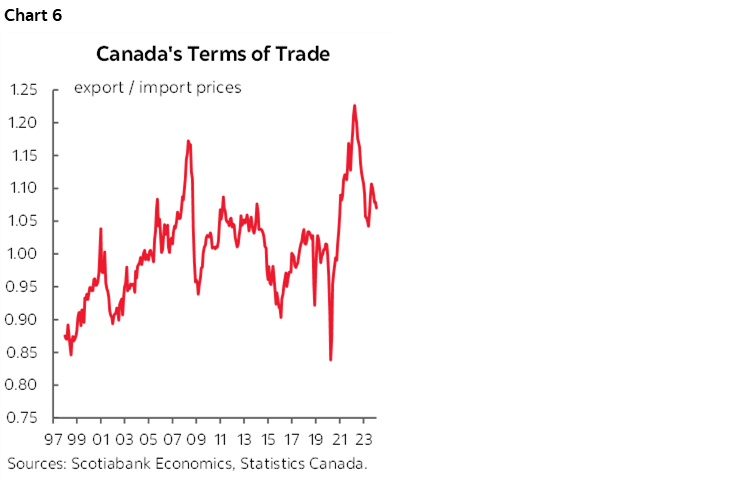

iv. The Terms of Trade

When the terms of trade—the ratio of export prices to import prices—has risen or held firm in the past it has, all else equal, been cause for the BoC to either turn less dovish or more hawkish.

Recall that this measure matters to a country like Canada that trades a lot and produces lots of commodities. When it rises or hangs out at elevated levels then it's like an imported positive income shock, selling our stuff at attractive prices relative to what we're paying for other junk we buy from abroad. The effects trickle down through improved fiscal balances (giving even more money to spend....), corporate balances and household financial conditions.

Well the terms of trade is holding firm but it's only up to February (chart 6). There are a lot of component prices, but much of the run-up in oil prices is not being captured yet. Western Canada Select started February at about $53/barrel and left March at about $70.

v. Other Considerations

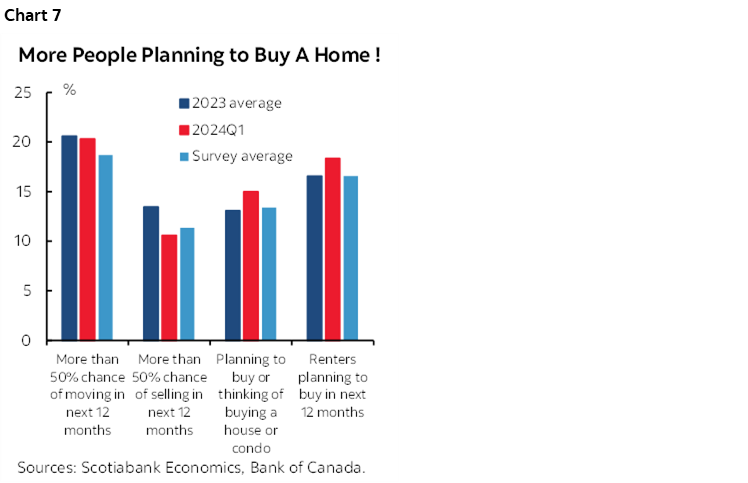

There are other considerations with a couple of them worth briefly mentioning before moving on. One is that Canada is about to enter the thick of the Spring housing market over April to June. The Easter Bunny robbed realtors of some sales in March that should be made up in April but the uncertainty lies around how powerful the season will turn out to be. Buying intentions remains very strong (chart 7). Housing shortages pre-existed the surge of immigration that has compounded them while strong trend job gains and firm wage pressures are supportive of housing demand. First time buyers are sitting on the sidelines having waited out a soft patch on prices. Targets for permanents residents remain high and so it will take many years yet to address housing shortfalls and pressures on affordability in a best case scenario.

That also depends upon what the Federal government has up its sleeve by way of potential further housing initiatives. PM Trudeau recently stated "On mortgages, we will have more to say between now and the budget date on April 16th, and perhaps we will save it for April 16." That fanned speculation toward what may be in the works. Anything that stimulates housing demand even further should be treated with great care as it could ultimately wind up fanning further pressures on affordability.

An added consideration is the Federal Reserve. Another 303k payroll positions created in March and firm wage pressure in the context of a resilient US economy doesn’t scream out in favour of cutting rates any time soon especially given the way the year has started with higher than expected core inflation.

INFLATION—US CPI TO DOMINATE

A series of inflation reports are due this week including some of the world’s biggest economies and throughout our clients’ markets within the Americas.

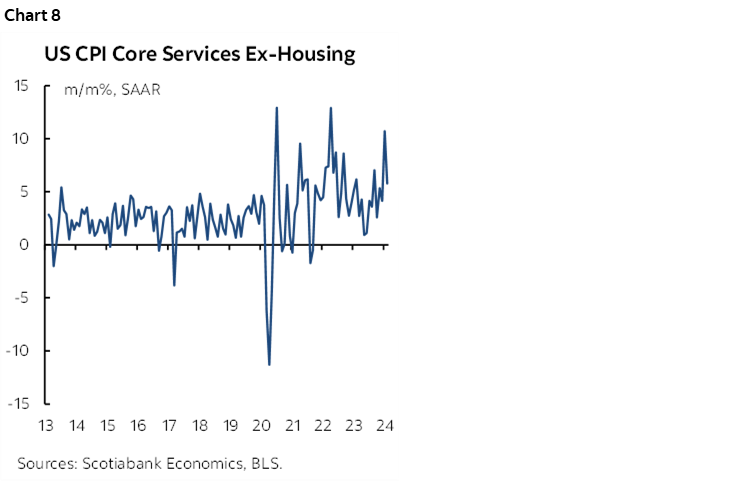

- US CPI (Wednesday): I’ve estimated a gain of 0.3% m/m SA for core CPI and 0.4% for headline inflation. The difference between the two measures is partly driven by the rise in gasoline prices last month. Industry guidance points to a decline in used vehicle prices that could subtract about 0.1 ppts off of headline CPI and slightly more off of core. New vehicle prices are expected to be relatively little changed. OER is expected to post another 0.4–0.5% m/m gain with rent of primary residence performing similarly. Key—and more difficult to estimate—will be core services inflation that has been a driver of the recent reacceleration (chart 8).

- China CPI (Wednesday): Year-ago base effects have shifted in favour of ending so-called deflation. March CPI will continue that trend and CPI is likely to continue to rise in y/y terms over the duration of the year. I maintain that China was never really in deflation in the first place using the economist’s typical definition of it versus the media’s treatment.

- LatAm: Chile reports on Monday and its year-over-year inflation rate is expected to push below 4% and possibly reverse the mild upward pressure in the prior reading. Mexico reports March CPI on Tuesday with the usual running head start provided by bi-weekly readings driving expectations for a slight gain to 4½% y/y. Brazil’s inflation rate is expected to pull back to 4% y/y and to continue its descent from a post-pandemic peak of 12.1% (Wednesday).

I’ll write more about other releases over the week. CBCT watchers will keep an eye on Taiwan’s March reading (Tuesday) amid potential disruptions in the next report after the worst earthquake in 25 years. Wednesday brings out Norway’s update. Both Sweden and India update on Friday.

OTHER CENTRAL BANKS—FOMC MINUTES AND THE ECB THE HEADLINERS

I wrote a fair bit about the Bank of Canada because I think it’s going to be the most interesting of the central banks to weigh in this week and because it’s close to home. There are, however, going to be several other central bank communications that could be impactful.

FOMC Minutes

Minutes to the March 19th–20th FOMC meeting arrive on Wednesday at 2pmET (recap here). Markets took the communications somewhat dovishly when they arguably should not have. The communications indicated a base case outlook for 75bps of cuts starting later this year without a compelling need to rush it and with a skewness in FOMC participants’ views toward less than 75 this year. The minutes will have a partially stale feel to them, however, since Q4 GDP was revised up afterward, core PCE inflation was revised higher to 0.5% m/m SA in January and printed at 0.3% in February, and nonfarm payrolls and wages came in strongly for February.

The key thing to watch, however, will be the promised fuller discussion about balance sheet management plans. Guidance pointed toward a decision “fairly soon” and further discussion. From my recollection, ‘soon’ leans toward the next meeting, so ‘fairly soon’ could sound like within the next couple of meetings and hence perhaps by the June FOMC. Watch for possible discussion about the ranges for the first taper, ranges for end target and ranges for timelines. Powell did say, however, that nothing was decided at the meeting which indicates that further discussion on the modalities will occur at the May/June meetings with an announcement.

ECB—In Play After This Week

Thursday’s outcome should be a placeholder before the more critical meeting on June 6th. Tuesday’s bank lending survey may inform one part of how the ECB is thinking about broad conditions in this case financial conditions and monetary policy transmission effects. There will be no forecasts offered with this meeting as they were updated the last time in March.

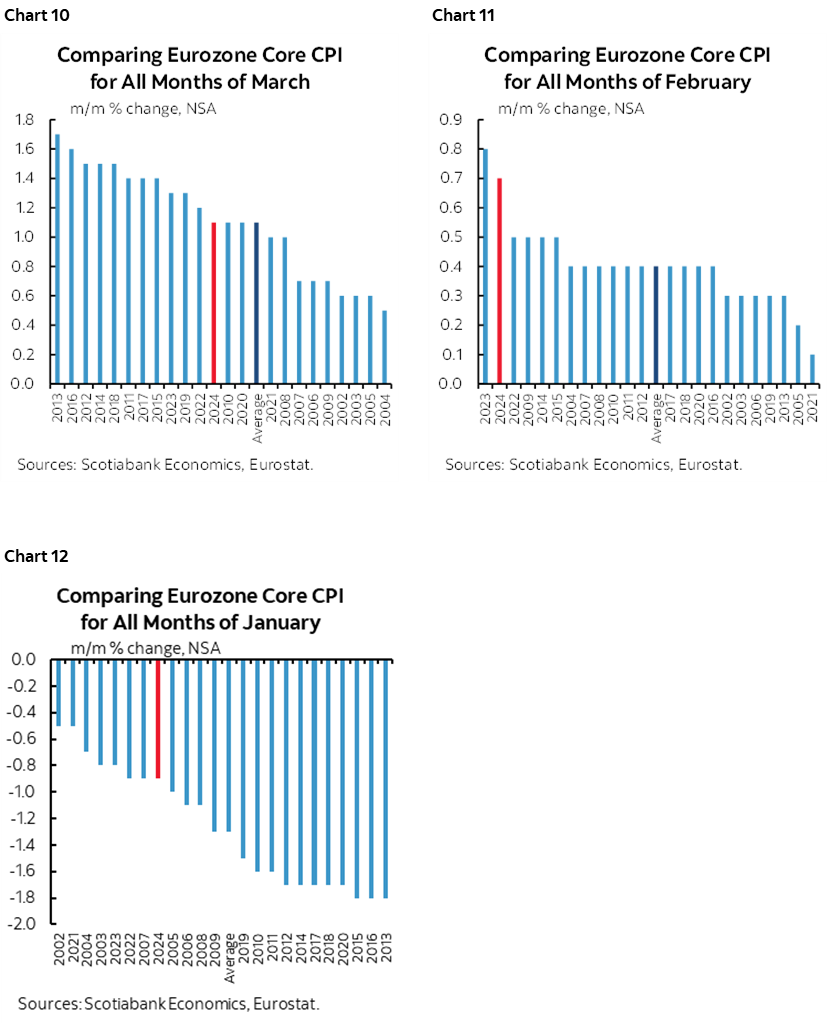

In my opinion, the full pricing for a quarter point rate cut in June may well be the end outcome but I’m surprised that there isn’t so much as a few basis points of uncertainty being factored in. Oil prices are soaring and if this persists then it will probably flow through as a renewed source of upside risk to inflation over the duration of 2024 into 2025. The ECB has also been clear that they wish to see the results of the critical start to collective bargaining exercises when Q1 wage data arrives into the June meeting to further inform the trajectory for wages (chart 9). Furthermore, core Eurozone inflation hasn’t exactly been light on a trend basis (charts 10–12).

In short, I personally just don’t see the need for the ECB to be in a rush to begin cutting rates. The path toward about 100bps of rate cuts into year-end looks aggressive to me.

Others

A half dozen other central banks will deliver policy decisions over the coming week. I’ll write more about them over the week and just offer highlights as time runs out this week.

- Bangko Sentral ng Pilipinas is expected to leave its policy rate unchanged at 6.5% on Monday.

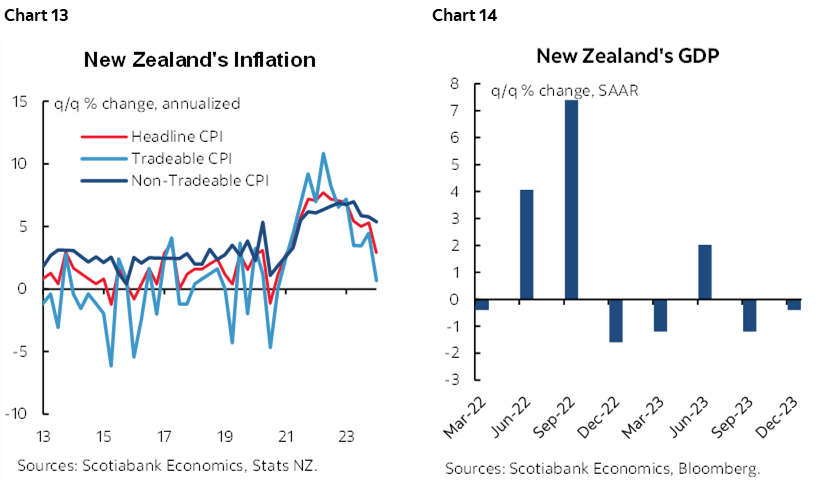

- The RBNZ is forecast to hold its cash rate at 5.5% on Tuesday evening ET but toe signal further patience over coming meetings. The economy slipped into recession by the end of last year and inflation is sharply declining (charts 13, 14).

- The Bank of Thailand is expected to hold at 2.5% on Wednesday.

- Peru’s central bank is expected to hold on Thursday.

- The Bank of Korea is also expected to hold on Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.