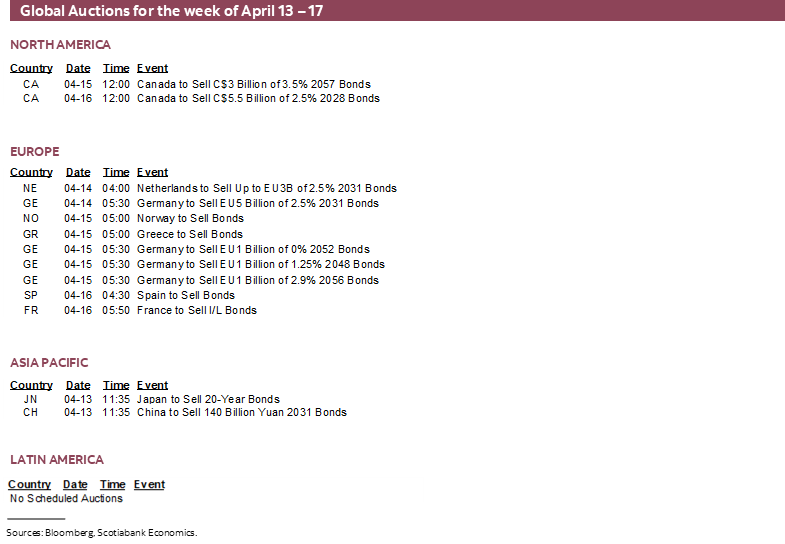

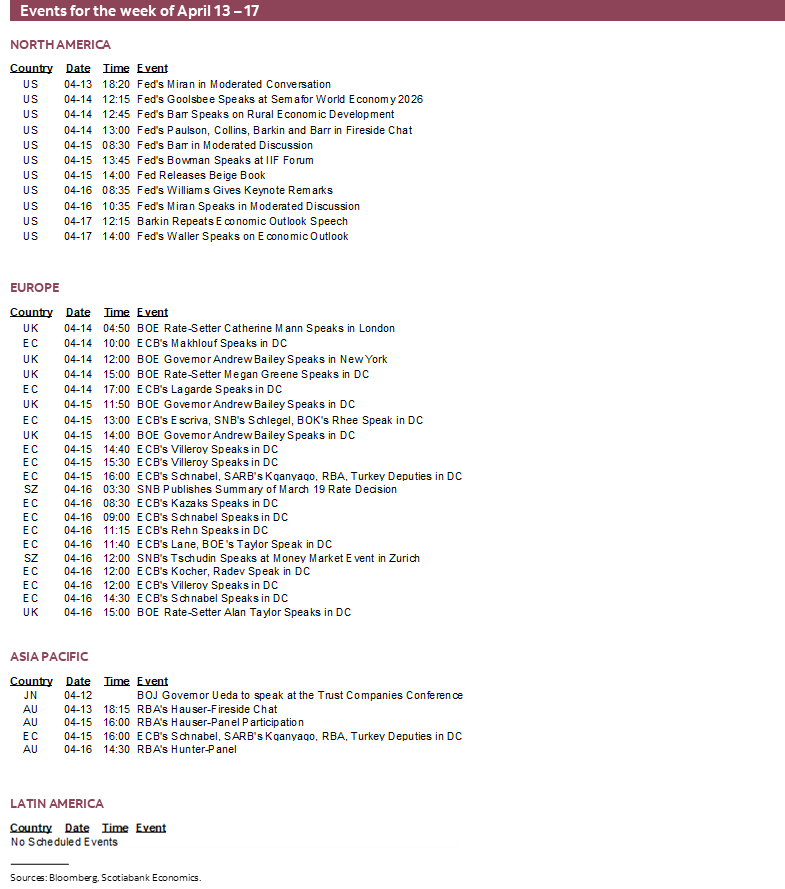

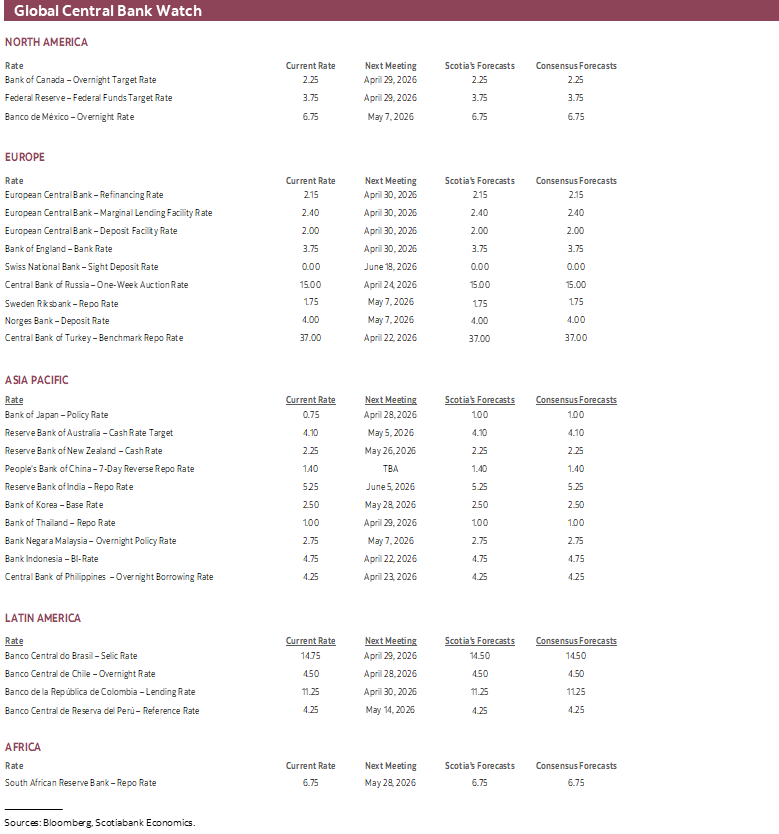

Next Week's Risk Dashboard

- US-Iran negotiations kick off amid widespread disagreement, elevated risk

- The Q1 US earnings season starts with financials

- US financial regs & the cycle — right time for a lighter touch?

- Canada is very likely to have a majority government this week

- Orbán out? Hungarians paid a steep price during his tenure. Literally.

- Warsh’s delayed confirmation process is rather complicated

- Peru’s first round Presidential election unlikely to reveal a winner

- Aussie jobs report to segue into the next RBA decision

- Strong data due in Canada

- US producer and import prices likely surged

- China’s economy is still looking resilient

- Global macro

Chart of the Week

An eventful week with more to it than war talk lies ahead. Hooray!

US earnings season kicks off in earnest amid profound regulatory movements at a fragile point in the outlook. Elections will give Canada a majority government and could oust Hungary’s Orbán after a sixteen-year run that cost Hungarian pocketbooks dearly. We might learn more about when Kevin Warsh’s Senate confirmation hearing could be scheduled along a potentially long and complicated path. Several global macro readings will aid our understanding of developments in China, the UK and Australia.

FRAGILE NEGOTIATIONS TO COMMENCE

But let’s start with war talk, bwah. Clearly financial markets will be strongly tuned into talks between the US and Iran that may begin on Saturday in Islamabad, Pakistan. WTI futures prices remain elevated and in fact really haven’t signalled any move lower across future months into 2027 (chart 1).

The air will be charged with mistrust on both sides. Frankly, the way both sides are talking before they’ve even sat down makes it sound like there are remote odds of some grand agreement. Guidance points to talks that could extend over two weeks. The people concentration risk will be skyward as officials meet at one hotel—that booted its existing tenants—albeit amid strengthened security. Media reports indicate that US VP Vance, envoy Steve Witkoff and Trump’s son-in-law Jared Kushner are to lead the US delegation presumably with Trump on speed dial. Iran is sending Parliament Speaker Ghalibaf and Foreign Minister Abbas Araghchi to lead talks. Ghalibaf said on Friday that a ceasefire in Lebanon and the release of Iran’s seized assets must occur before negotiations begin.

Perhaps the negotiators would benefit from reading this piece that I enjoyed on parallels to prior experiences during the first Gulf War and the potential pitfalls to avoid this time. It’s a compelling read that cautions against repeating the varied steps leading to the many years of conflict after the Gulf War of 1990 followed by the invasion of Iraq in 2003 and ultimately 9/11 and the war in Afghanistan.

Yet the sides are far apart on demands. Iran demands the lifting of all primary and secondary sanctions on Iran and Trump has indicated this is in negotiation. Iran also wants control over the Strait of Hormuz including the right to charge fees that are reportedly already being charged, to which Trump retorted “they better not be and, if they are, they better stop now!” Iran has demanded that US forces leave the Middle East; fat chance. Iran has also demanded an end to attacks and assurances they won’t be attacked again in future; whether this is agreed upon is unclear, but it would be worthless anyway. Iran wants freezes on its assets abroad to be lifted. Iran also wants the US to accept enrichment of uranium for its nuclear program with the Russians already reportedly helping; this is highly unlikely. Lastly, Iran has stated that attacks on Lebanon and Hezbollah must stop; this would require greater success by the US in controlling Israel.

What we may be left with is intense risk that negotiations could fall apart at any moment, while a broad agreement would take an extended time to achieve while other parties like Israel and neighbouring countries like Saudi Arabia and the UAE have a strong stake in success or failure of any deescalation. So does Russia. Putin’s economy is one part war machine, one part energy-driven with the latter funding the former; he has every incentive in the world to maintain high oil prices through a variety of means, perhaps including false flags.

WARSH’S CONFIRMATION HEARING IN LIMBO

Federal Reserve Chair-nominee Kevin Warsh might have had his confirmation hearing this week on Thursday before the Senate Banking Committee until anonymous sources told newswires it would be delayed. There is nothing on the official Committee calendar, but his hearing could be inserted at any moment. If so, then he would deliver prepared opening remarks (Powell’s from 2022 are here) and would then be grilled by the members.

When it does happen, Warsh may be disinclined to avoid stepping on Chair Powell’s toes. Warsh has been openly critical of Powell’s approach during the pandemic and critical of the Fed in general. He has previously indicated a strong bias toward thinking of AI as disinflationary and possibly opening up room for easing. His remarks could be impactful to markets looking to pricing the Fed over the back half of this year. He nevertheless faces a very sceptical Committee of eleven others that has turned more hawkish as measured by attempts to assess the composition of their language (chart 2).

One reason the hearing could be in limbo is that GOP Senator Tillis remains adamant that he will not vote for Warsh until the Trump administration ends its criminal probe into Chair Powell’s alleged role in renovations of the Eccles building. He has said he could dig in for the rest of this Congress until a new one convenes in January. It won’t get to that, but if it did, the Committee’s composition could be drastically different.

In order to proceed to a full vote in the Senate, Warsh’s nomination must first pass the Committee. Tillis could place a ‘hold’ on the nominee that would delay the proceedings, but Senate leadership can ultimately override a filibuster attempt and force a majority vote.

Enter the second problem. The GOP has a slim majority on that Committee of just 13–11. A simple majority is needed to advance Warsh’s nomination. Should Tillis vote against then he could thwart the nomination. There are other complicated tactics that could circumvent Tillis’s opposition, but they involve delays and uncertainty.

Afterward, the full Senate vote is also conducted on a simple majority basis. Warsh is very likely to be confirmed but the process is more complicated due to the unjustified criminal proceedings against Powell. So is the path thereafter given Powell’s determination to remain as a Governor for as long as the criminal proceedings continue which holds up other developments on the Board of Governors at the Fed.

US EARNINGS SEASON—TIME FOR A LIGHTER TOUCH?

The start of another US quarterly earnings season will be a welcome change of pace from war, tariffs, and what the Fed should do. It starts in earnest on Monday when key financials begin releasing. Chart 3 shows analysts’ expectations for EPS.

First up will be Goldman Sachs on Monday which has a knack for making money whatever the circumstances. Blackrock, JPM, Wells Fargo, and Citi follow on Tuesday. BofA and Morgan Stanley (Wednesday), Keycorp—of relevance to my employer—releases on Thursday along with Netflix, followed by State Street on Friday. Some other regional players in the US banking industry also release over the week as part of the roughly 30 S&P names to release.

Top of mind may be the credit cycle, provisioning in a weakening economy, and risks to private market exposures all in the context of regulatory changes that eased standards. Forward guidance on how lenders anticipate their behaviour to evolve may count more than their backward Q1 earnings.

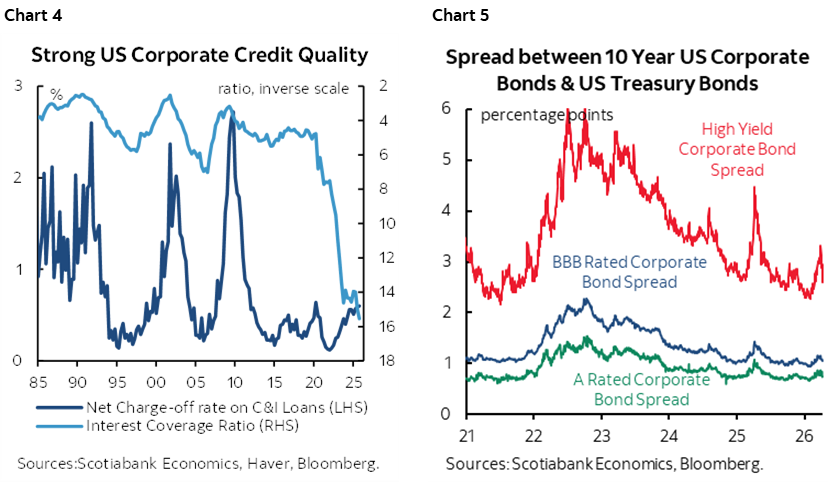

US corporate credit quality generally remains robust. Chart 4 shows impressive heights in EBITDA coverage of interest expense and how interest coverage—plotted on a reverse scale—explains much of why net charge off rates on commercial and industrial loans remain quite low. This is one consideration behind still-tight corporate bond spreads (chart 5).

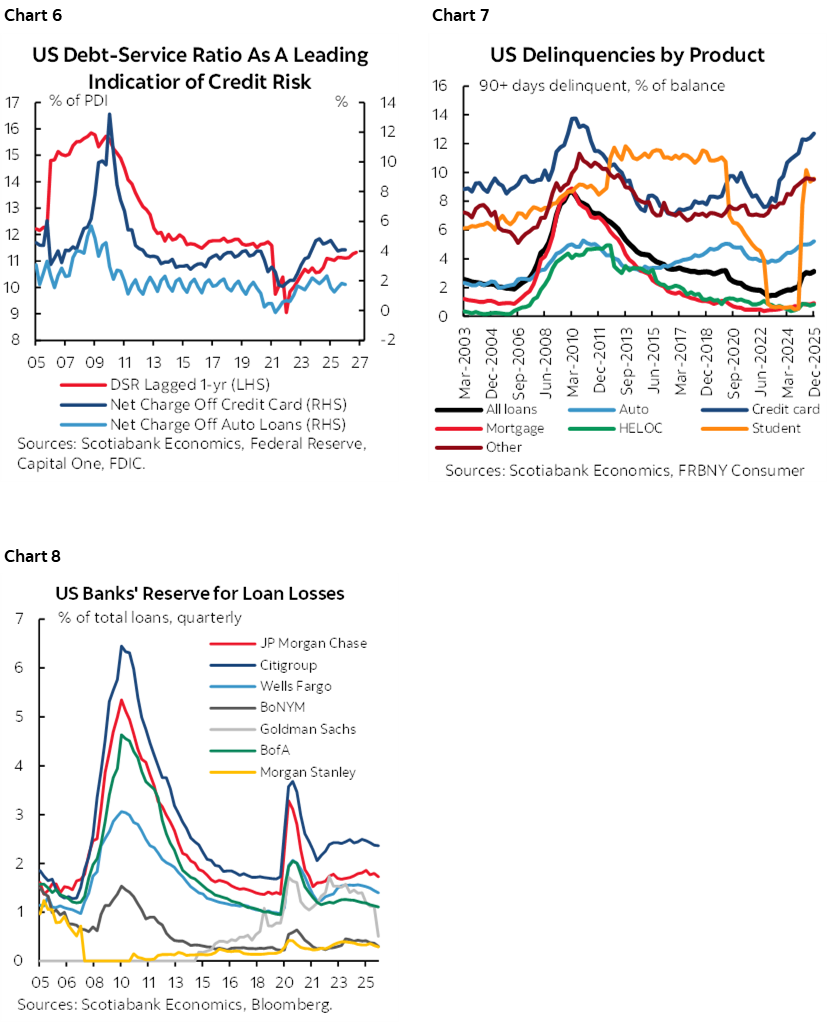

US household credit quality is generally sound but with some cracks. Chart 6 shows the charge-off rates on cards and auto loans connected with the household debt service burden. Chart 7, however, shows rising seriously delinquent accounts. Chart 8 shows bank provisioning for bad loans.

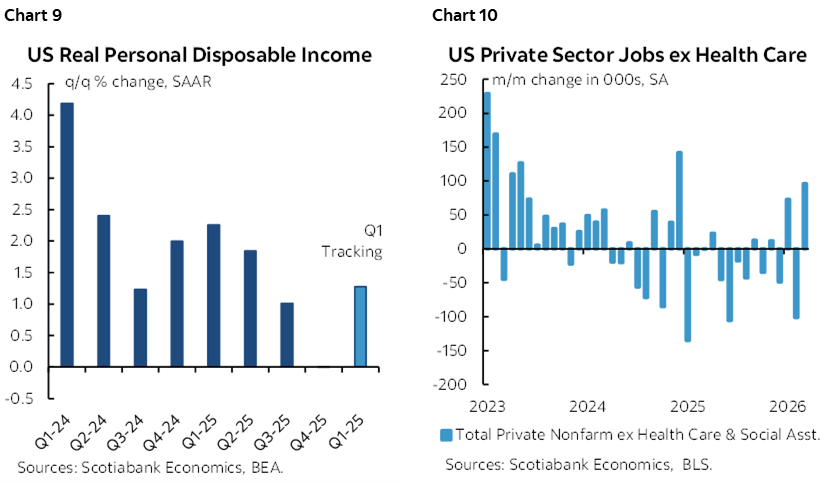

The backdrop to this is a weakening US economy. Little to no inflation-adjusted disposable income growth has been registered over the past three quarters (chart 9) while private payrolls—ex-health care that has been marching to its own drummer—have been volatile with many more downs than ups of late (chart 10).

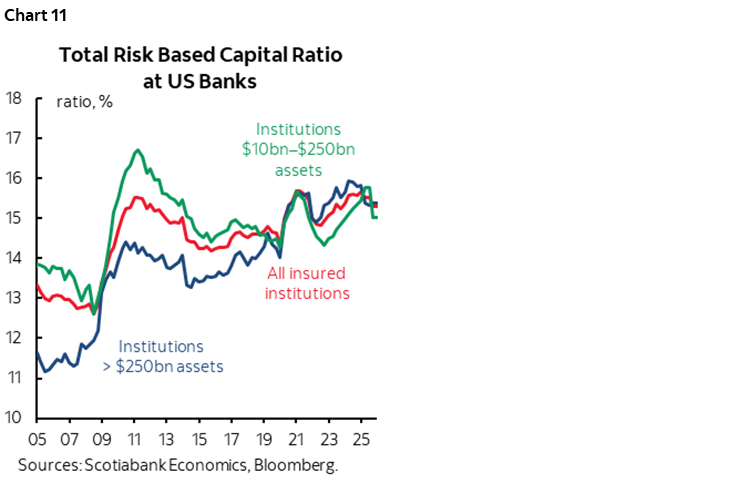

US banks are generally well capitalized (chart 11).

Yet much of the focus in the management dialogue on calls and in formal releases may be upon exposure—directly and indirectly—to private credit and private equity. A good general primer on the issues is available here. Returns on the funds have fallen as capital allocated to them has exploded in an elevated rate environment as some of the funds merely represent more leveraged exposure to tech valuations all the while as restrictions against redemptions have amplified investor concerns.

Post-GFC regulatory changes pushed this activity out of mainstream banks into the less regulated sphere—that is, until recently. The OCC’s decision in December of last year to abandon the 2013 restrictions on banks’ leveraged lending in favour of prudent risk management was explicitly designed to bring the risks back into the core banking sector where they can be more directly overseen by regulators. This is a total about-face from the post-GFC desire to make the banking system sounder. The extent to which banks take the bait into this market will be closely observed.

In parallel to such changes is the move to reduce capital standards in the US banking sector that was announced by the Federal Reserve last month. As this piece articulates, these reforms may drop large bank capital requirements by about 2½% that when combined with reforms to stress tests would amount to a cumulative reduction of about 5%.

Also working alongside such efforts is Trump’s desire to open up the US$9 trillion retirement savings market to investments in private equity, private credit, crypto and other assets generally deemed higher risk. Last August’s executive order (here) gave 180 days for the Department of Labour—that sets the rules for retirement plans—to complete its reexamination of prior restrictions. That review resulted in this proposal for public feedback. The broad message leaned toward prudent person principles in driving investment choices within 401k plans:

“The department’s days of picking winners and losers are over. Our rule clearly spells out that managers must evaluate any and all potential product offerings by following a prudent process. This proposal is decidedly neutral and refrains from saying that any asset class is any better or worse than other investment types, as the law requires.”

Watch for guidance on how banks plan to manage through all of this regulatory change once implemented after consultation phases. Will they guide increased appetite for lending into a questionable set of risks governing the US economic outlook? Will they pay out in dividends and buy-backs? Will they launch another wave of consolidations? Will they pay themselves more handsomely? Will they follow the money toward liberalized asset classes? The balance that is struck will help to inform the balance on risk and reward facing the banks and the broader financial system.

This uncertainty is precisely why some key Fed officials do not support the capital deregulation such as Governor Barr’s statement issued on the same day as the Fed’s announcement lowering capital standards.

ELECTIONS—MAJORITY IN CANADA, ORBÁN POSSIBLY OUT, AND HERE WE GO AGAIN IN PERU

Three sets of elections will be held into the start of the week. One matters geopolitically, and the other two are of consequence to Canada and Peru.

Canada is Very Likely to Have a Majority Government by Monday

Canadian PM Mark Carney will likely secure a majority government by Monday evening once the results of three byelections roll in. Carney’s mandate is therefore likely to extend without having to face voters again until 2029.

The outcome could lend supportive stability to the Canadian dollar and domestic markets while emboldening the Carney administration to more aggressively pursue fiscal, regulatory, investment and trade policies without having to depend upon the fragmented opposition. Time to bone up on additional features within their ‘Canada Strong’ party platform into last April’s election. The time for delays or excuses will have passed and with it the expectations will rise across multiple policy arenas.

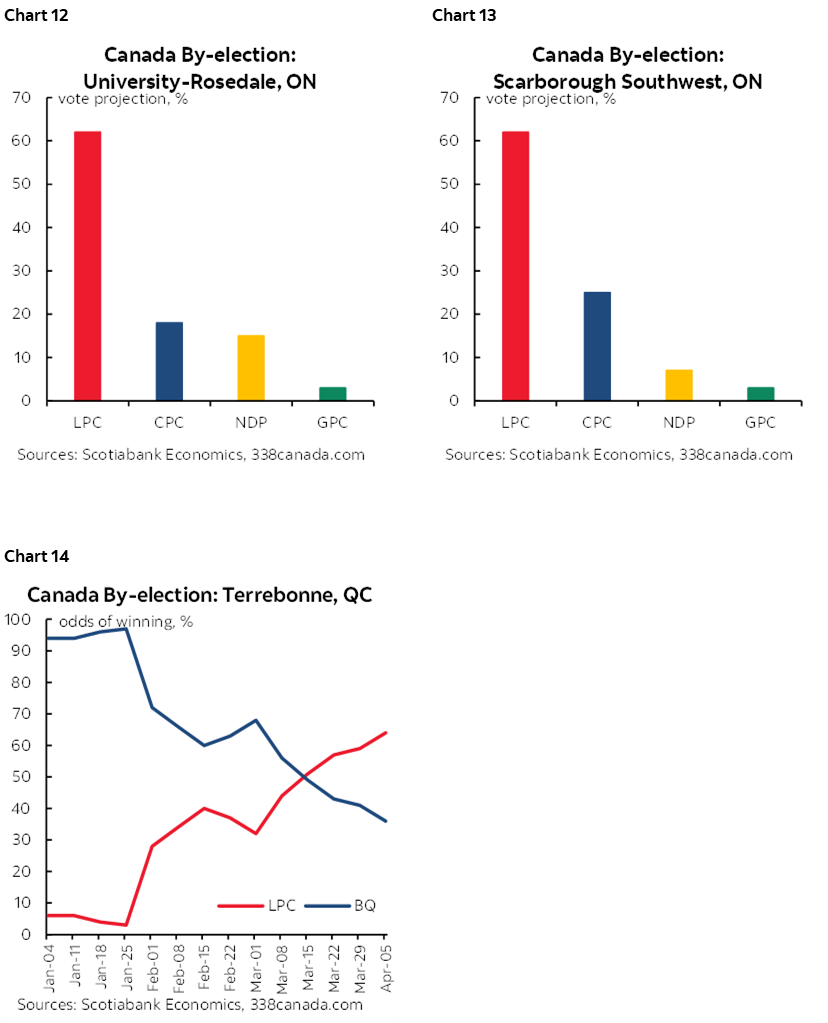

Two ridings in the Toronto area are about as red as they get (University-Rosedale and Scarborough Southwest). A third riding in Quebec (Terrebonne) may be closer after a toss up between the Liberals and the regional Bloc Quebecois was nulled by the Supreme Court following last April’s election. Polls close at 8:30pmET with results likely to roll shortly thereafter. Charts 12–14 show polling.

The Libs’ 171 seats after the latest defection put them one seat shy of majority status in the 343 seat House of Commons. In essence, the Libs have a working tacit coalition with the Green Party’s solitary seat and the six member NDP but one that barely passed last year’s Budget by a vote of 170–168 with four abstentions. One more seat, however, would perhaps lessen the Liberals’ reliance upon the other minor parties. In fact, polling is driving prediction sites to anticipate a Liberal sweep that would raise the number of seats to 174—two more than needed for a majority (here, here and here).

There may nevertheless be limits to party cohesiveness. The Liberals have gained five members who crossed the floor from other parties; four were Conservatives, one was from the NDP. As this piece notes, voters often reject crossers when given the next chance to do so. A Liberal majority would therefore remain partly dependent upon keeping demonstrably unfaithful party members on side in future debates and votes.

And yet the country’s democratic ideals are under strain. Five MPs leveraged their party’s platforms, resources, and brand and were voted in by constituents who often vote first—if not exclusively—for the party, then perhaps for the person. Their constituents did not choose to support the Liberal party when given the chance in a general election. A shortcoming of the Elections Act is the failure to require a byelection should an MP choose to cross to another party. That failure compromises faith in democracy that breeds cynicism, distrust, and possibly lower voter turnout.

Once a majority is set, the machinations toward a Spring fiscal update are likely to be set in higher gear with a combination of targeted stimulus and updated fiscal position likely.

Hungary’s Orbán is On the Ropes

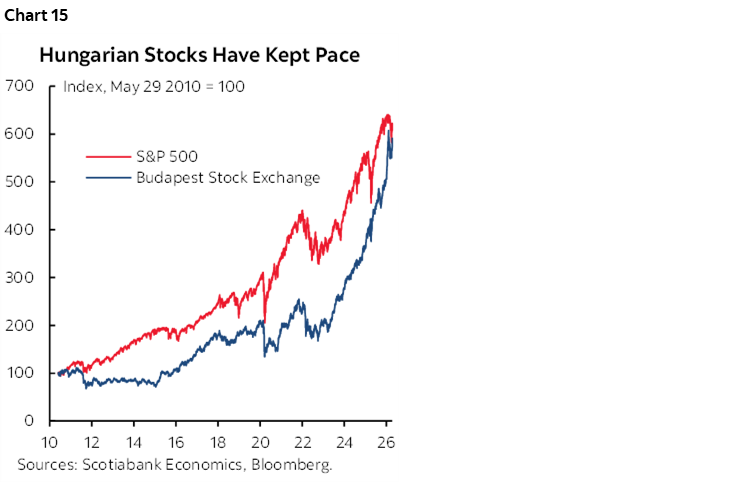

Some believe that the strong man type of leader is good for markets. Hungary’s stock market performance under Viktor Orbán’s leadership since May 2010 might lend itself to this narrative. Since his second return to office, Hungary’s BUX stock exchange has performed roughly on par with the US S&P500 (chart 15).

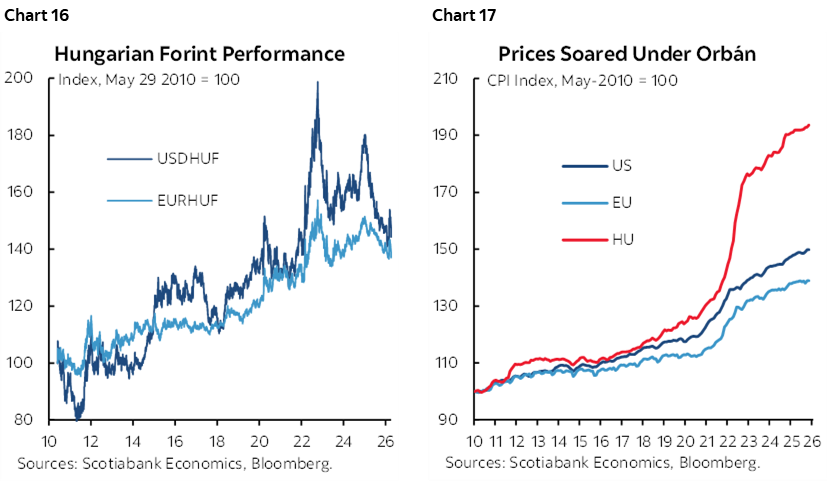

Having said that, the forint has not. Hungary’s currency has plunged by about 50% to the dollar and euro over this same time period (chart 16). Hungary pays 240bps above the US to borrow for 10 years which is about where the spread was when Orbán took office. Because of high import propensities, currency depreciation has contributed toward Hungary’s CPI index almost doubling over this time period and hence far outpacing US inflation and—even more so—Eurozone inflation (chart 17). The latter is ironic in that Orbán has been a persistent pain in the EU and Eurozone’s side. To the extent to which economics drives politics, this may become an example of how affordability challenges can bring down a strong man type of leader with a warning to others.

That’s because of Orbán’s frequent vetoes of EU initiatives as their reward to welcoming Hungary into the EU in 2004. His close kinship with Russia’s Putin has thwarted EU efforts to more effectively impose sanctions on Russia and address the Ukraine war.

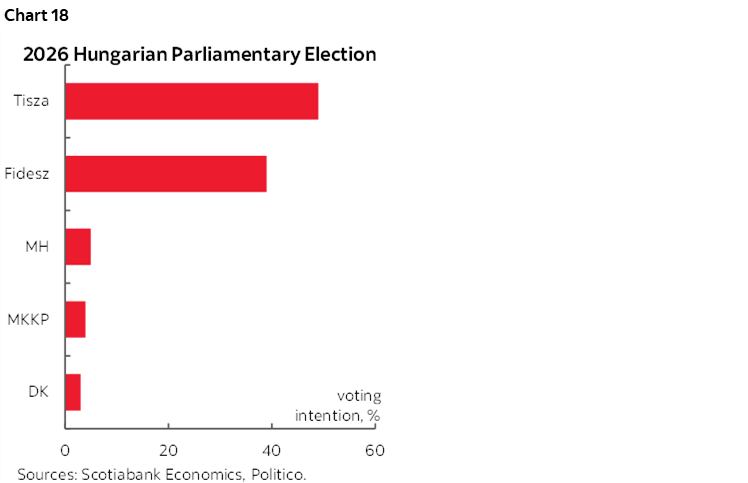

His opponent—Péter Magyar—and his centre-right Tisza party—hold double-digit polling leads over Orbán’s Fidesz party (chart 18). Alongside the economics of it all relative to the early promise held out by EU entry, Hungarians are focused upon endless tales of corruption, influence peddling and the drastic curtailment of the freedom of the press. Orbán’s affiliations with Putin and Trump could also serve as a referendum on how Hungarians wish to interact with the international order.

Polls shut Sunday evening at 7pm (1pmET). A blow out could mean the results follow soon thereafter whereas a tight vote could result in days being taken to determine the outcome.

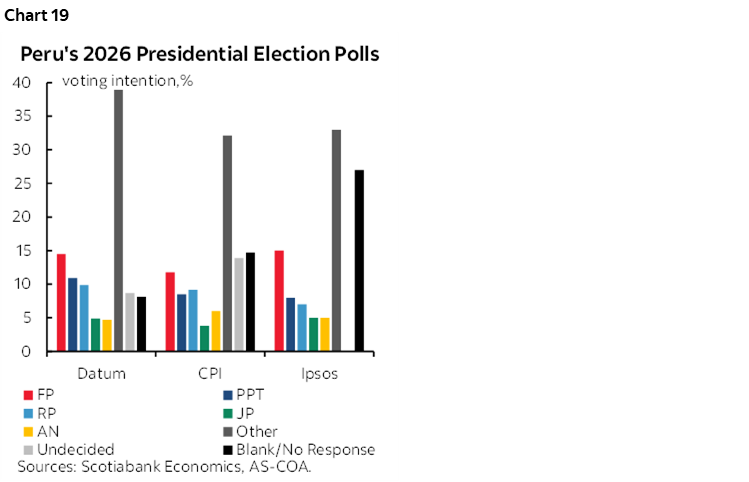

Yet Another Peruvian Election

Thirty-five names will be on the ballot in Sunday’s first round Presidential election. The outcome will determine who becomes the President after an average of one new President per year over the past ten years. That is, if the outcome is decided on the first round which may be unlikely, in which the top two candidates advance to a run-off on June 7th. A runoff is deemed likely to locals.

Keiko Fujimori, Rafael López Aliaga and comedian Carlos Álvarez are the front runners on the right, while Ricardo Belmont, Roberto Sánchez and Alfonso López-Chau are the front runners on the left.

Recent polls indicate that between about one-quarter and one-third of voters are undecided (chart 19). Who wouldn’t be with so many names! Those polls show a whopping 40%+ of the vote going toward the candidates other than the aforementioned leaders.

Given Peru’s challenges in recent times, the victor may be the one who resonates on top issues like corruption. Political volatility may nevertheless persist given the heavily divided field going in.

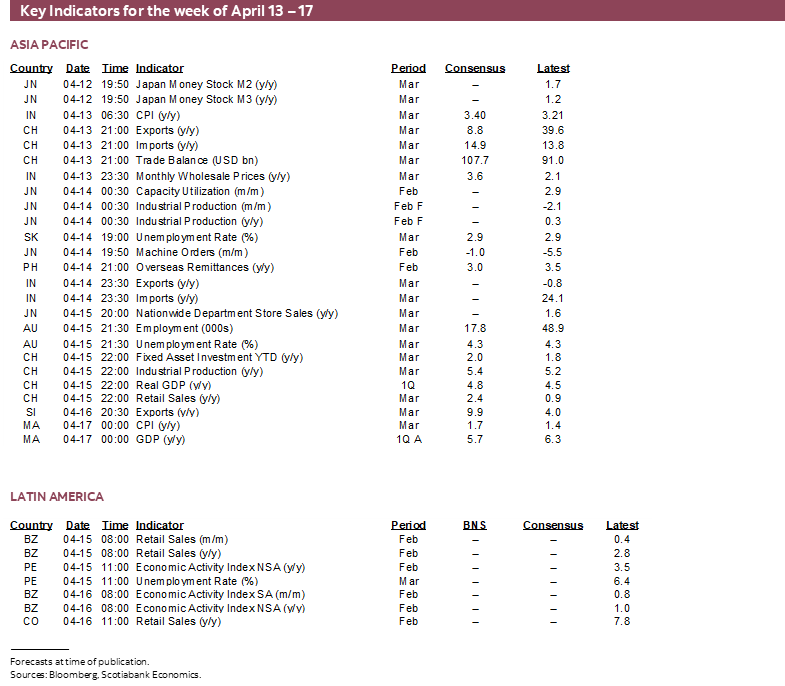

GLOBAL MACRO—SOMETHING FOR EVERYONE

Multiple regions of the world economy face a line-up of macro indicators that will be a mixture of stale readings and very preliminary assessments of the effects of war and higher commodities. I’ve partnered with my wonderful colleague Jay Parmar on what follows.

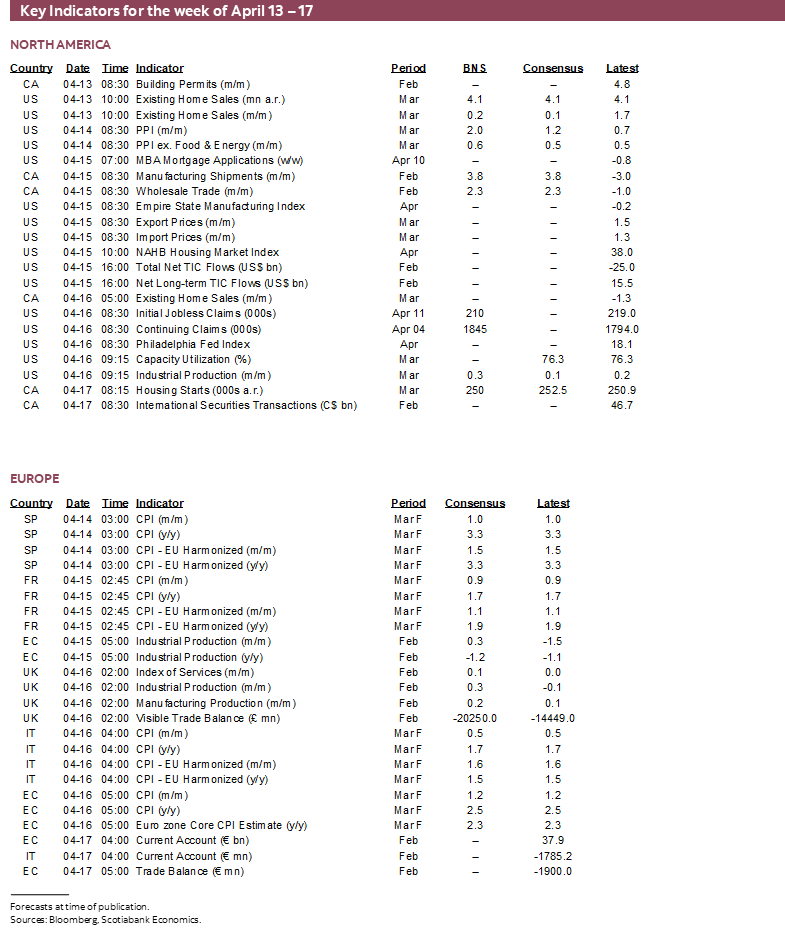

Canada—Strong Data

Canada will only update relatively minor data this week but it is expected to be strong albeit lagging. Manufacturing shipments probably grew by almost 4% m/m in February (Wednesday). Wholesale trade probably grew by over 2% m/m (Wednesday). Housing starts may hold in around 250k+ based on permits but March weather may be a temporary downside risk (Friday). Canada also updates existing home sales for March on Thursday.

US—Surging Producer and Import Prices

The US calendar will be dominated by earnings with little by way of macro readings to consider. Existing home sales may have been little changed in March (Monday). NFIB small business confidence including hiring and inflation measures for March (Tuesday) will be accompanied by March producer prices that could post a strong commodity-driven gain. Select components of producer prices will be used to firm up expectations for the Fed’s preferred PCE prices gauge. The monthly parade of regional manufacturing gauges kicks off with the NY Fed’s Empire measure (Wednesday) alongside import prices for March that will no doubt be explosive. The Fed’s Beige Book (Wednesday), and then both claims and industrial production (Thursday) round it out.

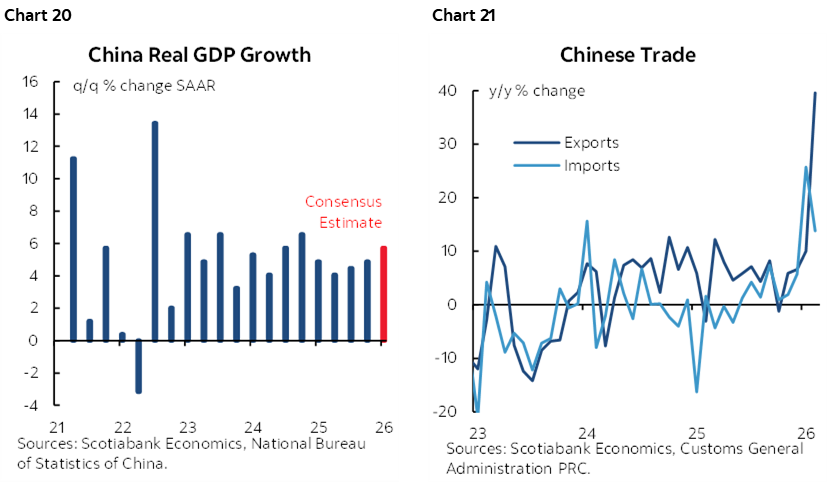

China’s (Backwardly) Resilient Growth

China’s March trade data are due on Monday, with Q1 GDP and March readings for retail sales, industrial production, and home prices scheduled for release on Wednesday. Strong hard data through February, alongside PMI indicators pointing to modest expansion, support expectations of Q1 GDP growth of approximately 1.4% q/q non‑annualized seasonally adjusted (5–6% q/q SAAR). Year-over-year growth figures, however, will be affected by base effects related to the tariffs-imposed on China at the start of the Trump administration.

China’s economy to date has been fairly resilient (chart 20). One reason is booming exports (chart 21) as China’s trade surplus with the US moved lower due to tariffs, restrictions and the dirty-managed yuan peg to the dollar, but the aggregate surplus with the world has been resilient. China has worked its way into new markets and may be leaving the US behind.

Looking ahead, the ongoing geopolitical tensions in the Middle East and an uncertain global economic environment are likely to weigh on external demand, creating downward risks for the Chinese economy, which remains heavily reliant on trade. As a result, key aspects to monitor in the upcoming data will be the strength of domestic demand and any signs of stabilization in the property market.

Aussie Jobs—The Last Jobs Print Before the Next RBA Decision

In Australia, RBA watchers will closely monitor the March labour market data to be released on Wednesday, ahead of the May 5th monetary policy meeting, following stronger-than-expected employment gains in February. Consensus expectations point to another modest increase in employment in March, with the unemployment rate seen holding steady at 4.3%. Job vacancies remain elevated (chart 22). However, a further upside surprise in the jobs report would reinforce the RBA’s hawkish bias and increase likelihood of another rate hike in May. Currently, markets are pricing in around a 60% probability of a rate hike by May, rising to near-full probability by June.

Other key sets of data releases from the Asia-Pacific region include India's March inflation and trade figures, due on Monday and Wednesday, respectively. Meanwhile, Malaysia will release its Q1 GDP alongside March inflation data on Friday.

Europe—Stale on Arrival

In the UK and Europe, a batch of backward‑looking activity data for February will be released this week. The UK is scheduled to publish industrial and manufacturing production figures, along with trade data, on Thursday. In Europe, industrial production data will be released on Wednesday, followed by trade figures on Friday.

LatAm—Hello, February

Finally, in Latin America, Colombia and Brazil are set to release their February economic activity data on Wednesday and Thursday, respectively.

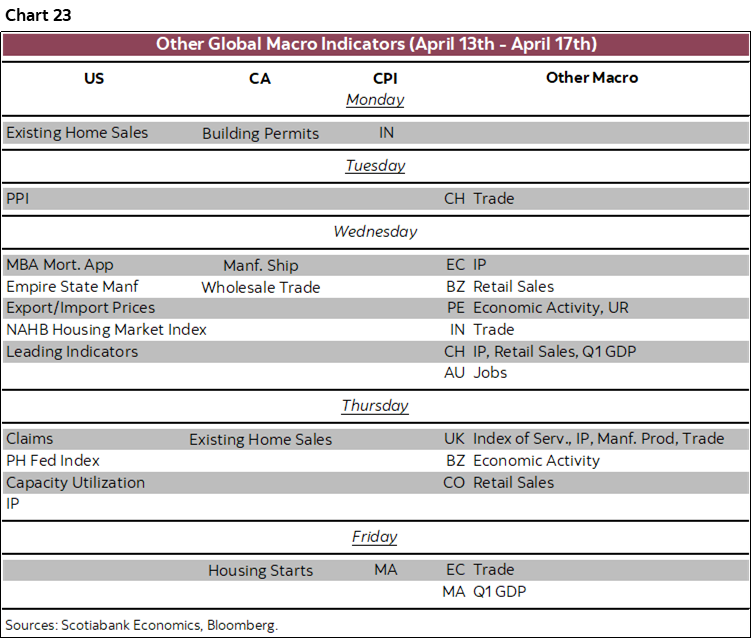

Also see chart 23 for the summary of readings by day.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.