Next Week's Risk Dashboard

- Nonfarm payrolls preview — Aye Aye AI!

- AI & economics — a nonfarm illustration

- Canadian jobs preview — Set low expectations

- Overall state of the Canadian and US job markets

- More tariff threats

- RBA — unfinished business

- BoC testimony may provide further insights

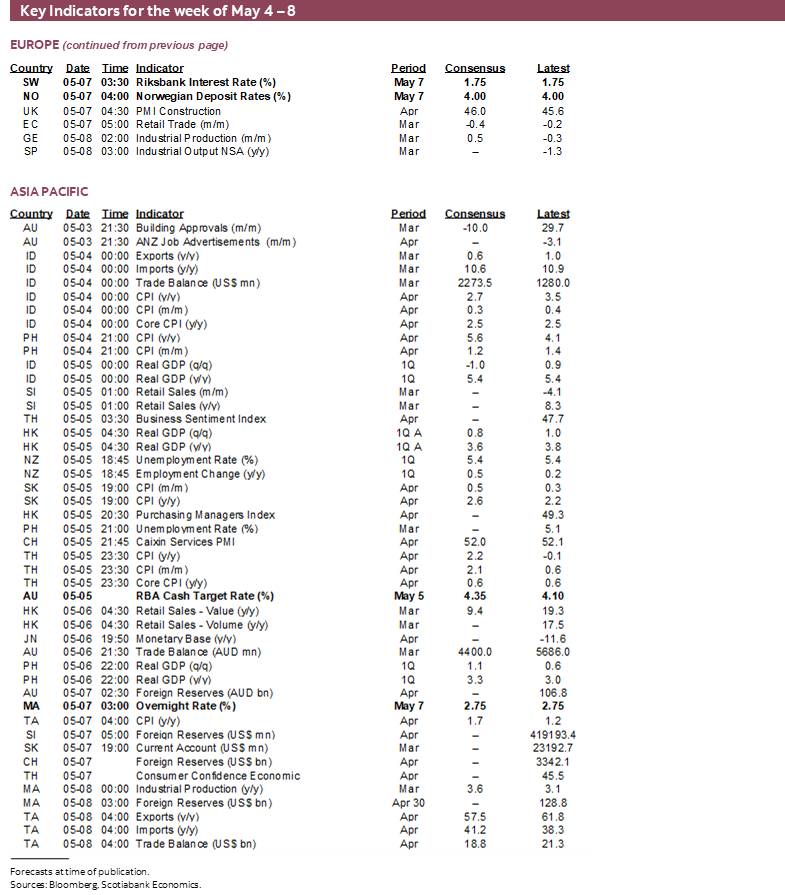

- Norges Bank — Soaring oil Vs. restrictive stance

- Negara — Taxes and debt or rate hikes?

- Riksbank — Up or Down? Yes.

- Banxico — The last dance?

- BanRep — After the shock

- Global macro: Eurozone wages, NZ jobs, LatAm & Asia-Pacific CPI

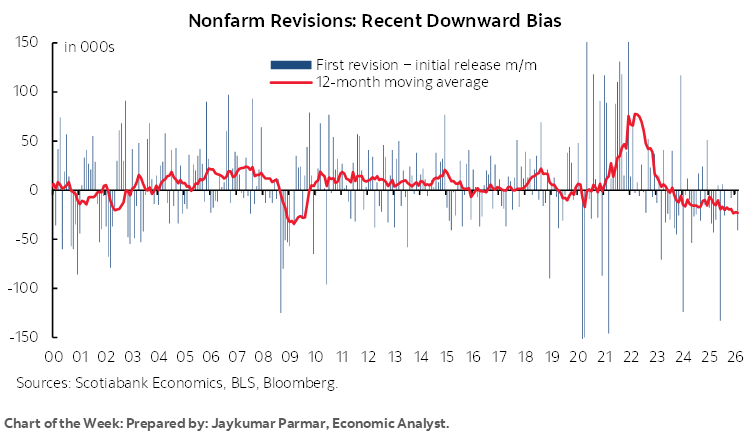

Chart of the Week

Several risks could come to a head over the coming week across most areas of interest to markets. It’s unclear how it may all net out.

Earnings will continue to figure prominently. Another 126 S&P-listed firms will release in the US, plus 91 TSX-listed firms, and a wave of foreign earnings reports. So far, they’ve been supportive as the S&P has pushed to an all-time index high with 81% of 315 firms that have released thus far beating EPS expectations and 72% have beaten sales expectations. This is always a tango between underlying strength and more conservative analysts since SOX.

Top shelf data risk will be pronounced especially on Friday when nonfarm payrolls land. This could be a soft one ahead of potentially wild distortions over subsequent months. A full preview is provided along with a take on the overall state of the US job market.

Canada releases its job figures at the same time as nonfarm payrolls and may be the less-watched sibling. This one may also be on the soft side, with a full preview and state of the job market north of the border offered in what follows.

And while the key figures of central banking are out of the way now, not to be neglected will be a bevy of still notable ones to watch. Five in total. Norges may hike. Banxico may cut. Further insights from the BoC will be provided. The three may not march on in unison despite sharing oil in common in part because of varying policy stances going into the commodity shock. Net energy importers like Australia will probably hike while Sweden can’t make up its mind and perhaps wishes it had its neighbour’s problem.

Tariffs are also back alongside threatened troop withdrawals as US-European relations worsen. Trump has threatened 25% tariffs against European autos as he alleges Europe is failing to fully live up to its trade deal. There is no order yet. His pattern is to back down. It may be either a negotiating or diversionary tactic. Europe may be more inclined to retaliate this time if Trump carries through on his threat. Europe would perhaps be well advised to show more of a spine this time. Trump’s 5,000 troop removal order is retaliation for what Merz said about Trump’s handling of Iran. Stress is clearly not in short supply in the White House.

And speaking of diversions, talks between the US and Iran appear to remain in a total stalemate with Trump—in his usual subtle ways—threatening to “blast the hell out of them” should Iran not meet his terms, while Iran threatens to counter. I have a hard time believing Trump and the GOP will wish to see further tariffs passing through to American consumers and businesses as gasoline probably continues to climb through the summer driving season as supply shocks have yet to fully hit US shores. How about US$6–7/gallon?

NONFARM PAYROLLS—AYE AYE AI!

Will nonfarm payrolls matter to the FOMC? There is a high bar set against arguing that it will matter at this point given the dominant focus upon the price stability half of the dual mandate. Still, it could be impactful to markets—especially if my estimate is in the right ballpark.

I went with a gain of only 10k payroll jobs in April. The unemployment rate is projected to dip to 4.2%. After 178k payroll positions were created in March, a near-donut with more downside than upside risk to the call could restore a little more balance in fed funds policy rate pricing that doesn’t presently think the FOMC will cut until year 2200, give or take.

Before getting into the weeds on the calls, on a lark I asked ChatGPT to write a nonfarm payrolls preview for me. It was partly for entertainment, partly out of morbid curiosity to see what the jobs of economists are up against. Check it out in the accompanying box 1 where I pasted what I asked and what it spat out in about 2 seconds flat.

Suffice if to say that I’m not so worried. It told me weather was a drag on jobs in March especially in construction and leisure and retail which is wrong (see below). It told me that the labour force participation rate was near cycle highs, when instead it has steadily fallen by a large 2.7 ppts from its late 2023 peak. It told me that the unemployment rate is expected to “hold steady at 3.8% or edge up to 3.9%” when it’s at 4.3% going into April’s numbers which in my biz is a huge half-point error. And so forth.

Kids, rely on this tool for your homework to your own demise. What ChatGPT gave me is worth an ‘F’ and ethics training. It’s useful for other things—like, say, Taylor Rule scenarios and the like—and can sound informed to a layperson, but it’s a dumpster fire to anyone who follows the facts and arguments closely.

So, moving on, here’s the logic, which is always presented by first reminding us that nonfarm payroll changes have a 90% confidence interval of +/-122,000 which is actually about 15k lower than the last time I checked with the BLS. 90 times out of 100 in repeated sampling the estimate would be expected to fall somewhere within what they publish and 122k higher or lower. It’s noisy, in other words. Rankings speak to outperforming others dealing with the same noise.

Weather

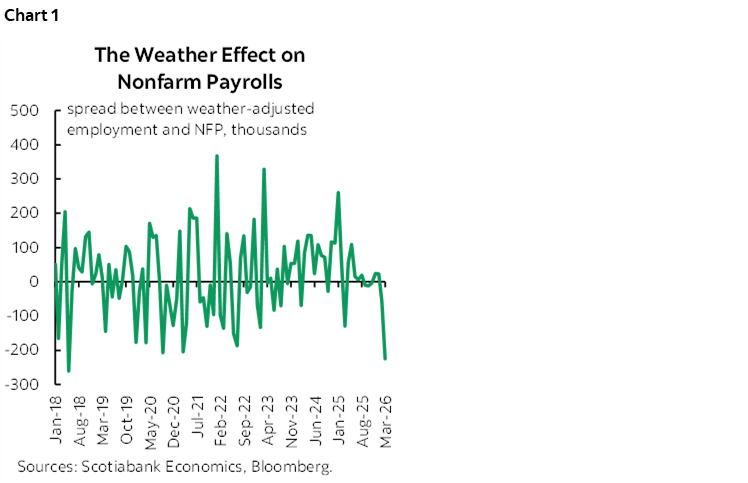

The San Fran Fed’s estimate of weather effects on nonfarm payrolls in March showed that weather overstated the job gain by between 225–250,000 depending upon which of their two methodologies you use (chart 1 and here). Controlling for weather, the official 178k gain in March would have been more like roughly -50k to -75k. This matters because even though there were plenty of tornadoes and storms across the Midwest during April’s nonfarm reference period, a high contribution from weather effects in March makes it tougher to post a repeated large gain the next month. Weather should be a drag on m/m payrolls this time.

Seasonality

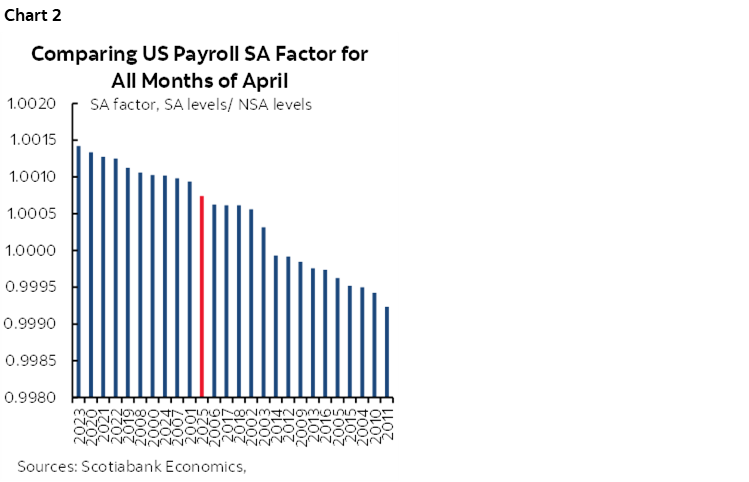

Seasonal adjustment factors for like months of April are shown in chart 2. I went with a replay of last April. The highest SA factors—that would boost payroll changes relative to lower seasonal adjustment factors—were all set in the 2019–2023 period and the BLS has been migrating away from those peaks.

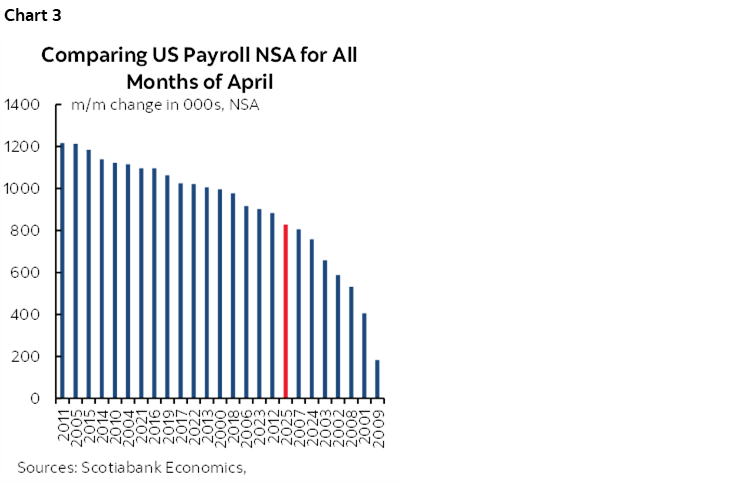

April is usually a strong seasonal up-month for employment creation before controlling for this with seasonal adjustments (chart 3). Having said that, just to keep flat on the m/m SA payroll change would require marrying last April’s SA factor to a seasonally unadjusted gain of at least 750k m/m. That’s possible, but a repeat gain over 100k m/m SA would require at least 850,000 jobs to be gained in seasonally unadjusted terms when the US has been losing hiring momentum.

Health Hiring

I don’t have a strong view on this contribution which is a risk to the call in both directions. What I’ve assumed is a bit of cooling from the 90k addition of health and social service jobs that were added in March. The powerful and concentrated flu season distorted the ebbs and flows in this category for a number of months. The expiration of some ACA subsidies at the end of 2025 may be a trend downside to health sector hiring but this is very difficult to time. Health sector job postings are the most likely to offer visa status which has a higher option value in the context of current immigration policy.

Revisions

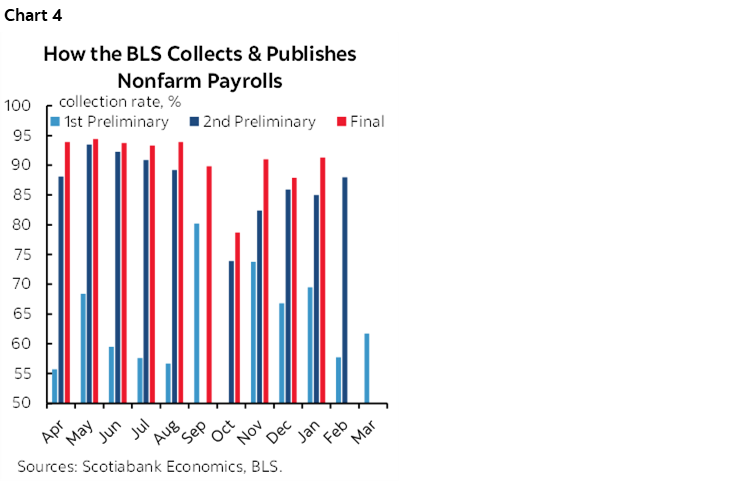

Another nervousness factor surrounding the call is how the prior two months get revised this time. I’ve gone with a modest 20–30k downward revision which is around the trend, but the high degree of under-sampling that happened last month could mean bigger revision effects—we just can’t necessarily tell in which direction (chart 4). Negative revisions are becoming a bigger factor as Jay Parmar’s chart of the week on the front cover demonstrates.

Other Readings

There is a limited number of other job market readings with more on the way over the coming week, but they’re rather mixed. They’re also not usually very helpful in relation to nonfarm’s own sample and quirks such as seasonality adjustments and the birth-death model that seeks to control for non-sampling error reflecting difficulty capturing job growth through the creation of new businesses (more here).

ADP private payrolls could be up by about 150–160k m/m in April. That would suggest upside to nonfarm private payrolls (ex-government), but ADP throws off so many head fakes and can be so heavily revised that it’s never trusted.

‘Indeed’ job postings fell in April’s nonfarm reference period over the readings in February and March.

Initial jobless claims were range bound between the March and April nonfarm reference periods and fell afterward. Further, rule changes have dampened its usefulness as a guide that was always limited because it only tells you gross claims for benefits.

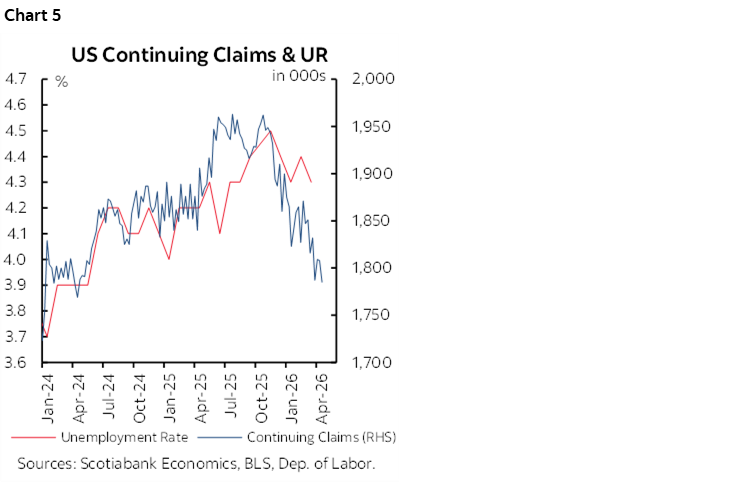

Falling continuing claims suggest that the unemployment rate could edge lower given the correlated movements in the two measures (chart 5). The unemployment rate has nothing to do with the nonfarm call as it comes from the more volatile household survey that has been posting three consecutive months of declines in employment and a falling labour force in two of the past three months.

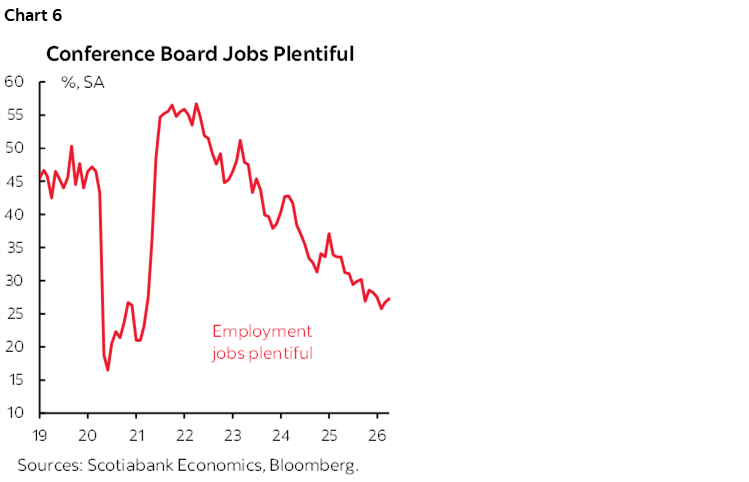

How consumers view the availability of jobs remained soft in April after ticking a touch higher in March (chart 6).

ISM-manufacturing-employment continued to contract in April’s reading, but manufacturing jobs are only about 8% of total nonfarm payrolls.

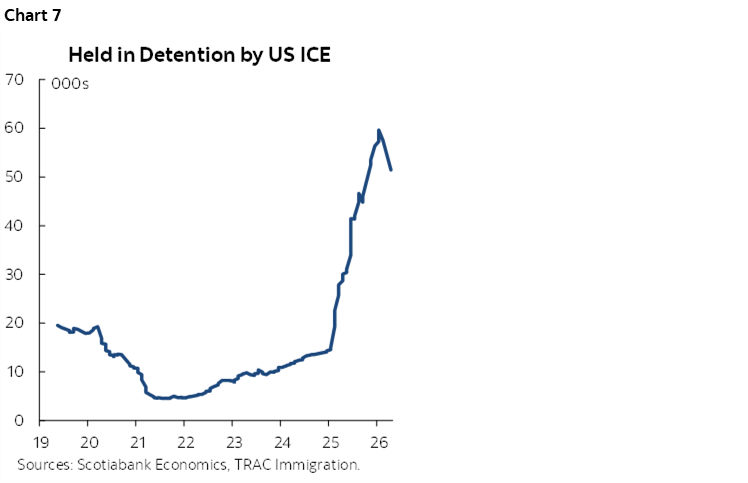

ICE detentions are still quite high but coming off the peak (chart 7). The fear factor may still be keeping people out of the workforce as a partial explanation for falling participation rates.

Over the coming week we’ll get JOLTS job openings and quits data for March that inches a little closer as a guide to April (Tuesday). Challenger job cuts in April (Thursday), Revelio’s nonfarm change estimate (Thursday) and ISM-services-employment (Tuesday) might also help as input.

The Overall State of the US Job Market

In a nutshell, it’s not as healthy as Chair Powell has tended to portray.

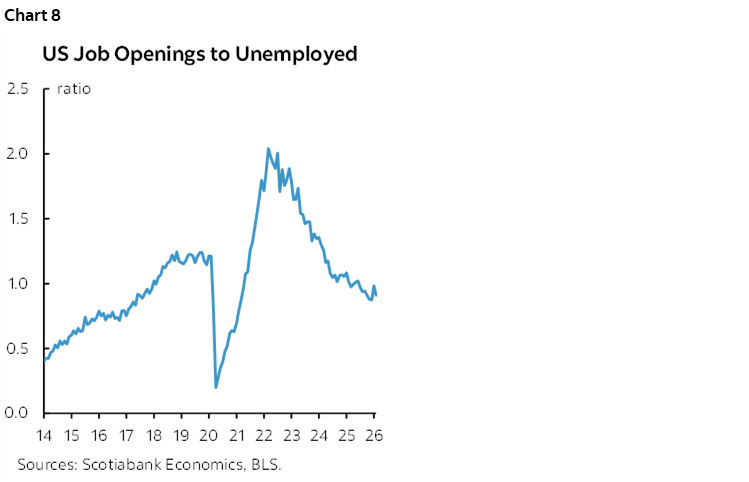

For one, the ratio of job openings to the number of unemployed has been below 1.0 for three months, indicating an insufficient number of opportunities before then turning to whether there are skills mismatches (chart 8).

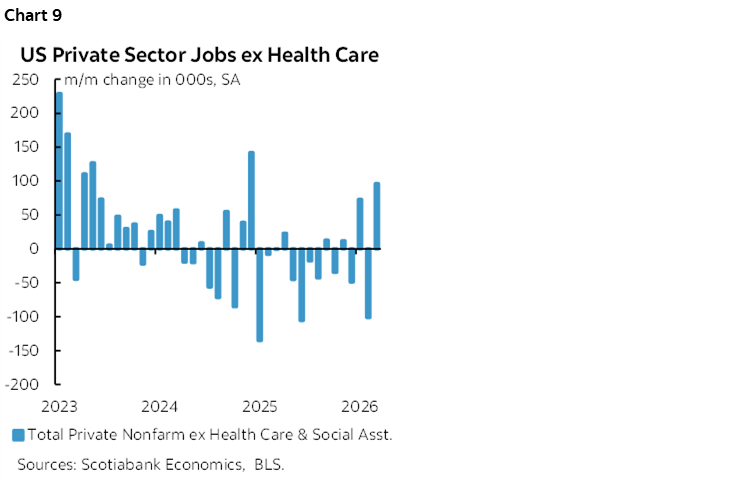

Private nonfarm payrolls have generally been down more than up the majority of months since just before the US election in 2024 such that something began to pivot before that moment (chart 9).

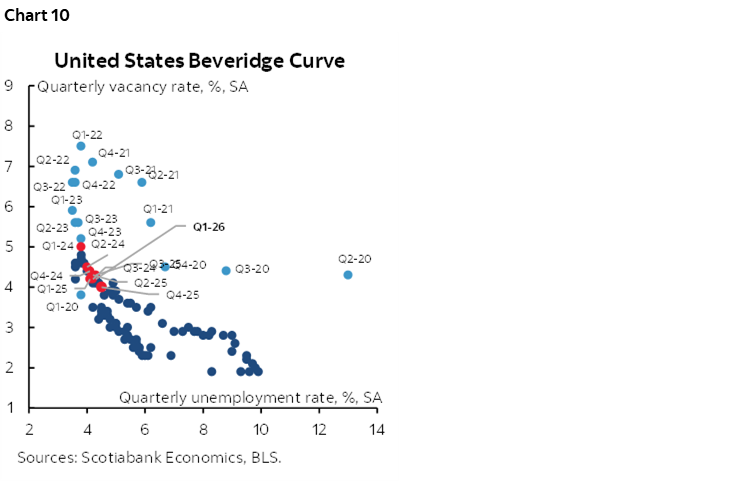

The so-called ‘Beveridge Curve’ shows the balance that exists between job vacancies and unemployed and demonstrates a degree of slack (chart 10). Where the US labour market sits today is roughly around the high end of vacancies and low end of the unemployment rate especially excluding the distorted pandemic period shown in light blue.

It’s inadequate to say there shouldn’t be worries about the US job market because the unemployment rate is well behaved. The unemployment rate is about a full percentage point higher than it was at the low in 2023 in addition to the sliding participation rate. That the shock to the unemployment rate from weakening trend private payrolls has not been greater because of tighter immigration policy overly discounts the fact that growth in jobs and incomes drive growth in consumer spending and demand for housing.

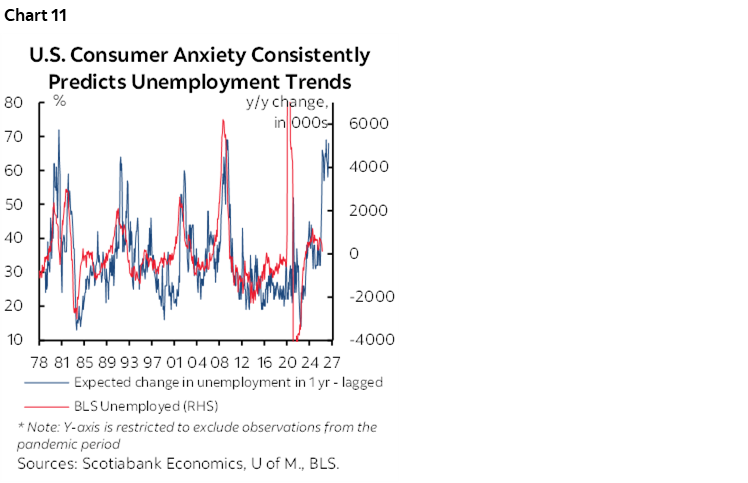

Measures like the UofM survey’s expected change in the number of unemployed Americans over the coming year have historically been very closely tied to what actually happens and this measure continues to flash a strong warning sign (chart 11). It’s soft data, but with a strong record and consumers are closer to what’s happening at their employers than economists and markets.

Unfortunately, the ability of the FOMC and markets to read the state of the job market may be significantly distorted by coming factors that will need to be controlled. Estimates after April will start to get more complicated by temporary factors. The end of the partial shutdown affecting Homeland Security employees might be slightly additive to May payrolls. FIFA World Cup hiring may begin to make contributions in May but with the bulk of the hiring focused upon June and July before this effect reverses afterward. Estimates of the number of folks who will be hired or volunteer on a temporary basis push into the hundreds of thousands.

BOX 1: WHAT CHATGPT OFFERED AS A NONFARM PAYROLLS PREVIEW

Please write a nonfarm payrolls preview for the month of April. Make sure it includes references to weather effects, health sector hiring, seasonality, unemployment rate expectations, other job market indicators and expected revisions to prior months.

U.S. Nonfarm Payrolls Preview—April 2026

We look for a moderate rebound in job growth in April following softer prints earlier in the year, with headline nonfarm payrolls rising by ~175k–200k. The underlying trend in hiring remains resilient but is no longer accelerating, as tighter financial conditions and slower demand growth continue to temper labor demand.

Weather effects

Weather is likely to provide a modest positive payback in April. March data were likely held down by residual winter disruptions in parts of the Midwest and Northeast, including unseasonably cold temperatures and localized storms during the survey week. April’s more typical conditions should support a rebound in construction, leisure & hospitality, and some retail categories. That said, weather effects this time of year are usually second-order compared with January–March volatility.

Health care and social assistance

Health sector hiring should again be a key pillar of job growth, with gains in the 40k–60k range. Structural demand—aging demographics, backlog of procedures, and ongoing expansion in outpatient services—continues to drive steady hiring in ambulatory care and hospitals. This sector has consistently outperformed and is likely masking softness elsewhere.

Other sector dynamics

- Leisure & hospitality: Likely to bounce back after weather-related weakness, though trend hiring has cooled from last year’s pace.

- Construction: A weather-driven rebound is expected, but underlying momentum remains mixed given high borrowing costs.

- Professional & business services: Likely subdued, reflecting weaker demand for temporary help and consulting services.

- Government: Continued steady gains, particularly at the state and local level (education-related hiring still a factor).

Seasonality and residual distortions

April data are generally cleaner than the heavily adjusted winter months, but seasonal adjustment noise remains a risk—particularly in education, retail, and construction. Recent years have seen persistent early-year seasonal quirks, so some payback from earlier distortions is possible. However, we do not expect a large seasonal “snapback” comparable to prior cycles.

Unemployment rate and household survey

We expect the unemployment rate to hold steady at 3.8% or edge up to 3.9%, reflecting:

- Slightly slower employment growth in the household survey

- Continued expansion in labor force participation

The participation rate is likely to remain near cycle highs, supported by prime-age workers, though gains are becoming more incremental.

Wages

Average hourly earnings should rise ~0.3% m/m, keeping the y/y pace near 4.0%–4.2%. Wage growth continues to gradually cool but remains above levels consistent with 2% inflation.

Other labor market indicators

Recent high-frequency and survey data point to gradual cooling but not deterioration:

- Initial jobless claims remain low, consistent with limited layoffs

- Continuing claims have drifted higher, suggesting longer job search durations

- JOLTS data show declining job openings and a lower quits rate, indicating reduced worker confidence

- ADP employment has been volatile but broadly consistent with mid-range payroll gains

- NFIB hiring plans continue to soften, pointing to slower small business hiring ahead

Revisions to prior months

We expect modest net downward revisions (~25k–50k) to February and March. Recent benchmarking patterns and softer incoming data suggest prior estimates may have slightly overstated momentum. That said, revisions are unlikely to materially alter the broader narrative of a gradually cooling labor market.

Bottom line

April payrolls should show a weather-assisted rebound with continued strength in health care and public sector hiring, offset by softer cyclical sectors. The labor market remains solid but is clearly transitioning toward a more sustainable, slower pace of growth, consistent with a gradual rebalancing rather than an abrupt slowdown.

CANADIAN JOBS—SET LOW EXPECTATIONS

Canada also updates job market conditions for the month of April on Friday at the same time as nonfarm payrolls. If you think forecasting payrolls is tough, you need extra good fortune forecasting this one.

The main measure that is followed in Canada is the Labour Force Survey. It’s a household survey, like the US version that accompanies nonfarm payrolls. Household surveys have higher noise factors. The 95% confidence band for the change in Canadian employment is about +-57,000 which would be about half a million in the context of the US labour market for reference purposes. It’s also huge in the US household survey where the BLS says the 90% confidence interval for its measure of the change in the number of unemployed is about +/-425k.

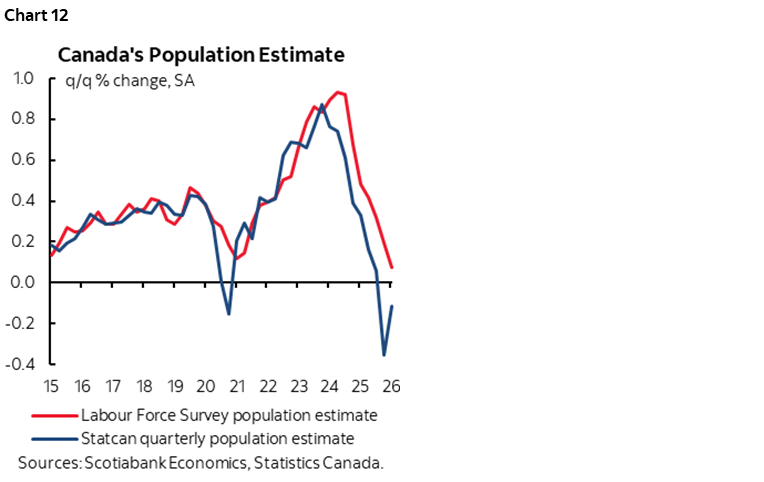

I’ve estimated no change in jobs during April and a flat unemployment rate of 6.7%. Key for the unemployment rate is when the survey starts showing a contracting population and contracting labour force as a reflection of tighter immigration population. That’s especially applied to the temps category that includes international students, temporary foreign workers and asylum seekers. As StatCan explains, the LFS applies a 12-month moving average to the size of the temp category and therefore its measures lag actual population changes (chart 12). The time for LFS to catch up and begin showing declining population is approaching.

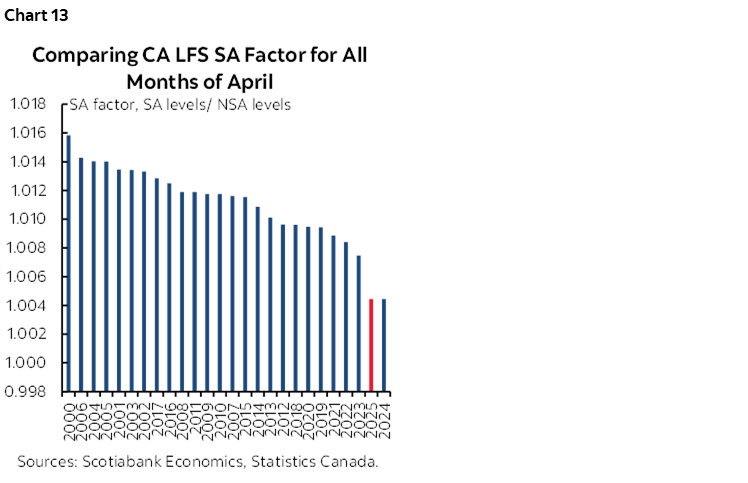

Statcan does not revise jobs on a monthly basis like the US does. The problem this time is a bit of a quirky argument. The seasonal adjustment factor is expected to remain lower than historically as has been the pattern for like months of April in recent years (chart 13) while there is a very high bar for the seasonally unadjusted change in employment to be big enough to keep the change in jobs in the black.

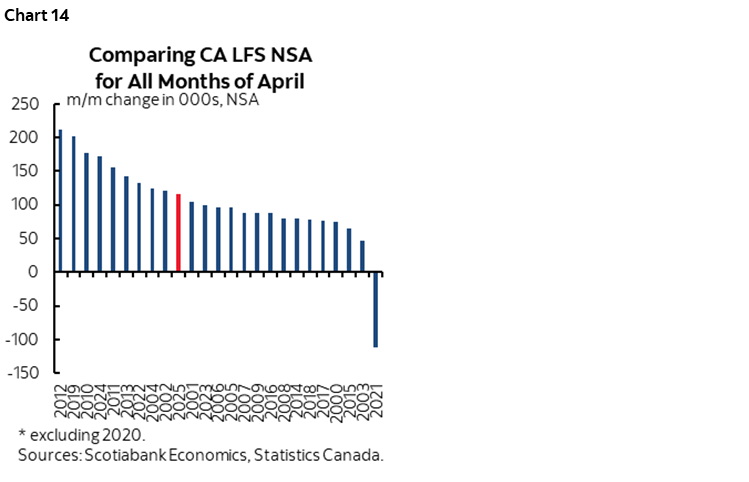

In fact, you’d need a seasonally unadjusted change of 170k m/m just to keep seasonally adjusted jobs flat. As chart 14 shows, 170k would be among the very small handful of the strongest gains in history. There is more downside than upside risk to a flat reading.

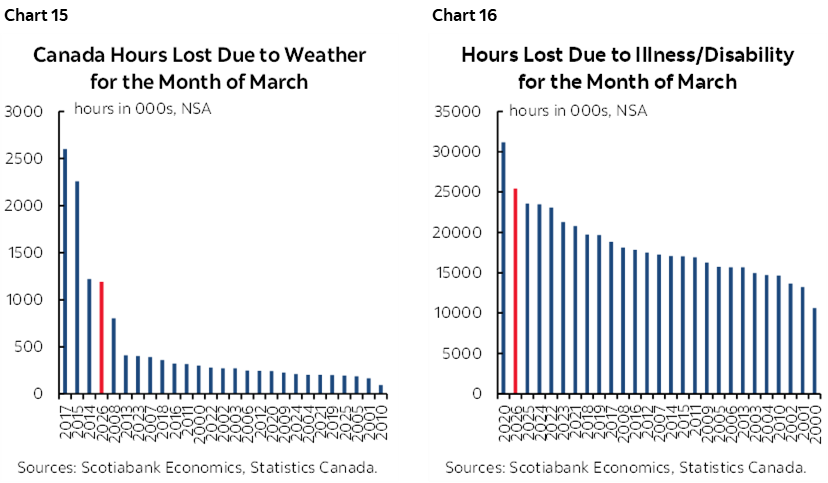

What might help could be the weather and sickness arguments that may have held back hiring and interviewing in the past month. We know that to have been the case in terms of hours worked (charts 15, 16).

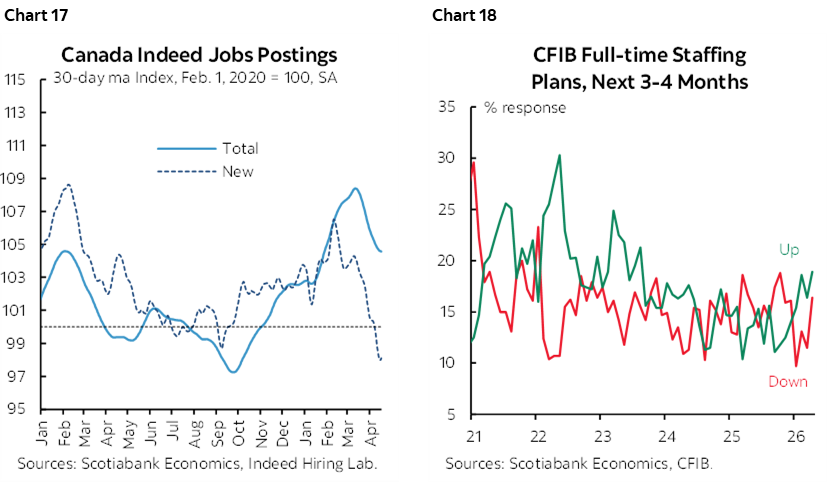

Across other advance readings, ‘Indeed’ job postings have been softening with new postings falling (chart 17). Small businesses indicate a bias toward hiring more workers (chart 18).

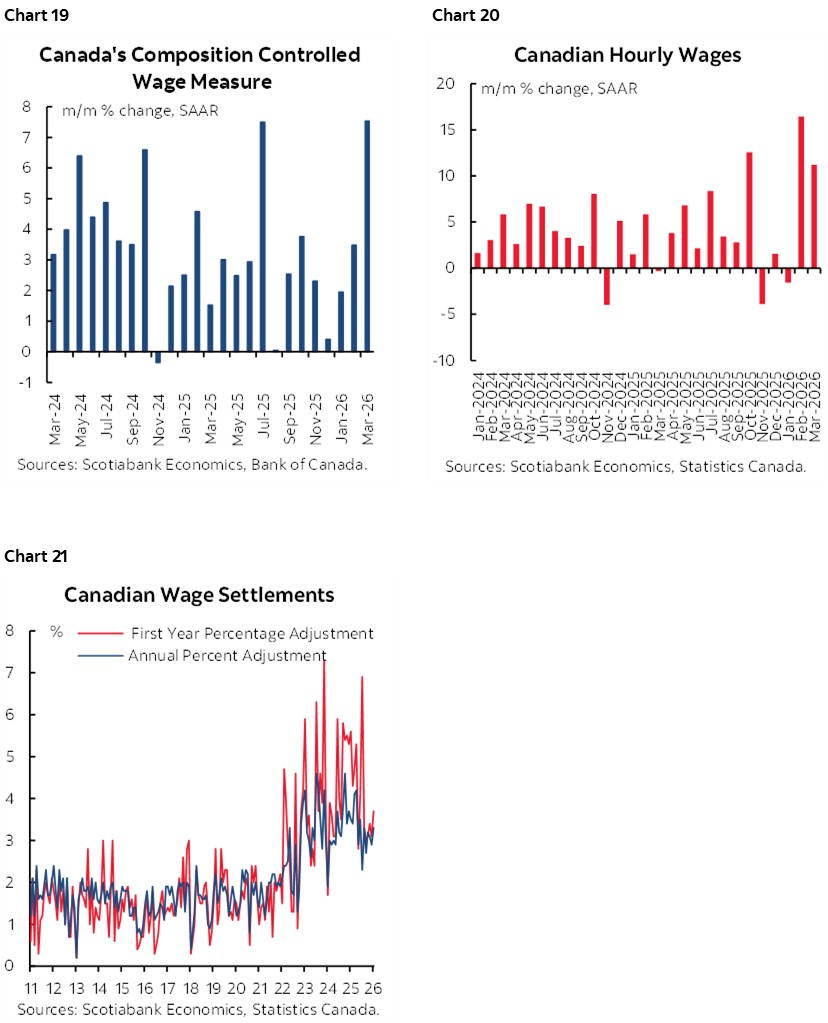

What’s more interesting in Canada is that the Bank of Canada’s figures for wage growth that control for compositional shifts surged last month according to their fresh estimates (chart 19). There is little different compared to surging wage growth that does not control for compositional changes (chart 20). Canada is still very much in an upward wage spiral including the effects of expiring collective bargaining agreements struck 3–4 years ago that are cementing years of wage gains above the BoC’s 2% inflation target going forward (chart 21). Canada is not the US in so many ways, one of which being the extended wage resets with triple the 10% unionization rate that exists stateside.

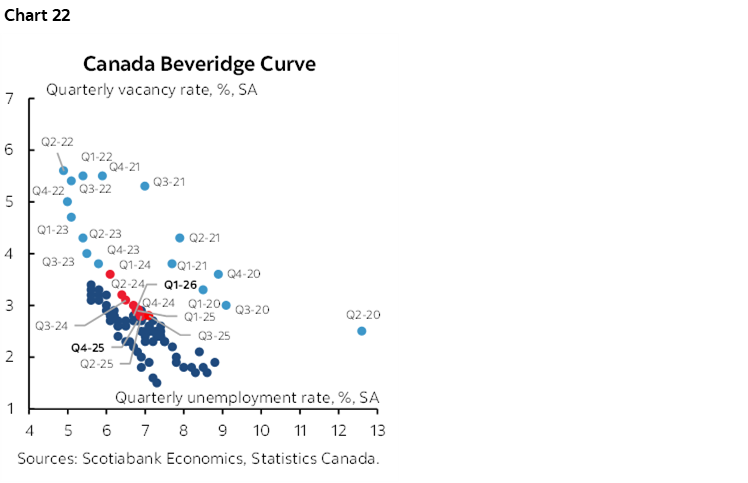

As for the broader state of the Canadian job market, Canada’s Beveridge Curve is shown in chart 22. The relationship between the job vacancy rate and the unemployment rate is about smack dab in the middle of historical experience.

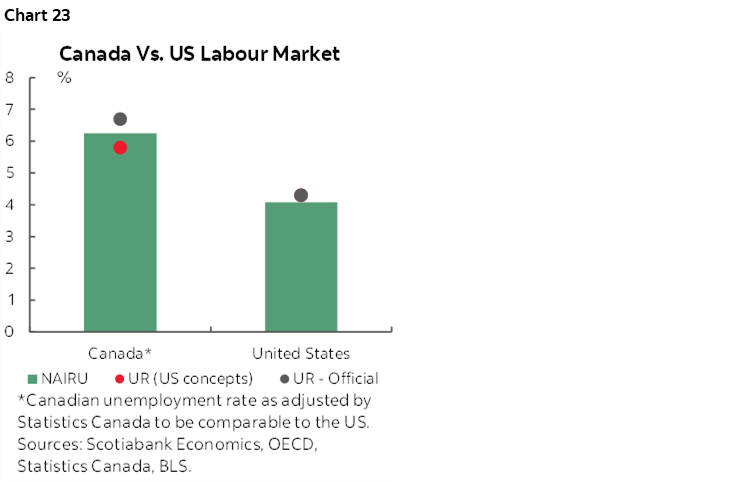

Chart 23 shows unemployment rates compared to estimate of full employment unemployment rates (NAIRU) in Canada and the US. It also shows Statcan’s measure of the Canadian unemployment rate measured using US concepts, since Canada’s defines the labour market starting at a younger age, has less stringent criteria for defining who is actively looking for work etc. Canada always has a higher unemployment rate than the US but right now there is perhaps marginal slack in both countries relative to estimates of full employment.

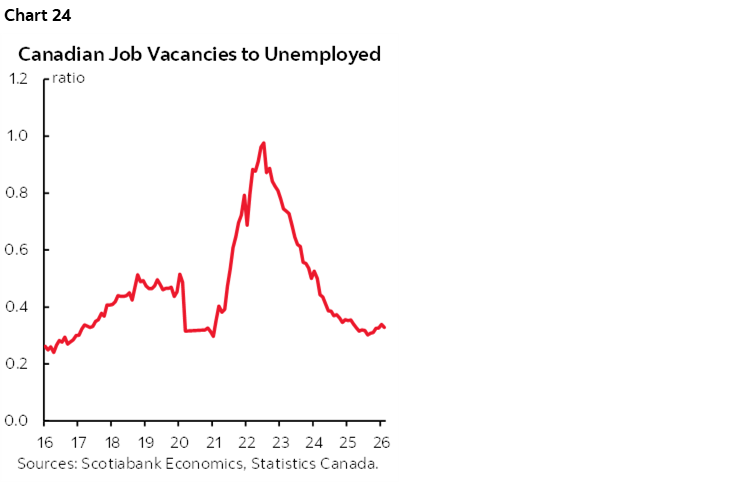

Chart 24 shows that in Canada, job vacancies tend to almost always be fewer in number than the number of unemployed. Canada’s labour market always has more structural unemployment driven by regional, policy and other frictions some of which frankly I’d rather not get into!

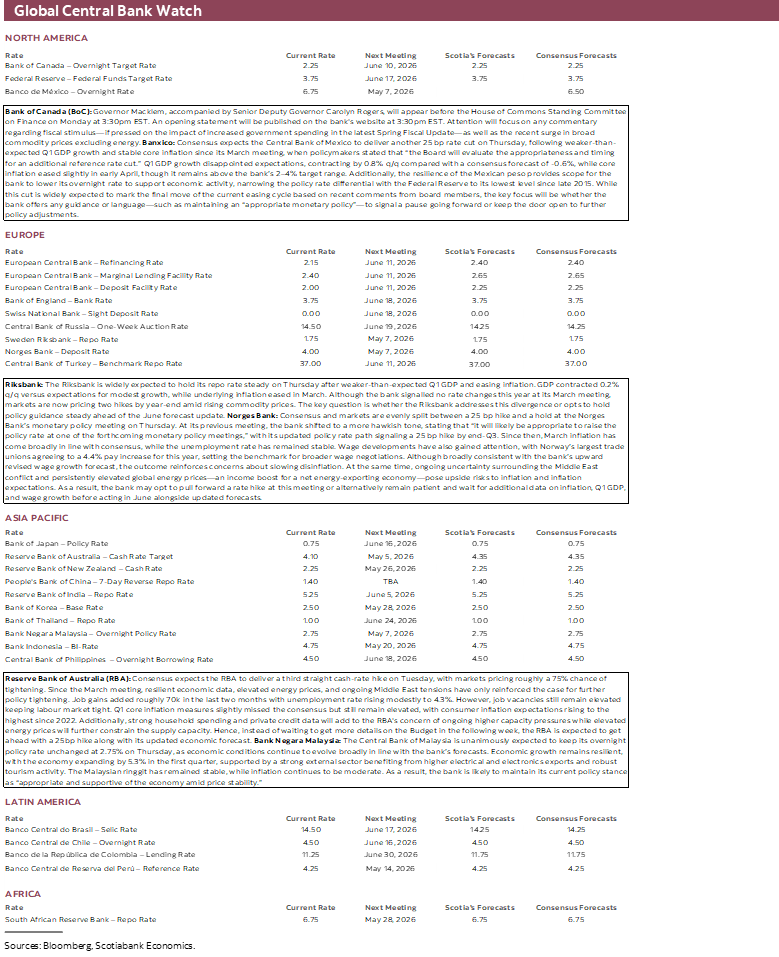

CENTRAL BANKS—REGIONAL AFTERSHOCKS

Five regional central banks will weigh in with policy decisions this week in the aftermath of the key figures this past week. A few things might also be cleared up in two rounds of Bank of Canada testimony.

BoC Testimony—More Insights Needed

BoC Governor Macklem and Senior Deputy Governor Rogers will deliver two rounds of parliamentary testimony on Monday (3:30pmET) and Wednesday (4:15pmET). The post-BoC recap provided areas where I’m hoping for more to be revealed in the discussion with members of Parliament (here).

Like why did they only speak about the effects of surging oil and gas prices and supply chain challenges and not about all the other commodities that are on fire? Expect the opposition to go after the BoC on the implications of more federal government spending equal to ½% of NGDP this year and ¼% next year and expect the BoC to shrug and avoid commenting on friends in government. Expect grilling on why you’d downgrade growth projections ex-inventory effects when everything the country sells by way of key commodities is on fire now. The BoC says medium-term inflation expectations are around their target, yet no measure in Canada supports this including their own. Why does the BoC have the lowest inflation forecast on the street? Perhaps ask them to comment on the possibility Canada gets a trade deal and commodities stay high. Why is the BoC easing via the inflation-adjusted policy rate into a commodity shock?

RBA—Unfinished Business and More to Come

Consensus almost unanimously expects Australia’s central bank to hike by another 25bps to a cash rate target of 4.35% on Tuesday. Australian futures and OIS markets attach three-in-four odds to a hike.

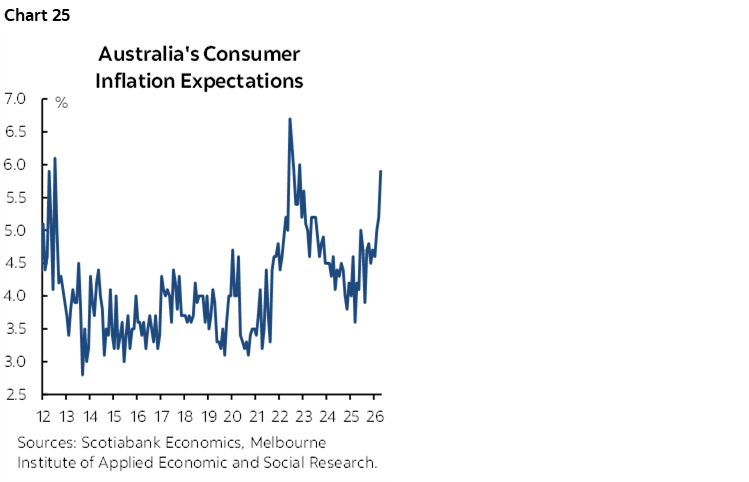

Inflation at 4.6% y/y with still hot trimmed mean CPI and soaring inflation expectations (chart 25) would be leaned on as a rationale for hiking a third time since February. Those readings during Q1 largely pre-date the additional inflation shock that will be coming over the months and quarters ahead. The possibility of affordability measures in the following week’s Budget on May 12th may be implicitly guiding a tighter stance.

Negara—Taxes and Debt or Rate Hikes?

Malaysia’s central bank is widely expected to stay on hold on Thursday at an overnight rate of 2.75%. Consensus is unanimous and markets are priced for no change.

CPI is running at just 1.7% y/y up to March. Malaysia applies subsidized price caps on gasoline and recently lowered purchase quotas by one-third to 200 litres. While this approach shifts incidence effects of soaring energy prices onto others including government and taxpayers, it temporarily mitigates inflation pass through.

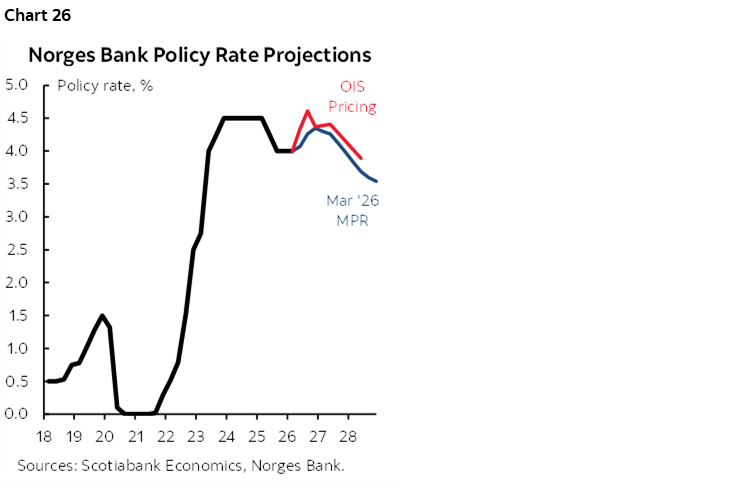

Norges Bank—Soaring Oil Vs. Restrictive Stance

Norway’s central bank will be a tougher call on Thursday. Most within consensus see the central bank holding at a deposit rate of 4%. A minority expect a 25bps hike. Half of a quarter-point hike is priced in OIS. So what gives?

Normally this central bank provides explicit forward guidance. At its last meeting in March it gave less than explicit guidance. Governor Ida Wolden Bache said “…the Committee judges that it will likely be necessary to raise the policy rate at one of the forthcoming monetary policy meetings.”

That could mean May, June, August, or maybe thereafter. Since Norway is heavily dependent upon oil production and is strongly benefiting from oil prices as the US and Israeli war against Iran continues, it seems this is very likely to be the first of the developed world’s commodity-oriented central banks to hike.

The rub lies in the fact that—unlike the Bank of Canada—Norges Bank remains in restrictive territory on its policy rate and might decide this is enough to give it further time to assess conditions.

Markets don’t have a whole lot priced for Norges (chart 26).

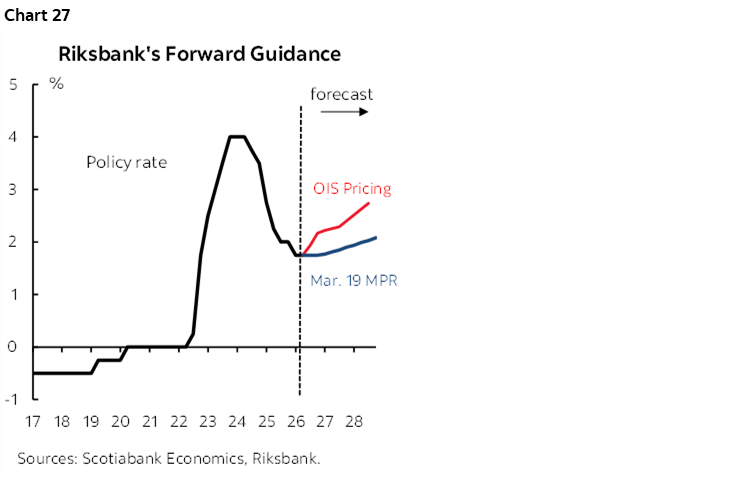

Riksbank—Up or Down?

Sweden’s central bank is widely expected to leave its policy repo rate unchanged at 1.75% on Thursday. Guidance that was provided at the March meeting signalled uncertainty about the future direction of the policy rate that is unlikely to have been settled since then. Sweden is a net energy importer and so it doesn’t enjoy the riches flowing to its Scandinavian neighbour. Here’s what they said in March and what data dependency may largely repeat this time:

“One possible scenario is that the war has significantly greater effects on the global economy and leads to a broader and more persistent upturn in inflation. The Riksbank would then have to raise the policy rate, even though economic activity in this case would be significantly lower. Another possible scenario is that the negative effects on demand become more significant at the same time as inflationary pressures become weaker. The Riksbank would then have to cut the policy rate to stimulate demand and thereby stabilise inflation at the target.”

Markets are nevertheless calling for a hike profile (chart 27).

Banxico—The Last Dance?

Mexico’s central bank is widely expected to cut its overnight rate by 25bps on Thursday. Consensus is unanimous and markets are largely priced for a cut.

At 6.75% going into the meeting, Banxico’s policy rate is within reach of the middle of its neutral rate range if not higher. This stance provides somewhat more flexibility aligned with another large energy exporter—Norway—compared to, say, an energy exporting nation like Canada where the central bank’s policy rate is at the bottom of its neutral range.

Banxico has an easing bias as indicated by saying at its March meeting that “the Board will evaluate the appropriateness and timing for an additional reference rate cut.” Growth is disappointing as the economy contracted in Q1. Still, expect dissenting voices again after Deputy Governor Jonathan Heath voted against easing the last time because of inflation worries. Governor Victoria Rodriguez Ceja recently remarked that the end of the easing cycle is near at hand and so this could be the final cut.

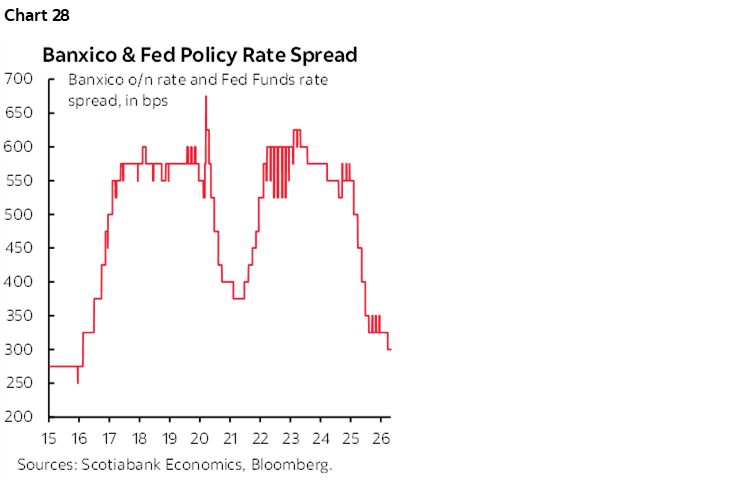

A limiting factor is that Banxico’s policy rate spread over the Federal Reserve is toward the tights and with the FOMC not sounding like it’s in a hurry to cut with the hawks lining up (chart 28).

BanRep Minutes to Offer More Colour

Colombia’s central bank stunned forecasters and markets by staying on hold at an overnight lending rate of 11.25% this past week. Many had anticipated a 50bps hike. Wednesday’s minutes will provide further opportunity to elaborate on the rationale.

GLOBAL MACRO—SIDE SHOWS

Canada will mainly focus on BoC testimony and Friday’s jobs report, but Tuesday’s trade figures will improve our understanding of Q1 GDP tracking. Some little watched PMIs will be released that same day.

US markets will obsess over nonfarm and related readings, but there will be a few other more minor gauges to consider. Factory orders should be strong after the surge in durable goods orders (Monday). The trade deficit is expected to widen a bit given we already know the goods portion (Tuesday). ISM-services will help to inform growth momentum in services but also broader inflation risk since the ISM price gauges are a leading indicator of coming inflation (chart 29). New home sales in March (Tuesday) are expected to post a solid gain into modest growth in construction spending (Thursday). The week closes with UofM sentiment (Friday).

CPI inflation readings from across Asia-Pacific and LatAm markets will be the rest of the main line-up. It starts with Indonesia and Philippines (Monday), then Switzerland, South Korea, and Thailand (Tuesday), followed by Sweden (Wednesday), Mexico and Taiwan (Thursday) and wrapped up by Chile and Colombia (Friday).

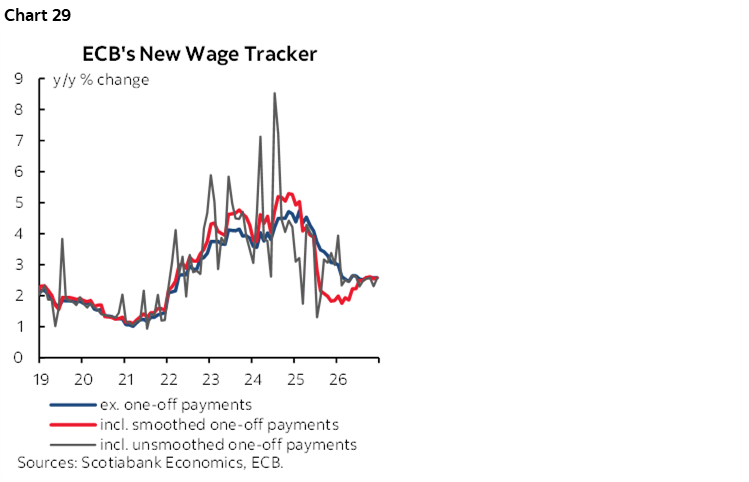

At the euro‑area level, the key release will be the updated EU wage tracker on Wednesday, which will provide insight into recent wage negotiations and their implications for future wage growth. The tracker is currently pointing to wage growth of around 2.6% in 2026 and will be closely monitored by the ECB as it assesses second‑round effects from the global energy price shock.

In Asian markets, New Zealand is scheduled to release its Q1 labour-market data on Tuesday, which is expected to show another modest increase of 0.3% q/q. However, the focus will be on the unemployment rate, which is expected to remain steady at 5.4%. Any uptick would further support the case for the RBNZ to remain on a patient hold. Furthermore, China will release its private services PMI on Tuesday.

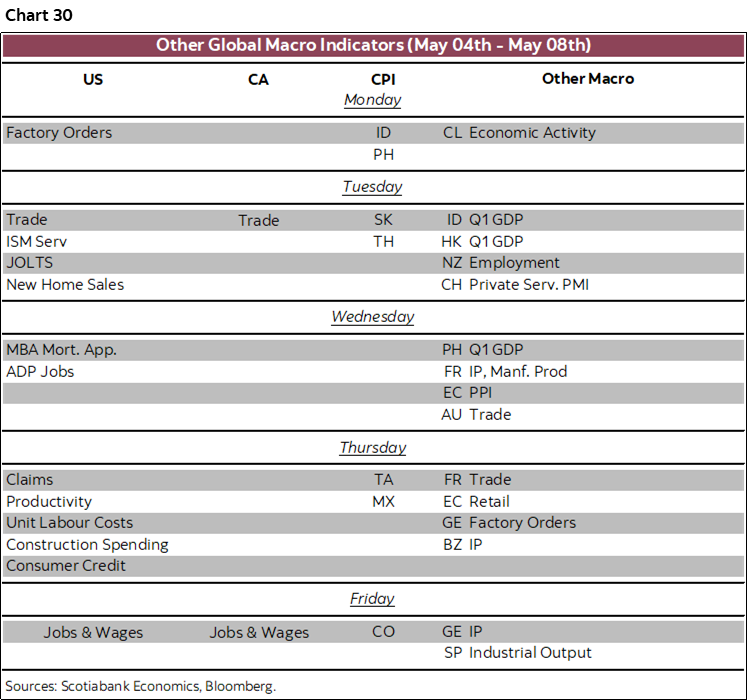

Chart 30 showcases the rest of the global line-up.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.