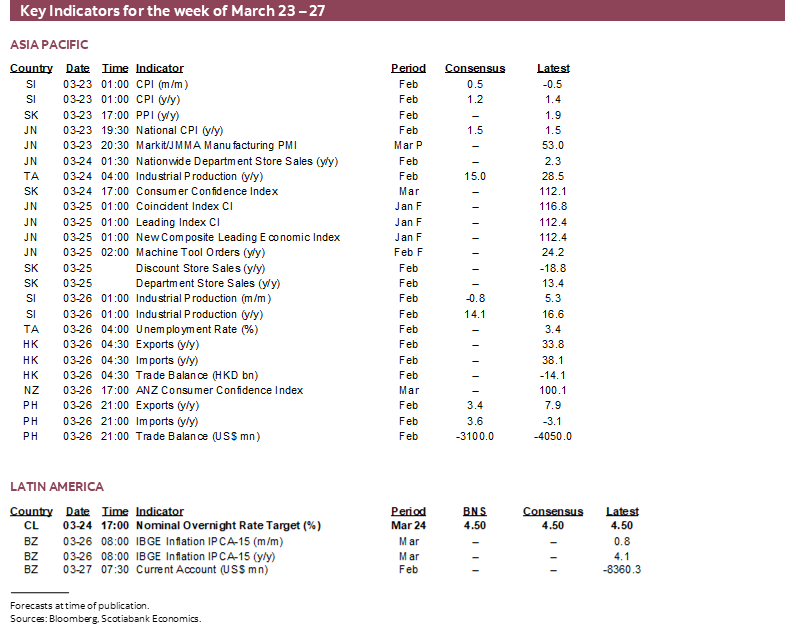

Next Week's Risk Dashboard

- Iran risks could escalate into next week

- Inflation risk is spreading with more to come

- How central banks should manage inflation risk more wisely this time

- Rewriting the narrative at commodity-driven central banks…

- …as BCCh gets squeezed on copper and oil…

- …Banxico’s hawks might get a boost within a divided consensus…

- …Norges may abandon prior guidance…

- …and SARB faces unmoored inflation expectations

- Global PMIs to offer a first glimpse of the oil shock’s effects

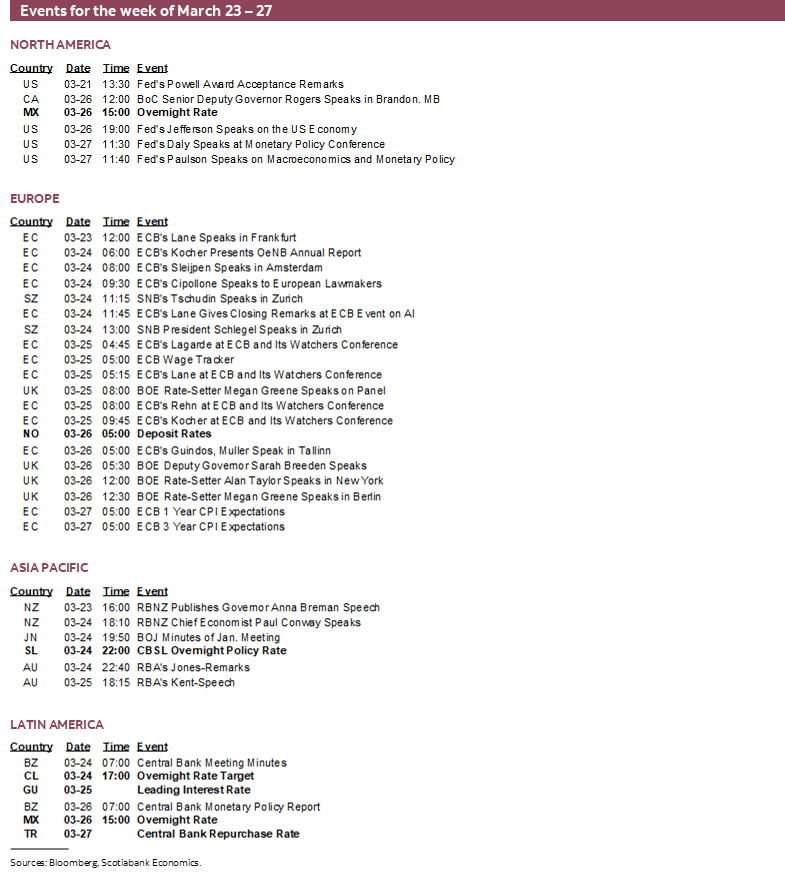

- BoC’s Rogers to weigh in on the outlook

- Spain will be the first to offer a glimpse at March inflation

- Danes head to the polls

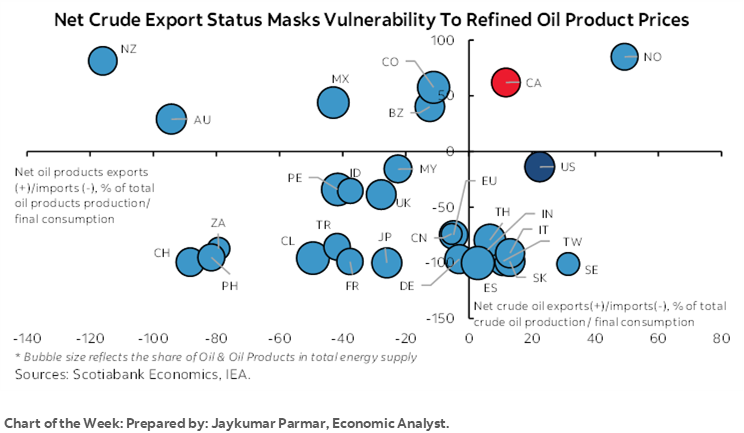

Chart of the Week

The key question now lurking in global financial markets is the extent to which widespread inflationary pressures may reemerge and how central banks may respond. Many of them should avoid making the same mistake they made by dithering around the last time. That’s especially so amid signs the war may intensify despite —or because of, if they’re seeking to lower the enemy’s guard—the administration’s words as more marines are being sent, Kharg Island appears to be in their sights, and Iran’s reaction could add to escalation risk. Enriched uranium stockpiles and scientists have yet to be secured which leaves the aims incomplete while leaving behind a potentially even more destabilized region amid long-term damage to energy infrastructure.

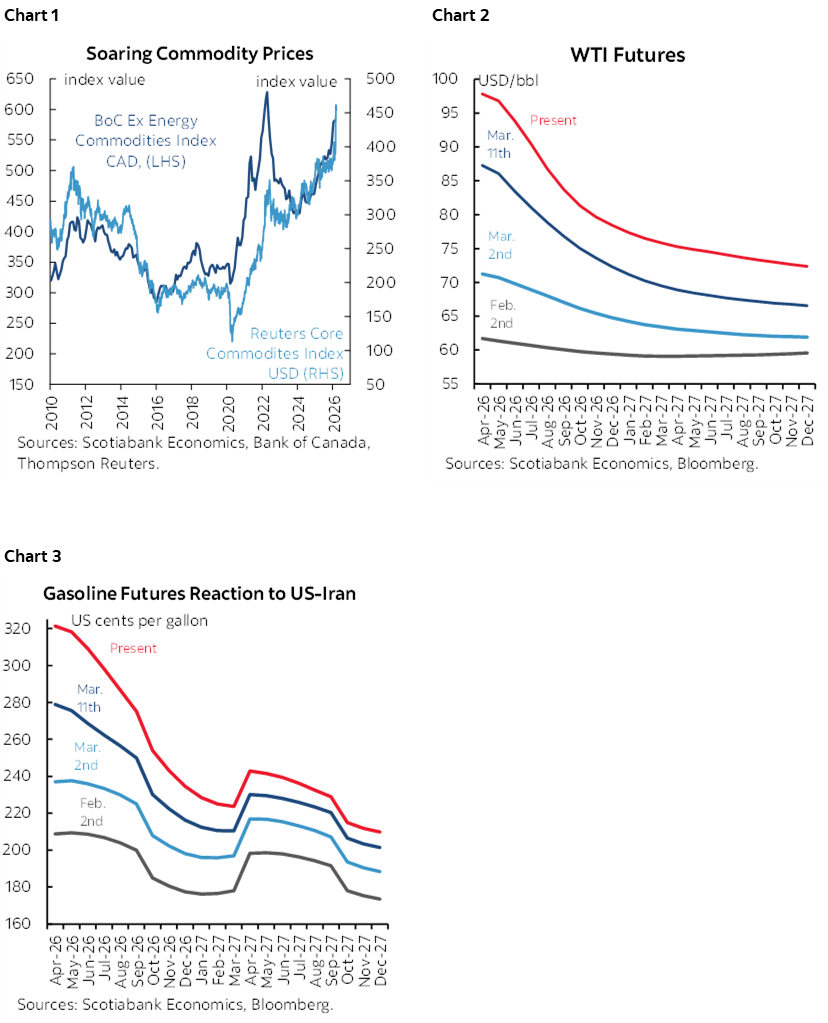

The inflation surge is already here but with consequences that may vary by market. Broadening inflationary pressures are being understated as they reach beyond energy markets (charts 1–3).

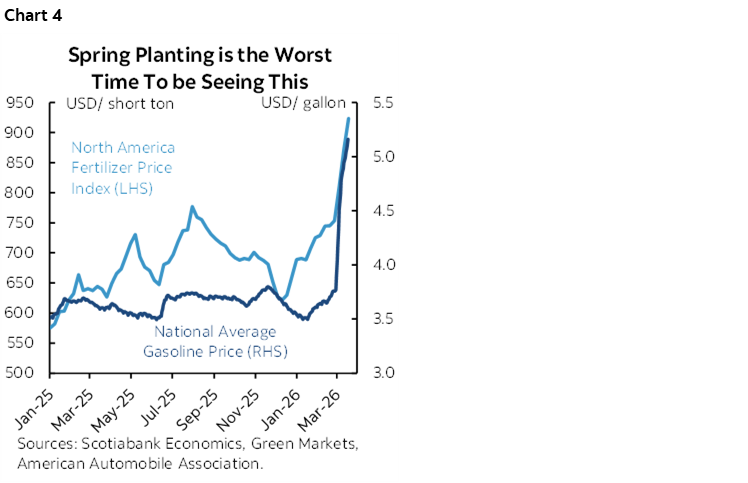

Food prices are on the verge of breaking out once more. Grocery prices are bound to become more of a headache for consumers, suppliers and governments. Two reasons for this are shown in chart 4. Input cost shocks to the agricultural sector are happening at the worst moment in the northern hemisphere as Spring planting season arrives. Fertilizer prices have risen by about two-thirds since the start of last year and are about 40% higher ytd. This is because the Iran war has restricted nitrogen and phosphorous exports through the Strait of Hormuz while higher energy costs are impacting shipping and mining. Diesel prices are up by about 50% since the start of the year.

The war would have to settle down awfully fast in order to avoid sharply rising pass through to retail groceries throughout the next year or beyond. Farming is often a tight margin business dealing with perishable inventory. Perishable food industries gave less ability to absorb surging input costs in profit margins and by smoothing inventories than other sectors.

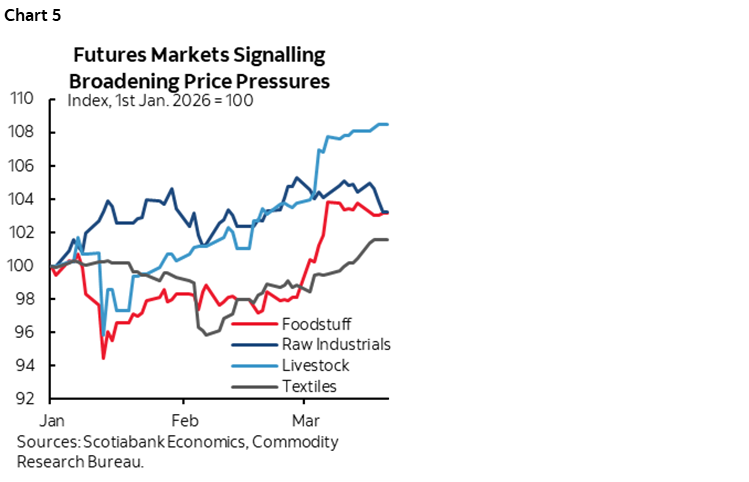

Some spillover effects of higher energy and food costs are already arising (chart 5). Food and livestock futures prices are rising and if input costs stay high then greater pass through is possible. Textiles futures prices are rising perhaps in part due to transportation costs.

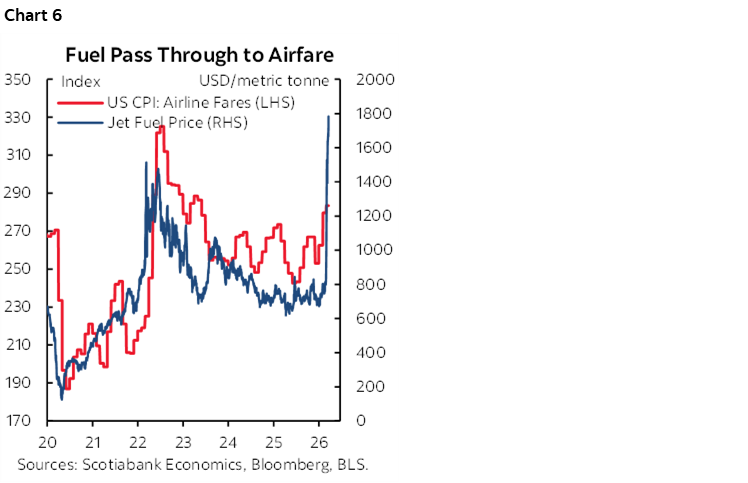

Soaring jet fuel is rising to levels unseen even in the pandemic which, given lags, has only just begun to show up in airfare (chart 6). This is already sparking guidance from airlines to brace for fare hikes and flight cancellations due to fuel shortages.

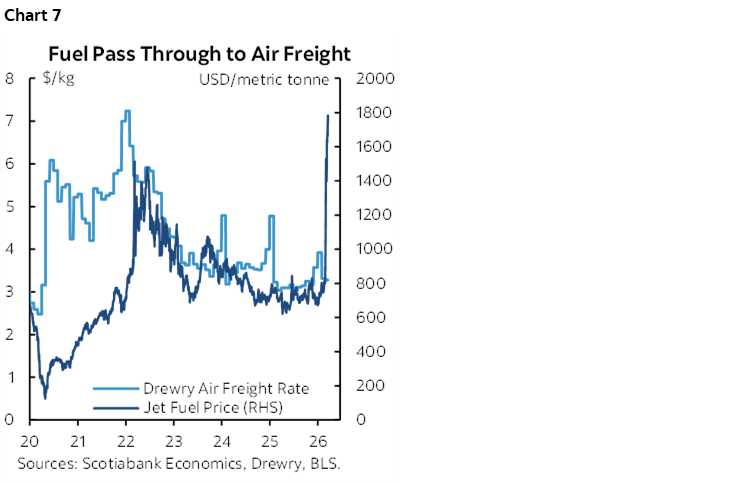

Commercial air freight costs are bound to experience the same outcome (chart 7). Expect the same for other modes of transportation—a mixture of higher prices and supply curtailment that will impact other sectors.

Central banks focus more closely upon core inflation that excludes volatile food and energy and other core measures. The key here is whether pass through of higher energy and food prices will show up in wage expectations, broader prices and inflation expectations that feed upon themselves in order to cause a cycle of inflationary pressures. There is a lot of uncertainty around this, but I would brace for core measures surging very soon. It’s nearly impossible to imagine that many businesses will not be passing on higher costs. Multiple studies showed pass through of US tariffs into US prices, so why not pass through the commodity, insurance and transportation surges?

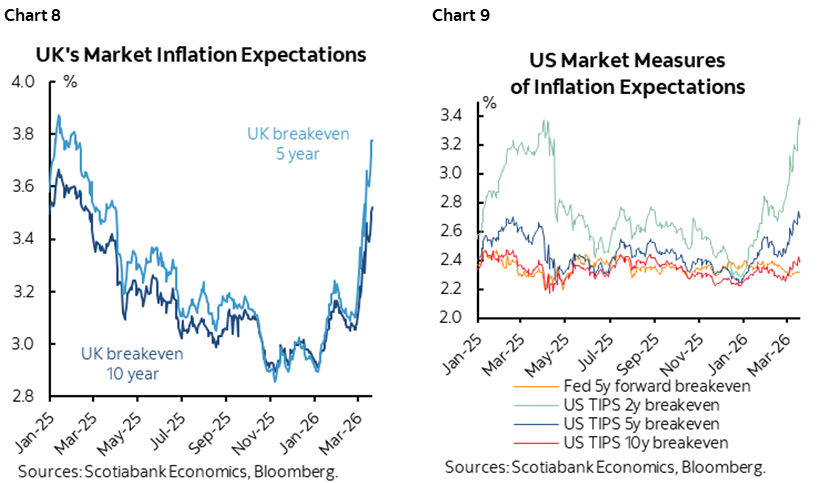

There is mixed evidence on inflation expectations. Where inflation expectations are rising in the most pronounced ways are in the UK that had a pre-existing inflation problem that is getting shocked further (chart 8), and across multiple emerging markets that are highly dependent upon imported food and energy and faced with weakening currencies. US measures have picked up, but so far not alarmingly so (chart 9). Canadian measures are very poor quality as market measures are unreliable while survey measures are constantly playing catch-up as the BoC’s April surveys will be stale on arrival.

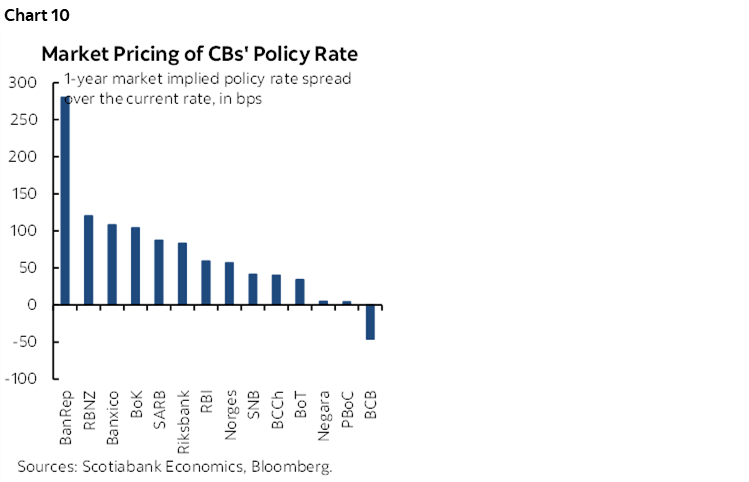

How should central banks respond? Chart 10 shows market thinking around this issue. They’re pushing central banks that are now in the awkward position of having to contemplate pushing back against hike pricing and thus easing more restrictive financial conditions in the face of an inflationary shock. They should not rely upon tighter financial conditions doing their work for them since that in turn is dependent upon monetary policy actually tightening.

They should not make the same mistake as last time. The Fed and the BoC among others looked through all signs of inflation coming out of the depths of the pandemic and emphasized pushing the frontiers of fully inclusive, maximum employment. By the time they caught onto the evidence on inflation it was too late. Being too late meant hiking more than may have been necessary with an earlier and more gradual risk management approach to the uncertainty. Waiting until they have firm data in hand that input costs are driving core inflation readings much higher risks making it too late for them all over again and into what is emerging to be another supply squeeze and hoarding activity.

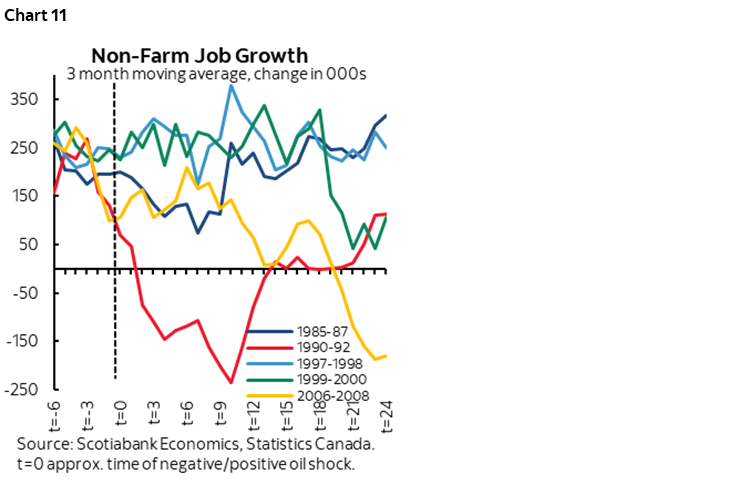

The Federal Reserve may be able to take more time in assessing the right direction of movement because it is already in mildly restrictive territory on the policy rate and the measures of inflation expectations they follow tend to be contained. Further, the Fed’s dual mandate is likely to face downside risk on the employment side given what happened to payrolls in past oil shocks (chart 11).

As for the Bank of Canada, they must not repeat the same mistakes of the pandemic. Their policy rate is likely to be pushing further negative in real terms, effectively adding stimulus in an inflationary shock in a marked distinction from the Fed. The BoC has a purer inflation target. Fiscal policy additions to growth are more direct and likely to grow in future. Trade uncertainty poses bidirectional risks and I just can’t fathom a major trade shock on top of an energy shock into the US midterms without the GOP being utterly destroyed on November 7th. There is a bit of time to judge, but don’t assume that you have a lot.

Don’t wait until you have a clear answer on how long the conflict will endure and how far it will reach. Don’t wait until you’re staring straight in the whites of the eyes of another inflation shock. Don’t wait until it’s fully evident in headline and core inflation readings. If—and emphasis upon if—this is a durable energy shock for a commodity-dependent economy and the oil futures curve is anywhere close to being correct over 2026–27, then deal with the uncertainty by staggering the policy rate adjustments. There is still time ahead of the next 2–3 meetings, but if energy markets don’t abruptly cool off, then we should all be open-minded toward insurance hikes, over waiting until its lights out. Get control of the bond market in terms of the belly and long-end parts of the term structure.

My worry about Governor Macklem is that he waits and waits and waits and then we’re back in another devastating inflation problem with political consequences. Insurance hikes leave open the door to stop and/or reverse if needed while also leaving open the door toward doing more while lessening the risk of a massive catch-up overshoot on the policy rate like the last time when moving too late meant going from 0.25% to 5%. Insurance hikes don’t put all of your eggs in one basket in hoping for an ultimately peachy outcome. That, in my opinion, would be the bigger sin if repeated by the BoC.

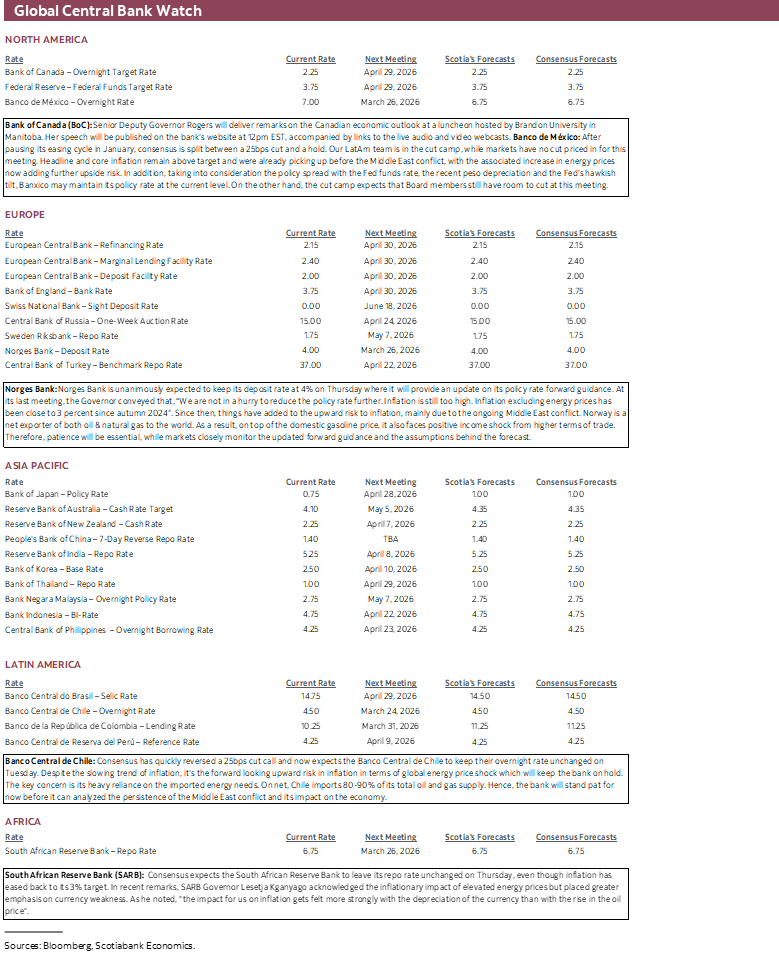

CENTRAL BANKS—REWRITING THE NARRATIVE AT COMMODITY-SENSITIVE CENTRAL BANKS

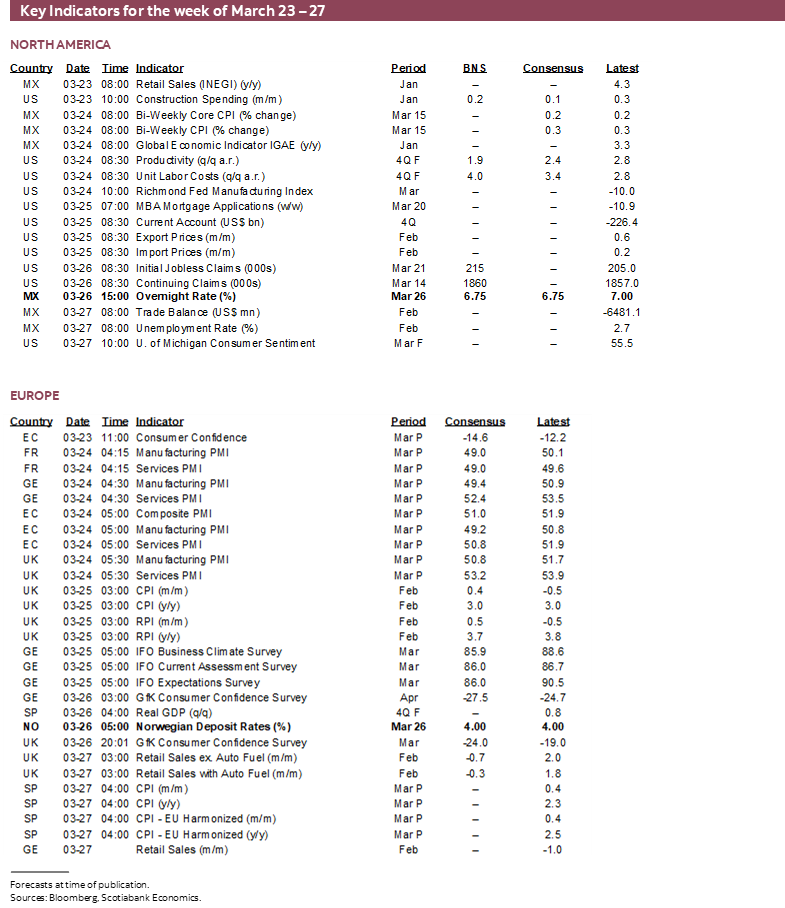

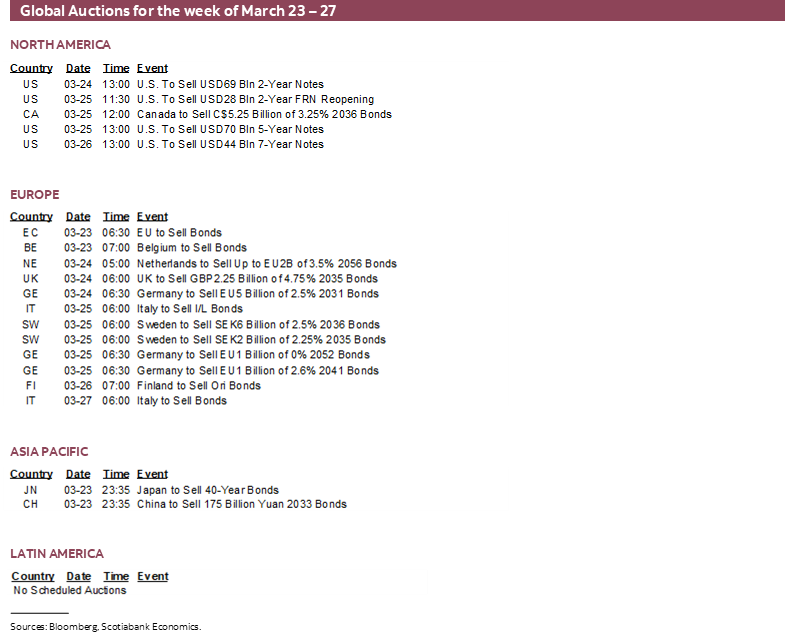

Four more central banks will weigh in with decisions this week following the fourteen who updated their views over the past week. None are expected to change their current policies, but the bias may be key. They are all commodity sensitive central banks and so their guidance could further inform policy attitudes across other commodity sensitive central banks.

There will also be a speech on the economic outlook provided by BoC SDG Rogers on Thursday. Market risk may be low given recent BoC communications (recap here) and ahead of next month’s Spring fiscal update from the Federal government and the Bank of Canada’s next decision on April 29th including fresh forecasts.

BCCh—A Double Whammy on the Terms of Trade

Chile’s central bank will be first out of the gates with its decision on Tuesday (5pmET).

Markets and consensus expect the overnight rate to remain at 4.5% in an extension of the on-hold narrative since cutting in December. The quandary facing the central bank is achievement of its inflation goals—which may merit easing—in the face of rising upside risk to future inflation. BCCh may elect to take its time in assessing conditions.

BCCh had forecast in December that CPI would land on its 3% objective in 2026Q1. This happened sooner than expected as the latest reading for February fell back to 2.4%. CPI excluding volatile items is running at 3.4% and so the central bank can claim to be broadly on track.

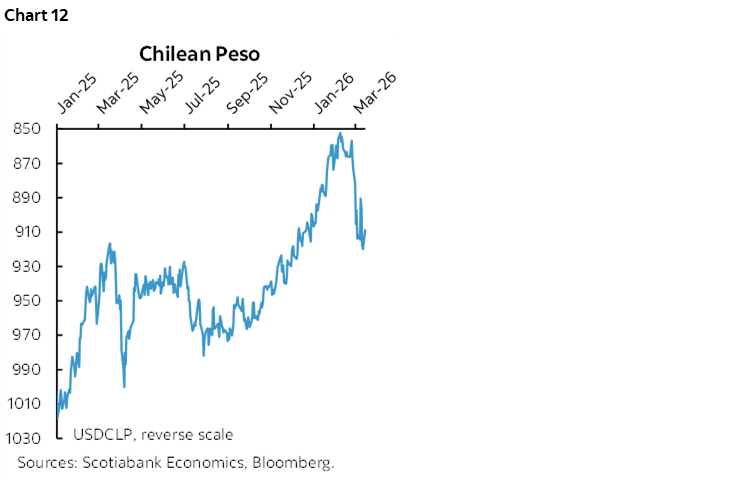

Still, copper prices are dropping back to where they were at year-end which means less money coming into the country while oil prices are rising which means more money leaving given the country’s net oil importer status (here). The combined terms of trade effects imply a squeeze on incomes.

Further, the 6% depreciation of the peso since February 25th adds some upside risk to imported inflation (chart 12).

Norges—Course Correction?

Norway’s central bank is expected to stay on hold at a deposit rate of 4% on Thursday. What it does on the bias could be instructive to other central banks in commodity exporting countries.

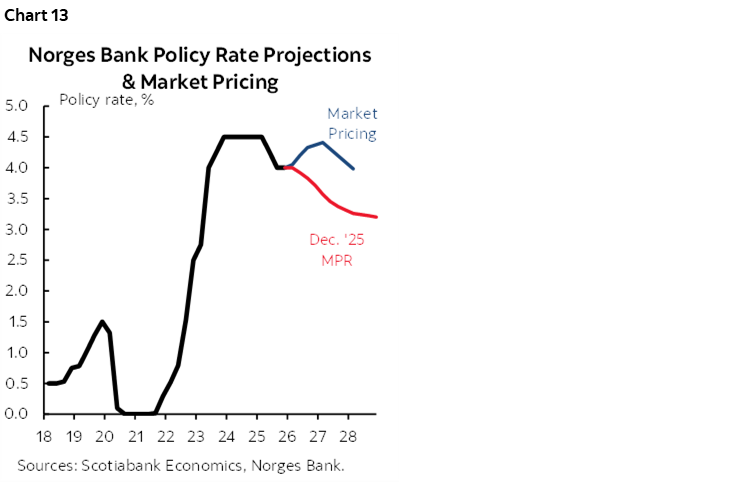

Key, however, is whether the central bank’s prior guidance in January will be rewritten in fresh forecasts and forward guidance. Recall that on January 21st, Norges Bank guided that “if the economy evolves broadly as currently envisaged, the policy rate will be reduced further in the course of the year.”

Granted, even that guidance was cautious in nature as Governor Ida Wolden Bache stated “We are not in a hurry to reduce the policy rate further. Inflation is still too high.” Soon after saying so, mind you, inflation tumbling from 3.6% y/y to 2.7% and underlying CPI inflation slipped to 3% (3.4% previously).

Enter the oil shock and Norway’s status as a significant net energy exporter. Markets are pricing most of one quarter point hike by summer. This shouldn’t necessarily surprise, given the connection between Brent and the deposit rate over time albeit with often lagging adjustments that may make nearer term tightening premature (chart 13).

SARB—Unmoored

South Africa’s central bank is expected to stay on hold at a repo rate of 6.75% on Thursday. It has been cutting the policy rate since September 2024 and now faces market pressure to pivot toward tightening policy by the second half of the year.

At 3% y/y, headline inflation’s continued descent into February might be construed as providing room for policy easing. That’s unlikely as backward data is put on the backburner in the face of forward-looking risks.

South Africa is dependent upon energy imports (here). The rand has been among the worst currency performers in the world, having lost about 6% of its value to the dollar since late January. The combination of higher oil prices and a falling currency adds to imported inflation risk.

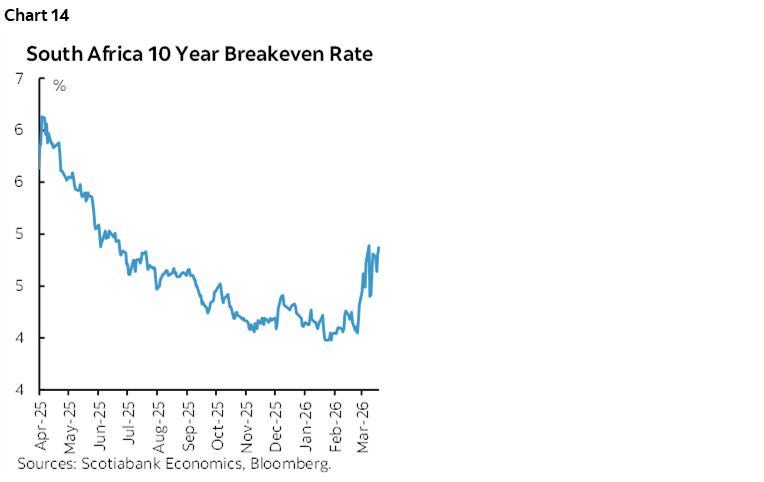

That hasn’t exactly gone unnoticed by markets. Longer term inflation expectations have been rising sharply (chart 14). SARB is sure to take note, putting in place either the risk of a hike and/or hawkish forward guidance.

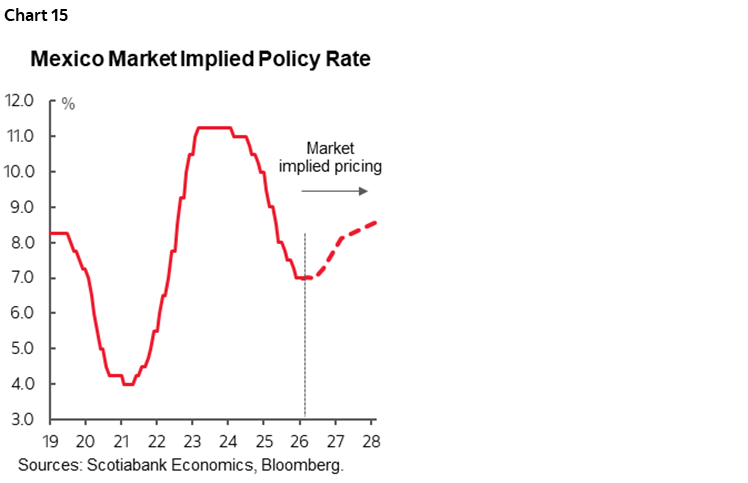

Banxico—Energy Shock May Further Embolden the Hawks

When Mexico’s central bank last weighed in on February 6th, they paused the easing cycle because Governing Council was concerned about ongoing inflation risk. The easing campaign before that meeting was dividing members who pivoted toward full agreement to halt cuts.

You might think they would be hesitant to restart it now. Hawks like Deputy Governor Heath—who was previously warning and dissenting against easing—have already weighed in. He said about a week ago that “I think we should have paused in March, and now, taking into account a more complex scenario due to the armed conflict in the Middle East, even more so.”

The further unmooring of market-based measures of inflation expectations is bound to be of concern to Banxico and to markets that are pricing the next moves to be upward as soon as later in the year (chart 15).

Yet consensus is split between a cut and a hold.

GLOBAL MACRO—DANES VOTE, PMIS IN FOCUS

The Danish general election will determine who squares off against Trump if and when his attention returns to demanding Greenland, while the macro release line-up contains a few gems.

Denmark’s General Election—Same Leader, Different Coalition?

Danes go to the polls in a general election on Tuesday. PM Mette Frederiksen is enjoying a bit of a wind in her sails brought on by President Trump’s demands to take Greenland. She has also pivoted further left with her policies including a proposed 0.5% wealth tax. Her Social Democrats party is polling ahead of others, but attempts at modelling coalitions suggest that the existing one between the Social Democrats, Venstre and Moderates may not survive (here).

PMIs—Soft Data to Inform Early Reactions to the War with Iran

The global line-up of other macro risks is looking pretty light over the coming week. Purchasing managers’ indices will feature prominently toward the end of the week.

PMIs are useful as soft data guides to momentum in the global economy. They provide details like growth in new orders, order backlogs, inventories, prices, and hiring intentions. Since they are survey-based they can be sentiment driven, but their timeliness often provides an early reading on how the economy is holding up in the face of fresh shocks like, well, now.

Before the war, most of the PMIs were signalling moderate growth with above-50 readings except for France. India was the strongest growing performer but is well off its growth peak of last August.

Australian and Japan kick it off on Monday evening and then through the overnight into Tuesday each of the Eurozone, Germany, France, the UK, India and eventually the US will release.

Other Releases

Among the few inflation readings watch Spain’s the closest (Friday). That’s because it will start the round of Eurozone readings for March that will extend into the following week. Markets will be watching for early signs of the extent to which energy prices lift total inflation and whether there are very early signs of pass through into core inflation ex-food and energy.

February inflation readings from Japan (Monday), Australia (Tuesday) and the UK (Wednesday) just won’t cut it by way of much market focus in light of forward-looking risks.

The same lack of freshness might have markets looking through Friday’s UK retail sales figures, although the prior month’s 2% jump in sales ex-fuel will be a tough act to follow. Subsequent reports will inform how consumers are reacting to the surge in energy prices.

Ditto if we get German retail sales for February at the end of the week or the following week, plus Mexican retail sales but in this case for back in January (Monday) just ahead of the GDP proxy for January the next day.

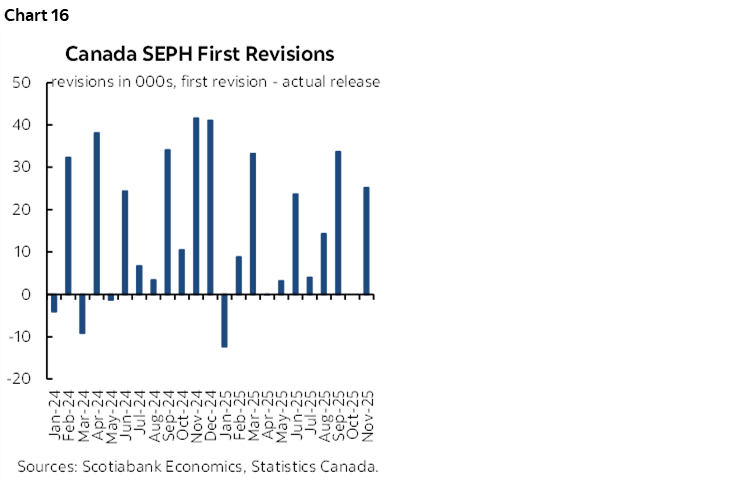

Canada only refreshes the payrolls survey for January. It lags. It’s incomplete because it doesn’t include jobs off formal payrolls that are important in Canada given the size of the small business sector. And it’s frequently and heavily revised on first pass (chart 16) and final estimates. Can’t wait.

Other US macro readings will include construction spending during January (Monday), the weekly ADP private payrolls measure into the first part of March with the prior report leaning toward the monthly gauge being up by around 40k when it arrives later. Import prices for February (Wednesday) will be worth watching because of expected heat, but the next month’s reading will more fully capture commodity influences.

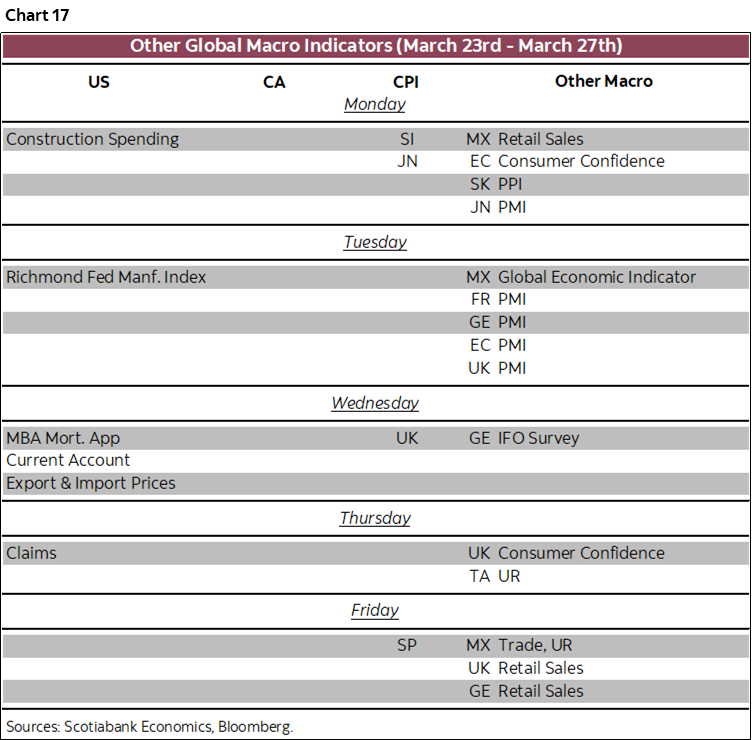

Chart 17 summarizes the line-up.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.