- Tapering is likely to commence in November…

- ...with purchases ending mid-2022

- The FOMC forecasts more hikes…

- ...while being divided on whether to start in 2022…

- ...with 2023 still the base case

- Forecast changes were focused upon higher inflation

- Additional press conference insights

The FOMC tweaked guidance in a few areas but on net they were either relatively minor changes and/or so far out in time as to be met by a ‘show me’ degree of skepticism in markets. Markets are also keenly watching matters surrounding the US debt ceiling and China’s Evergrande and in a way that may involve taking Fed commitments on tapering and hikes with a grain of salt. The sum total of the moves broadly met Scotiabank Economics’ expectations.

The S&P500 closed flat compared to just before the full suite of communications from the Fed, the USD slightly strengthened and the Treasury curve slightly flattened with a marginal rise in the two year and five year yields and a marginal decline in the 10 year yield.

That’s a perfectly sensible and very mild market outcome in relation to the overall set of changes and remarks that were offered.

A Summary of What the FOMC Did

The FOMC unanimously set up a probable November taper, guided that purchases would likely end by the middle of next year, played with the dot plot to show a split toward whether to hike or not next year and added to rate hikes thereafter at a pace that roughly equates to about one quarter-point hike per calendar quarter. They also tweaked forecasts by somewhat adding to their inflation expectations and punting growth from this year into next. Elaborations upon each of these moves follows and then additional considerations that were drawn from the press conference are highlighted afterward.

1. When to Start Tapering

The FOMC conditionally set up a reduction of Treasury and MBS purchases at the November 2nd–3rd meeting barring a big negative surprise in the one and only payrolls report before their next decision and assuming nothing else goes off the rails.

They did so by referencing that “a moderation in the pace of asset purchases may soon be warranted.” The word “soon” is the Fed’s code language for signalling something imminent.

2. How Fast to Taper

Chair Powell said in the press conference that the plan is to complete the wind down from US$120 billion per month of Treasury ($80B) and MBS ($40B) purchases to net zero by “around the middle of next year.” That is in keeping with our expectations.

Powell said that no decision was made on the pace of reductions. He also did not remark on the composition of purchase reductions and specifically whether or not to reduce Treasury and MBS purchases in proportional terms or favouring one or the other. It’s likely they’ll do so in proportional terms, but the Chair did not broach the topic today.

3. Hike guidance

The committee was divided on whether to hike in 2022 but I sense Powell is sceptical toward a 2022 lift-off. They upped the 2023 hikes a bit and added 3 hikes in 2024 to get to 1.8% 3+ years from now, but few take the dot plot literally anyway given its performance. They left the UR forecasts unchanged and slightly increased core PCE forecasts in 2022–23 while extending above-2% to 2024 (2.1%).

Statement Changes

There were very few statement changes that are flagged in the appendix to this note. They included the following that bolster the observations provided above.

- The biggest is in the fourth paragraph that states a taper “may soon be warranted” while dropping references to “coming meetings” that when combined together suggest that a November taper is in the cards barring a notable disappointment over the next six weeks. That same paragraph struck out reference to “continue to assess progress” and replaced it with the lower standard that conditions a taper around “If progress continues broadly as expected.”

- The second paragraph offered minor changes, the biggest of which was to replace inflation “has risen” with “is elevated” which implies a touch more discomfort toward present levels rather than just saying they’ve risen.

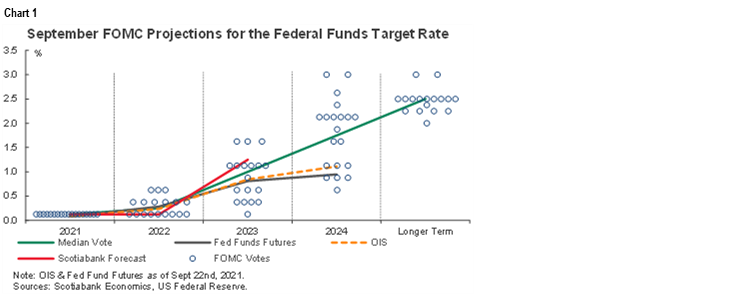

Revised Dots

Chart 1 on the front page shows the latest Rorschach plot from the FOMC. 2022 went from 11–7 in favour of a hold with 5 calling for one hike and 2 expecting 2 hikes, to now showing 9 expecting a continued hold and 9 expecting a hike with six expecting one hike and 3 expecting two hikes. The median estimate is on the bubble between a hike and no hike next year. Key remains vote-weighting this outcome and note that the composition of the FOMC shifts toward being incrementally more hawkish next year.

2023 saw a bit more of a shift with two more hikes than previously and toward a 1% rate by year-end.

2024 showed for the first time three more hikes to a 1¾% policy rate.

The long-run neutral rate estimate of 2.5% was left unchanged.

Stepping back from some of the surprises, it's worth noting that even by 2024 the median dot is still saying they'll only be at the bottom of the estimated neutral rate range 3+ years from now, ending at 1.75% with 6 hikes total.

Forecast Revisions

Charts 2–5 show the forecast revisions to GDP growth, the unemployment rate and inflation rates. Summary observations follow.

1. GDP

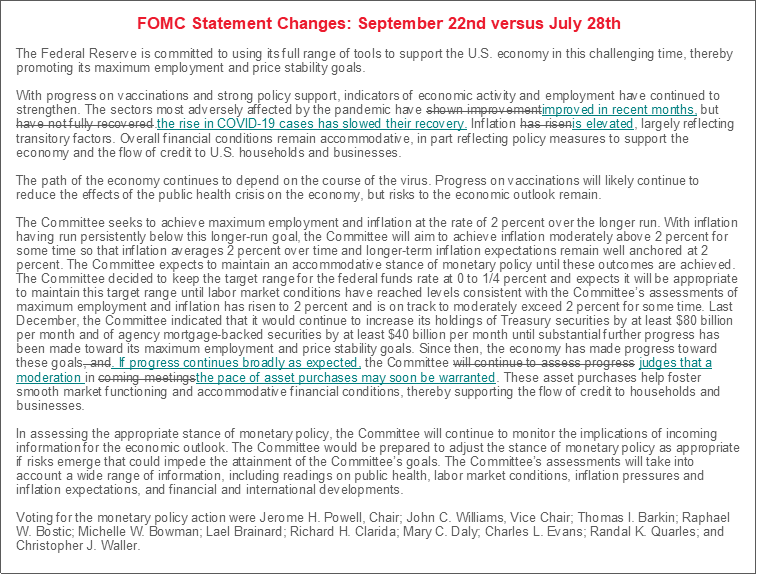

Growth projections were lowered for this year in a mark-to-market sense like everyone else given recently mixed readings (5.9% from 7%). 2022 was revised up to 3.8% (from 3.3%) and so the bias is to punt this year’s downward revision into next year. 2023 was little changed at 2.5% (from 2.4%) and the addition of 2024 sees the FOMC consensus at 2% with an unchanged longer run proxy for potential growth unchanged at 1.8%.

2. Inflation

Core PCE inflation was revised up by 0.7% to 3.7% this year largely in mark-to-market fashion given that the FOMC previously underestimated inflationary pressures to date. They went further, however, by revising up 2022 by two ticks to 2.3% and by revising up 2023 a tick to 2.2% with the addition of the 2024 forecast expecting another above 2% reading of 2.1%.

Headline inflation was revised up 0.8 points to 4.2% this year but also revised up a tick to 2.2% in 2022 with 2023 left unchanged at 2.2% and then the addition of 2024 set at 2.1%.

When commenting on the forecast revisions, Powell noted that the FOMC moved up its nearer terms forecast due to bottlenecks and shortages and how they have not yet begun to abate and could be with us into next year.

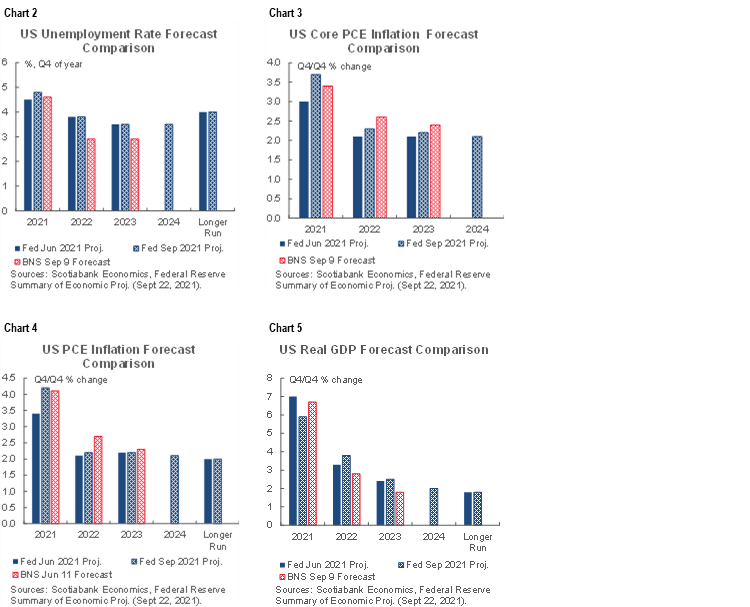

3. Unemployment

The unemployment rate was revised up a bit for this year to 4.8% from 4.5%, but left unchanged for 2022 (3.8%) and 2023 (3.5%) while the addition of 2024 sees the rate flat at 3.5%. The longer run unemployment rate remains unchanged at 4%.

Additional Press Conference Insights

Beyond the statement and forecasts, Powell’s press conference offered the following insights.

A High Bar to be Knocked Off Taper Plans

When asked whether he still expects solid jobs reports going forward and whether a soft September report would affect prospects for tapering as soon as the November meeting, Powell said “it would not take a knock-out jobs report to meet the test, only a reasonably good report.” Powell went on to dismiss the August payrolls weakness as a Delta report while indicating that he still expects faster job growth when parents return to work as the kids go back to school. That’s unclear, however, in that the Household Pulse survey shows that most parents already went back to work over the summer during the months when about one-million per month gains were being clocked. If so, then September payrolls could still reflect the Delta drag and be absent the parental effect that might have largely concluded earlier.

An Inclusive Recovery and Monetary Policy

Powell has backpedalled on the extent to which the Fed will focus upon a fully inclusive recovery compared to earlier in the pandemic. When asked point blank “Would a sustained black versus aggregate unemployment rate gap alter your plans, Powell said that eliminating racial and other disparities is best left to fiscal and education policies and that “We've done our part.” That’s sensible to monetary policy observers who understand the limits of the Fed’s powers to affect individual groups in society relative to other policy tools, but it’s a striking difference to Powell’s earlier remarks on the need to have a fully inclusive recovery before seeking policy exits.

Ducked the Debt Ceiling

Powell was asked what he thinks of the debt ceiling uncertainties and simply gave a throwaway comment on how “it’s very important to pay our bills and address the debt ceiling.” When probed for what he tells members of Congress and other officials, Powell deflated by saying “I don't discuss conversations I have with elected officials.”

Evergrande’s Effects

Powell was asked two questions regarding China’s issues with Evergrande. The first question was whether it was a preview of the risks facing US corporate debt given the level of US corporate debt. Powell shot that down by noting US corporate defaults are very low and that while they were concerned at the beginning of the pandemic due to the revenue hit, they did not ultimately get a wave of corporate defaults partly due to the CARES Act.

The second question regarding Evergrande pertained to how the Fed views its implications. Powell argued that it seems very particular to China which has very high debt for an EM economy and Evergrande is part of getting that under control. He noted that there is little direct US exposure and that big Chinese banks have little exposure. In general, Powell’s tone indicated he is not so fussed by it all. One hopes he’s right, but near-term events will rapidly inform this perspective.

What Happens After Tapering

Powell was asked about his thoughts on shrinking the balance sheet and deflected the question by saying “let's taper first and then get to those other related issues. We'll do that but first things first.”

Earlier Rate Hikes?

When asked whether lift-off on rates could occur before finishing tapering, Powell said “That's not my expectation,” and went on to note that they could instead speed up or slow down taper plans. He also observed that back in 2013–14 they said tapering is not on a pre-set course and yet “This will likely be a shorter period than in 2013 because the economy is much further along than back then.” The implication is that rather than hiking ahead of ending purchases, the Fed would be more likely to speed up tapering first and should conditions warrant such a step.

Digital Currencies

On digital currencies, Powell advised that the Fed is looking at whether to introduce a central bank digital currency (CBDC) and evaluating the pros and cons. He noted there will soon be a discussion paper to inform the Fed’s stance on a CBDC. He noted that they need to ensure that appropriate regulatory conditions are in place and that they are not.

Please see the attached tracking of changes in the September policy statement compared to the July statement.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.