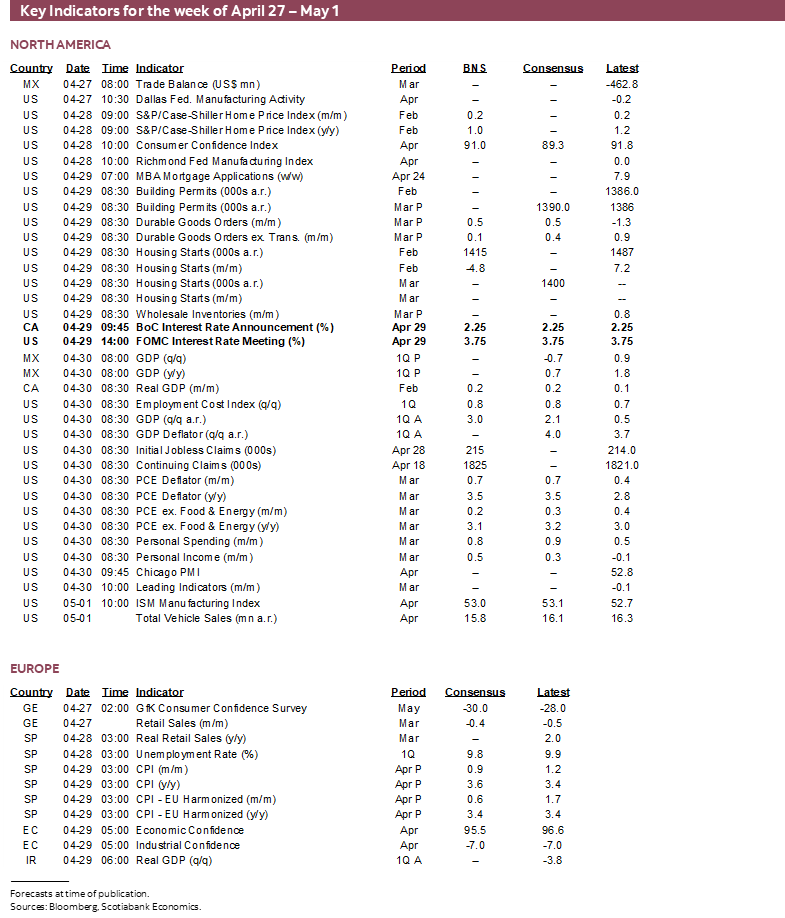

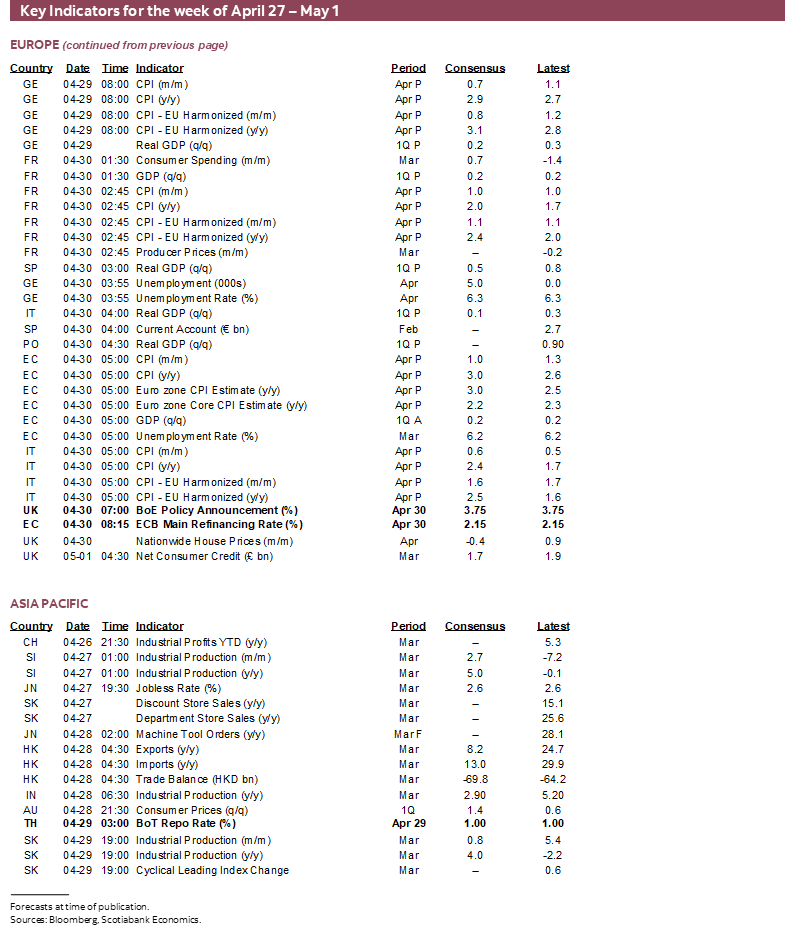

Next Week's Risk Dashboard

- US-Iran negotiations — Sending in the ‘B’ crew

- Bank of Canada preview

- The war wasn’t the catalyst for our BoC hikes…

- …but it strengthens the case

- Canadian fiscal policy — pre-spending the commodity dividend

- BoC’s gross bond buying could happen sooner

- FOMC preview: Powell to pass the baton

- BoE — A new shock compounds residual inflation

- ECB — Waiting for June

- BoJ — Hold with hawkish cues?

- BCCh — Extending the hold

- BCB — Easing off a deeply restrictive stance

- BanRep — Continued divisions?

- BoT — No follow-up

- Canadian GDP in line with BoC?

- US GDP — All about what lurks beneath

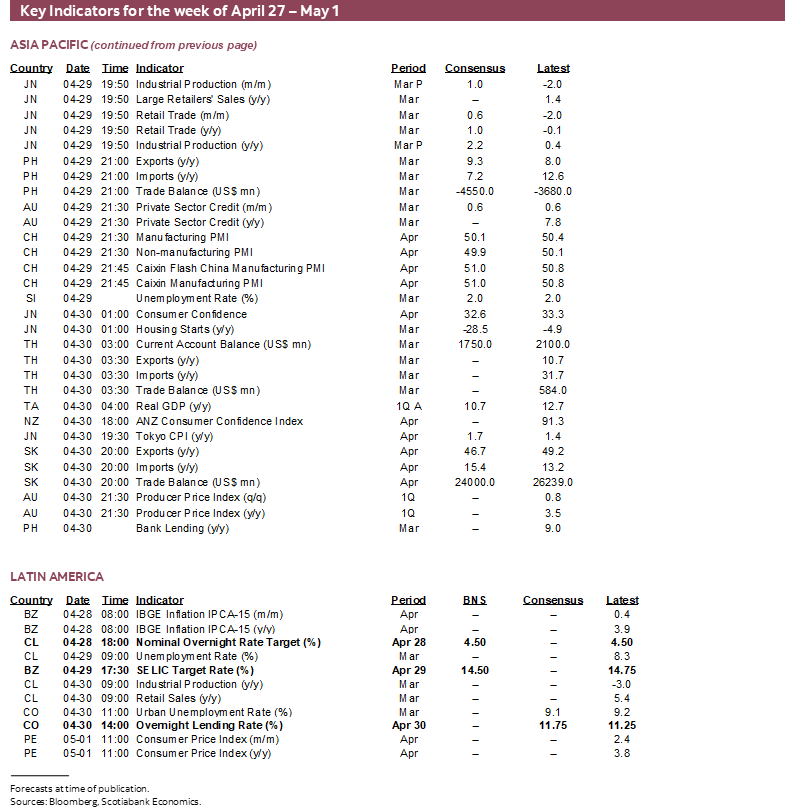

- GDP: US, EZ, Taiwan, Sweden, Mexico

- Inflation: US PCE, EZ, Australia, Tokyo, Peru

- China PMIs

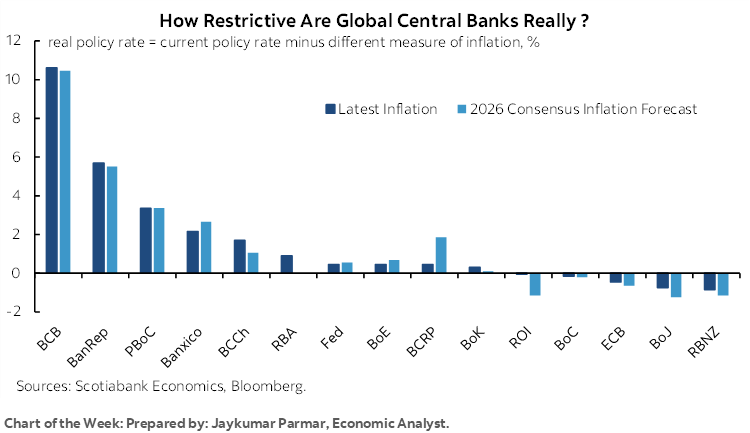

Chart of the Week

A sure fire sign of expected negotiating success is when it’s the ‘B’ team that gets sent in. The US and Iran will kick off a new week in the markets by sending Witkoff and Kushner to represent the red, white and blue—keeping Vance and Rubio at home—while Iran counters with a delegation led by Foreign Minister Araghchi—keeping Speaker Ghalibaf at home. At the time of writing it was thought that the Iranian delegation may have come more firmly under the control of the Iranian Revolutionary Guard Corps. While difficult to tell as outsiders, the result could mean that divisions have given way to a firmer negotiating stance by the Iranian regime.

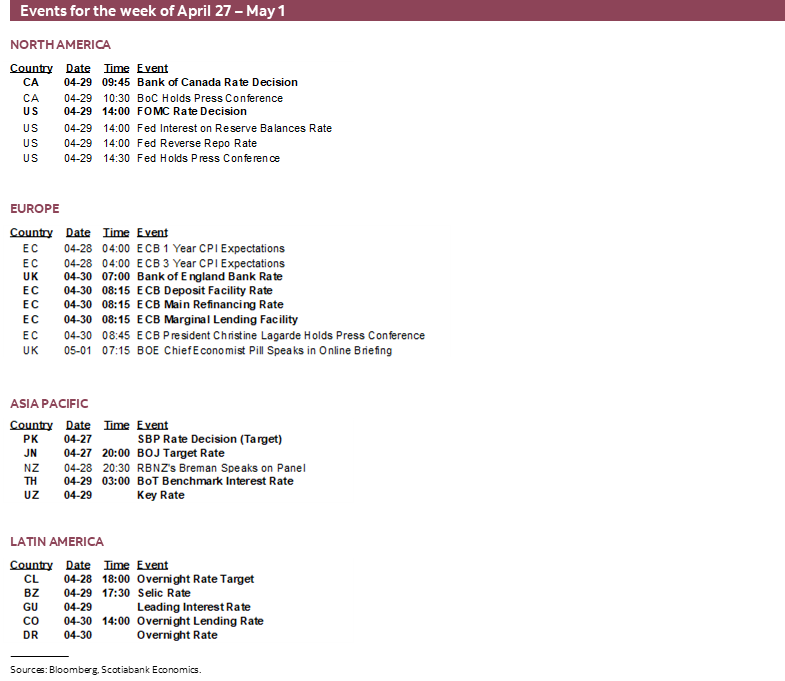

That won’t help central bankers as an onslaught of decisions arrive. Each of the Federal Reserve, ECB, BoJ, BoE, BCCh, BCB, BanRep and BoT will weigh in with decisions and guidance. Watch for a possible vote date set by the US Senate on Kevin WarshCanada watchers will also face a Federal Spring fiscal update on the eve of the BoC decision.

Large waves of global earnings reports and global macro reports also lie in store. Canada’s pre-war economy might be tracking BoC expectations after all, while US GDP is likely to be strong but weak under the hood. GDP and inflation reports from several other regions and China’s state PMIs are also due out.

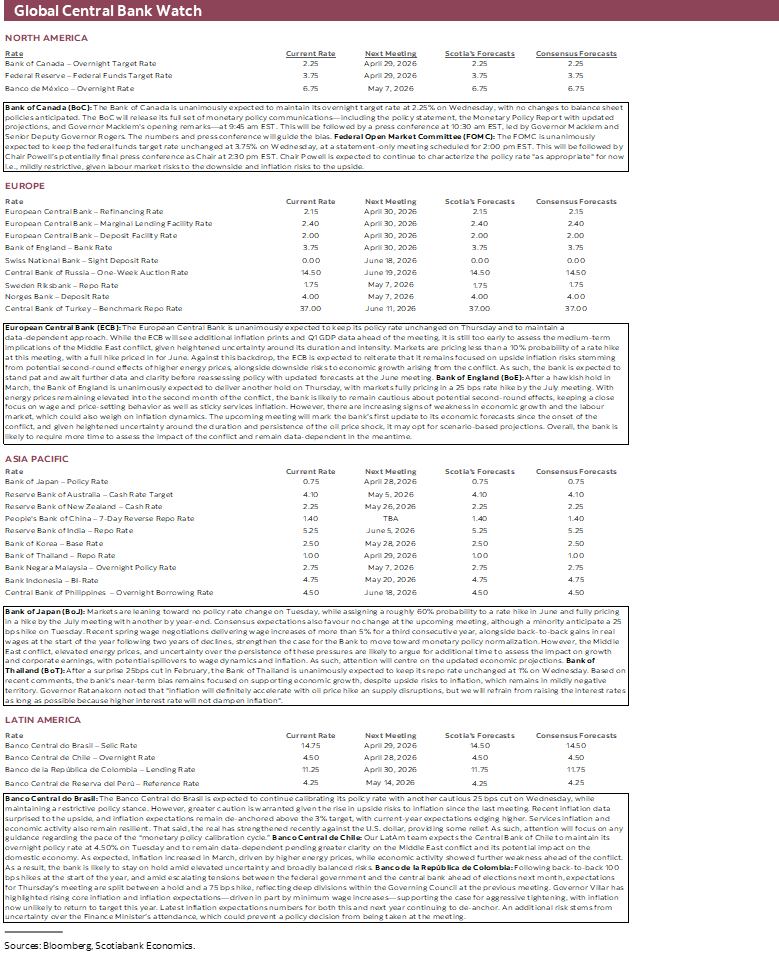

BANK OF CANADA—FORECAST LEADERSHIP

The BoC delivers its latest policy statement, a fresh Monetary Policy Report including updated projections, and Governor Macklem’s written opening remarks to his press conference at 9:45amET on Wednesday. This will be followed by the press conference led by Macklem and Senior Deputy Governor Rogers starting at 10:30amET and lasting for typically 45+ minutes. The press conference can be watched for free at CPAC.CA with French and English translations or here at the BoC’s website; frequent technical difficulties merit using more than one feed.

No Policy Changes at this Meeting

We expect the overnight rate to be left at 2.25%. This is priced in OIS and consensus is unanimously supportive of a policy hold. No changes to balance sheet policies are expected but CORRA—a repo market approximation for the policy rate—continues to trade about 5bps above the policy rate. More on the balance sheet and possible coming changes in a moment.

Key, however, will be how the BoC lets the numbers do the talking and the colour they choose to put behind a policy bias at this point—if any.

I’ll also explain our forecast. We are the only ones in consensus forecasting tightening this year with markets priced for about 1½ 25bp hikes later in the year. Some shops have merely punted their tightening views into 2027Q1. We were also way ahead of the consensus herd with hikes in the pandemic and strongly outperformed consensus and markets. I don’t know if today is the same as late 2021 when I began writing notes above much earlier hikes than anyone else anticipated but will present the case for being different from what every other shop is guiding today and why markets have a hiking bias partly priced in.

How the BoC May Change Its Forecasts

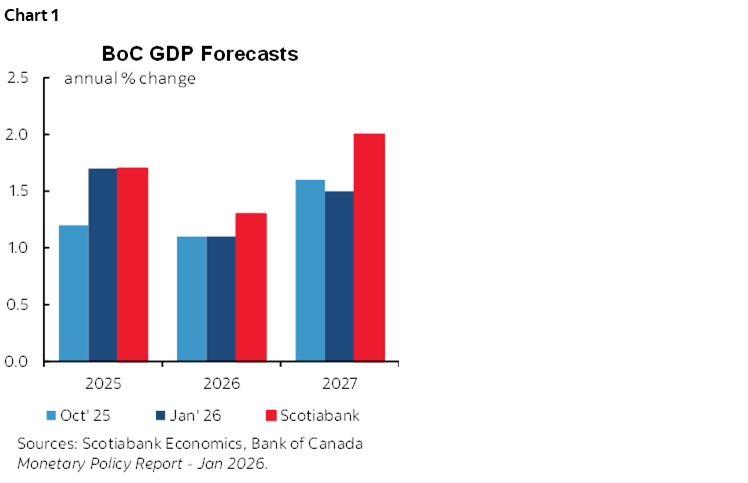

The intent behind charts 1–2 is not to critique the BoC’s January MPR forecasts since a lot has changed since then, but rather to emphasize potential changes rooted in our own fresher forecasts.

Chart 1 shows our view that the BoC may revise up GDP growth this year and next. 2026Q1 GDP could still land toward the BoC’s 1.8% q/q SAAR view based on our tracking but the commodity price surge would be among the measures they could cite for revising growth higher.

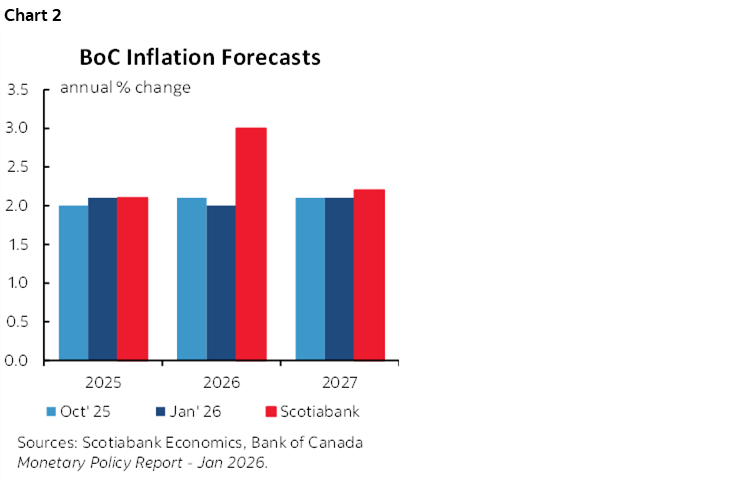

Chart 2 shows that they probably must revise headline inflation forecasts higher at least for 2026, but what they do for 2027 may also be important with the caveat that their inflation forecasts will embed an unknown implied rate policy that may include rate adjustments.

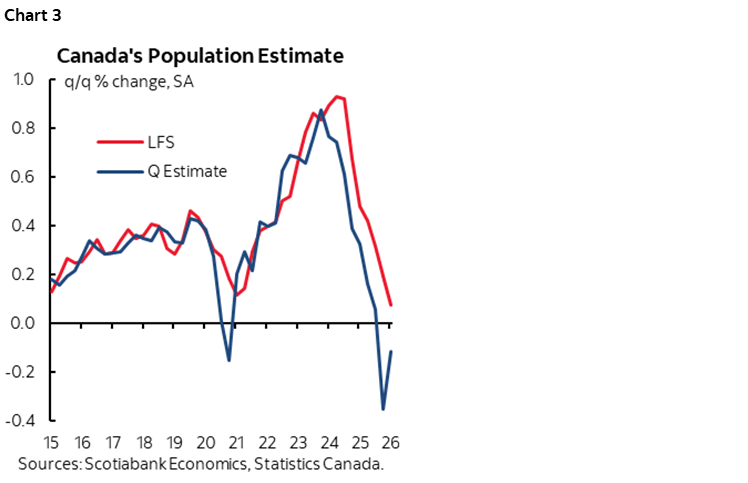

This is also the time of year when the BoC reassesses potential GDP growth—the economy’s non-inflationary speed limit to growth and hence a supply-side driven metric. They have assumed to date that potential GDP would grow by about 1% over the 2026–27 projection horizon. One driver of such a soft supply side was tighter immigration policy that is driving a population contraction (chart 3). Another is persistently soft labour productivity. Another is tariffs and trade tensions. At this point, none of these arguments has changed.

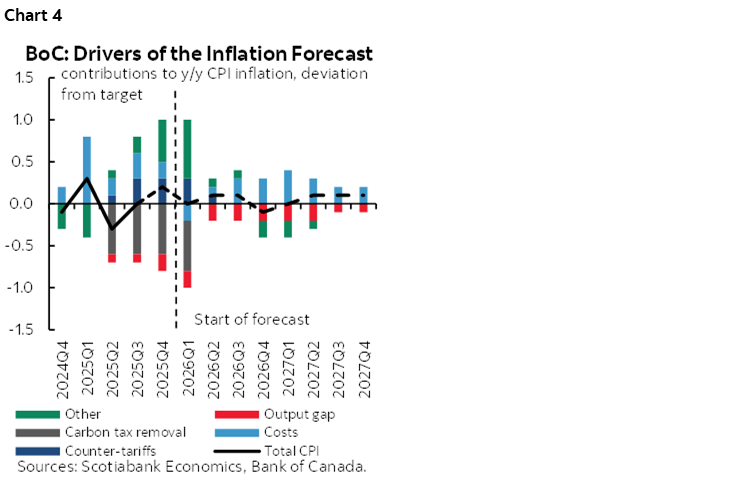

If they stick with the same potential growth rate but revise up growth, then they may project a narrower amount of slack than previously judged and with less downside pressure on projected inflation from this source. Recall they only previously forecast that slack would account for less than -¼% of a weighted drag effect on inflation over the 2026–27 forecast horizon (chart 4). They had argued in January that drivers like higher cost pressures being passed through would be a bigger upside driver of inflation and may be further inclined to think so this time around.

How the BoC May Deliver its Policy Bias

It’s expected that there will be stronger warnings on the implications of an inflation shock to the policy rate’s path but with no commitment. No explicit guidance is likely, but the policy rate bias is likely to sound like it leans in a more hawkish sounding direction.

On the possible bias that may be conveyed beyond the narrative told by the numbers, let’s start by reminding readers of a few key things that the BoC has recently done and said.

“We’re all feeling like you don’t want to jump too early and raise interest rates and lower growth, particularly when growth is already weak. On the other hand, you don’t want to be late and let inflation get a hold and get entrenched.” —Governor Macklem, Friday April 17th 2026.

In that quote I only saw hike risk with uncertainty around probability and timing. I see behind that quote a divided Governing Council. That’s clearly where their head is versus easing. If not, then the Governor chose his words poorly and should have been more open-ended.

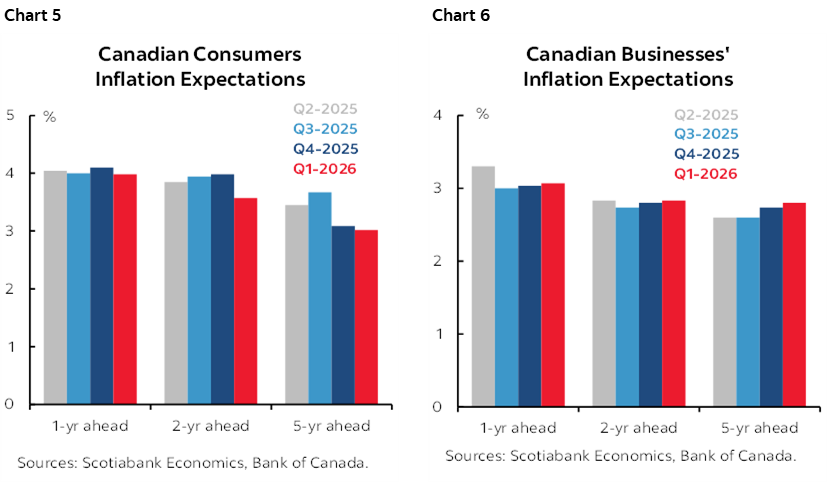

Macklem also emphasized on that same day that while higher nearer term inflation expectations would not worry them, higher medium- to longer-term measures would. Enter charts 5–6 showing the BoC’s latest survey measures with all medium-term measures of inflation expectations toward the top-end of the BoC’s 1–3% inflation target range or above it. Further, these measures are stale as the BoC conducted the surveys in February before war broke out. Subsequent surveys are bound to show further increases. Watch the monthly CFIB survey measures of small business inflation expectations that lead the quarterly BoC surveys with another updated of those not due until July based on May responses.

Further, recall that back on March 18th in the earlier days of the war, the BoC struck out statement-codified reference to how it “judges the current policy rate remains appropriate.”

That made us nervous since you wouldn’t strike it out unless you were suddenly thinking there was the risk of a nearer term move and wanted to insert some optionality into the debate. On the direction of that possible move, it would be exceptionally unusual if they meant to signal a cutting bias into a massive positive commodity price shock in a commodity producing country. The natural influence may well have been that they signalled a debate between holding and hiking in future.

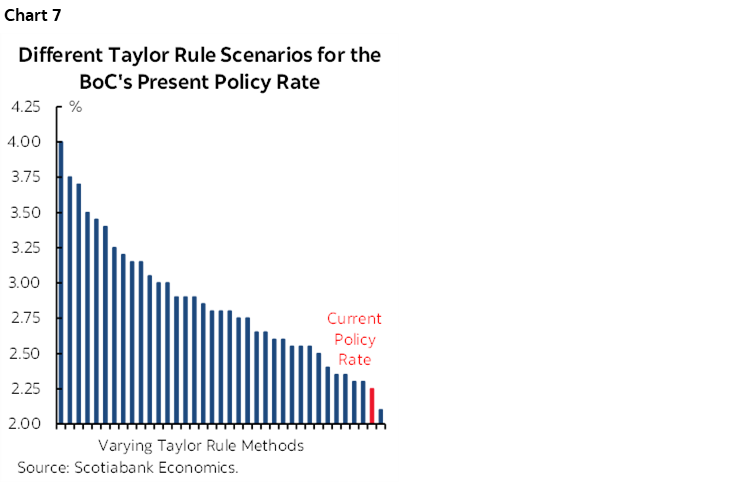

A Taylor Rule Approach—Policy Remains Easy

Under virtually any Taylor Rule approach, the Bank of Canada’s present 2.25% policy rate is significantly accommodative (chart 7). This chart goes back to using what I did here to show how anyone has access to a modelling approach to estimating Taylor Rule approximations for the policy rate by using ChatGPT. It’s a powerful tool that enables iterative and scenario-based approaches with assumptions and parameters you can change yourself. The BoC has been in accommodative territory on its policy rate because of uncertainty surrounding several forward-looking risks.

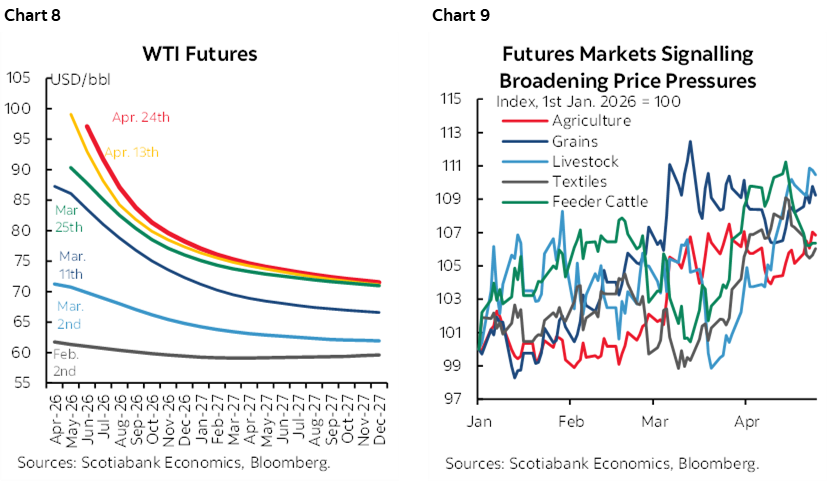

To be as deeply in accommodative territory in the face of a broadly positive commodity price shock (charts 8–9) may be less appropriate now.

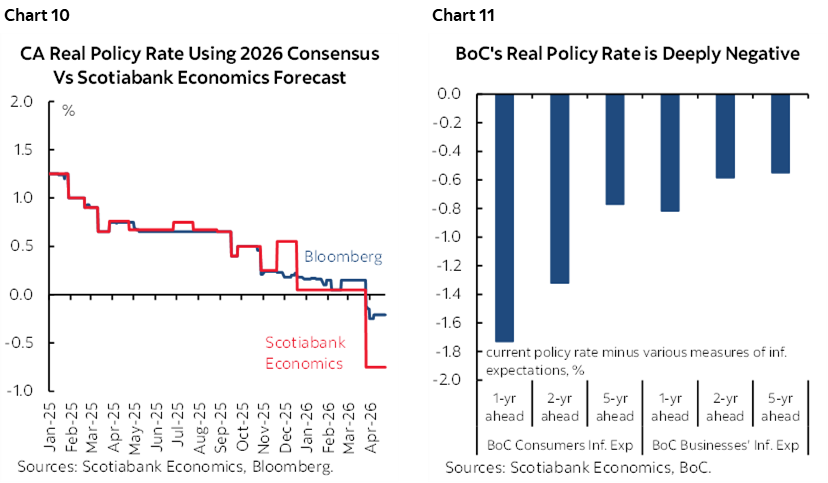

The real—inflation-adjusted—policy rate using one-year ahead forecast inflation has plunged to around -100bps (chart 10). The BoC has passively eased monetary policy by doing nothing in response to this commodities shock. If instead of our inflation forecast, we used expected future inflation drawn from the BoC’s surveys then the real policy rate remains negative throughout the projection period if they leave the nominal rate unchanged (also chart 11).

Key is how the commodity price boom sustains itself and whether the effects on inflation would be….dare we say it…transitory or more persistent and how this layers onto pre-existing motives for us to show rate hikes well before the war and commodities took off.

Our Forecast—We Had Forecast Hikes Even Before the War

Scotiabank Economics has had a forecast for +50bps in BoC hikes by the end of 2026 since our November 2025 forecast—not just since the war-driven commodity shock. Our view long pre-dated the move by markets starting in March of this year to price between 25–75bps of hikes over 2026H2 (presently 1½ 25bps hikes). We added one more H2 hike to a cumulative year-end target of 3% in our March forecast earlier this year, but even that wasn’t a cumulative addition as opposed to bringing forward 75bps into 2026H2.

We led consensus and markets and made money for clients who listened versus every single other voice on the street that continued to talk about further cuts and lost money for their clients who listened to them.

We argued last Fall that despite successfully forecasting two cuts that were delivered in September and October, the BoC was taking out insurance against downside risks that defied a Taylor Rule approximation that said they should not be cutting. Our model said no cut but we overrode it with judgement. Our argument at the time was that removing those insurance cuts and gravitating away from the bottom of the neutral range and toward the middle would be sensible over time within our 2026–27 forecast horizon.

Some foundations for this view at the time—and hence that predated the commodity shock—included:

- a dissipating impact on growth from trade uncertainty over time. The apex of that uncertainty was ‘Liberation Day’ and the greater distance from the shocks would be accompanied by movement toward a new equilibrium in the economy in terms of supply and demand;

- the release of some pent-up consumer and investment demand as distance from the shock grew;

- a tightening labour market through cutbacks in immigration policy that drive falling population;

- the addition of fiscal policy stimulus that the newly elected Carney administration was likely to begin introducing with haste and in multiple stages that are ongoing to this day;

- Positive upward revisions to GDP levels last Fall and smaller upward revisions to potential GDP that in our opinion meant less slack than previously judged;

- a narrowing amount of forecast slack and upside risk to the 2% inflation target;

- cautious optimism toward trade negotiations with the US as the outlines of a deal existed last Fall and still appear to exist today.

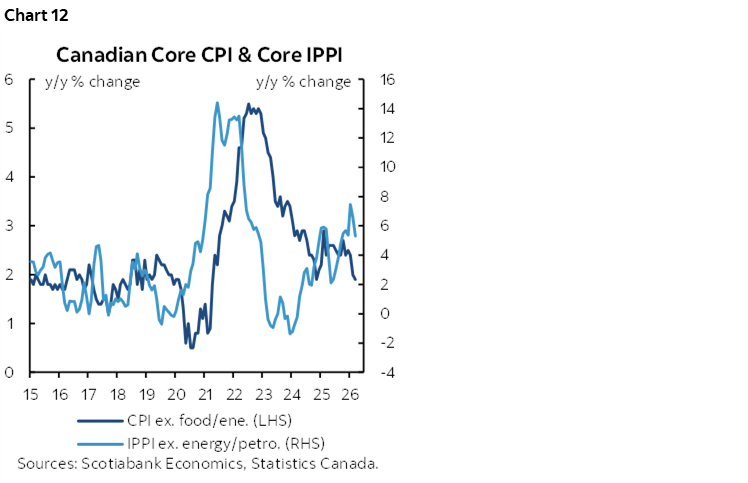

As argued here, we’re starting to see early evidence on reemerging from a temporary soft patch on core inflation with soaring trend industrial prices presenting pass through risk going forward (chart 12).

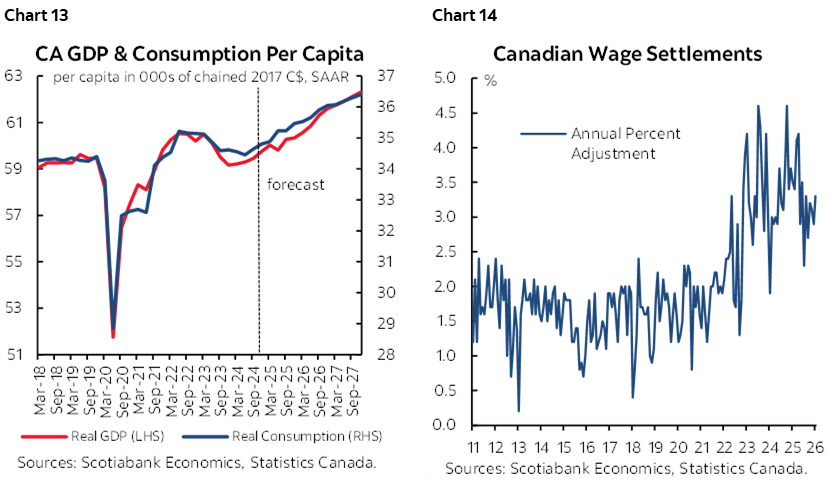

Also key to the argument was that per capita GDP and per capita consumption figures would begin to rebound and there is nascent evidence of this already happening (chart 13). Meanwhile wage setting exercises for the one-third of the workforce governed by collective bargaining agreements continue to cement gains well above the BoC’s inflation target (chart 14) absent supporting trend productivity to justify them.

Add to this views on trade negotiations such as ones I recently expressed here that argued Canada has the edge in trade negotiations with the US and the risk of a trade shock is commonly overstated.

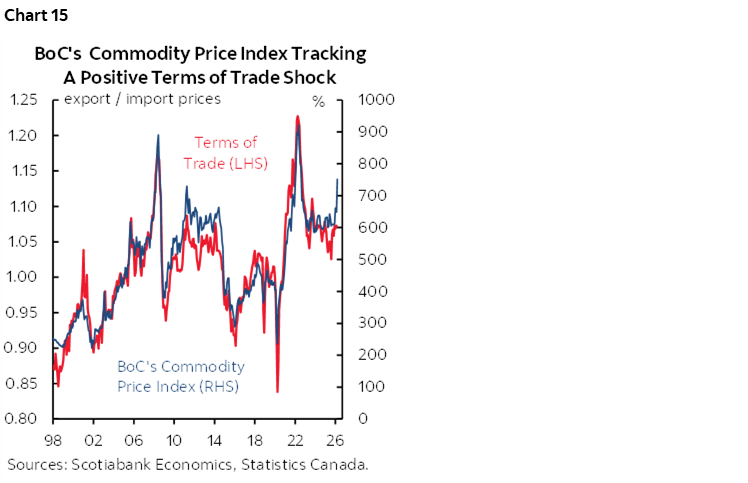

To this view is added the war and commodity effect. Broad-based commodity gains across futures markets benefit most of the commodities that Canada produces. The outcome is likely to drive higher terms of trade—the ratio of export to import prices (chart 15). The impact of selling exports at higher and more rapidly rising prices than imports should be to raise imported effects on aggregate national income for a significantly commodity-dependent economy.

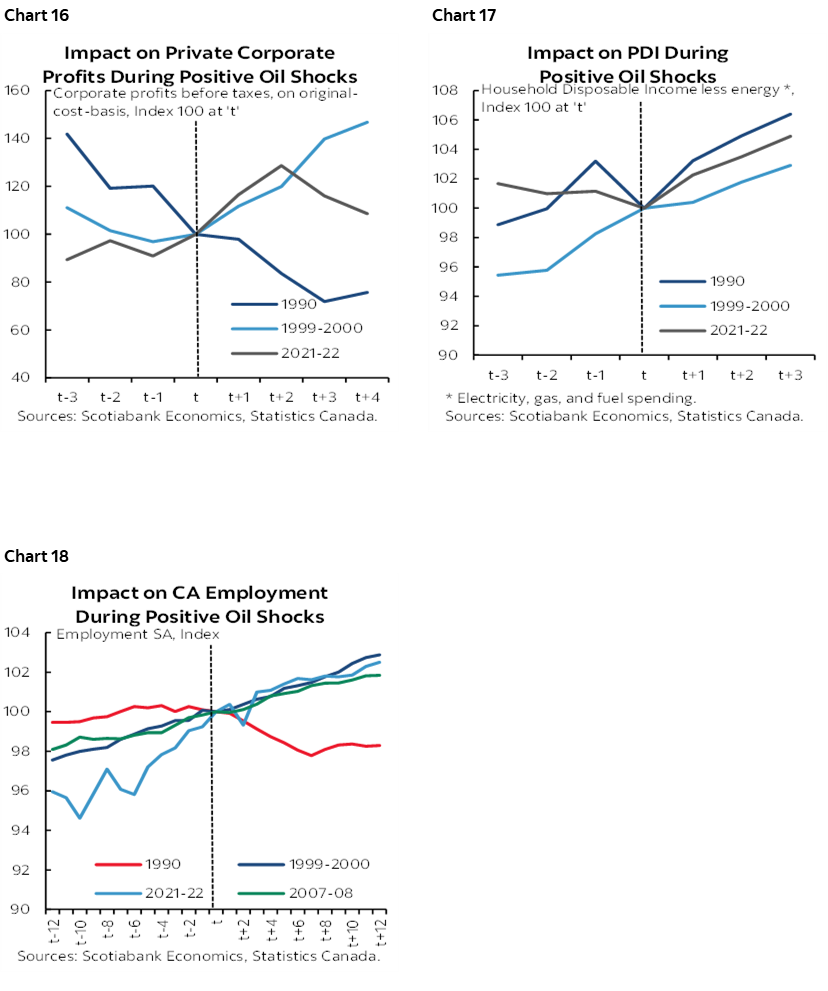

Historically when that has happened it has driven trickle-down benefits to incomes in broad sectors including improved fiscal balances which we are already seeing (see next section), aggregate growth in corporate profits (chart 16) and aggregate personal disposable income growth (chart 17) and employment (chart 18). The only main exception to this experience in reasonably modern times was the early 1990s when everything was going wrong through compounded shocks to the Canadian economy.

With more income it is likely that real activity will be generated. More spending and faster growth means the quicker elimination of spare capacity. Reduced spare capacity and more cost-push types of inflation risk translate into higher inflation risk.

On this count, bearish views on how consumers may be impacted by higher commodities could be dead wrong. Again. When oil prices spiked in 2022 on the heels of Russia’s invasion of Ukraine, Canadian consumers responded by smoothing the impact through dropping the saving rate almost toward zero and continuing to spend. The pattern was erratic following the pandemic but it wasn’t clear households spent less because of a commodity shock.

Higher cost-push inflation comes from cyclical, shock, and structural drivers. Cyclical drivers were already noted as part of the foundation for our pre-war rate forecasts. Structural drivers include being at a nascent stage of adjusting to long-tailed shocks to supply chains. Much like how China’s accession to the WTO in 2001 did not motivate immediately dovish inflation readings but had its influences over many years ahead, today could be similar. The past ten years has given rise to Brexit, Trump 1.0, the pandemic, Trump 2.0 and various geopolitical shocks. Border risk to supply chains is fundamentally higher as a result. Inventories are being held at higher levels as just-in-time has been replaced by just-to-keep-alive. Where to produce and under reconsideration. New markets, new suppliers, new production molds, and new workers all involve long-tailed costs to revamping supply chains and that doesn’t happen overnight.

Yet we’ve barely added much of anything to our BoC policy rate view because of commodities to date. We’re cautious. Should a commodity shock prove to be durable, continue to drive elevated inflation expectations and feed knock-on effects in transmitting price pressures into the core inflation basket, then more rate hikes than we are forecasting cannot be discounted.

This is because all that our rate forecast presently does is to remove insurance cuts and go toward the upper end of the BoC’s neutral rate range of 2.25% to 3.25%. A move into restrictive territory cannot be ruled out among various possible scenarios.

Risk Management Should Dominate

Overall what is key among the uncertainty is to adopt more of a risk management approach this time. The last time around, the BoC waited until it was staring a deep inflation problem squarely in front of it. By that point, it’s lights out, and the BoC had to hike by 475bps and more than it may have needed to by being more pre-emptive. Don’t make that same mistake again.

There would be little cost to a risk management approach that balances the risks through marginal and gradual tightening before having all of the answers. A 25bps hike would do little to the economy but would preserve the optionality to do more in sequence if needed, or to abandon tighter policy if all turns out to be just peachy.

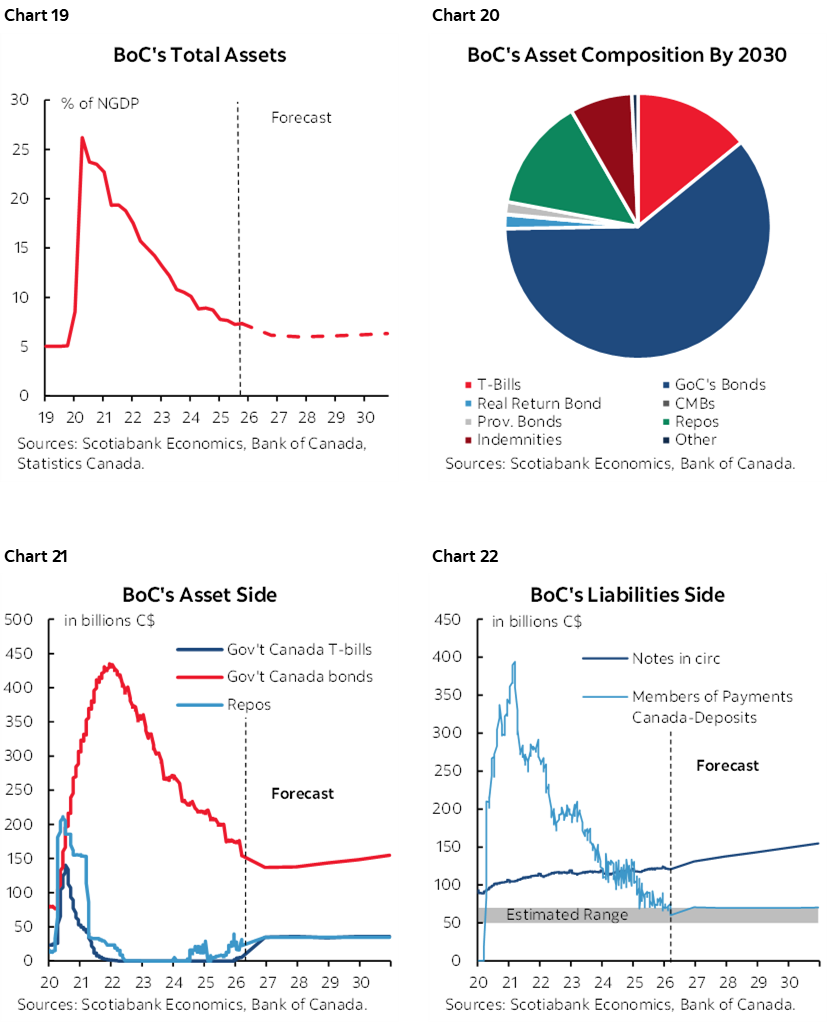

The BoC’s Balance Sheet—Earlier GoC Purchases?

Bond market participants should be prepared for updated guidance on balance sheet plans at some point possibly later this year. The BoC returned to expanding the balance sheet last year at first through repo activity and then t-bill buying late in the year. The next step involves gross purchases of Government of Canada bonds that has been guided to be on track for 2027.

Prior to the commodity shock, the BoC may have done so only well into next year. Charts 19–22 show our projections for total assets as a share of the economy, and the composition of the balance sheet.

We now face the possibility that faster nominal GDP growth due to the commodity shock could merit a bigger balance sheet in dollar terms to maintain a steady share of the economy. With quicker growth in NGDP goes possibly quicker growth in currency in circulation. Since the BoC is targeting a longer-run balance sheet that equates GoC holdings with currency in circulation this could merit earlier than previously planned gross bond purchases to more than offset maturities as they drop off the balance sheet.

It all depends upon high long NGDP is boosted, but earlier purchases are still not expected for quite a while yet. The point being to watch for guidance on this issue as the year evolves including any possible annual update by Deputy Governor Gravelle on the topic.

CANADA’S SPRING FISCAL UPDATE—OTTAWA IS ALREADY SPENDING ITS BONUS

The Government of Canada will issue its Spring Economic Update on Tuesday after markets close and hence just hours before the next morning’s communications from the BoC. It may be a relatively bland affair.

The Carney administration shifted timing of the interim update to the Spring instead of the Fall and the timing of the full Budget from the Fall to the Spring. Perhaps PM Carney’s time in the UK with its Autumn budget motivated the change. Perhaps it’s just an offshoot of the timing of last April’s federal election and the reluctance to issue a budget even last Fall when markets forced them to do so.

It’s imperative to emphasize that Ottawa’s routine playbook is usually to avoid big surprises on game days when these updates and full budgets are delivered. Advance announcements tend to reduce the intrigue by the time Minister Champagne stands to speak before the watchful eyes and ears of PM Carney after 4pmET on Tuesday.

In fact, there is a case for saying that the government has already pre-spent much of a positive shock to its finances.

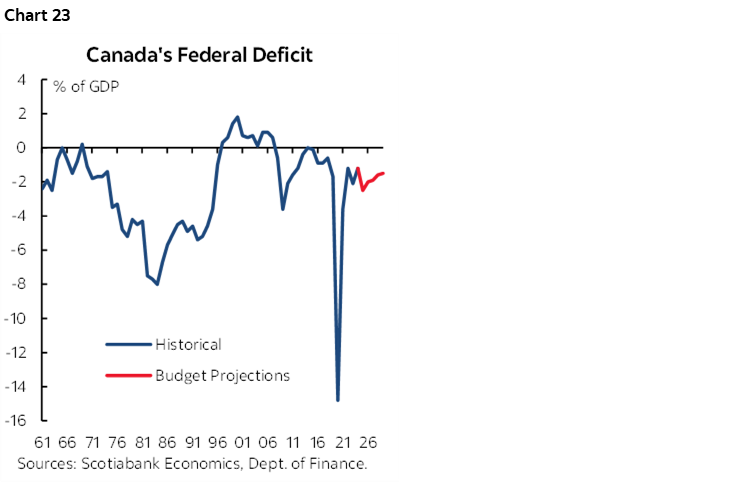

In any event, a full suite of updated tracking of fiscal plans including expenditures, revenues, deficits and financing is due. The Budget presented a deficit of C$78.3 billion in FY25–26 which was the biggest ever outside of the pandemic in dollar terms, but not even close to a record as a share of the evolving size of the economy (chart 23). On that, Canada looks much better than virtually anywhere else. It is AAA rated. The whole Canada curve sits well below the US Treasury yield curve partly because of less debt issuance, but probably more so because of weaker expected growth and productivity. Other levels of government benefit as well; witness Alberta that has been flirting with zero spread premium over the Feds.

The line-up of favour-seekers outside Finance Minister Champagne’s door is already long including small business associations (here). Ditto for the critics (here). The new FY26–27 fiscal year began on April 1st and so we’ll get a full update on the numbers for FY25–26 including the size of the deficit, gimmickry aside as to splitting operating and capital budgets.

The update occurs one day before the BoC’s April MPR communications which gives Governor Macklem an out in terms of not having to respond with analysis of any effects until July’s MPR—ages after most folks have forgotten about it. So much of independence. Yet Macklem may say that a first sniff of the update yields relatively minor effects on the outlook; a problem with this approach is its serial application to last Fall’s Budget, pre-announced measures in the lead-up to this update and the update itself. At some point it becomes misleading to dismiss the cumulative effects.

One key is the extent to which the commodities boom impacts its finances and how much of this will be spent versus put toward deficit reduction; I laughed to myself while typing the last two words. This is a government on a mission.

The surging price of oil presents a bonanza. Every US$10 rise in the price of a barrel of oil adds between C$1.5–3.5 billion to federal coffers per year. The increase since Budget day on November 4th 2025 has been three times this amount. If sustained, then it could mean between around $5–$10B per year. If they go by the WTI futures curve, then the impact could be just a few billion per year. This is among the reasons why the deficit should be tracking lower than previously guided if only for serendipitous reasons.

Yet they may have already spent this nice surprise in the short run. That could make the Spring update a somewhat boring affair. They have already announced several recent efforts.

One was the announcement in January about juicing HST transfers; the groceries benefit that had nothing to do with groceries (here). Call it Carney bucks, like Trudeau bucks, or Ford bucks, or Klein bucks. At the time of its rollout the minority Liberals may have been pump priming with another shot at an election in their sights, but unfaithful floor crossers have made this moot.

The PBO estimates the cost of this initiative to be C$12.4 billion over the next six years including over C$3B in the FY25–26 fiscal year and under $2B/year thereafter.

The effects of the one-time increase in payments in transitioning toward a relabelled benefit that is due to be distributed in June could more than double q/q annualized personal disposable income growth to over 6%. The trend line thereafter pivoted higher because of the 25% increase in payments thereafter for years to come. With consumption already tracking a strong Q1 gain as previously noted, the effect could sustain spending strengths at least over summer.

Temporarily suspending the federal fuel excise tax until September was more performative than substantive (here). The estimated C$2.4 billion cost in FY26–27 eats up some of the corporate income tax revenue surge from higher commodity prices.

Add it up and the commodity fiscal dividend to the Government of Canada appears to be getting spent on disbursements back to households and some businesses. This is how an imported positive income shock to Canada from higher commodities works through fiscal policy disbursements.

More may be on the way and will be evaluated once the plan has been presented.

For further detail, see this piece by Rebekah Young who champions Canadian fiscal policy and Canadian provincial economies in our group.

FEDERAL RESERVE—PASSING THE BATON

A fresh FOMC statement lands at 2pmET on Wednesday. It will be followed by Chair Powell’s press conference starting at 2:30pmET for 45+ minutes. There will be no Summary of Economic Projections and dot plot this time after presenting updates in March with the next one due at the June meeting.

Nothing much is expected from this meeting. The March dots showed the Committee median vote leaned toward one cut this year and one more next year. That’s unlikely to be settled for a long while yet. Powell is unlikely to be comfortable with teeing up such a move before his successor takes over and he faces eleven other voting FOMC members that are more worried about inflation at the moment.

Our forecast remains for one cut by late year and another in early 2027 which would drop the fed funds upper limit rate to 3.25% and hence still on the boundary between restrictive and neutral.

Markets and the Committee are focused upon what they can readily observe now: prices. Commodity prices are transparent including several commodity futures curves. Forecasters can infer inflation risk from the information contained within those curves and make assumption on pass through into core inflation, magnitude and persistence.

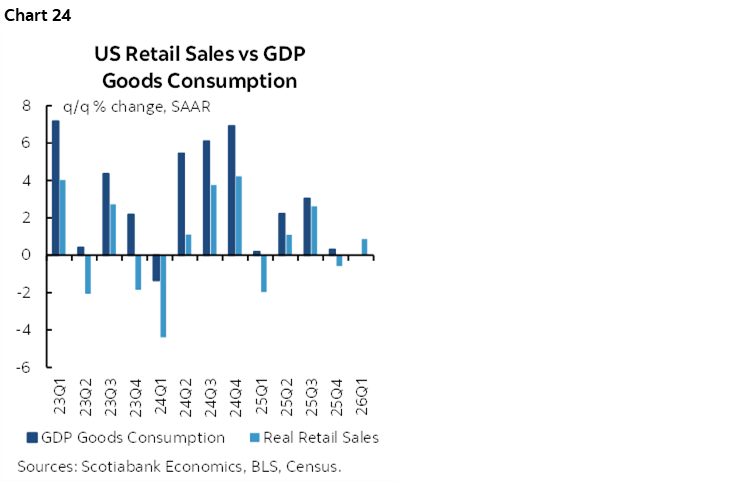

Much more difficult to do in real time is to assess how the economy and full employment side of the dual mandate hold up. We think that various forces will motivate weaker growth and correlated softening of employment trends. The consumer sector has been in a marked slowdown (chart 24).

This will be Powell’s last press conference as Chair. I respect his devotion to public service notwithstanding strong disagreements with various facets of his leadership especially as a cause of runaway inflation during the pandemic.

Kevin Warsh’s Senate confirmation vote was probably expedited by the Trump administration’s decision to drop its probe of Fed renovations. Senator Tillis (GOP) had expressed support for Warsh but demanded the probe be dropped or an alternate more independent investigation being substituted. His opposition to holding a vote is likely to be dropped and watch for a vote to be scheduled.

If I were Powell, I still wouldn’t trust the administration that could reintroduce a probe once Warsh has been confirmed and if Powell steps off the Board before he is technically entitled to remain until 2028. Powell will be asked whether this means he will step down and his answer could then inform whether the administration will nominate his replacement that could mean extending Governor Miran’s temporary position.

As for how Warsh seeks to change things up, see this note I wrote earlier this past week that I won’t repeat here. His idealism is likely to be checked by the Committee, markets, and Fed staffers while his inaction is bound to immediately place him in Trump’s line of fire.

For the rest of the central bank comments to follow from here on I’ve partnered with my colleague Jay Parmar.

ECB—WAITING FOR JUNE

The European Central Bank is unanimously expected to keep its policy rate unchanged on Thursday and to maintain a data‑dependent approach. Having just presented fresh forecasts in March, the next opportunity to issue fresh projections will come at the June meeting by which point greater information will be available.

While the ECB will see additional inflation prints and Q1 GDP data ahead of the meeting, it is still too early to assess the medium‑term implications of the Middle East conflict, given heightened uncertainty around its duration and intensity.

Markets are pricing less than a 10% probability of a rate hike at this meeting, with a full hike priced in for June. Against this backdrop, the ECB is expected to reiterate that it remains focused on upside inflation risks stemming from potential second‑round effects of higher energy prices, alongside downside risks to economic growth arising from the conflict. As such, the bank is expected to stand pat and await further data and clarity before reassessing policy with updated forecasts at the June meeting.

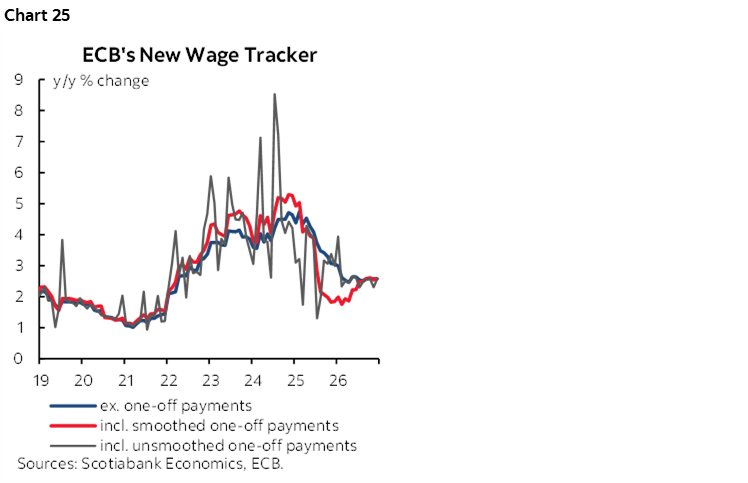

Some believe hiking would be inappropriate for the ECB given disinflationary damage done by higher commodities in a region that is a large net importer. Countering this view may be that the policy rate is at neutral—unlike the Fed’s mildly restrictive stance—and that inflation expectations, passthrough risk, and wage setting exercises present very different dynamics than elsewhere that could drive accelerating gains (chart 25). Among the scenarios that can’t be ruled out is temporary tightening much like which Jean-Claude Trichet delivered after the Global Financial Crisis.

BANK OF JAPAN—HAWKISH CUES?

Markets are leaning toward no policy rate change on Tuesday (Monday 8pmET), while assigning a roughly 60% probability to a rate hike in June and fully pricing in a hike by the July meeting with another by year‑end.

Consensus expectations also favour no change at the upcoming meeting, although a minority anticipate a 25bps hike. Recent spring wage negotiations delivering wage increases of more than 5% for a third consecutive year (chart 26), alongside back‑to‑back gains in real wages at the start of the year following two years of declines, strengthen the case for the Bank to move toward monetary policy normalization.

However, the Middle East conflict, elevated energy prices, and uncertainty over the persistence of these pressures are likely to argue for additional time to assess the impact on growth and corporate earnings, with potential spillovers to wage dynamics and inflation. As such, attention will centre on the updated economic projections.

BANK OF ENGLAND—A NEW SHOCK COMPOUNDS RESIDUAL INFLATION

After a hawkish hold in March, the Bank of England is unanimously expected to deliver another hold on Thursday, with markets fully pricing in a 25bps rate hike by the July meeting.

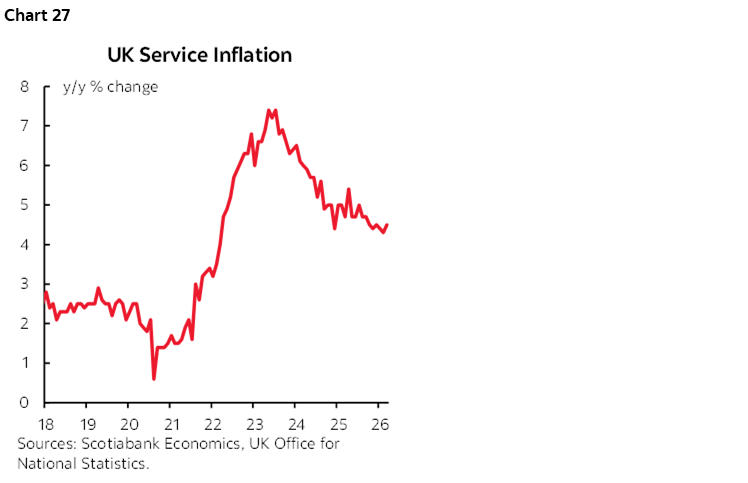

A first consideration is the debate over whether the BoE had conquered inflationary dynamics that preceded the commodities shock. CPI was persistently running above target on headline and core measures, services inflation has continued to run much hotter than total CPI (chart 27), and wage growth remains well above the BoE’s inflation target absent trend productivity gains to support it.

With energy prices remaining elevated into the second month of the conflict, the bank is likely to remain cautious about potential second‑round effects, keeping a close focus on wage and price‑setting behavior as well as sticky services inflation.

However, there are increasing signs of weakness in economic growth and the labour market, which could also weigh on inflation dynamics. The upcoming meeting will mark the bank’s first update to its economic forecasts since the onset of the conflict. Given heightened uncertainty around the duration and persistence of the oil price shock, it may opt for scenario‑based projections.

Overall, the bank is likely to require more time to assess the impact of the conflict and remain data‑dependent in the meantime.

BCCH—EXTENDING THE HOLD

Our LatAm team expects the Central Bank of Chile to maintain its overnight policy rate at 4.50% on Tuesday and to remain data‑dependent pending greater clarity on the Middle East conflict and its potential impact on the domestic economy. As expected, inflation increased in March, driven by higher energy prices, while economic activity showed further weakness ahead of the conflict. As a result, the bank is likely to stay on hold amid elevated uncertainty and broadly balanced risks

BANK OF THAILAND—NO FOLLOW-UP

After a surprise 25bps cut in February, the Bank of Thailand is unanimously expected to keep its repo rate unchanged at 1% on Wednesday. Based on recent comments, the bank's near-term bias remains focused on supporting economic growth, despite upside risks to inflation, which remains in mildly negative territory. The Governor noted that "inflation will definitely accelerate with oil price hike and supply disruptions, but we will refrain from raising the interest rates as long as possible because higher interest rate will not dampen inflation".

BANREP—CONTINUED DIVISIONS?

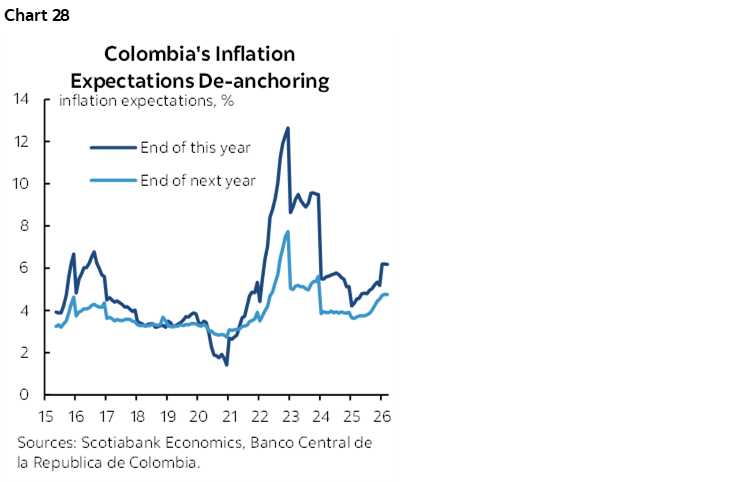

Following back‑to‑back 100bp hikes at the start of the year, and amid escalating tensions between the federal government and the central bank ahead of elections next month, expectations for Thursday’s meeting are split between a hold and a 75bp hike, reflecting deep divisions within the Governing Council at the previous meeting. Governor Villar has highlighted rising core inflation and inflation expectations (chart 28) —driven in part by minimum wage increases—supporting the case for aggressive tightening, with inflation now unlikely to return to target this year. The latest inflation expectations for both this year and next year continue to de‑anchor. An additional risk stems from uncertainty over the Finance Minister’s attendance, which could prevent a policy decision from being taken at the meeting.

BCB—EASING OFF A DEEPLY RESTRICTIVE STANCE

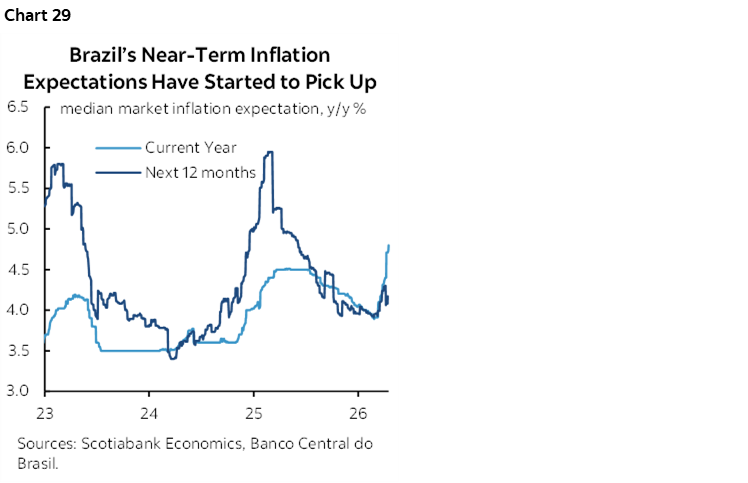

After starting to ease at the March meeting, Banco Central do Brasil is expected to continue calibrating its policy rate with another cautious 25 bps cut on Wednesday, while maintaining a restrictive policy stance. However, greater caution is warranted given the rise in upside risks to inflation since the last meeting. Recent inflation data surprised to the upside, and inflation expectations remain de‑anchored above the 3% target, with current‑year expectations edging higher (chart 29). Services inflation and economic activity also remain resilient. That said, the real has strengthened recently against the U.S. dollar, providing some relief. As such, attention will focus on any guidance regarding the pace of the “monetary policy calibration cycle.”

GLOBAL MACRO—A LONG “A” LIST

A heavy line-up of global macro indicators will include GDP reports from Canada, the US, and Eurozone, inflation readings from the US, Eurozone, Australia and Peru, plus Chinese PMIs as some of the ‘A’ list offerings on tap.

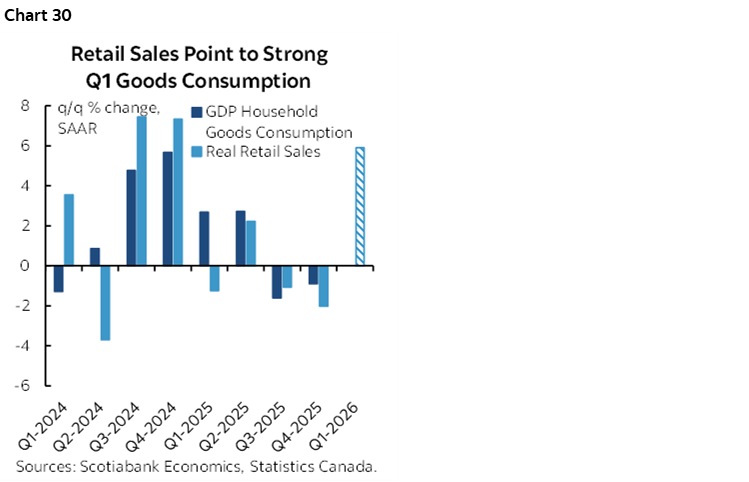

CANADA—Q1 ON TARGET?

Canada reports GDP for February and the preliminary estimate for March on Thursday.

February was initially guided by Statcan to have been tracking a 0.2% m/m gain last month. Updated estimates are still in the same ballpark but we’ll also get important details on sector drivers. More meaningful may be the flash guidance—sans details—for March GDP for which there is very little information thus far but a small gain is feasible.

The outcome will further inform Q1 GDP growth tracking on a production/income basis using monthly GDP. It’s feasible that growth is tracking close to the BoC’s 1.8% January MPR estimate but that’s on an expenditure basis. The massive 4%+ inventory drag on Q4 GDP could reverse as an added upside.

One key is that consumer spending on goods is tracking a strong rebound in Q1 based on retail sales volumes (chart 30). It’s untrue that the economy is not exhibiting rate sensitivity—a view that is disproportionately driven by a false understanding of what’s keeping condo markets weak in Toronto and Vancouver.

US—GDP MAY BE THE KEY

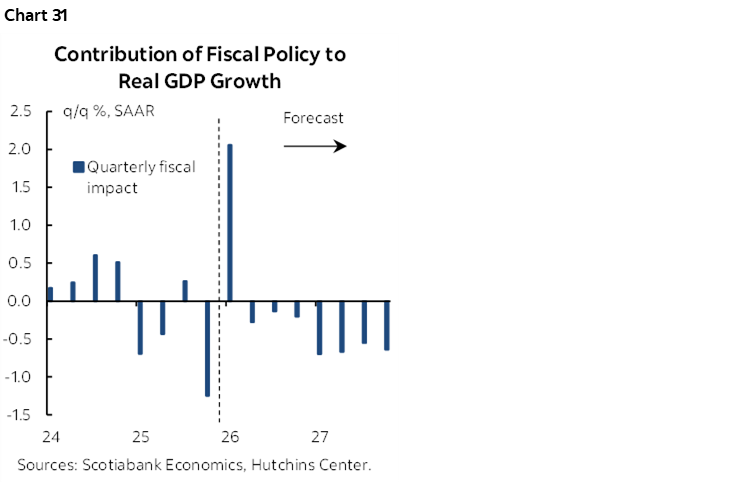

The first estimate for Q1 GDP lands on Thursday. It will start the rolling revisions until we get a firmer understanding, but the figures may look very different under the hood.

Q1 US GDP growth is tracking a rise of 3% q/q SAAR by our tracking. Don’t be fooled by illusory gains.

The reason for saying this is that Q1 GDP growth may be strong only because of the effects of the government shutdown. The Hutchins Center at the Brookings Institution estimates that fiscal policy will make a weighted contribution of over two percentage points to q/q SAAR Q1 GDP growth (here and chart 31).

Beyond that there won’t be much else. We figure that Q1 consumption was up by just 1.2% q/q SAAR which makes a weighted contribution of around ¾%. Net trade is tracking a modest positive contribution as much of the weighted impact of export growth was offset by the weighted impact of strong imports. Inventory effects look to contribute a small positive to growth. Ditto for broader investment.

What this leaves us with is emphasis upon private final domestic demand by excluding government, inventory and net trade effects (ie: just consumption and gross private investment) to show an economy that is rather weak. This measure grew by just 1.8% q/q SAAR in Q4 with GDP up by only 0.5% q/q SAAR as government dragged growth lower. Clearly the US economy lost momentum over the past six months.

The US calendar will also include the following measures:

- House prices (Tuesday): February’s estimate could make it seven consecutive gains in a row for repeat-sales measures which is weighing against, say, Fed Governor Miran’s dovish views on housing influences upon inflation.

- Dallas and Richmond Fed (Monday, Tuesday): April’s manufacturing indices follow gains in the Empire and Philly measures on the path the Friday’s ISM-manufacturing print.

- Consumer confidence (Tuesday): April’s measure may be vulnerable to what was previously resilient confidence in February and March as the war’s effects of affordability become more acute. Watch measures like inflation expectations and jobs plentiful.

- Advance trade (Wednesday): March’s export and import figures will inform the merchandise component of the overall trade balance. We’re flying blind because the government shutdown meant no updates to this measure since figures for December.

- Housing starts (Wednesday): March might be about some payback for the prior month’s strong gain in relation to permit activity.

- Durables (Wednesday): Airplane orders could contribute to another decent headline gain but key will be how orders for core capital goods (ex-defence and air) and holding up into the war’s effects.

- Personal income and spending (Thursday): Personal income growth could be fairly buoyant given a rebound in payrolls and tax refunds that while disappointing so far are still higher than prior years. Retail sales point to strong growth in the value of spending for the month but a soft overall Q1.

- PCE and core PCE inflation (Thursday): March’s total PCE inflation is likely to be quite strong with a gain around 0.7% m/m SA as it follows CPI and PPI. Core PCE inflation ex-food and energy, however, is expected to be tamer at about 0.2% m/m SA.

- Jobless claims (Thursday): Trend readings at fairly low levels are expected to continue.

- Employment Cost Index Q1 (Thursday): Another strong gain of about 0.8% q/q SA nonannualized is expected for combined wages and benefits.

- ISM-mfrg (Friday): I went with a small gain in April’s reading of manufacturing sector activity on the heels of the S&P PMIs that indicated advance order front-running to get ahead of higher prices across manufacturers in the US and elsewhere (here).

- Vehicle sales (Friday): April’s reading is expected to slip to below 16.0 million vehicles sold at a seasonally adjusted and annualized rate. This is based partly on industry guidance that is slightly shaved for possible late month sales softness.

EUROZONE—INITIAL SHOCK EFFECTS

The European Union’s upcoming data releases will shed further light on inflation pressures amid the second month of the Middle East conflict and persistently high energy prices, as well as on Q1 growth momentum ahead of the ECB’s monetary policy decision on Thursday.

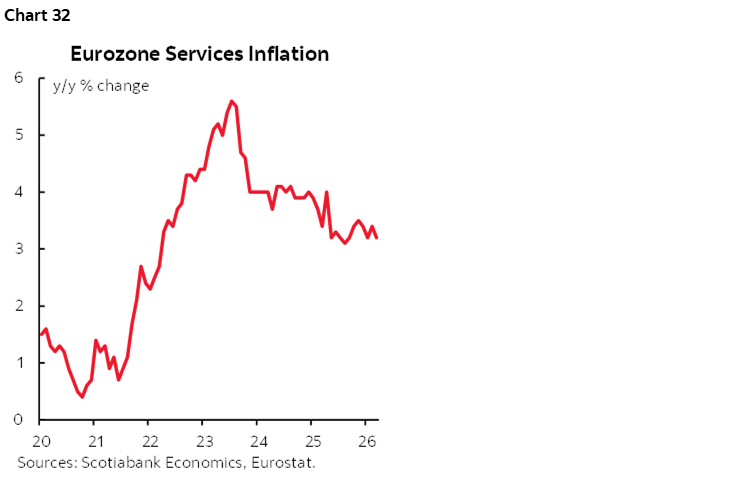

April inflation prints for Spain and Germany are due Wednesday, followed by France, Italy, and the euro area aggregate on Thursday. Eurozone headline inflation is expected to accelerate to 2.9% from 2.6% in February, while core inflation is seen remaining stable. The focus will be on the composition of the data, particularly early signs of broader pass‑through effects and the resilience of service inflation (chart 32).

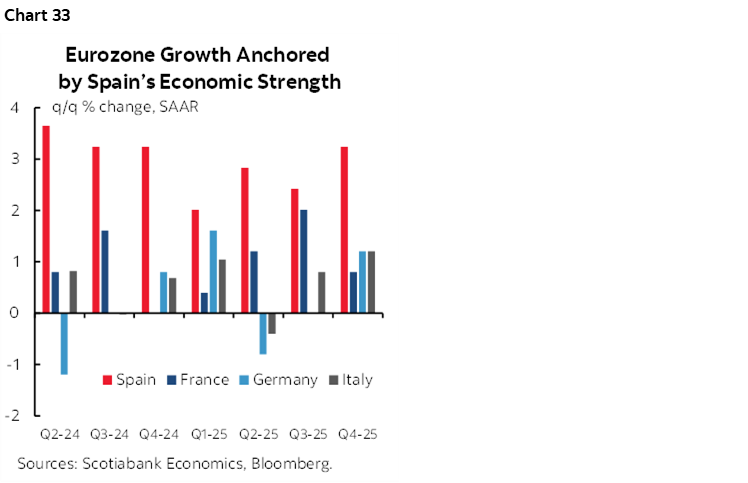

Alongside CPI releases on Thursday, Q1 GDP figures for the four largest euro area economies and the aggregate eurozone will be published. Consensus expects modest growth of 0.2% q/q SA. Key will be whether Spain continues to anchor euro area growth (chart 33).

Overall, the data are likely to be treated as placeholders ahead of the ECB meeting, with markets focusing less on the headline prints and more on underlying trends relevant for the policy outlook. Key will be duration and breadth of the shocks to growth and inflation which these reports will only partially inform.

ASIA-PACIFIC—AUSSIE INFLATION, CHINA PMIS, JAPAN’S DATA DUMP

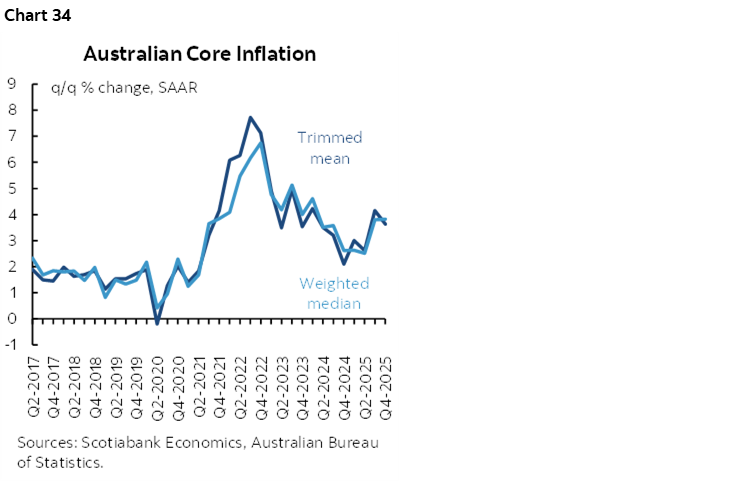

RBA watchers will be closely focused on the bank’s preferred core inflation measures (chart 34)—trimmed mean and weighted median—in the Q1 CPI release, the last major inflation input ahead of the May 5th monetary policy meeting. Markets are currently pricing a 75–80% probability of a 25bp rate hike in May. Consensus expects the Q1 trimmed mean to rise by 0.9% q/q, with any upside surprise likely to reinforce expectations for tighter policy at the upcoming meeting.

In China, April official PMI readings due Wednesday are expected to soften slightly, while the private Caixin manufacturing PMI is forecast to edge higher by a couple of ticks. This will be followed by the private services PMI release in the following week.

Japan will release a series of economic indicators this week following the Bank of Japan’s policy decision on Monday, offering further insight into domestic demand and price dynamics. The data flow begins with March’s unemployment rate on Monday, followed by March retail sales on Wednesday, and concludes on Thursday with March housing starts and April Tokyo CPI.

LATAM—PERU’S INFLATION

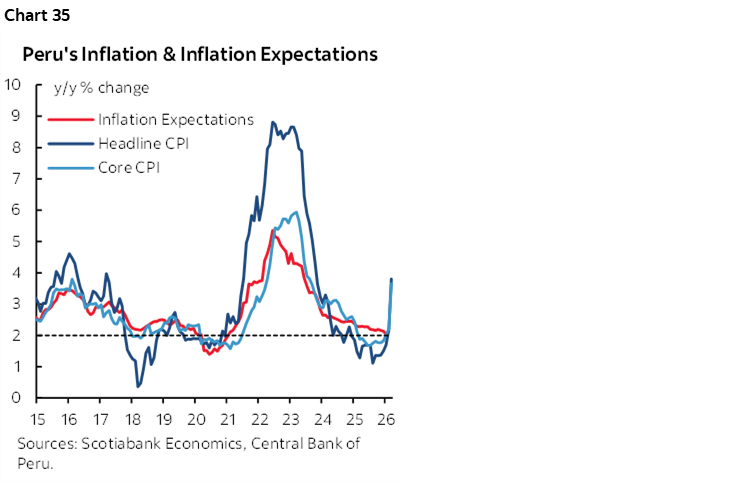

Finally, Peru’s April inflation print on Friday will provide further insight into inflation pressures following March’s upside surprise driven by higher energy prices and core inflation (chart 35). It’s the last reading before the May 14th BCRP decision following the recent holding pattern. With the BCRP expecting inflation to remain temporarily near the upper bound of the target range temporarily, the key focus is the energy pass‑through to core inflation as well as inflation expectations. Still, we wouldn’t expect the central bank to rock the boat with the run-off second stage Presidential vote scheduled for June 7th.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.