- A little more balance sheet was put in everyone’s stockings...

- ...through a significant liquidity injection that added support to Treasuries, risk assets

- Fed funds rate was cut by 25bps as widely expected

- Median FOMC rate projections were unchanged, still showing modest further easing

- Powell signalled a conditional pause awaiting coming data…

- ...that may have a shelf life measured in days or weeks

- US Treasury curve bull steepened, equities gained

Happy Holidays. The FOMC wants to wish you a very merry year-end. They pulled off a dual rally in bonds and equities by putting significantly more balance sheet in everyone's stockings paired with a rate cut and unchanged projections for modest further easing.

That offset the fact that Chair Powell conditionally leaned toward taking a breather on further policy rate adjustments in favour of seeing how the economy performs after 175bps of cumulative cuts from the 5.5% peak last year and 75bps since September.

Conditional, that is, upon how missing data evolves. That’s all very, very tentative with a shelf life potentially measured in days or weeks as key lagging and backed up data rolls in after the government shutdown. We need to see October and November payrolls next week, December payrolls in early January and multiple inflation readings. I would read about as much into this conditional pause as when Powell said a rate cut today was “far from” being likely back in October. It’s simply not known how conditions will evolve as the data backlog clears and how markets respond.

Powell’s comments that are backing upgraded GDP projections appear to be a speculative bet that productivity growth will surge partly on AI effects. Some of the views he expressed during the press conference are tough to square. Plus, the Fed is operating in the realm of massive unknowns, like how trade policy and its effects will evolve, how AI will work through the dual mandate, how fiscal policy could unfold with possibly further pump priming ahead of midterms, and how immigration policy will evolve among others.

Markets nevertheless liked what they heard. The 2-year Treasury yield fell by about 5bps to close down 7bps on the day, with 10s richening by 3–4bps on the day. The S&P500 moved up by about 0.6%. The dollar softened a touch. Overnight markets should rally.

UNCHANGED FORWARD RATE GUIDANCE

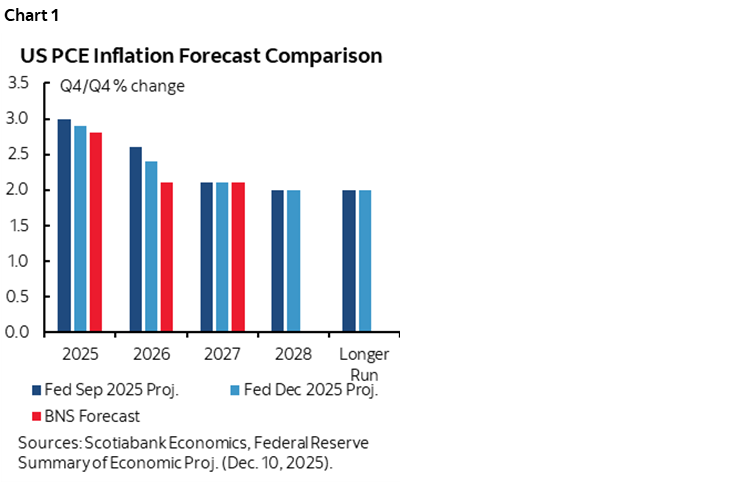

The language was tweaked a touch which I’ll come back to, but the Committee’s median policy rate projection did not. The median Committee member still expects another 25bps of cuts next year, then another 25 in 2027 and then holding at 3.25% (chart 1).

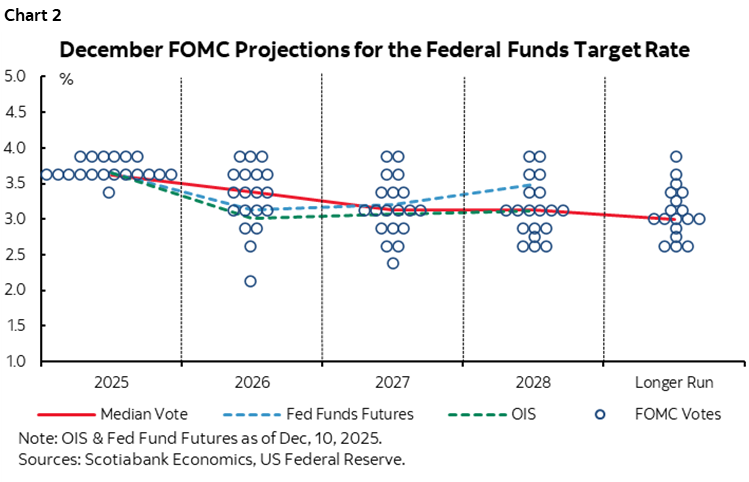

The dispersion of the dots remains high (chart 2). For next year, three want no cuts including a desire to have had nothing today, four want to hold at the present 3.75%, four want another –25bps, four more want –50bps, then 2 want –75bps, one wants –100, and one (probably Governor Miran) wants 150bps of further cuts. Our 3% (-75bps) by Spring is somewhat aggressive but not terribly so.

A PUMPED UP AMPLE RESERVES FRAMEWORK

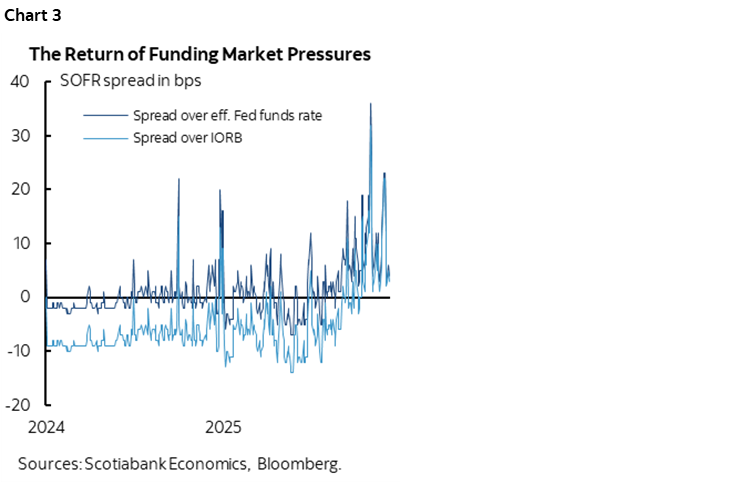

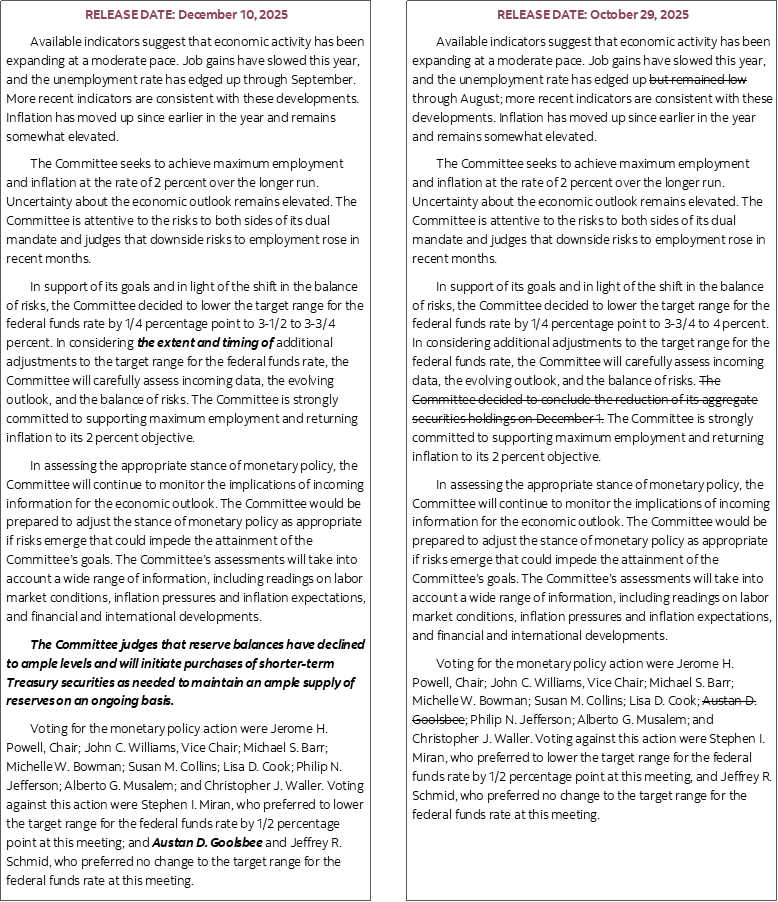

Key to the overall communications from a markets standpoint was the pair of announcements out of the NY Fed (here, here). They had previously announced ending the reduction of aggregate securities holdings on December 1st in the October statement.

Now they took that a big step further by essentially enabling US$40 billion/month of reserve management purchases. That injects significant liquidity into markets and is designed to ensure that bank reserves are truly ample not just now but through seasonal effects such as the April 15th tax deadline as Powell emphasized in his press conference.

Improved liquidity and reserves lends greater support to risky assets and improves monetary policy transmission effects as the volatile pressures on money market versus effective fed funds rates should abate (chart 3).

STATEMENT CHANGES

There were limited changes to the policy statement summarized as follows:

- They inserted “the extent and timing” in front of additional adjustments to the policy rate which adds a bit more uncertainty to the amount and timing of further easing.

- They struck out ‘remained low’ in reference to the unemployment rate which is a dovish signal.

- As noted, they changed balance sheet policies and statement codified this as follows: “The Committee judges that reserve balances have declined to ample levels and will initiate purchases of shorter-term Treasury securities as needed to maintain an ample supply of reserves on an ongoing basis.”

FORECAST CHANGES

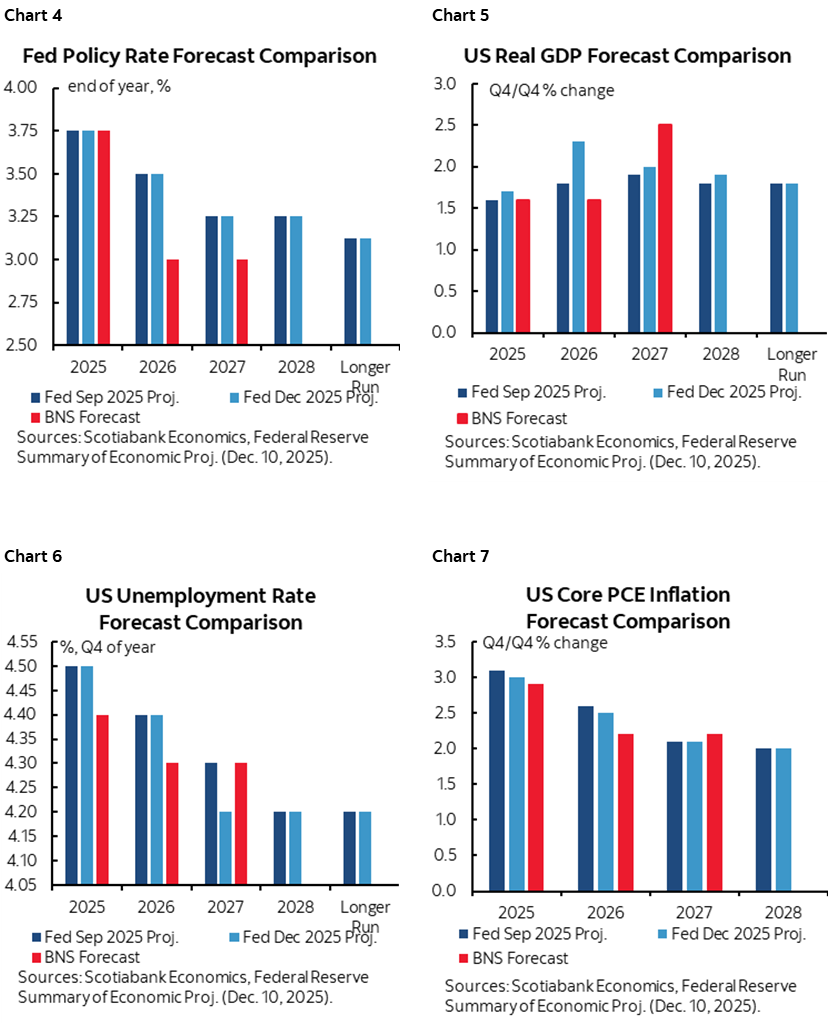

Forecast changes were fairly minor. Charts 4–7 compare their forecast revisions to our current projections.

- GDP growth was bumped up a tenth this year to 1.7% y/y (always Q4/Q4), 2.3% in 2026 (from 1.8%), 2% in 2027 (from 1.9%), and 1.9% in 2028 (from 1.8%). Longer-run potential GDP growth was left at 1.8%.

- The unemployment rate projection was left unchanged at 4.5% and 4.4% in 2025 and 2026 respectively but lowered a tick to 4.2% in 2027 and then flatlined with an unchanged natural rate of unemployment estimate of 4.2%.

- Core PCE inflation was revised down a tick in each of 2025 and 2026 to 3.0% and 2.5% respectively. Then unchanged at 2.1% in 2027 and 2.0% in 2028.

PRESS CONFERENCE TRANSCRIPT

What follows is an attempt at providing a rough transcript of the press conference. I would encourage readers to skim it as there are a few more gems in here. As always, any errors or omissions are to be blamed on my typing skills!

Q1. Does "extent and timing" indicate you are on hold until clear signals in data?

A1. The adjustments since September bring our rate to within broad ranges of neutral. The new language points out that we'll carefully evaluate incoming data. Having reduced by 75bps since September and 175bps since last Sept brings the policy to withing neutral rate ranges.

Q2. This seems like an optimistic outlook. Why?

A2. Partly that consumer spending has been resilient. AI spending and on data centres has been holding up investment. We expect a pick up in growth from today's relatively low level of 1.7% y/y Q4/Q4. Some of that is due to the gov't shutdown that transfers two-tenths. Fiscal policy is expected to be supportive.

Q3. Is the risk management phase of rate cuts over? Have you taken out enough insurance against data uncertainty?

A3. We'll get more data next week. We are well positioned now to wait and see how the economy performs from here.

Q4. You had a big increase in GDP but not a change in unemployment. Is that AI? Why?

A4. The implication is higher productivity. Some of that is AI. Productivity has been structurally higher for years now.

Q5. Is there a much higher bar for further cuts in the near term given some opposition? What does the Committee need to see to support a January reduction?

A5. Our two goals are in tension. Everyone agrees that inflation is too high and the labour market faces downside. The difference lies in how do you weight those two parts of the mandate. In terms of what it would take, the effects of the -75bps of reduction will lag. We'll just have to see the data. The data may be distorted really because data was not collected in October and half of November [ed. he's referring to the household survey, CPI].

Q6. Is there a point at which dissents become counter-productive?

A6. I don't feel that we're at that point at all. These are good, thoughtful, respectful discussions. I could make the case on either side. It's a close call.

Q7. With policy closer to neutral is it a foregone conclusion that the next move is down or is policy risk two-sided here?

A7. A rate hike is not anyone's base case. Some people feel we should stop, or cut once or more next year. It's either holding or cutting a little or more than a little.

Q8. What gives you confidence the UR won't keep rising in 2026 especially given sectors like housing that still face restrictive policy?

A8. Cutting 175bps so far could put us in a position where the UR stabilizes and avoids a sharper downturn. At the same time, policy is now in a place where it is not accommodative. We're well placed to see how that turns out and the data will tell us whether we were right or not.

Q9. Why did the Committee decide to move today rather than January especially given your comment in October about slowing down into fog?

A9. Gradual cooling in the labour market has continued. The UR is up three-tenths. Payroll jobs we think are overstated by 60k in recent months. The labour market has continued to cool gradually, maybe just a touch more gradually than we thought. Inflation has come in a touch lower. Services inflation coming down is offset by tariff effects. It doesn't feel like a hot economy that wants to generate inflation.

Q10. How concerned were Committee members about tensions in money markets?

A10. Pressure on some money market rates is telling us we are in an ample reserves context. That's why we took today's steps to keep an ample reserves framework. We want ample reserves even when seasonal factors like tax season (APril 15th) work through.

Q11. How are you hoping SCOTUS [ed. Cook decision] will rule and why have you been so reticent to comment on such an important matter?

A11. It's not something I want to discuss.

Q12. Inflation forecasts have come down. Do tariffs pass through in 3 months or 6 months and is the threat to jobs?

A12. It could take quite a while for an individual tariff to have its full effect. Then is it a one-time effect or sustained inflation. If there are no new major tariff announcements then inflation from goods should peak in Q1 roughly or so and then from here it should be a couple of tenths or less and then after that, say nine months, you should see that coming back down in the back half of next year.

Q13. Does a new incoming Fed chair impact your decisions?

A13. No

Q14. Why do you think cutting will bring down longer term yields?

A14. Break-evens are at very comfortable levels beyond the short-term. Same with consumer surveys. [ed, who cares, markets and consumers routinely get longer-run inflation totally wrong].

Q15. Can you explain to Americans why you are prioritizing the labour market over inflation that is the bigger concern to Americans?

A15. The best thing we can do is restore inflation to its 2% goal but also have a strong economy where real wages are going up. You need some years of solid earnings growth to have some greater comfort about affordability.

Q16. Why is job growth so much worse than official data in your opinion?

A16. It's very difficult to estimate job growth in real time. They don't count everyone, it's a survey. There is a persistent over count. We think the over count in the payroll jobs numbers is continuing and we think it's about 60k jobs per month which could be wrong by 10 or 20 in either direction. Labour supply has also come down quite sharply. We need to watch the balance.

Q17. How much are you factoring AI into current weakness in the job market?

A17. It's been a small effect, sometimes cited in announcements. At the same time, people are not filing for unemployment insurance. Longer-term we don't know what we'll see but it may be that in past innovation eras you have seen some jobs destroyed and others made. When you get through that you have higher productivity and new jobs. This may be different. We're going to have to see. It's early days.

Q18. Why is there such a division between Board members and regional PResidents?

A18. There are people on both sides. I wouldn't put too much in that.

Q19. How would you react if SCOTUS struck down IEEPA tariffs?

A19. We really don't know, it depends on a whole bunch of things.

Q20. How sustainable is the k-shaped economy?

A20. Surveys are saying people are tightening their belts, buying less of certain things, while securities values are high and tend to be held by higher income earners. The top-third of earners accounts for way more than a third of spending. The best thing we can do is price stability and full employment.

Q21. Housing question.

A21. 25bps won't do much for housing, it's more of a supply issue and we don't have the tools to address this.

Q22. Where are the inflation risks? Why not cut more?

A22. We see most of the inflation over target is in goods. We expect this will be a one-time price increase and will come down. Tariff inflation could turn out to be more and more persistent. Or the labour market gets tight and feeds more inflation which I don't see as likely.

Q23. Are we experiencing a positive productivity shock? How much of that is driving projections?

A23. I never thought I see five or six years of the recent kind of productivity growth. And that was before AI. If you use it in your own lives then you see its impact on your own productivity. We're definitely seeing higher productivity. It's a little quick to say its GenAI. The pandemic may have driven companies to use computers to do more relative to workers.

Q24. You have 3 more meetings at the helm. What do you want your legacy to be?

A24. I really want to turn this job over to whomever takes over with the economy in really good shape with low inflation and a strong labour market.

Q25. Do you plan to stay on the Board after?

A25. I have nothing new to offer.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.