Next Week's Risk Dashboard

• PMIs: Eurozone, UK, US (Markit), Australia, Japan

• CBs: Fed-speak, BoC-speak, Banxico, BanRep…

• …PBOC, SNB, SARB BoT, BSP

• Inflation: US, UK, Brazil, Tokyo, Singapore

• Three more CDN budgets

• Other macro

Chart of the Week

Global markets will continue to price an inflection point in the world economy that is bringing with it less synchronous policy developments and greater scope for differentiation across market outcomes. Evidence of this development takes the form of diverging central bank actions which is not terribly unusual to see during the nascent stages of emerging from a global crisis. The Fed, for example, has clearly telegraphed it supports steeper sovereign bond yield curves and has been both passively enabling higher yields and actively encouraging this with upbeat forecasts and through ending the Supplementary Leverage Ratio’s exclusion of Treasuries and reserves from the definition of assets against which capital must be held. The full aftermath of the SLR decision and the related move to raise reverse repo counter-party limits to US$80 billion will require time to evaluate through a coming surge in bank reserves and broad liquidity. The Fed is gradually seeking to prime markets for when the time comes to taper bond purchases. The Bank of England and Bank of Canada are generally of a similar mindset toward bond market developments. The ECB is somewhat of an outlier in fighting bond market signals, but with limited success under differing circumstances.

The coming week will further this evolution of divergent policy and macroeconomic risks. We’ll see that in growth signals provided by economic indicators like a wave of global purchasing managers’ indices We’ll also probably continue to see central banks adopt altered policy stances suited to their domestic conditions including the possibility of further tightening guidance across EM central banks that are dealing with capital outflows and resetting prices on those flows as US Treasury yields rise. Canada’s largest provinces are among the world’s heaviest borrowers as a partial reflection of the greater powers they possess compared to many other global subnational governments and they will be watched for how their budgets navigate the balance between continuing to provide nearer-term stimulus and moving toward longer-term repair.

DIVERGING ECONOMIES

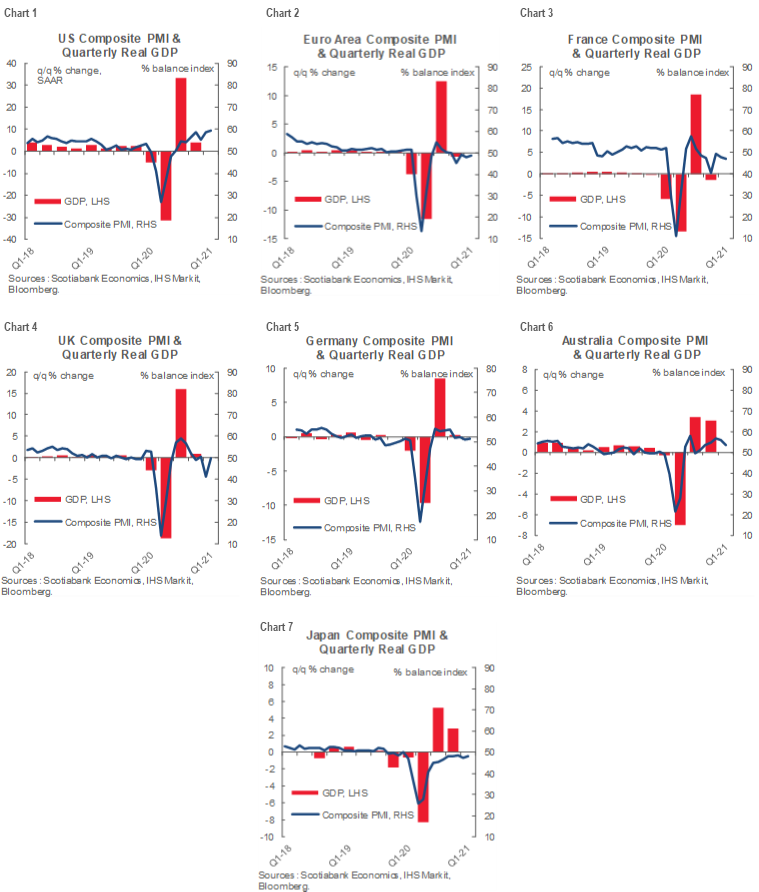

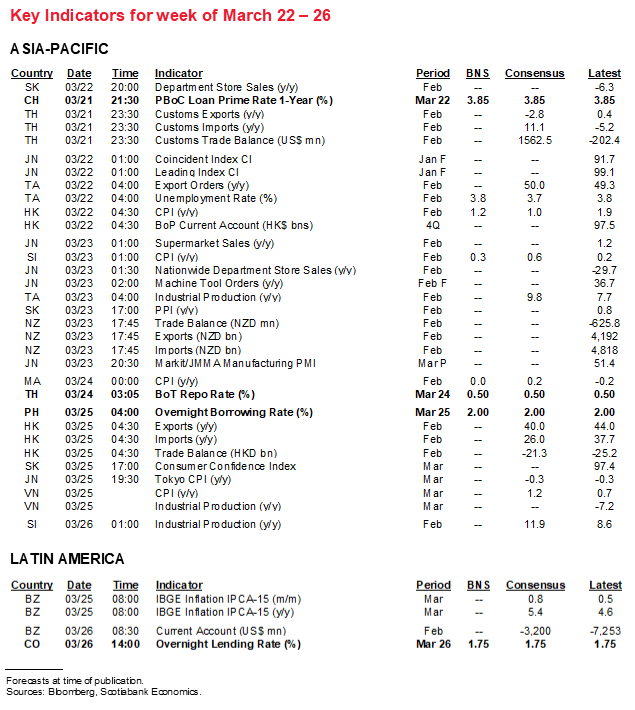

The global round of purchasing managers’ indices for March is likely to continue to showcase widely divergent growth conditions due in no small part to varying degrees of success on containing COVID-19 and administering vaccines.

In the sample of PMIs that arrive next week, it will probably remain the case that only the US and Australia are registering economic growth during the first quarter of the year and in that order by way of magnitudes. The rest of the regions have been stuck with readings below the 50 dividing line between expansion (above) and contraction (below). Charts 1–7 show the connections with GDP growth for each zone. Australia and Japan will be first up on Tuesday, followed by the PMIs out of the US, Eurozone and UK on Wednesday. The US measure will be the Markit gauge, whereas the Federal Reserve tends to place more attention upon the ISM measures mainly because they focus on the domestic operations of companies whereas the Markit measures include international operations. Note that Germany will also release sentiment gauges for consumers (Thursday) and business confidence (Friday).

CENTRAL BANKS—WHO'S NEXT?

What would a week be without more central bankers stepping up to the microphone?! Alone in the futile battle against the bond market is ECB rhetoric awaiting an evaluation of their actions, while global central bank actions are less synchronous in nature which is often the case at emerging inflection points.

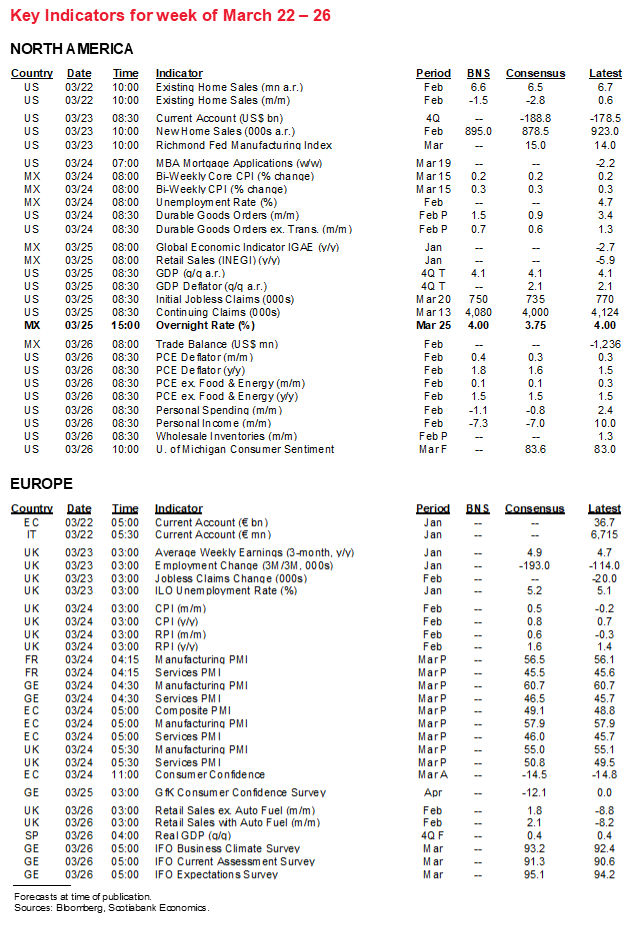

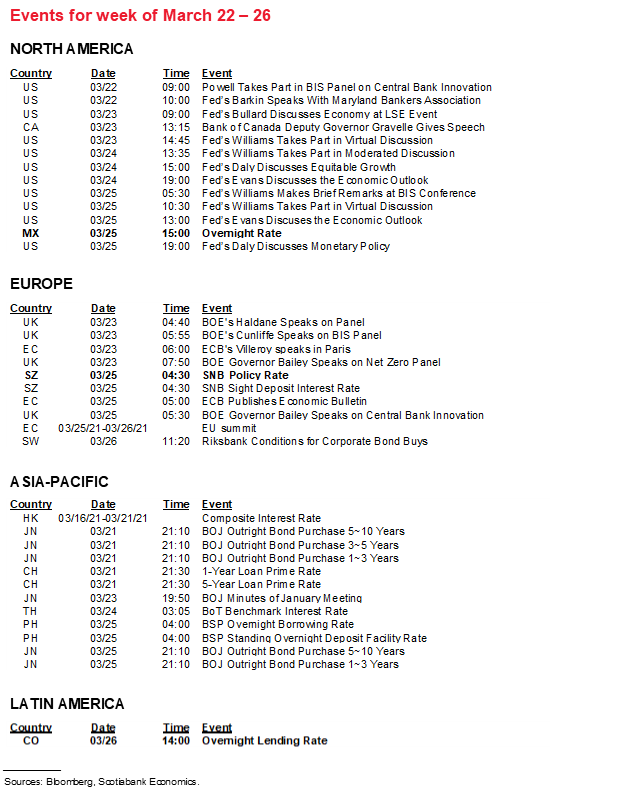

Federal Reserve: It’s not unusual for FOMC officials to beat the pavement (virtually these days) in the wake of a full FOMC meeting (recap here). This week won’t disappoint such expectations. Fed Chair Powell goes side-by-side with the person who used to have his job when Powell and Treasury Secretary Yellen deliver their required quarterly appearances during testimony before Congress on Tuesday and Wednesday. The focus is upon CARES Act implementation and effects, while remarks set in a forward-looking policy-oriented sense are likely to offer much more than what we just heard from the Fed this past week. Still, each of Vice Chairs Clarida (outlook) and Quarles (LIBOR transition) and Governors Brainard and Bowman (both outlook) will be speaking alongside several regional Presidents over the coming week. This past week saw further curve steepening in response to the Fed’s preference to get out of the way of the bond market through passively observing curve steepening that is taken as a whisper taper in advance of the actual commencement of tapering inside of a year from now with advance communication.

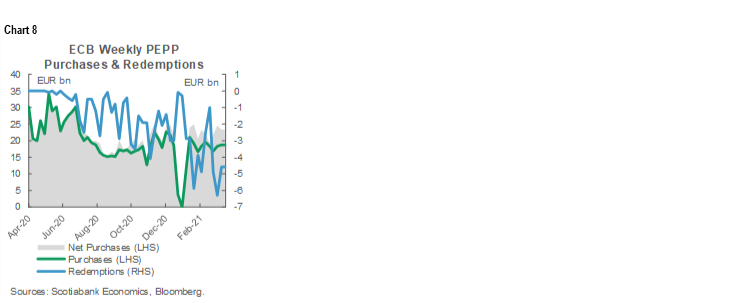

ECB: Weekly purchases are not yet at the point of requiring monitoring of how the ECB intends to implement its guidance that the Pandemic Emergency Purchase Program will “significantly” expedite EGB purchases in Q2, but Monday’s figure will still be monitored for advance signals of intentions (chart 8).

Bank of Canada: The BoC’s Toni Gravelle will also speak on Tuesday (no press) about the BoC’s role during periods of market stress and may include remarks on the status of current purchase programs, though policy guidance is not expected.

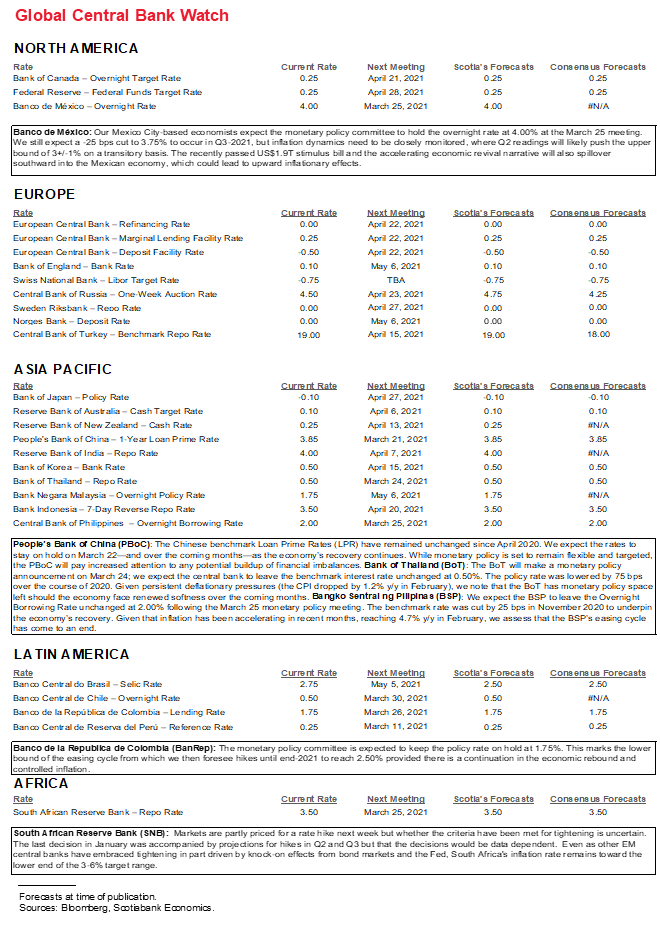

Banxico: Our Mexico City-based economists expect the monetary policy committee to hold the overnight rate at 4.0% on Thursday. At issue in guiding timing for future possible easing that is expected by many economists is the debate concerning the balance of risks to the inflation trajectory that is expected to stretch toward the upper limit of Banxico’s 2–4% target range over coming months and then subside. Then again, spillover effects from strong projected US growth, leakage effects of strong US fiscal stimulus, and expected vaccine progress could weaken the argument that inflation may prove to be transitory. Market implieds are generally of the view that the next move is up but not for a while (chart 9).

BanRep: Colombia’s central bank is widely expected to keep the policy rate on hold at 1.75% (Friday). With headline inflation at 1 ½% y/y and core inflation under 1% there is little near-term pressure to do otherwise. A tightening cycle is generally anticipated to occur over 2021H2.

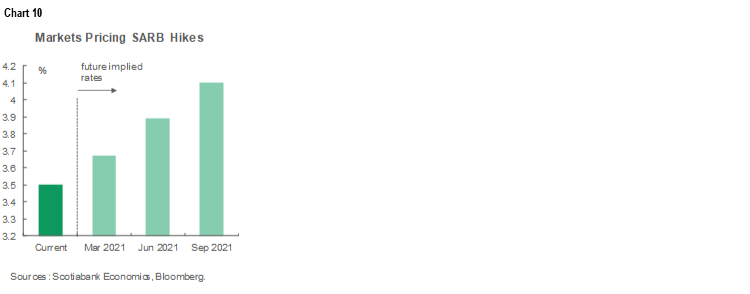

South African Reserve Bank: Markets are partly priced for a rate hike on Thursday as part of pricing in a couple of hikes this year (chart 10), but whether the criteria have been met for tightening is uncertain. The last decision in January was accompanied by projections for hikes in Q2 and Q3 but with guidance that emphasized how the decisions would be data dependent. Even though other EM central banks have embraced tightening in part driven by knock-on effects from bond markets and the Fed, South Africa's inflation rate remains toward the lower end of the 3–6% target range and the rand has not been as affected as several other EM currencies.

Swiss National Bank: The SNB is expected to leave policy unchanged on Thursday but watch for further comments on Swiss franc intervention following remarks earlier this month by SNB VP Zurbruegg that they could go further “should the situation require that.” The franc has nevertheless been moving sideways since his remarks.

The People’s Bank of China is expected to leave the 1 and 5 yr Loan Prime Rates unchanged at the start of the week. Each of the Bank of Thailand (Wednesday) and Bangko Sentral ng Pilipinas (Thursday) are expected to stay on hold.

OTHER MACRO—FOCUS ON THE US & UK

The US and UK will dominate the remainder of the global macro calendar.

There will be several US releases this week as follows.

Income/spending/inflation: February’s tallies land on Friday. Total consumer spending probably fell by about 1.1% m/m since we already know that retail sales (which carry about a 45% weight) fell by 3% m/m and we are assuming a less abrupt swing in services spending. Personal incomes probably fell by about 7.3% m/m as stimulus cheques that were received in January drop out of the February income numbers before March brings the effects of another batch of cheques. The Fed’s preferred headline PCE inflation likely accelerated to 1.8% y/y from 1.5% with PCE following the 0.4% m/m rise in CPI; base effect shifts are unlikely to be a significant driver. Core PCE likely held unchanged at 1.5% y/y and was probably up by 0.1% m/m in sync with core CPI.

Richmond: The Richmond Fed’s manufacturing measure will further inform ISM-manufacturing expectations after the very strong Philly Fed reading and the gain in the Empire reading.

Housing: Monday’s February existing home sales will probably register a modest decline of 1–2% m/m given they close 30-90 days after pending home sales that fell by 2.8% m/m in January and were up by only 0.5% in December. Tuesday’s February new home sales are expected to slip given the prior month’s large rise and softer model home foot traffic that may have been partly a function of cold, heavy snow and Texas power grid issues.

Durable goods: Wednesday’s durable goods orders are expected to post a modest rise partly on the hope that the uninterrupted streak of nine gains in core defence ex-air capital goods orders will continue.

Other: Final Q4 GDP revisions on Thursday are not expected to stray from the prior 4.1% estimate. Thursday’s weekly initial jobless claims will push right through the nonfarm reference period; despite the recent backing up, they are tracking somewhat lower in March than February which is a good sign for March payrolls.

A trio of UK macro reports will include expectations for slightly firmer headline CPI pressure during February on Wednesday, but with inflation still hovering under 1% y/y. Job growth will be updated for January the day before CPI and following the large lockdown-induced decline of 114k in December. UK retail sales close out the week on Friday and they are expected to rise following the large 8.2% drop that was also driven by the lockdown.

CANADIAN BUDGETS—CLEARING THE DECKS FOR THE FEDS

While Canada’s macro calendar will be dead quiet, three provincial government budgets will be focal points including from the two largest provinces that comprise almost 60% of the Canadian economy. Scotia’s Marc Desormeaux weighs in with his thoughts below.

While each of the provinces slated to release a budget next week faces its own unique challenges, there are common themes across the three. An improved global economic outlook since late last year bodes well for revenue growth, but changes to bottom lines will also depend on the degree of conservatism baked into economic projections and assumptions regarding the drawdown of one-time FY21 federal transfers. Bond rates and the split between short- and long-term borrowing will impact the pace of medium-term consolidation. Population growth forecasts for the post-lockdown period will provide some insight into the rate of longer-run expansion expected in each jurisdiction.

Nova Scotia has signalled that it will release its first multi-year fiscal blueprint of the pandemic era—and the first plan under new premier Iain Rankin—this week, though a specific date has not been announced. The province enters budget season with particularly strong labour market momentum. Helped by one of the lightest COVID-19 caseloads in Canada, its full-time employment sits above the year-earlier, pre-pandemic level (chart 11). Last week’s Throne Speech suggests that we will see policy focused on the environment, and continued emphasis on developing the high tech and ocean sectors.

The Ontario budget set to be tabled on Wednesday should continue to prioritize support for businesses and the health care system. Both are grappling with second pandemic wave impacts and gearing up for a possible third wave. There is some upside potential for fiscal balances. Recall that the November 2020 fiscal blueprint outlined deficit scenarios associated with various economic growth trajectories. Our latest forecast calls for a 6–6.5% expansion this year—in line with the private-sector mean—not quite the rate in the “high growth” scenario but still suggestive of smaller shortfalls in the coming years (chart 12).

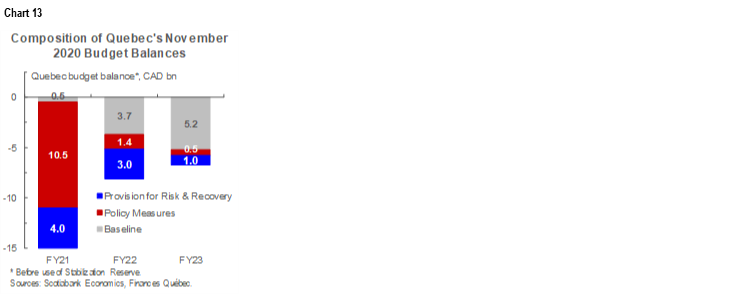

Quebec’s economic outlook has also improved, but we suspect that the province will continue to build significant prudence into its fiscal plan. To head off unexpected pandemic-related costs, its November fiscal update incorporated contingencies of $4 bn, $3 bn, and $1 bn in FY21, FY22, and FY23, respectively (chart 13). Still, Quebec’s torrid 61% q/q annualized gain in Q3 of last year—more than 20 ppts stronger than that for Canada as a whole—can reasonably be expected to provide a stronger revenue handoff into 2021.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.