Next Week's Risk Dashboard

- Should we fear the credit cycle in the US and Canada?

- US regional banks are in a different spot to 2023

- ‘Mag7’ earnings are coming

- Inflation week in Canada starts with producer prices…

- …then BoC surveys that will likely show lower inflation expectations…

- …and then Canadian CPI is unlikely to show relief from retaliatory tariffs…

- …and then outcome will firm up our BoC call for October 29th

- US CPI is (finally) coming this week

- PMIs to inform the state of global supply chains

- China’s GDP growth could tumble into the Asian market open

- Sovereign debt markets to react to France’s downgrade by S&P

- CPI updates to matter more to RBNZ, BoJ, than the BoE

- Argentina’s voters enter the final stretch

- BoK may remain in no rush

- Bank Indonesia is a coin flip

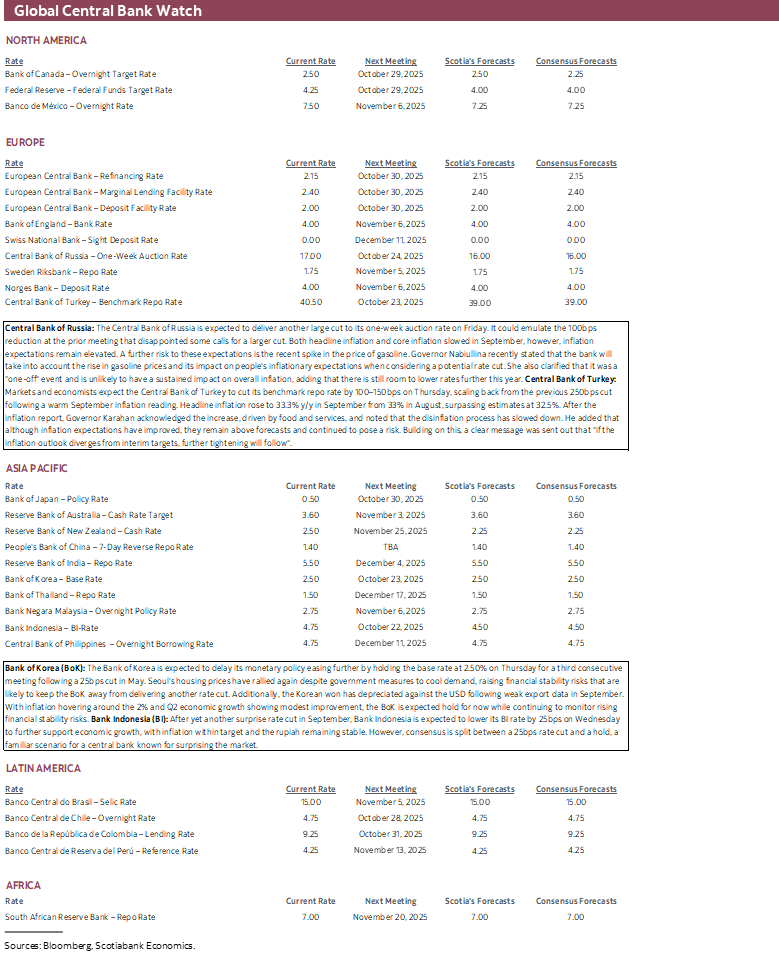

- Russia’s central bank may have more confidence to ease

- Turkey’s volatile central bank

Chart of the Week

This being a weekly publication, a considerable part of the focus is, naturally, upon the coming week’s expected developments. Interwoven throughout these weeklies, however, are usually special topics that are of relevance to markets. This week’s issue focuses on the credit cycle after markets gyrated to end the week due to a combination of debates about the credit quality cycle and President Trump’s volatile headlines on China.

In terms of calendar-based developments, the main focal points will be corporate earnings—including some of the ‘Mag7’—plus CPI inflation readings from the US, Canada, UK and Japan and global PMIs. Markets could start the week reacting to France’s downgrade late Friday, and key data on the health of China’s economy that could see growth tumble. Toss in four regional central banks before the next week’s decisions from the big boys and girls of central banking (the Fed, BoC, BoJ, and ECB).

NO ALARMS RINGING ON CREDIT QUALITY

A tiny handful of US regional banks reported that they’ve been victims of loan fraud and suddenly we’re being told that the end is near. This was the intimation provided by inflamed headlines about cracks and challenges appearing in credit quality as an alleged harbinger of terrible things to come.

While not 100% untrue, it is a grossly exaggerated narrative. Some perspectives will be shared, drawing upon a lot of work in my career on forecasting funding, credit, and saving products and credit quality cycles.

US Regional Banks Are in a Different Spot

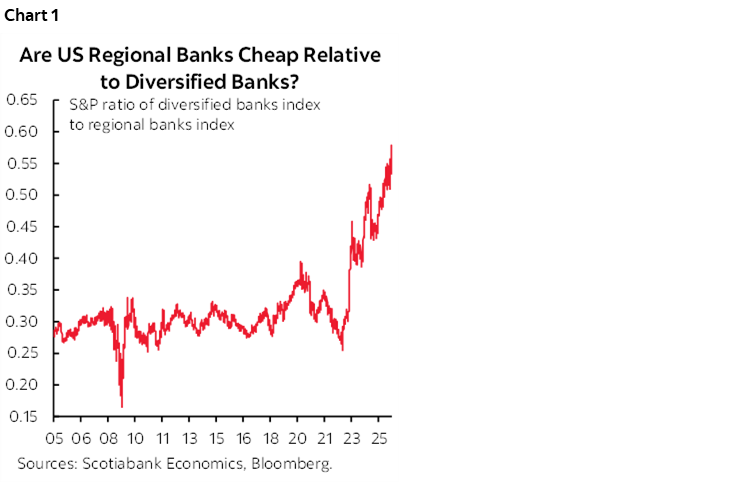

First, any parallels to 2023 when US regional banks went through turmoil face a very different starting point on valuations today. Back then, regionals were expensive relative to large, diversified US banks. Today they are much cheaper (chart 1). Ergo, relatively weaker prospects may be priced.

There are many potentially explanations of these movements in relative bank valuations perhaps among them being more lucrative rewards to big banks from deregulation, such as changing e-SLR leverage rules. I’m also still of the belief that the US banking system remains overly fragmented with 76% of FDIC-insured institutions having less than US$1 billion in assets and 96.5% of all US banks having less than US$10 billion in assets which are tiny numbers in the world of banking. Keep on consolidating, as the long wave movement away from pernicious regulation that kept banks localized is ongoing.

Furthermore, the Federal Reserve’s response to the regional bank frailties in 2023 showcased the ability to use a suite of tools to right the ship if they prove necessary to employ and while doing so independently from the conduct of overall monetary policy. Tweaks to discount window borrowing, funding market interventions, and a separate Bank Term Funding Program were among the tools rolled out—while the policy rate was managed separately toward dual mandate goals. Today, the signals being sent by the Fed indicate winding down quantitative tightening (shrinking its portfolio of bonds) over coming months as Chair Powell put it and this could lend confidence to markets debating pressures on liquidity.

Corporate Credit Quality Remains Robust

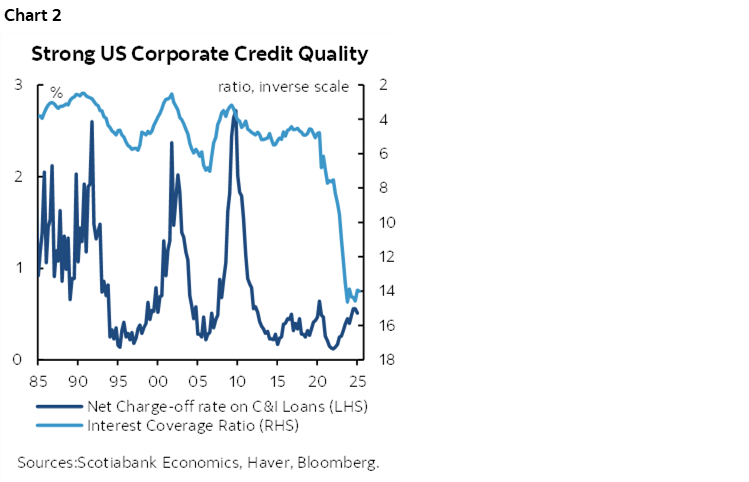

Second, the corporate credit quality cycle remains practically pristine. A macro indication of this is shown in chart 2. Corporate interest coverage—that divides a cash flow proxy by interest payments—is plotted on a reverse scale to show the high correlation with net charge-offs on US commercial and industrial loans. Coverage remains historically strong and while charge-offs are off the cycle’s bottom when credit was practically free in the pandemic, it remains very low by historical standards.

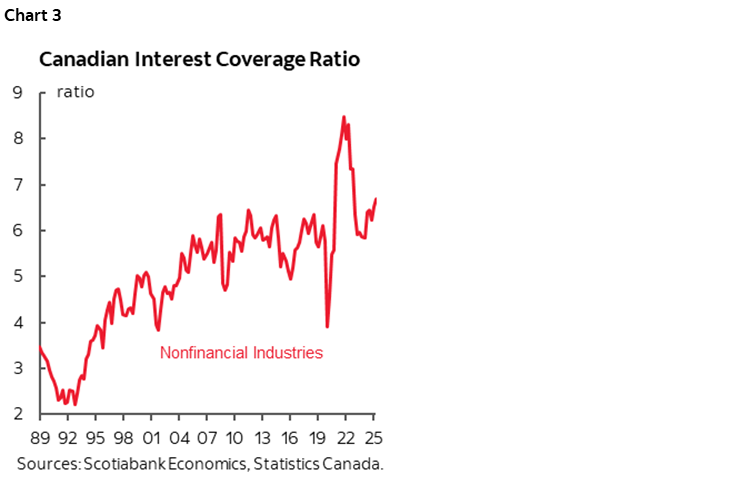

Chart 3 shows the Canadian equivalent for corporate interest coverage.

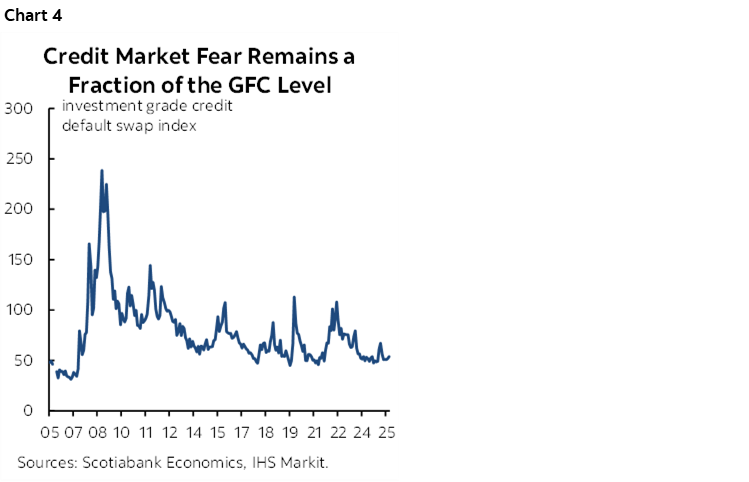

Markets See Low Corporate Credit Default Risk

Third, the market is pricing low credit default risk. There are many measures of this, but one of them is shown in chart 4 that plots an investment grade credit default swap index that equal-weights 125 credit default swaps on multiple sectors of the US economy.

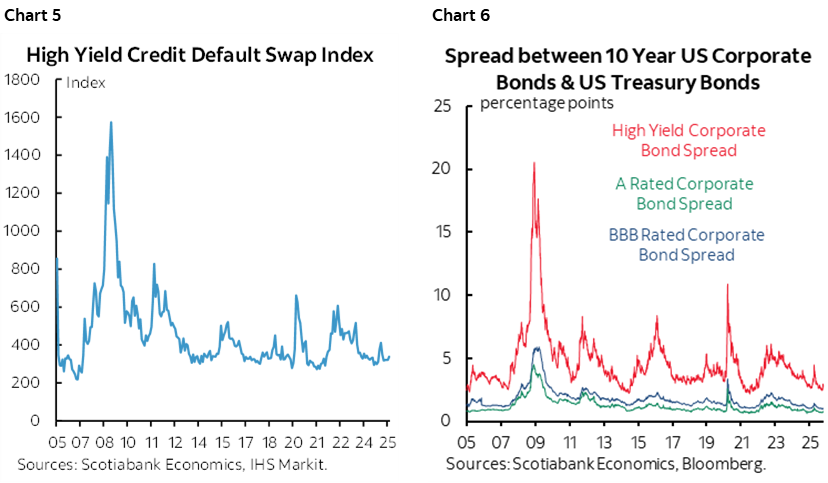

Chart 5 plots a similar measure for high yield non-investment grade entities. Chart 6 plots measures of corporate bond spreads that remain tight by historical standards.

A CDS enables investors to pay for protection against default. While the cost of protection has slightly increased of late for both investment and non-investment grade borrowers, it remains historically very low.

That’s not an assurance of anything, since recall that it was even lower than at present until about mid-2007 before lax regulation, malfeasance and excess off-balance sheet leverage drove the Global Financial Crisis. At least, however, we’re not seeing much by way of early warning signs that have investors scurrying for a lot of cover at this point.

Household Credit Quality is (Mostly) in Fine Shape

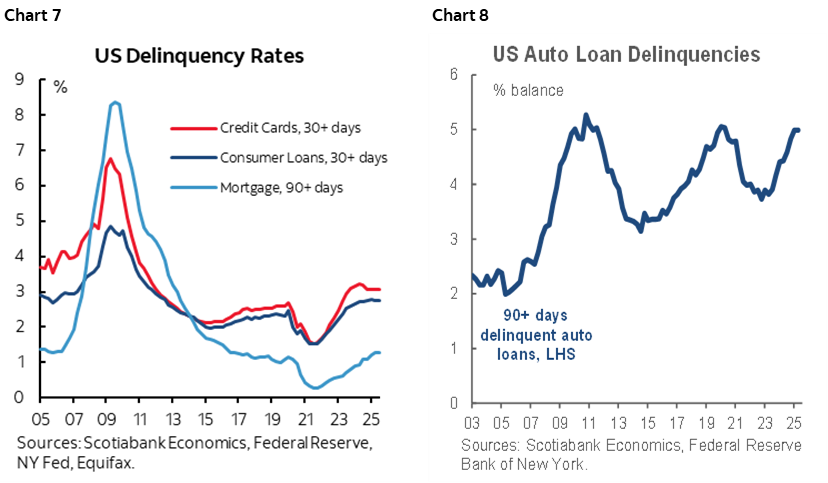

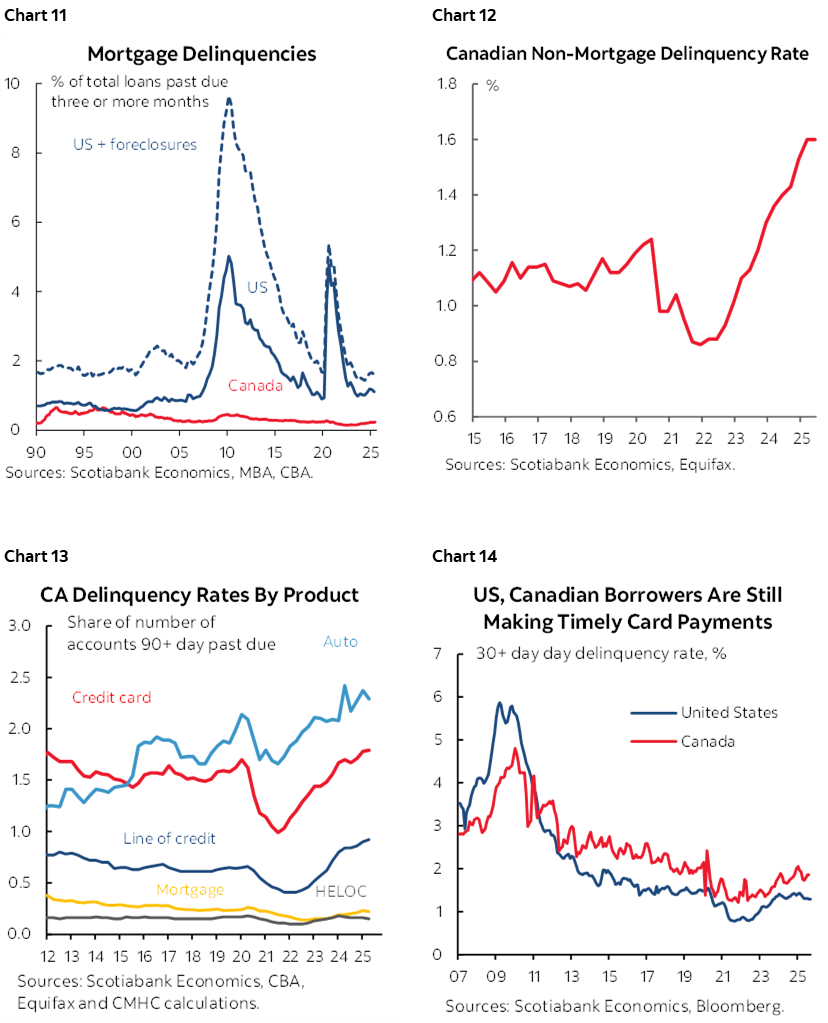

Fourth, the US household sector is showing somewhat mixed but generally still constructive signs for overall credit quality. All measures of delinquencies are off the pandemic lows as borrowing costs have risen, but most are not terribly disconcerting (chart 7). Mortgage loans dominate US household borrowing and mortgage arrears over 90 days are as low as they were on the eve of the pandemic. Delinquency rates on cards, consumer loans and auto loans are above pre-pandemic levels, but modestly so. Auto loan delinquencies are floating toward record highs while tariffs are likely to pressure financing affordability in the US (chart 8).

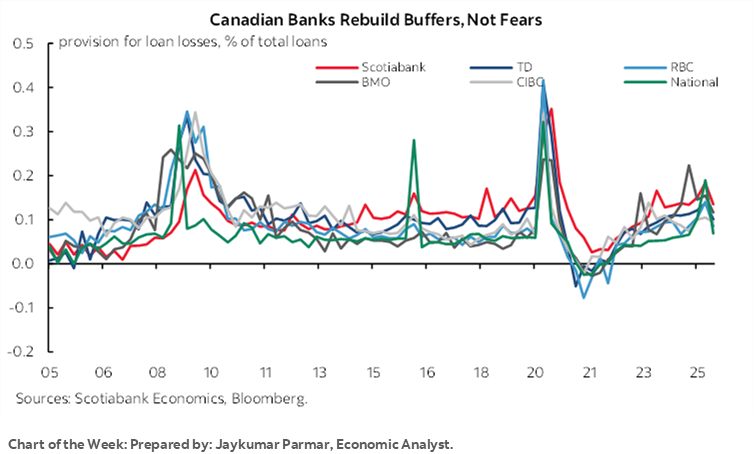

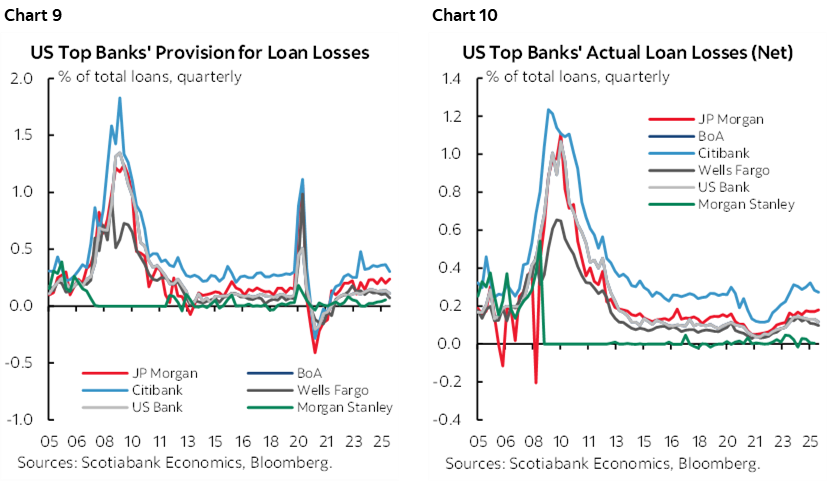

Charts 9 and 10 show US banks’ provisioning for loan losses and actually loan losses as a percent of all loans. From losing basically nothing during the free credit period of the pandemic, banks are mean reverting to something more akin to the prior period.

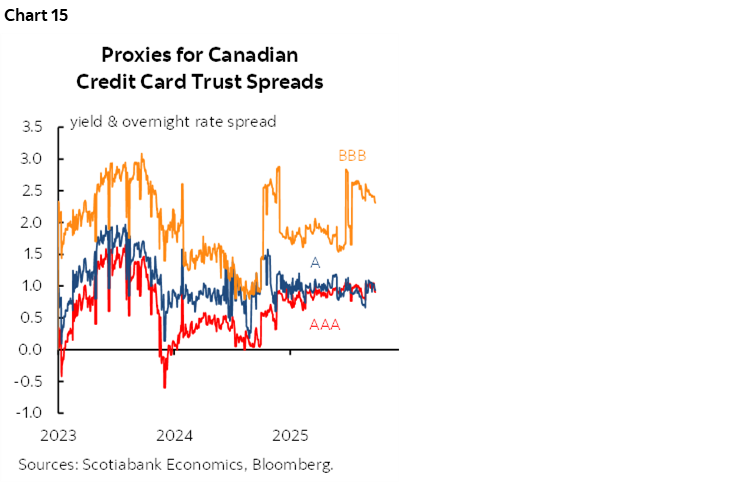

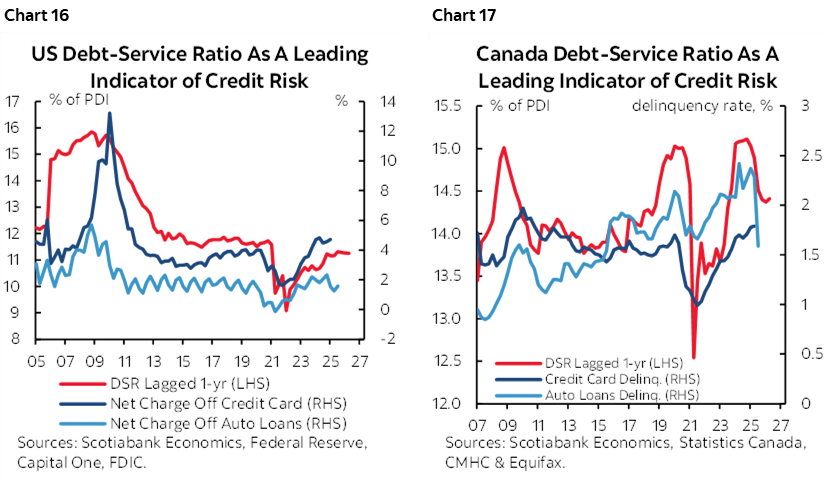

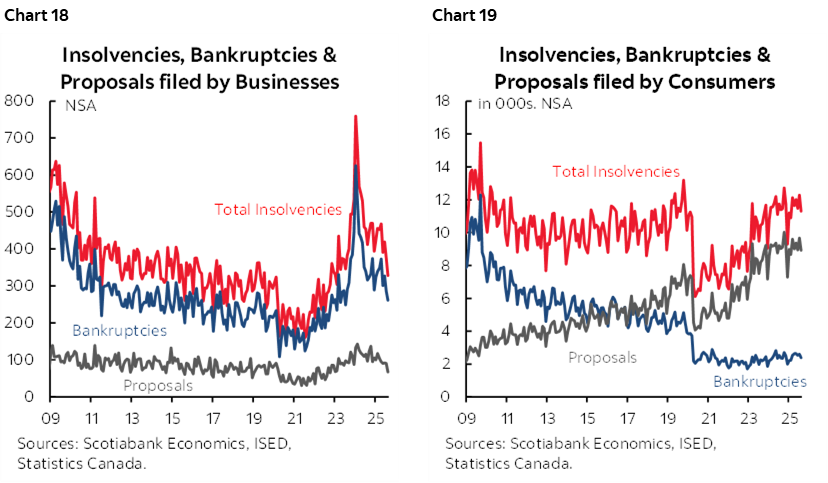

The same is generally true in Canada. Mortgage delinquencies are always very low and remain so in absolute terms and certainly relative to the US for a multitude of reasons (chart 11). Bank provisioning for mortgage loan losses remain well within historical norms as a share of the changing amount of loans granted over time. Delinquency rates on non-mortgage household loans are rising but still low (chart 12); at about 1.6%, the rate is double the pandemic low when nobody defaulted because credit was practically free in the pandemic (the real cost of borrowing pushed deeply negative). Still, the 0.4 percentage point rise compared to pre-pandemic remains very low. In my opinion, agencies selling their credit reports and services should be more careful with their commentaries. Chart 13 breaks out products. Credit card delinquencies are off their troughs in Canada and the US, but are generally only back to the pre-pandemic period when credit was far less cheap (chart 14). Further, market pricing for credit card trust spreads across ratings remains in volatile ranges (chart 15).

In both countries, the household debt service burden—the share of after-tax personal disposable income going toward total debt payments including interest and principal—serves as a leading indicator of delinquencies (charts 16, 17). As the migration away from dirt cheap borrowing costs in the pandemic raised the debt service burden, what we’re now seeing is a recent stabilization partly because monetary easing is working through the system in lagging fashion. If debt service is plateauing and easing off, then in lagging fashion so may delinquency rates.

As an offshoot of this argument in the Canadian context, chart 18 shows business bankruptcies and proposals and the combination (insolvencies) on a downward trend after the removal of pandemic supports. Resources are being reallocated. Chart 19 shows the same for consumers; work outs with lenders to deal with pressures like mortgage resets are still resulting in very low bankruptcy numbers.

The overall picture in corporate and household credit markets on both sides of the border comfortably supports cautious optimism. Conditions will require close monitoring as the lagging effects of policy developments and uncertainty work their way through the global, US and Canadian economies as fiscal and monetary policy adapts. In addition to borrowing costs, key will be how labour markets adapt to likely downside pressure on demand for workers but also less supply through sharply tighter immigration policies in both countries.

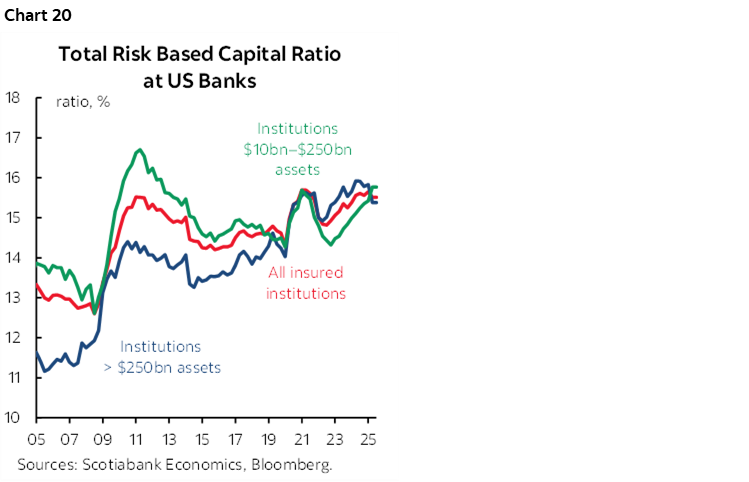

As for casual GFC parallels, unless you’re prepared to tell me that banks are not actually very well capitalized (chart 20), that regulators are asleep again, and that leverage is again being heaped on top of leverage off balance sheet in SPVs, then rein in such parallels. Today’s risks are fundamentally different than the balance sheet recession we went through back then. Today, if anything, is putting macroeconomic policy risk front and centre—needlessly so, in some cases—with the epicentre being US policies.

CANADIAN INFLATION—SMOKE SCREENS

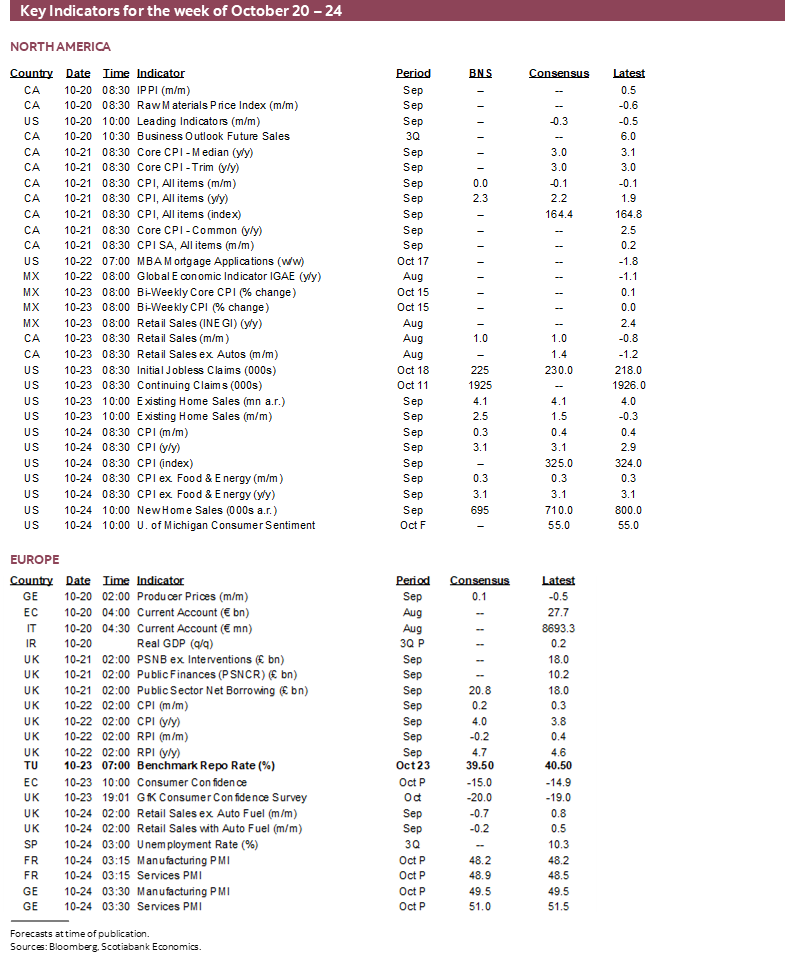

Canadian inflation nutters will get their fix this week through a hat trick of readings. Monday brings out producer prices in September along with the Bank of Canada’s quarterly pre-MPR surveys. Tuesday then reaches a crescendo with CPI for September.

The suite of these readings will be the last material pieces of the puzzle for firming up a call for the October 29th BoC decision especially after Governor Macklem’s emphasis on the data. At this point, the argument for another cut at that meeting is mixed.

- Given that the policy rate is already well into the neutral rate range, the BoC may be in the fine-tuning stage of adjustments that can be spread out while assessing developments. This was the approach the BoC took in early 2015.

- the 60k jobs created in September that also included gains in sectors—like manufacturing—that are most likely to be hit by tariffs offers temporary comfort. Still, however, Canada has lost about 46k jobs in the past three months. Cooling growth in population and the labour force could mean that the required monthly breakeven rate of job growth to keep the unemployment rate reasonably stable may by very low, but probably not negative.

- Canada ended many retaliatory tariffs in September which might alleviate some inflation risk, but I’ll come back to this point.

- The BoC may prefer to see the results of the November 4th federal budget before deciding whether to add monetary policy stimulus.

- The economy has been weak with three consecutive small declines in GDP of -0.1% m/m before a mild 0.2% expansion in July and preliminary guidance that August GDP was flat. Our tracking of Q3 GDP growth is barely positive and it wouldn’t take much to turn negative for a second consecutive quarter. With GDP tracking below potential growth, spare capacity is rising which may give the BoC added reason to cut given the longer-term disinflationary effects.

- Trade policy uncertainty will be elevated for a long while yet. When trade negotiations with the US may result in an agreement is as unclear as what kind of agreement may take shape. The BoC may wish to give this more time to develop.

Producer Prices on the Rise

Producer prices are an indirect possible measure of ultimate consumer price inflation that the BoC is mandated to manage at 2% over the medium term. Seasonally unadjusted industrial product prices have been rising more quickly than normal over the past three months to August with prices up 4% y/y and on a two-year upswing with September’s figures coming on Monday. Excluding energy, industrial prices are up by almost 5% y/y and led by metal products (20.5% y/y) and a broad array of other prices at lower rates of increase.

Expect this to continue on a trend basis, but key is pass through to consumer prices which is highly uncertain and quite limited to date.

BoC Surveys to Refresh Inflation Expectations

The BoC’s surveys on Monday will be stale on arrival as usual but could incrementally inform measures like inflation expectations. The prior Business Outlook survey showed more firms expecting input prices to rise over the next year, steady growth in selling prices, a shorter-term tendency to absorb tariffs in profit margins, yet inflation expectations still toward the top end of the BoC’s 1–3% inflation target range across all horizons (1-, 2-, and 5-years ahead).

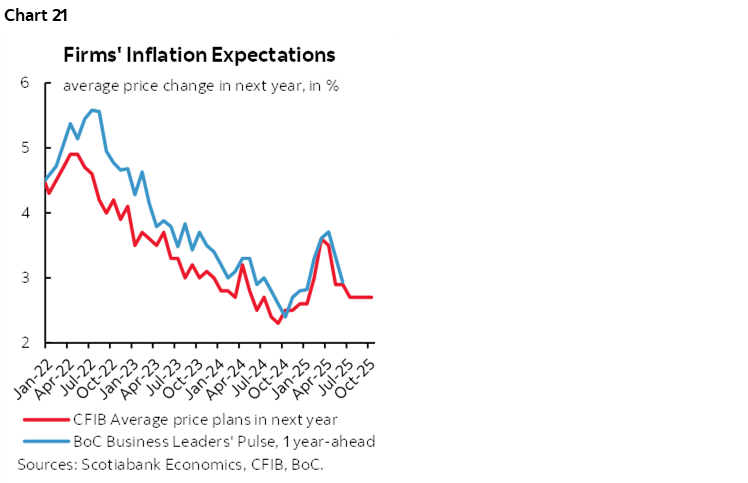

The CFIB’s monthly small business measure of inflation expectations is a timelier gauge and one that is highly correlated with the BoC’s lagging measure. It points toward a further reduction this time (chart 21). It could comfort the BoC if that happens.

The BoC’s consumer survey is also due out on Monday. It is a combination of online data collected during August with some top-up phone interviews in early September. Like the business surveys, they will miss important developments like the application of more US tariffs. In the prior edition, over half of respondents expected inflation over the coming year to be above 3% with about 29% in the 1–3% band. Survey-based measures of inflation expectations remain high.

There are no reliable market-based estimates of inflation expectations in Canada given the past freeze on issuance of real return bonds and the tendency of large investors to buy and just sit on them.

CPI—Reducing Retaliation May Not Help

Then September CPI lands on Tuesday. I’ve estimated headline inflation to be flat at 0% m/m in seasonally unadjusted terms as per the polling convention. That could translate into a 0.4% m/m seasonally adjusted rise based on a stable SA factor for September.

Canada ended most retaliatory tariffs against the US at the start of September. They affected about C$44 billion of goods imports. Canada retained tariffs on autos and metals that account for about another $15B of imports. Taken literally, ending 25% tariffs on 6% of imports could be a meaningful drop in CPI assuming full pass through. However, when the tariffs were first applied and over subsequent months, the discernible effect on CPI was negligible. By corollary, I’ve assumed their removal will also be a negligible influence on September CPI.

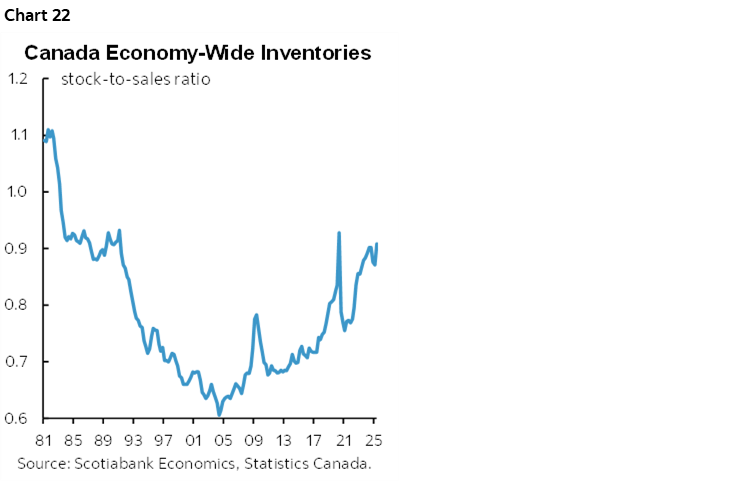

Aside from their limited application, one reason for no real pass through of retaliatory tariffs may be absorption in profit margins. Another may be that Canada’s inventory-to-sales ratio is at the highest since the early 1990s and therefore there is a lot of pre-tariff and early-tariff inventory sitting around (chart 22). Try to hike prices, and the competition will undercut you by selling down stockpiles. Another reason may be that businesses are hesitant to adjust prices until they know how permanent any tariffs may be.

In any event, the BoC’s preferred measures of core inflation—trimmed mean and weighted median CPI—exclude the effects of tariffs and other indirect taxes but not the potential indirect effects. It’s possible that the core gauges may show crowding in behind the elimination of tariffs, but that wasn’t very evident in the opposite direction when retaliatory tariffs were first introduced.

Gasoline is assumed to be a modest contribution to total CPI inflation along with shelter prices. The year-over-year inflation rate is expected to rise to 2.3% from 1.9% the prior month and mainly because of a shift in year-ago base effects. The elimination of the consumer portion of the carbon tax in early April will continue to weigh down the yearly inflation rate until next April after which it should jump when the year-ago comparisons shift to the lower price level.

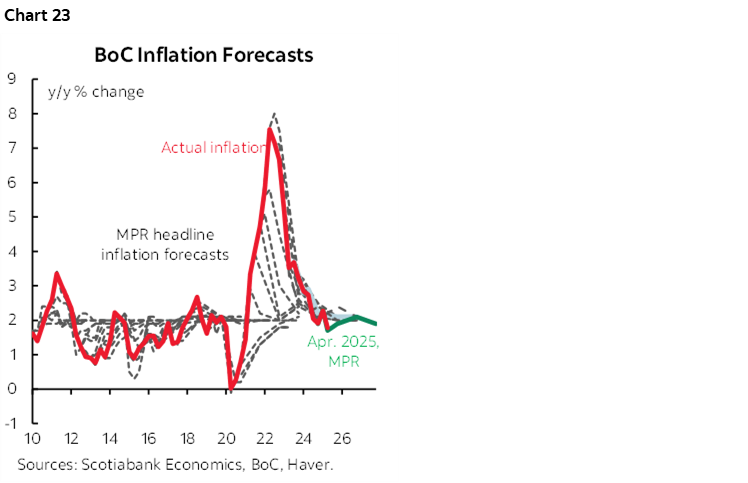

In any event, I’m no longer sure what the Bank of Canada follows when it comes to inflation. The main reason for this is that I don’t think they are sure either. There are already many measures of core inflation beyond trimmed mean, weighted median, and traditional core inflation ex-food and energy. The BoC is theorizing that maybe it could add at least two more complicated measures as part of next year’s review. More data doesn’t always drive better decisions. The message is one of policy obfuscation. When you’re not sure what to do, throw forward a lot of smoke screens. In the end, it’s not the data to date that will matter the most—it’s the judgement applied to future inflation risks that will determine whether policy is on the right track and that has not been a strong suit for the BoC (chart 23). The BoC’s MPR forecasts for inflation miss inflection points on a routine basis despite all the best models.

US CPI—MORE CONFIDENCE?

The Bureau of Labor Statistics will finally release CPI for the month of September on Friday. Despite the ongoing government shutdown, the BLS is taking the step of calling back employees to put out the numbers because of the requirement that Q3 CPI must be known for purposes of setting cost of living adjustments for benefits over the coming year.

The release will also help to inform expectations for the Fed’s preferred PCE gauges that don’t arrive until October 31st and hence after the FOMC decision on the 29th. The producer price gauges are unlikely to be released before the 29th to help complete the PCE picture unless the shutdown ends soon.

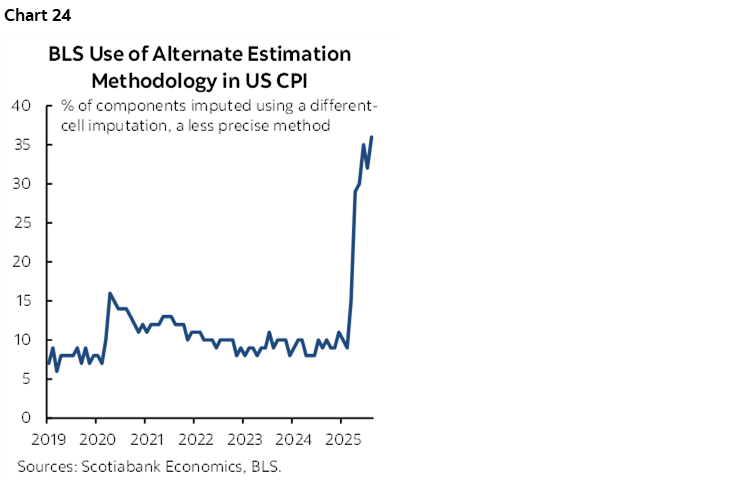

I won’t repeat earlier analysis that was provided in the prior weekly (here). Increases of 0.3% m/m SA are expected for both total CPI and core CPI excluding food and energy. The imputed share of the basket that is estimated through alternative means might stay high in light of budget cuts (chart 24).

Presumably right after the release the BLS staff will hit the exits again unless the government reopens in time.

CENTRAL BANKS—REGIONALS FILL IN FOR QUIET MAJORS

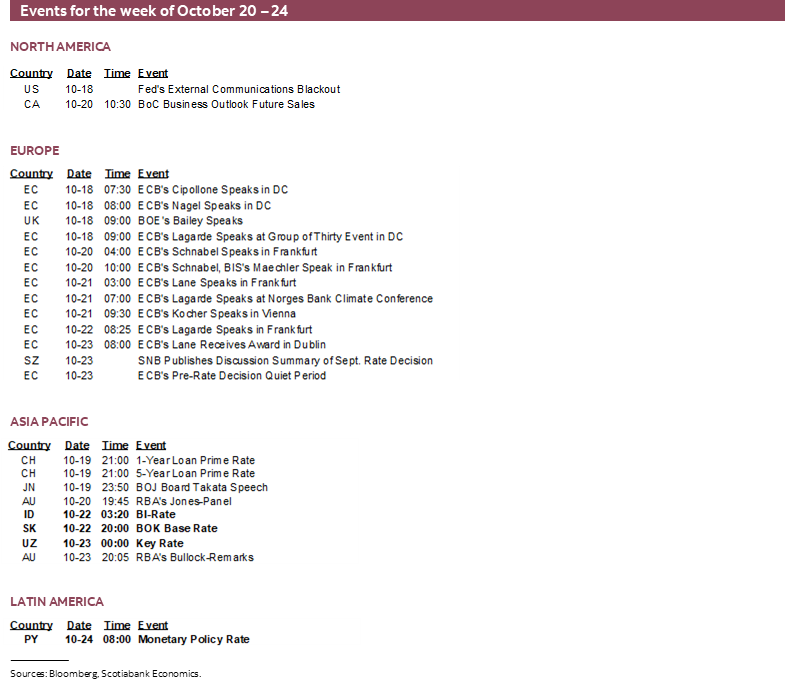

Four regional central banks will weigh in with updated decisions. The Bank of Canada enters its pre-MPR communications blackout on Tuesday ahead of the following week’s decision. The Federal Reserve will enter blackout on Saturday the 18th through to after the decision on October 29th—the same day as the BoC’s decision.

Bank Indonesia—Coin Flip

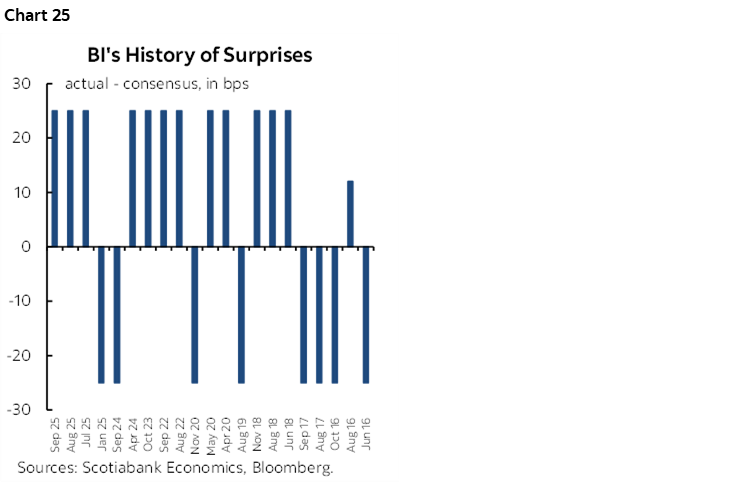

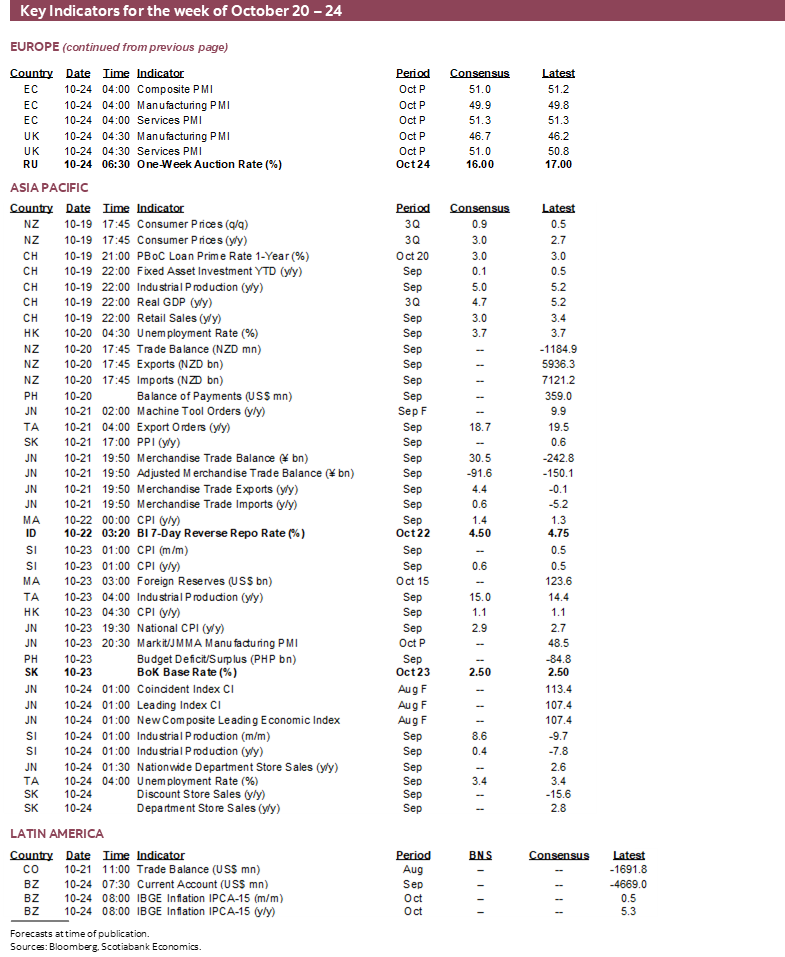

Consensus is split between a hold and a 25bps cut on Wednesday. Part of the uncertainty is because of learned helplessness. BI surprised by cutting 25bps on September 17th when no one expected it. It has a strong proclivity toward surprising, or consensus is really bad at forecasting its moves (chart 25). A dovish bias open to further easing is trading off domestic instability including political pressure on the government and protests against potential financial market instability through the effects on the rupiah. Since the September cut, the rupiah has depreciated by under 1% which is neither here nor there in the context of broad dollar strength over that period.

Bank of Korea—No Rush

Thursday’s decision has most forecasters expecting another hold at a base rate of 2.5%. BoK has been on hold since its last cut back in May. CPI is running at 2.1% y/y with core at 2.0% which is basically on target. GDP growth through to Q2 has been solid. The unemployment rate is holding around 2½% in a still-tight labour market. Political uncertainty and a weak currency that has underperformed other major crosses since the BoK’s last decision in August may keep the central bank cautious and still focused upon housing imbalances.

Central Bank of Turkey—Only the Brave

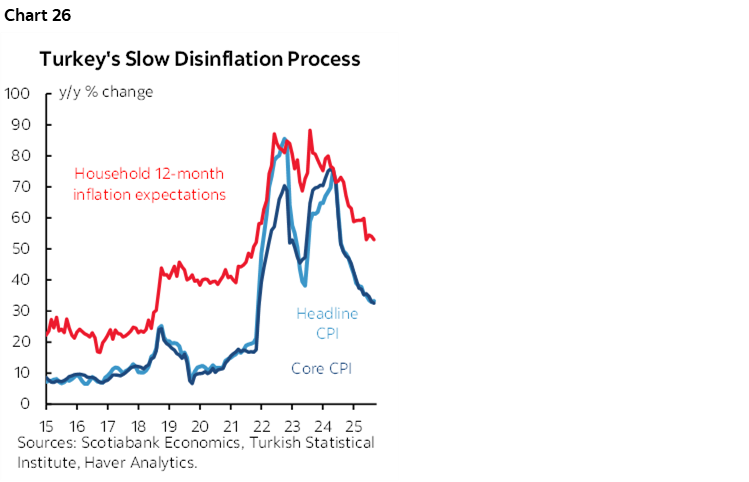

Never say never with this central bank. Its erratic history of decisions and political interference make it so that anything goes. For what it’s worth, a limited consensus has the central bank on hold on Thursday at a one-week repo rate of 40.50%. Some forecasters expect another large cut, but a smaller one than the 250bps cut in September. Governor Karahan’s remarks on inflation and inflation expectations have sounded like they lean more toward a hold while they come down but remain elevated (chart 26).

Central Bank of Russia—Less Fiscal, More Monetary?

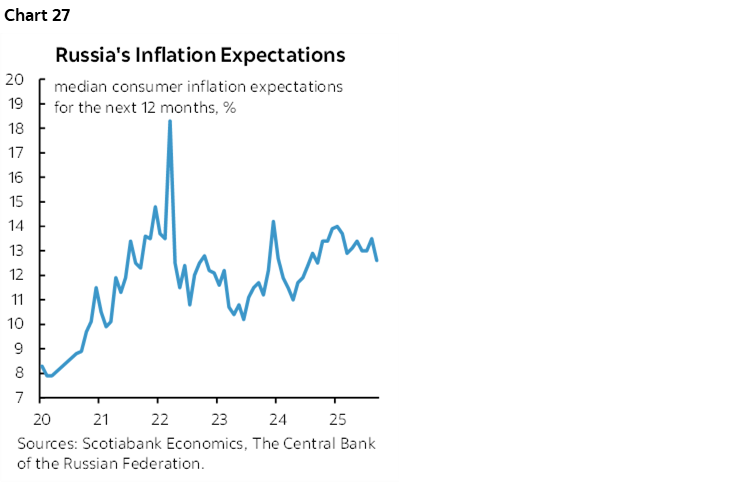

Russia’s central bank faces a difficult decision on Friday. Governor Nabiullina had said at the last decision on September 12th that a pause was considered before ultimately delivering a 100bps cut to 17% that was half of what consensus expected. Her concern was uncertainty over fiscal policy developments. Shortly after the decision, the Ministry of Finance offered refreshed guidance on a budget rule that had analysts believing the signal favoured less fiscal stimulus going forward. That could give more confidence for the Governor to deliver another sizeable cut this week on the heels of recently cooler inflation but still very elevated expectations (chart 27).

EARNINGS—THE BEAT GOES ON

Eighty-six S&P500-listed firms release earnings this week as the US Q3 earnings season broadens out. Some of the ‘Magnificent Seven’ are due out including Tesla (Wednesday) and Intel (Thursday). Other names include Tuesday’s Netflix, GM Tuesday and GE, and then Ford on Thursday.

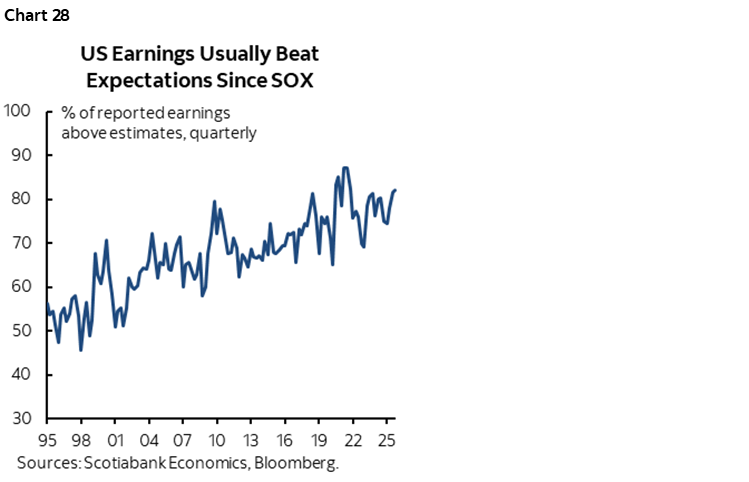

So far, 82% of US earnings have beaten analysts’ expectations which is in the ballpark of what has been typical since SOX legislation (chart 28).

Canada’s earnings season brings out 9 TSX-listed firms including names like Teck Resources, West Fraser, and Rogers.

GLOBAL MACRO—YOU WON’T MISS US GOVERNMENT DATA

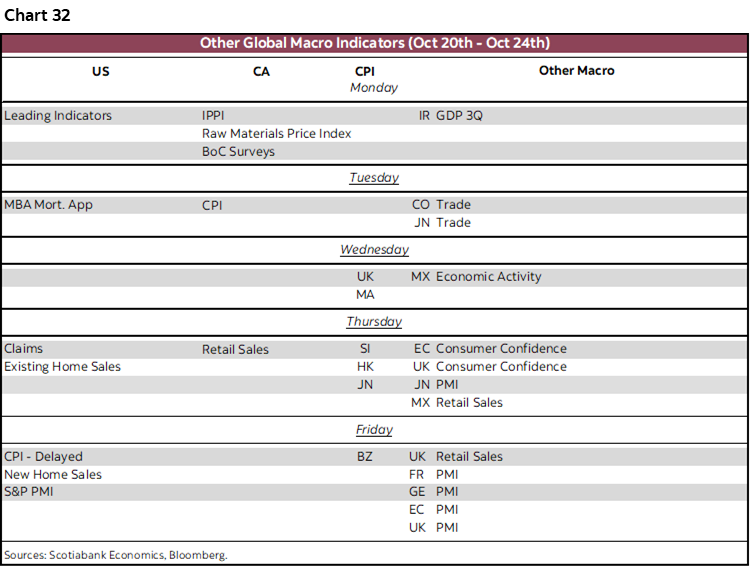

Chart 32 summarizes the rest of the expected macro readings due out over the coming week. There should be more than enough for globally minded folks to follow with the US government still shut.

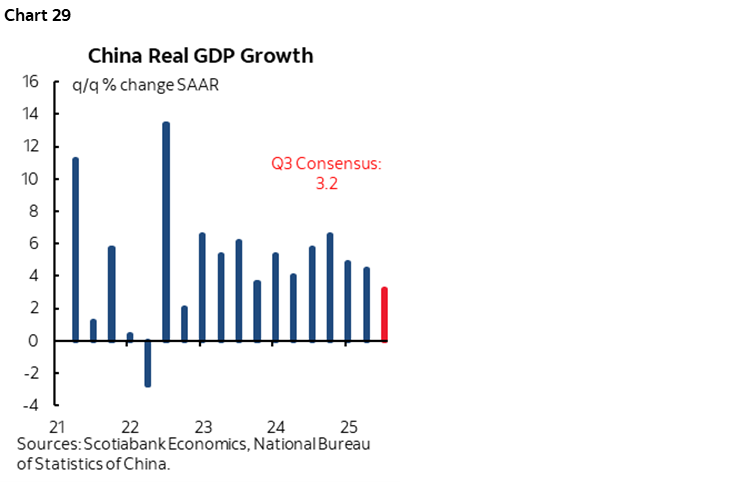

Key may be what we learn about the state of China’s economy into the Monday Asian market open. China will release Q3 GDP and monthly measures late on Sunday evening eastern time. Quarterly annualized GDP growth is widely expected to fall to something in the 3% q/q SAAR range or lower. Whether the economy posts the weakest growth since temporary periods over the past couple of years, or the weakest since the earlier stages of the pandemic period is unclear (chart 29). What will also matter will be how Q3 ends and transitions to the mathematical implications for Q4 GDP growth when we simultaneously get September readings for retail sales, industrial output, property investment, as well as new and resale home prices and the jobless rate.

Another key will be purchasing managers’ indices for October. They all arrive by the end of the week, first from Japan and Australia on Thursday evening (eastern time), then India in the early morning hours of Friday, followed by the UK, then Eurozone, and finally the US. We’ll learn much more about the state of global supply chains, hiring attitudes, input and selling price pressures, and general attitudes toward growth. It’s soft data which poses the advantage of being timely, but not necessarily indicative.

Canada should post a healthy gain of around 1% m/m SA in retail sales during August (Thursday). That’s largely based on advance guidance from Statcan, but it can be a heavily revised number. More important may be the first flash estimate for September when all we have to go by so far is that autos and gas will likely be downside influences.

US private data releases will include aforementioned PMIs but also some housing data. New home sales in September (Friday) are expected to reverse much of the prior month’s massive 20.5% m/m SA surge. Jobless claims and existing home sales would have been due out on the Thursday, but the government shutdown and lags after it eventually ends will push out their releases.

CPI readings will include ones from NZ for Q3 on Sunday as the last full set of readings before the RBNZ’s next decision on November 26th, as well as the UK (Wednesday), Japan (Thursday), Malaysia (Wednesday) and Mexico’s bi-weekly readings (Thursday). With the Bank of England on a prolonged pause that has markets not pricing a material chance at a rate cut until December or February, the main reading of interest may be Japan’s.

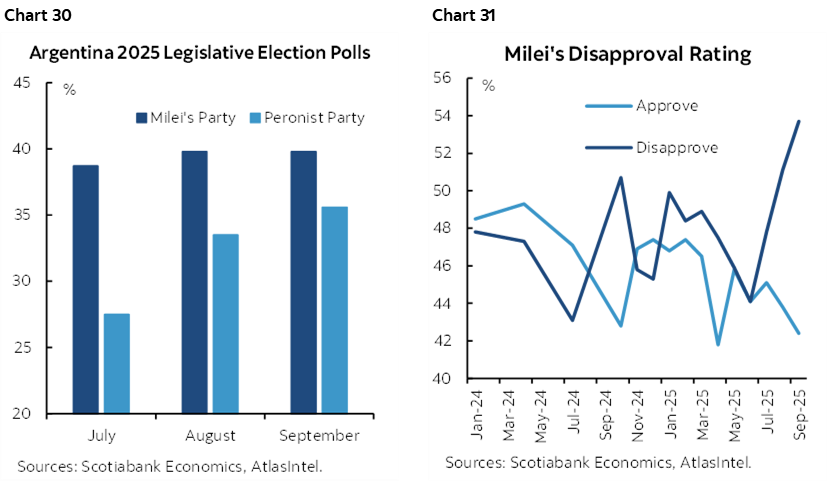

LatAm markets face light data with monthly GDP proxies due for the month of August from Colombia (Monday) and Mexico (Wednesday). Key will be that it’s the final week before Argentina goes to mid-term elections on Sunday October 26th that may determine the fate of President Milei’s attempted reforms. His approval ratings have dropped but his party has been polling ahead of the Peronists, but perhaps not by enough to have enough control (charts 30, 31).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.