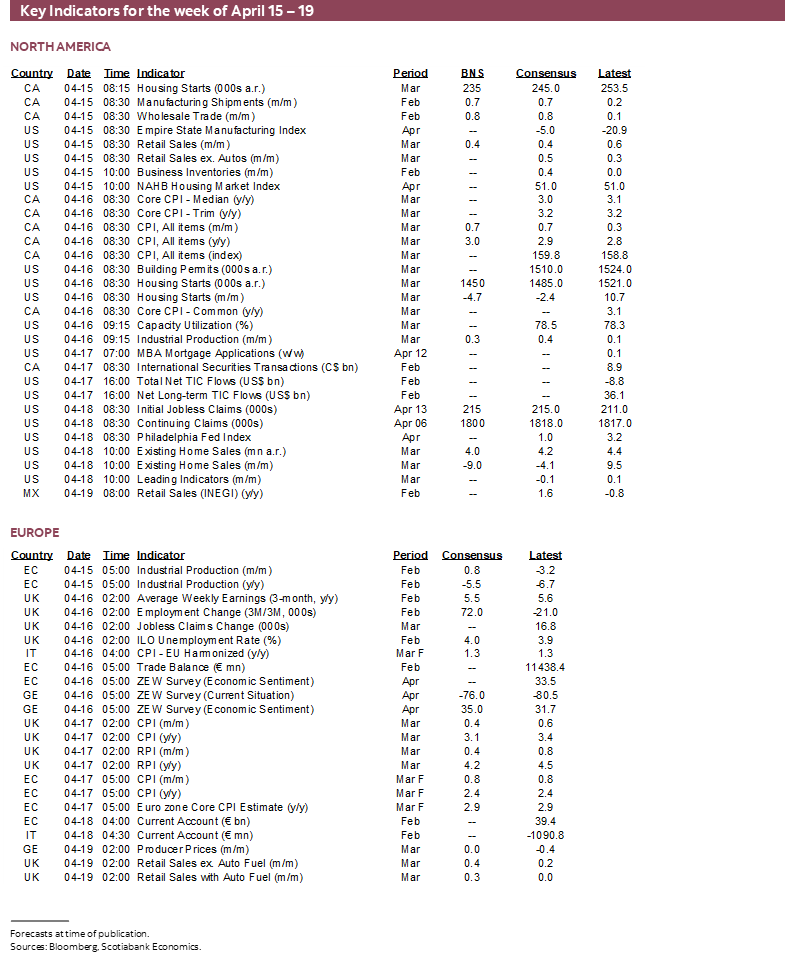

Next Week's Risk Dashboard

- Energy markets on alert

- IMF/World Bank meetings to showcase key central bankers

- Will Canadian CPI rebound?

- The BoC’s absurdly low bar

- Canada’s homebuilding target is wildly optimistic

- Canada’s Budget to crank up the spending—and taxes

- US earnings season intensifies

- China’s economy may accelerate

- PBOC like to stay on hold

- Are US consumers still spending?

- UK CPI, jobs and wages will be key to the BoE

- Australian jobs face a tough act to follow

- NZ CPI to inform RBNZ risks

- Japanese inflation to reaffirm Tokyo gauge

Chart of the Week

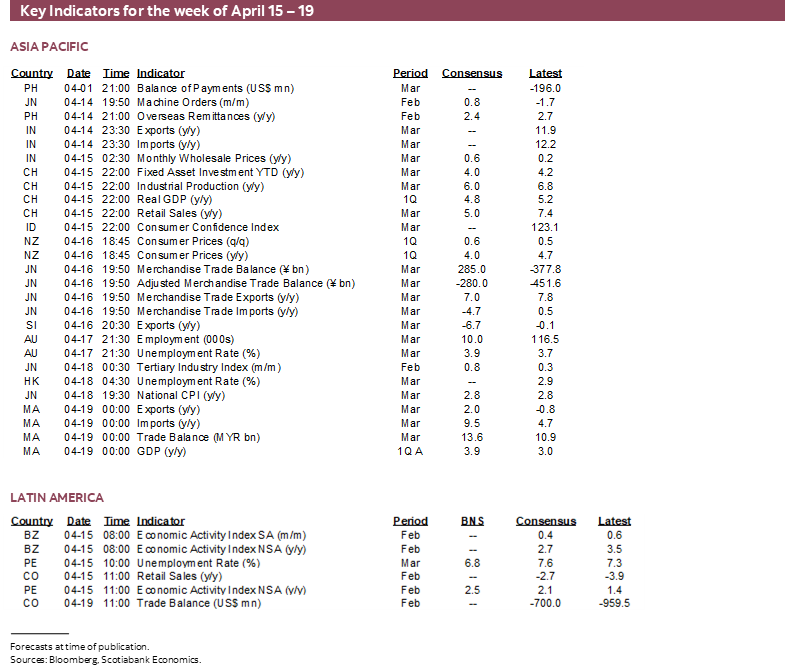

A jam-packed week of developments lies ahead that is sure to drive heightened volatility. Oil, broader financial markets, and general harmony are all at risk should threatened imminent strikes against Israel by Iran in retaliation for Israel’s attack on Iran’s consulate in Damascus drive further escalation. Several key central bankers such as Powell, Bailey and Macklem will speak from the annual Spring meetings of the IMF and World Bank in Washington. US earnings risk will intensify. The PBOC will weigh in with an updated decision. Top shelf data will focus upon China’s economy, US consumers, Australian jobs, UK jobs and wages, and CPI reports out of Japan, the UK and New Zealand that may inform central bank expectations.

Canada will face particularly intense risk when a hat trick of concentrated developments arrives on Tuesday. It starts with CPI that will help to further inform whether the country has merely experienced a two-month soft patch or started something more durable. Governor Macklem weighs in with Chair Powell a few hours later. Then Canada’s Budget lands with a dull thud after the market close. Out of all of that, CPI and oil are likely to pose the greatest Canadian market risks.

CANADIAN CPI—THE CRAZINESS OF IT ALL

Canada updates CPI inflation figures for the month of March on Tuesday morning to kickstart a jam-packed day for Canada-watchers. Given recent BoC communications (recapped here), there is scope for a potentially violent reaction in nearer-term policy rate pricing whichever way things go.

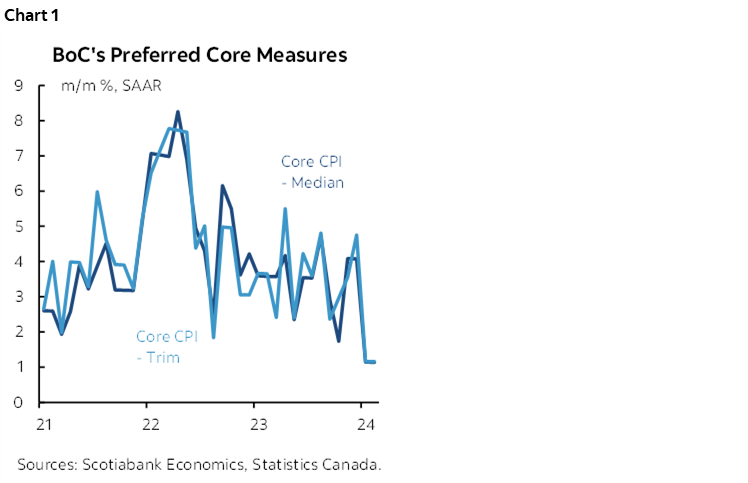

A rebound in the core gauges (chart 1) would derail possibly premature optimism around the prior two-month soft patch. Alternatively, another soft set of core gauges could fan easing bets. I would still set a higher bar for easing than 2–3 months of data and would want to assess many other considerations regardless of Tuesday’s outcome.

For headline CPI, I went with 0.7% m/m NSA and 3% y/y. I lean toward a solid risk of a rebound in the trimmed mean and weighted median measures. I’ll explain why, but with moderate conviction. Estimating these gauges is nearly impossible to do in the way that counts which is m/m SA. The 55 CPI components that go into their calculations are mostly unknown and difficult to track in advance. Knowing which readings to lop off in the upper and lower 20% of the weighted distribution of price effects is even more futile. Ditto for knowing which exact price might be at the 50th weighted percentile for the weighted median CPI gauge.

With that cover-your-tender-bits caveat, what gives? Why is there the solid risk of a rebound in the core gauges? My take on the last reading (here) alluded to some of the reasoning along with the following points that go well beyond just observing that the BoC is far too dismissive toward the possibility that what happens in Vegas doesn’t necessarily stay in Vegas (chart 2).

In short, what drove a fair portion of the sudden soft patch over January and February had much less to do with the lagging effects of rate hikes and much more to do with a highly unusual panoply of distorting effects reflecting inventory management, weather, and bullying by the Federal government.

Clothing Prices Poised to Rebound?

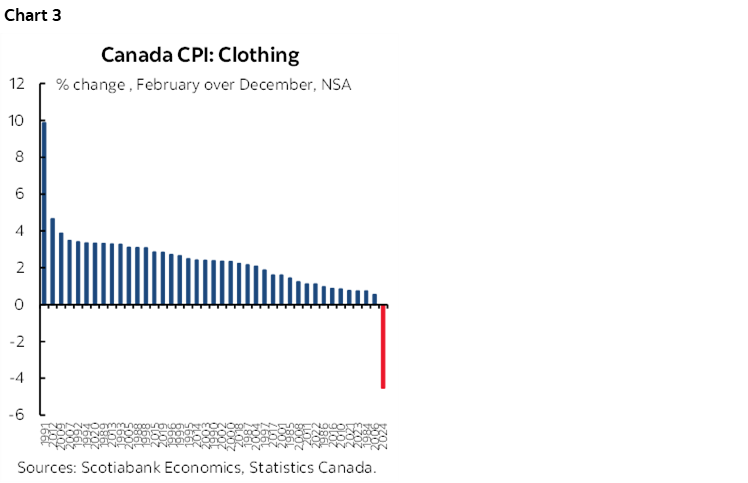

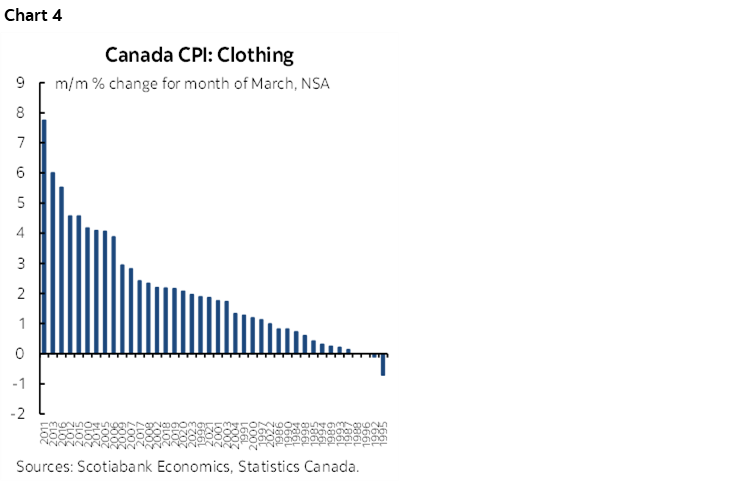

Pay attention to clothing prices since they contributed to some of the drag this year including the 2.7% m/m SA drop in February. The decline in clothing prices over January and February was a massive outlier. 2024 is the only year on record when clothing prices fell from December to February inclusive (chart 3). It wasn’t a small decline either. Clothing prices fell by a cumulative -4½% NSA over this period.

They may be poised for a rebound from such unusual softness that I still think was significantly driven by inventory excesses of seasonal lines that prompted added discounting due to a warmer and drier than usual Winter because of El Nino that was relatively strong this year.

On top of such an unusual jumping off point, clothing prices normally rise in March (chart 4). New Spring lines start to get introduced across a variety of categories such as clothing, outdoor seasonal goods etc. When that happens, prices usually jump.

A combination of the two points on clothing prices could drive a sharp rebound. If it doesn’t happen this month, then I think the case would be pushed forward.

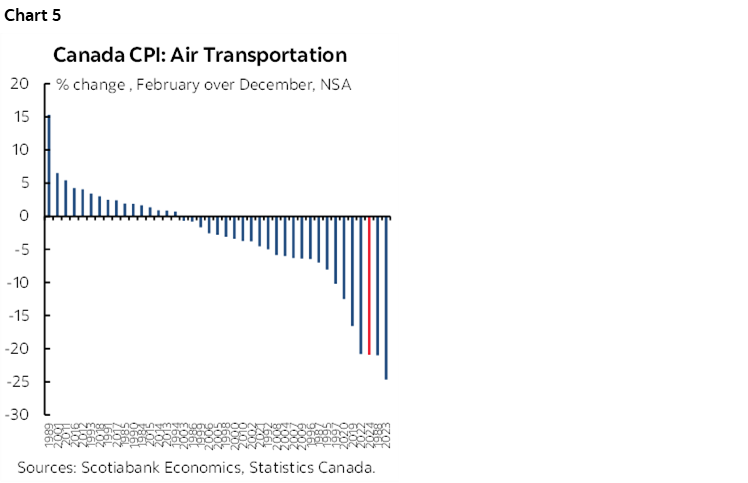

Ditto for Airfare

A similar argument applies to airfare. This year was among the weakest periods on record (chart 5). Five of the seven weakest periods on record have been in the pandemic era. On top of this unusual softness is the added fact that airfare in CPI usually pops higher in March over April.

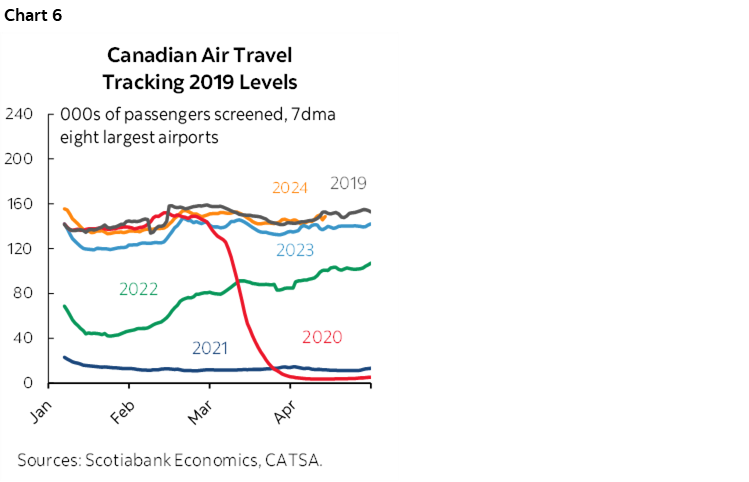

What could add to this argument is that there were more people flying through March including at the start of the pandemic than there were before the pandemic (chart 6). CPI samples prices in the first two weeks of the month (first three for food). Therefore, CPI should capture peak March break travel activity that was more elevated than usual.

It’s also possible that Statcan is still having difficulty with seasonal adjustments in categories subject to unusually large variations.

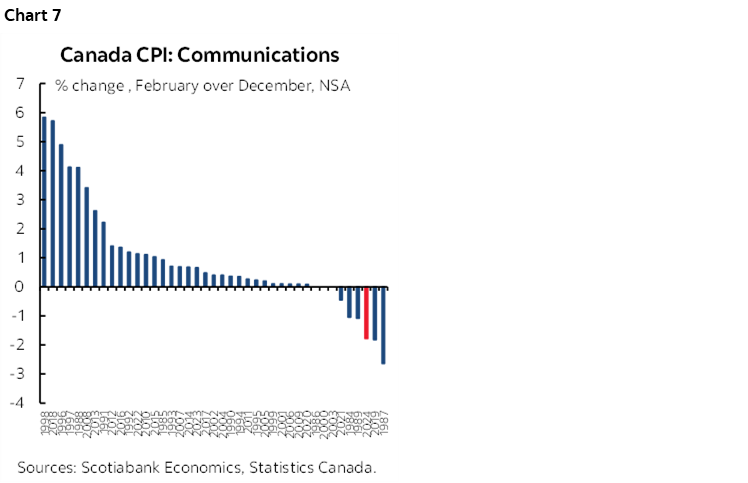

Why Communications Prices Were Cut

Here’s yet another extension of the same principle. Historically unusual softness in communications prices may be poised for a rebound. The December to February period this year saw one of the largest declines in communications prices on record when it’s more commonly a period marked by higher prices (chart 7). In this case, however, March has been more mixed on communications prices than the other categories which on its own may lessen confidence in a rebound.

Still, the pace of price declines in February is not sustainable. A continuation of the -9.4% m/m and 13.5% y/y pace of decline in prices for internet access services in February and the 26.5% y/y decline in cell phone plans within CPI would make them free inside of a year!

What’s driving it? Political pressure. The ‘big three’ telecom CEOs were all summoned to Ottawa in March. They are under political pressure to lower prices and expand features.

There is a limit to political pressure especially as telecoms are under political pressure to increase access at much higher cost to them and taxpayers. That limit may soon be reached as heat reaches a crescendo with the coming Federal Budget.

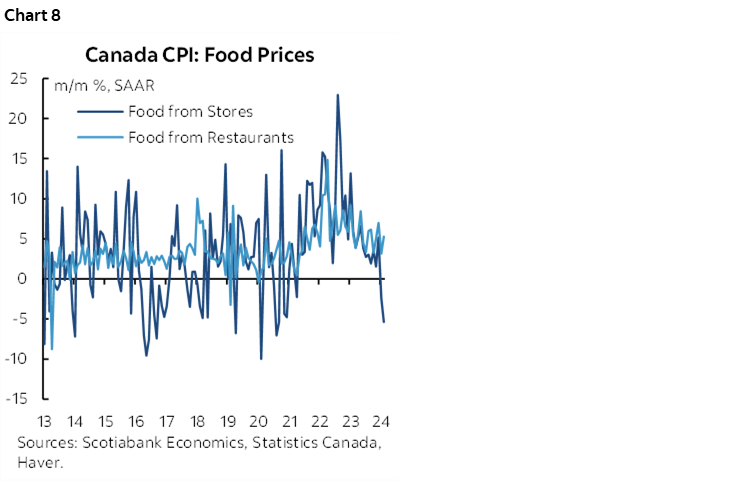

Grocery Prices—Bullying Paid Off

Here’s another one. CEOs of grocery chains cut prices just ahead of being hauled off to Ottawa to testify before Committees in a game of political theatre. Ottawa’s bullying of private industry contributed to a large decline in grocery store prices (chart 8). But what about after the Budget passes and shareholders question management?

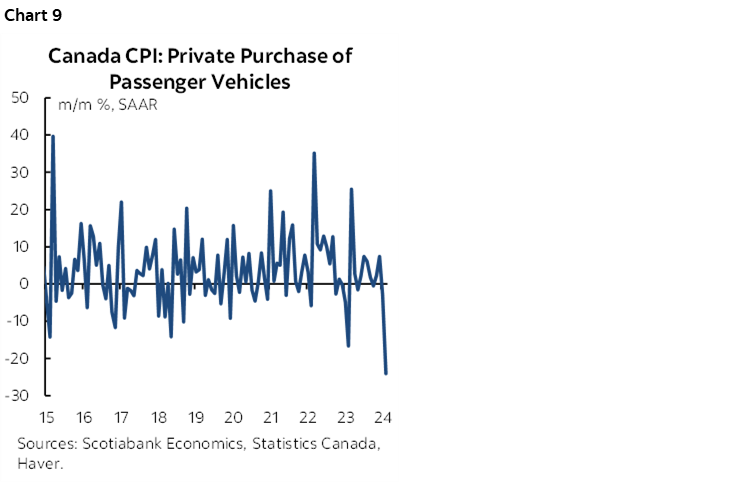

Vehicle Prices—Temporary or Lost Love for Used?

Adding to how unusual the price moves have recently been is the fact that vehicle prices posted an usually large decline in February (chart 9). Used vehicles drove most of that with a drop of 2% m/m NSA.

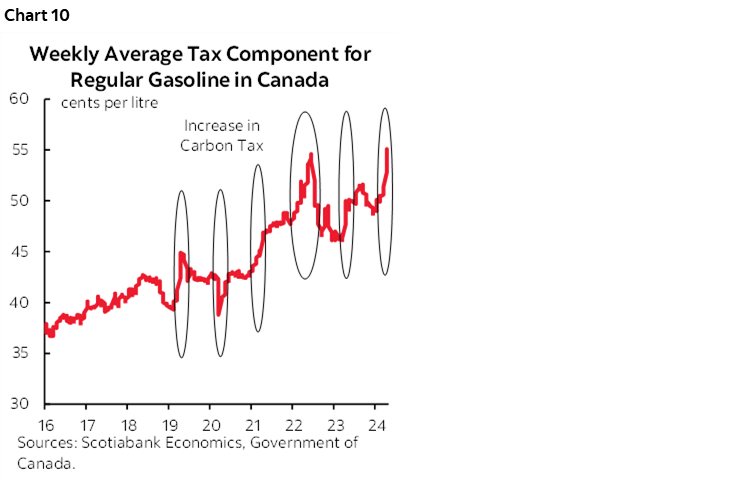

April Teaser—Carbon Taxes to Figure Prominently

This won’t be a factor in March’s reading on Tuesday, but I’m figuring that the increased carbon taxes during April will easily add 0.2–0.4 percentage points m/m to April CPI including direct and indirect effects. This is beyond whatever we’ll be tracking by then.

The direct effect is partially captured by its impact upon gasoline taxes that jumped 5 cents/liter in April over March (chart 10). That accounted for about one-third of the rise in gasoline prices so far in April versus the beginning of March.

Do carbon taxes matter to monetary policy? Yes and no. The BoC would probably instinctively remove as much of the direct and indirect effects from the inflation data as possible. That might be tricky to do with high accuracy.

Further, your average person isn’t sitting there wondering why the cost of living is going up. They just see it rising and at risk is more extrapolative behaviour in terms of inflation expectations and hence behavioural shifts behind contract demands.

The Craziness of it All

It’s absolutely crazy that it has come down to this level of data sensitivity at the BoC. Most of what they said in their communications and forecasts made it sound like they were in no rush to cut. Governor Macklem’s casual ‘yes’ response to whether June was a live meeting was an exception, along with very aggressive forecast changes they made to the supply side. He is being too reactive to very short-term data.

We’re only two months removed from when the two measures of core inflation were both running over 4% m/m SAAR (chart 1 again). The very recent soft patch may be an anomaly and not the first soft patch.

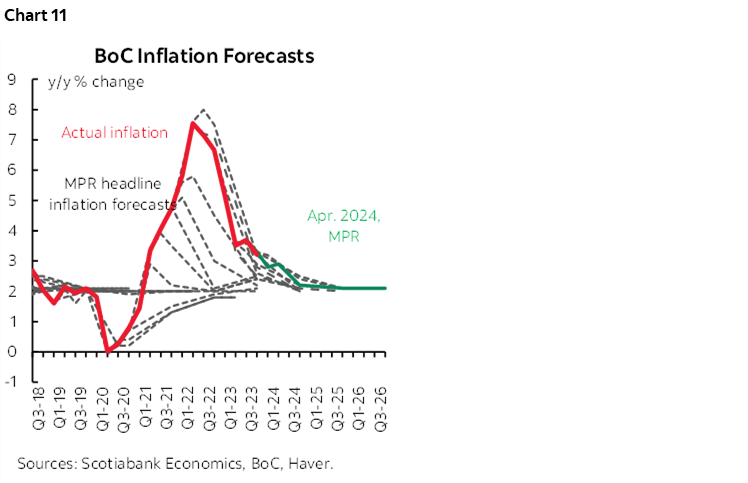

Given that the BoC has an awful track record at forecasting inflation, one would expect them to require vastly more evidence of softer inflation before pulling out the pom poms (chart 11). They always forecast a magical return to their 2% inflation target and usually miss the turns by overshooting and undershooting the path.

CENTRAL BANKS—THE HERD GOES TO WASHINGTON

Only one central bank will deliver a decision this week, but plenty of other central bankers will be gabbing away particularly as they gather in Washington.

IMF-World Bank Meetings

Key may be the annual Spring IMF-World Bank meetings in Washington. They will bring together a number of central bankers and finance ministers among other officials. There will be opportunities to speak publicly.

Federal Reserve Chair Powell appears alongside BoC Governor Macklem on Tuesday in Washington. Key will be whether Powell repeats that nothing much has changed after yet another upside surprise to core inflation. Key for Macklem will be if he wishes to revisit his casual remark on the probability of a cut in June. Many other Fed-speakers will share their views throughout the week and will be particularly watched for comments in the wake of the hot CPI reading (recap here).

Bank of England Governor Bailey speaks at the meetings on Wednesday after delivering an interview at the meetings the day before. Other BoE officials will also attend and speak. Some ECB officials are scheduled to appear in Washington and at the Economic Club of New York.

When these large international gatherings occur there can be a coordinated tone shift across the central banks.

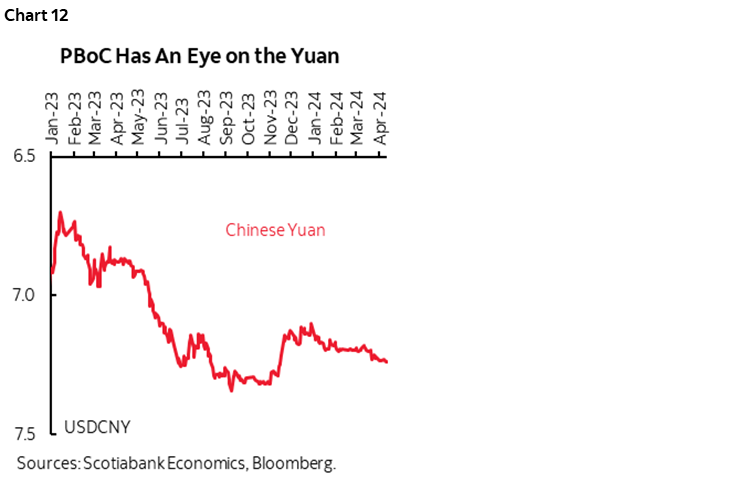

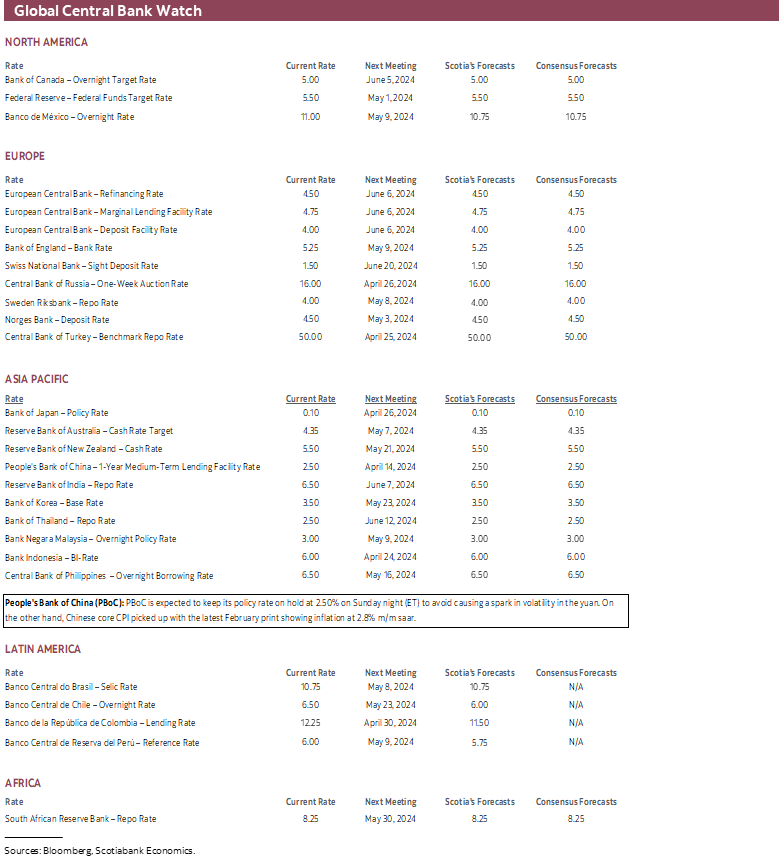

PBOC—Patiently Watching the Fed

China’s central bank delivers its latest decision on the 1-year Medium-Term Lending Facility Rate on Monday (Sunday ET). No one expects a change to the present 2.5% rate.

Key is managing currency risk. The yuan has mildly depreciated this year but is about 15% weaker to the USD since early 2022 (chart 12). To cut when the outlook for easing by the Federal Reserve keeps getting pushed out could unmoor the currency. That could unmoor the currency and be a risk to financial stability.

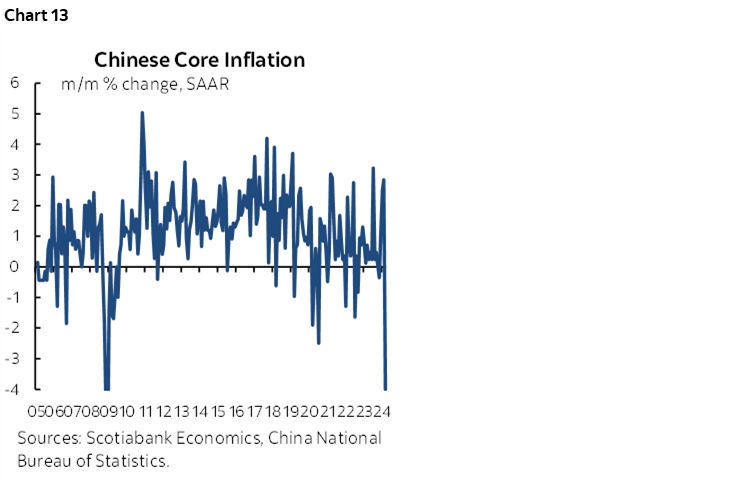

I don’t think the PBOC should overreact to recent inflation figures either. The last time China’s core inflation reading was this weak was back in the GFC (chart 13). Core inflation fell -0.6% m/m NSA, or -4% m/m SAAR and ebbed to 0.6% y/y from 1.2% the prior month.

Part of the explanation for the weakness has to do with the shifting timing of the Lunar New Year that was on February 10th this year. That was later than average, and it sometimes falls in January, which means that the period of peak holiday spending was well into February. That could explain why February’s core prices were up by 2.8% m/m SAAR and so March retreated from that holiday-driven gain.

The details support this view as the weakening was pronounced in categories like recreation and education (1.8% y/y from 3.9% prior) and transport/communications (-1.3% y/y, -0.4% prior). But the magnitude of the retreat also plays to the narrative that disinflationary forces remain prevalent due to excess capacity, just not as acutely as the headline readings suggest.

Should we call it deflation? Not by the standard definition most economists would apply that says deflation occurs when an economy-wide decline in general prices occurs for a lengthy period and is expected to persist while driving changed behaviour that, through postponing purchases into a cheaper environment, drives more downward pressure on prices. That can be a very difficult scenario to turn around and it’s highly premature to be calling what China is experiencing true deflation. More data is required to help inform developments.

CANADA’S FEDERAL BUDGET—SPEND, SPEND, SPEND, TAX, REPEAT

Thank heavens it’s almost over! Canada has a cottage industry of folks employed in the business of developing, forecasting, assessing, and evaluating government budgets. It’s quite unlike many other parts of the world particularly given how seasonal the trade is with activity usually lighting up when the first major province releases a Budget—often British Columbia in February—and culminates in budgets from the Federal Government and the biggest provinces. The season is almost at an end, for now.

Canada’s Federal government releases its annual budget on Tuesday. Much of what it will contain has already been spilled. Long gone is the era when Budgets would be all new on Budget day and followed by business leaders attending evening and morning-after presentations and meetings by economists as well as accounting and consulting firms. For years now, governments have used Budgets as rolling p/r stunts. Imagine a company that releases its financials in bits and pieces over weeks in advance as routine habit.

It’s no secret that it will be a big spending budget that will probably hit relatively upper income earners and corporations with higher taxes while never targeting a balanced budget. Key in terms of whether the latter matters or not is whether the assumption of a beautiful economy for years to come through decade’s end comes to fruition given the rise of structural deficits that could be substantially magnified by a wider primary deficit in a weaker scenario. Ottawa is sending it out faster than it comes in on the assumption that the skies stay sunny forever; this assumption through the 1970s and 1980s ultimately led to a crisis.

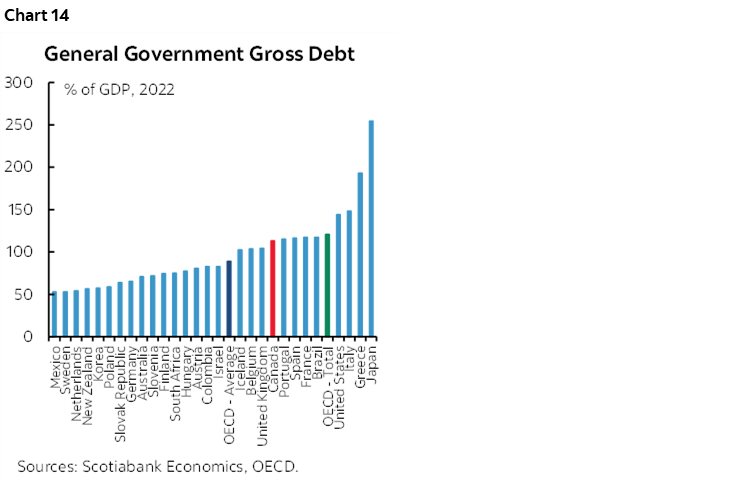

Canadian governments are not lightweights when it comes to debt (chart 14). Many cite net debt to GDP ratios that are healthier but do so on the implied assumption that the financial assets in sinking funds, sovereign wealth funds, pensions etc are accessible.

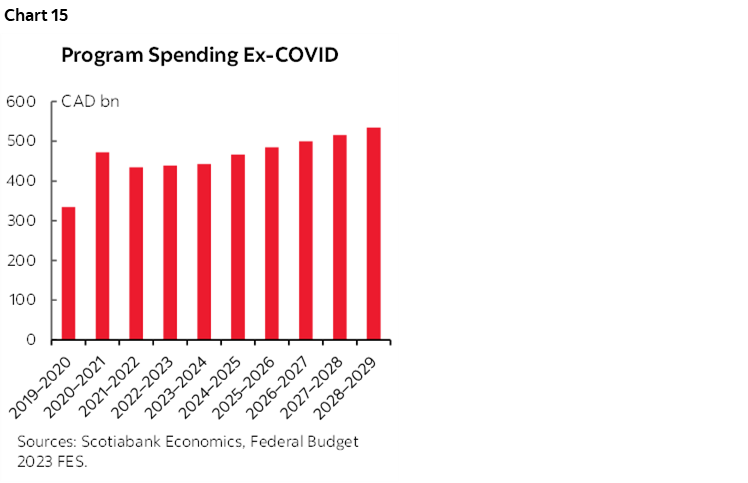

But for now, the manageable deficits are one thing. The impact on the economy from heavy spending is another. As chart 15 shows, the Federal Government’s program spending has skyrocketed by about one-third compared to the fiscal year just before the pandemic and is slated to be 60% bigger than pre-pandemic levels by FY 2028–29. If not for such spending by the Feds and provinces, the Bank of Canada would not have had to hike its policy rate by as much as it has and might have already been in a position to begin easing.

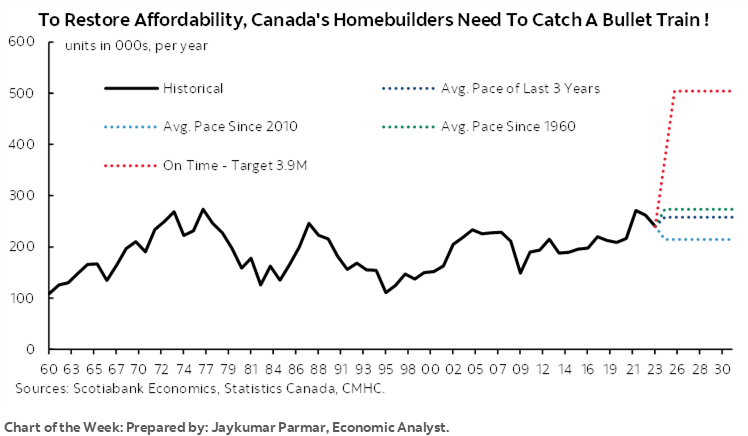

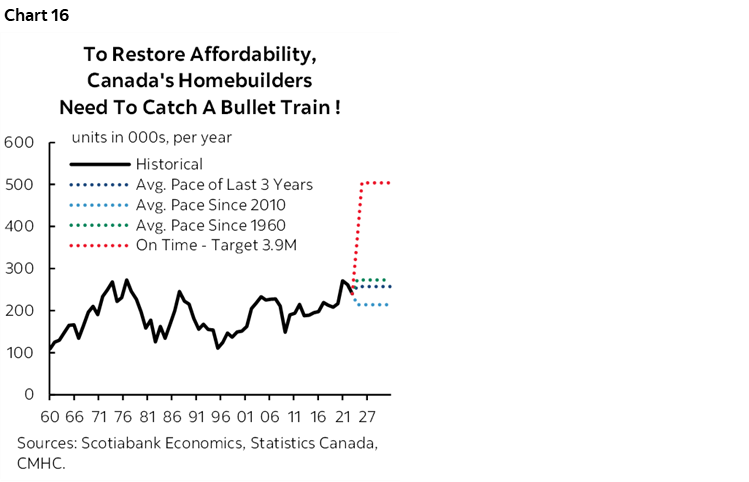

Expect a strong focus upon housing. The government created a problem with severe housing shortages through serial application of demand-side stimulus and wildly excessive immigration and is now trying to fix that with sundry incentives to build more housing. Its target of 3.9 million additional homes to be built by 2031 is laughable. As Jay Parmar’s chart of the week shows on the front cover and repeated in chart 16 demonstrates, Canada would have to sustainably ramp up annual housing starts to much more than double what has ever been achieved in any prior year and despite labour shortages. The housing plan they have announced has some constructive elements, such as training for the skilled trades, but its targets are a pure and simple photo-op. The targets also assume there will be demand for the type of housing they are trying to encourage—cheap units on public lands, factory-built homes, and homes like the ones built in mass fashion for returning soldiers after WWII that have since driven a booming business in tear downs and rebuilds.

Alongside such fanciful supply-side ambitions are curious efforts to further stimulate demand despite already widespread housing shortages. I wrote about the plans to ease mortgage financing here.

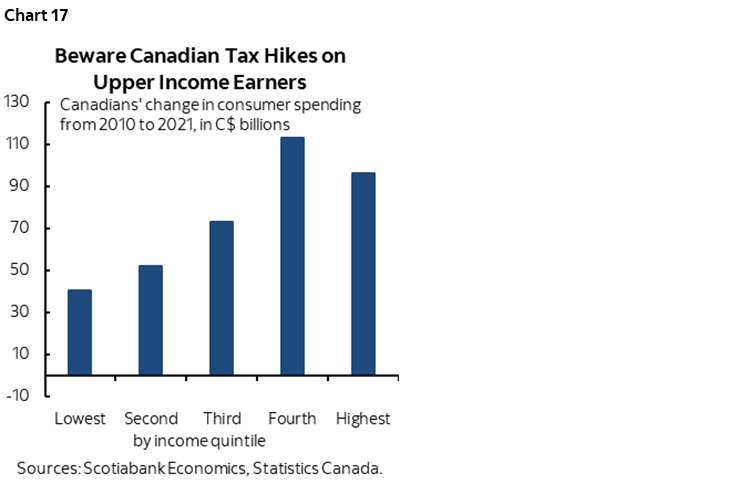

As for taxes? That depends upon how you define the middle class and how you adjust this definition for different types of families, different regions, and varying individual circumstances. We’re told the middle class will be left unscathed but are unclear about how the Feds will define this. At risk is hiking taxes on the folks who drive much of the growth (chart 17) and further vilification of successful industries and, by the government’s definition, anyone outside of the middle class doesn’t work hard...

We will be assessing the implications of the Budget for the Bank of Canada in light of its recent communications (recap here) and the fact it has yet to incorporate anything on the Budget in its forecasts. How ratings agencies respond may be a risk.

Finally, it would be extraordinarily naïve to assume that whatever is announced on Tuesday will be the end of the government’s plans. Canada faces an election by no later than October 2025. Governments that are doing as badly in the polls as the Trudeau-Singh-Freeland administration is performing don’t typically turn fiscally prudent. Bear that in mind in terms of the prospect for further fiscal easing that complicates the outlook for the BoC and that entails drawing implications for debt management and issuance plans beyond what is laid out this week.

For more, see Rebekah’s preview here.

US EARNINGS SEASON ESCALATES

US earnings season continues this week with 41 companies listed on the S&P500 ready to report.

Financials will continue to figure prominently after this past week’s opening salvos. Goldman Sachs kicks it off on Monday, followed by names like Morgan Stanley, BofA and others on Tuesday. Netflix reports Thursday. Chart 18 shows expectations for the overall season.

GLOBAL MACRO—TOP SHELF RELEASES

Several key global indicators are due for updates this week with enough breadth across countries to inform overall global momentum.

China’s Economy in Focus

The state of China’s economy will be a major focal point when Q1 GDP is released on Monday along with end-of-quarter readings on industrial output, retail sales and job markets that will inform momentum effects into Q2. The economy is forecast to grow by about 6% q/q SAAR that, if achieved, would be an acceleration back to 2023Q3 rates after a softer patch to end the year.

US Consumers Still Spending?

US retail sales will dominate the domestic calendar. They land on Monday. A dip in auto sales last month could weigh on the headline number with a mild gain in sales ex-autos and gas expected. Housing starts (Tuesday) could give back some of the prior month’s 11% m/m SA rises while existing home sales for March (Thursday) are also expected to soften from the 10% m/m SA prior gain and trend softness in pending home sales. Industrial production is expected to post a small gain (Tuesday).

UK CPI and Jobs Will be Key to the BoE

The UK is forecast to continue further progress toward lower inflation when March’s estimates are released on Wednesday. Core CPI is nevertheless still expected to stick above 4% y/y. Markets are presently pricing a BoE cut by the August 1st meeting and a decent chance at one by the June meeting.

The UK will also update the state of its labour markets this week. Tuesday will bring out total employment during February and payroll employment for March plus what could be the first sub-6% y/y rate of increase in wages ex-bonuses since September 2022.

Australian Jobs—A Tough Act to Follow

Australia’s jobs report for March faces a tough act to follow in the February reading when 117k more jobs were created including 78k full-time positions. That was the biggest gain since November 2021. It wouldn’t be surprising to see a pullback, but it would be surprising to markets to see another notable gain.

Canada—Little Else Left in the Tank

Canada should report a generally upbeat round of figures this week. Manufacturing sales have already been guided to post a 0.7% m/m SA rise in February so Monday’s report will include revisions and details like volumes. Wholesale trade figures are due on the same day and they were previously guided to have registered a rise of 0.8% m/m SA. Monday’s housing starts for March may give back some of the prior month’s 14% m/m SA rise unless milder and drier weather provides a boost that offsets a softening trend in building permits.

Peru’s Rebounding Economy

LatAm markets face two main economic indicators. Peru will update its monthly economic activity index reading for GDP growth in February on Monday and it is expected to post year-over-year growth above 2% for the first time since late 2022. Mexican retail sales in February (Friday) are forecast to slightly rebound from a declining three-month trend.

Kiwi, Japanese CPI

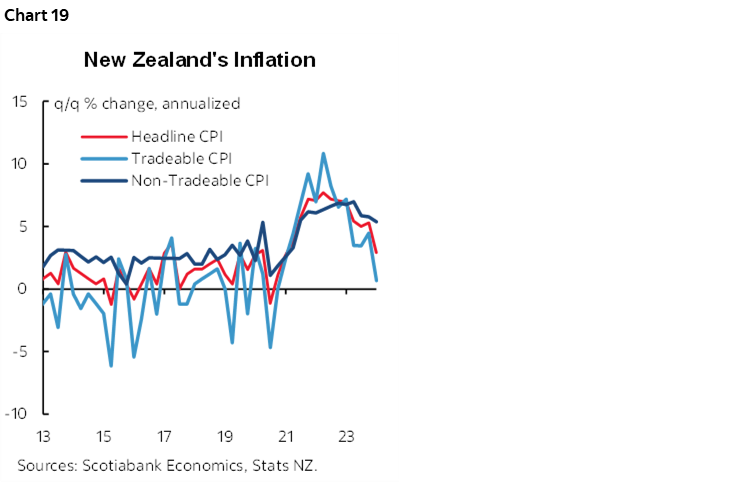

Kiwi inflation during Q1 (Tuesday) is forecast to continue to decelerate in year-over-year terms but the break down between tradeable and nontradeable components and details will also matter to the RBNZ that is not priced to begin easing until at least the August or October meetings (chart 19).

Japanese CPI inflation during March (Thursday) is expected to follow the earlier Tokyo gauge with a mild deceleration in the year-over-year core readings.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.