- Q3 growth is probably tracking beneath BoC expectations…

- ...but not by as much as monthly estimates suggest…

- ...which leans toward Q3 gap closure more than Q2…

- ...unless growth is punted forward

- Still, the case for hikes does not only hang on output gaps

- Markets paid more attention to soaring US labour costs…

- ...and continue to challenge BoC forward guidance

- It would take Macklem explicitly ruling out an early hike…

- Market trick or market treat? Macklem to speak on Halloween!

CDN GDP, m/m % SA, August:

Actual: 0.4

Scotia: 0.7

Consensus: 0.7

Prior: -0.1

September ‘flash’: ‘unchanged’

Canada’s economy somewhat disappointed expectations for August, although the preliminary guidance for September wasn’t terribly surprising. At the margin, this suggests that the BoC’s ’21Q3 GDP forecast is probably tracking too high, but there are important caveats around this statement.

Markets emphatically said ‘so what’ and are pricing a 25bps hike in January and much of another in April against the BoC’s forward guidance which is facing its most serious credibility challenge in many years. The strong acceleration in US employment costs toward the fastest since in at least a quarter century since data began signals escalating wage pressures and dominated market action as it raised the bond market’s concern that wages are reinforcing the next leg of inflationary pressures (chart 1). It also fed the narrative that the Fed and the BoC are improperly ignoring wage pressures across N.A. supply chains but next Friday’s jobs reports will further inform this issue.

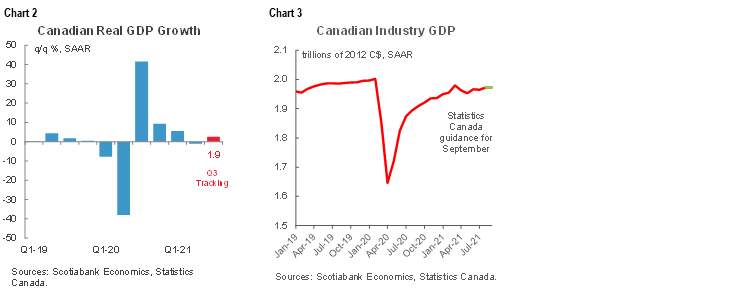

Q3 GDP TRACKING

Q3 GDP growth is tracking just 1.9% q/q at a seasonally adjusted and annualized rate using the production/income side monthly accounts including September’s guidance. See charts 2 and 3.

What does that mean for the BoC’s growth tracking? Recall that just two days ago the BoC forecast that Q3 GDP growth was expected to be 5.5%, but that was based upon different measures for GDP growth that are drawn from expenditure concepts. The difference between the expenditure accounts and income-based estimates can often boil down to the issue of how economic output changed in relation to inventory and import swings. What the BoC had factored into its expenditure-based GDP growth forecast of 5.5% was a strong weighted contribution from exports on the order of ~5 percentage points to Q3 GDP growth. They had also assumed a net drag from combined inventories, higher imports (as a leakage from the GDP accounts) and government spending of less than the positive contribution from gross exports.

Where does that leave the risks to the BoC’s growth tracking for Q3? That’s uncertain but it’s likely higher than 1.9% and lower than 5.5% with something in a 3-handled range being feasible and with further data ahead. That could also put it a little lower than our recent 4% growth forecast for Q3. The BoC could also once again emphasize that the composition of growth matters if growth in final domestic demand excluding autos and one-off shocks to agriculture and forestry holds firm.

TIMING CLOSURE OF THE OUTPUT GAP AND RATE HIKES

What does that mean to the BoC’s forecast closure of the output gap? It had said that spare capacity would close sometime over Q2–Q3 and today’s numbers would lean toward Q3 or possibly even later absent any other considerations.

It’s possible, however, that the BoC just punts more growth forward into Q4/Q1 and winds up with roughly the same guidance. Maybe they’ll keep fiddling with unobservable potential growth estimates that they currently have pegged at 1.6% on average over 2021–23. I don’t like that approach, but one can’t discount the argument that prices are more revealing of capacity constraints and markets might see things that models cannot.

In any event, if the BoC’s forward guidance to stay on hold until spare capacity is shut is strongly adhered to, then at the margin this report taken in isolation of other potential considerations would lean more toward a July or maybe September hike. Our current print forecast remains for a July hike.

MARKETS VERSUS THE BOC

However, there are additional complications. First, the BoC is blowing the bands on its flexible 1–3% inflation targeting framework and since they are mandated to guard against inflation there are limits to ignoring a powerful overshoot. The BoC also doesn’t have a monopoly on thinking toward the drivers of inflation. For one thing, it could be that more of the inflation this time is driven by imported drivers that would make a rigid interpretation of domestic slack’s influence upon inflation improper.

Domestic output gaps are one set of potential inflation drivers, but they are also highly uncertain not least of which because who knows what has really happened to the economy’s noninflationary speed limit to growth. There are plenty of other drivers of inflation as we’ve seen through the march toward 5% y/y even with spare capacity in place.

Fundamentally, I disagree with the notion that tighter monetary policy would be inappropriate in addressing imported and domestic supply chain effects since we probably have those supply chain problems in no small part due to overstimulating the demand side through excessive monetary and fiscal policy!

In any event, markets are still fully priced for a 25bps hike in January and another 25bps hike in April. If the BoC strongly disagrees, then it has to do so with a pointed commitment to not hike until at least April, not just vague guidance it may hike somewhere around April through September. Firmly rule out the early contracts if you have conviction as a central bank to do so, otherwise markets will do what they’ve done. This was the same issue in Lagarde’s presser the other day. To that effect, tune in to Macklem’s interview with Radio-Canada on Sunday at 11amET.

By January, also note that we could well receive new information to the output gap framework. Further fiscal stimulus packages in the US and Canada may be delivered. Canada’s top-ranked vaccination status across the world should also get a further boost when the 5–11 cohort gets added soon which could raise confidence.

Beyond output gaps, we could get further information into January on other counts as well. Will the BoC stand as firm when it sees ~5% inflation toward year-end into early next year? What if wages continue to accelerate in the more timely Labour Force Survey’s metrics?

It could even be that if the BoC ignores other inflation drivers and rigidly sticks to hiking only when its precious output gap framework gives the green light, then it may risk having to embrace a more abrupt move higher with a 50+ move or two when it finally gets around to hiking.

DETAILS: HOW THE ECONOMY PERFORMED DURING AUGUST

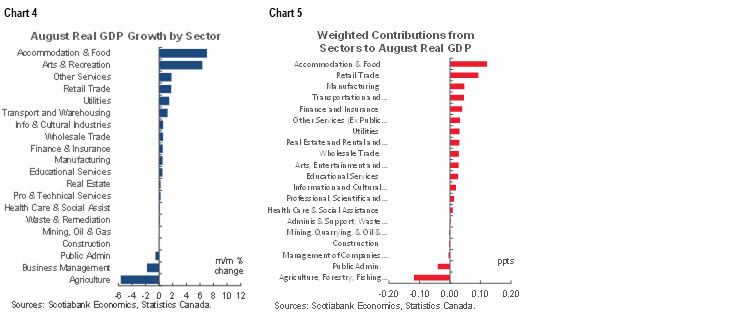

August landed at 0.4% m/m which was materially shy of StatCan’s ‘flash’ guidance for a 0.7% m/m gain.

August’s gain had mixed drivers. Reopening services led the way with a 0.6% m/m gain while the goods sector was slightly weaker at -0.1% m/m. Chart 4 shows the changes in GDP by individual sector which shows that the restaurants and hotels behind the accommodation and food sector led the way followed closely by arts and recreation. These two high contact sectors make sense as the dominant growth drivers given the relaxation of constraints. Chart 5 does the same thing on a weighted contribution to GDP growth basis.

The biggest downside in August came via agriculture, forestry and fishing that fell by 5.7% m/m which also matched July’s decline. Crop production was hammered over the two months due to drought conditions, while forestry fell due to disruptions from forest fires. This is important to flag in that one wouldn’t think monetary policy would be as fussed by forest fires and drought on the hope they are transitory factors setting up future rebounds.

ADVANCE GUIDANCE FOR SEPTEMBER

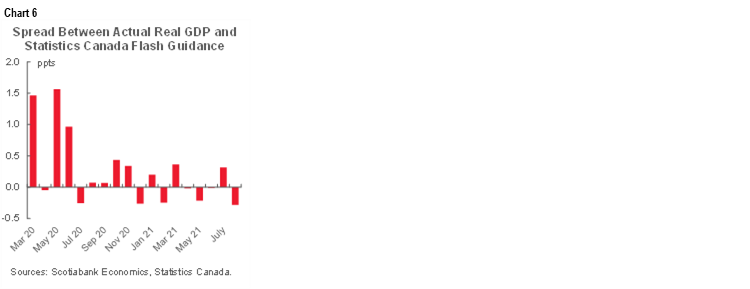

The preliminary guidance for September was “essentially unchanged” which we take to mean zero, although it could be marginally higher or lower. Chart 6 provides a reminder of how the initial flash guidance can deviate from what StatCan currently says was the pattern across monthly changes in GDP and recall that the path to the current estimates across the months has been peppered with multiple revisions along the way.

As for September, there are never details around the ‘flash’ estimate and the only verbal guidance from the agency was that there were gains in mining and energy, wholesale and trade offset by declines in retail trade and manufacturing concentrated in transportation (likely autos) which we knew before hand through the agency’s flash estimates for those goods side readings.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.