Next Week's Risk Dashboard

- How real is separation risk in Canada?

- What’s missing in US-Iran negotiations

- US CPI—the second round is already here

- Why are US jobless benefit claimants falling?

- BCRP expected to hold

- RBA to have a watchful eye on Australia’s budget

- Global macro

Chart of the Week

A lighter week for calendar-based risk affords the opportunity to talk about something other than central banks, Iran, tariffs, and top-shelf macro reports.

The few exceptions to this will include a round of US inflation readings, updated US consumer spending, a probably uneventful decision by Peru’s central bank, Australia’s budget with the RBA actively watching, and UK macro reports.

The bigger market risk could well be continued wild volatility around Iran war headlines. It remains in Iran’s interest to prolong tensions while adhering to the “managed irresolution” narrative around its behaviour. Keep the US administration guessing, stringing them along, waiting for the terms it demands, knowing full well what lies ahead on the US election calendar six months from now.

That’s by no means a defence of the awful Iranian regime as separate from the Iranian people who have to live with it or leave. It’s necessary to judge market risks through the lens of Iran’s demands. The reported US proposal meets some of them, such as unfreezing Iranian assets and lifting sanctions. The quid pro quo US demand is to jointly reopen the Strait of Hormuz and that Iran must commit to a moratorium on nuclear enrichment. It’s unclear what the status of the uranium stockpiles would be beyond what Trump claims. It’s also unclear that Iran’s other previously stated demands are being addressed including:

1. A complete cessation of the adversary’s “aggression and assassination” operations.

2. Establishment of concrete mechanisms to ensure the war is never again imposed upon Iran.

3. Guarantees and clearly defined procedures for payment of compensation and reconstruction costs resulting from the war.

4. Cessation of hostilities across all fronts and across all resistance groups involved throughout the region.

5. International recognition and guarantee of Iran’s sovereign right to exercise jurisdiction over the Strait of Hormuz.

At the point of publishing we remain highly sceptical toward the prospects of agreement and even less so toward the durability of any agreement and any quick recovery in supply chains.

As for what follows, I’ll start with separation risk in Canada as it has repeatedly come up in domestic and international marketing.

HOW REAL IS SEPARATION RISK IN CANADA?

Every now and then I’m asked by global clients about separation risk concerning Quebec and Alberta. The issue has come up in domestic meetings, calls and foreign travel. I don’t blame them, given the headlines on the issue, but will argue that markets are correct in downplaying the unwanted risk while nevertheless cautioning against letting one’s guard down. A primer is offered alongside explanation of some of the complicating factors.

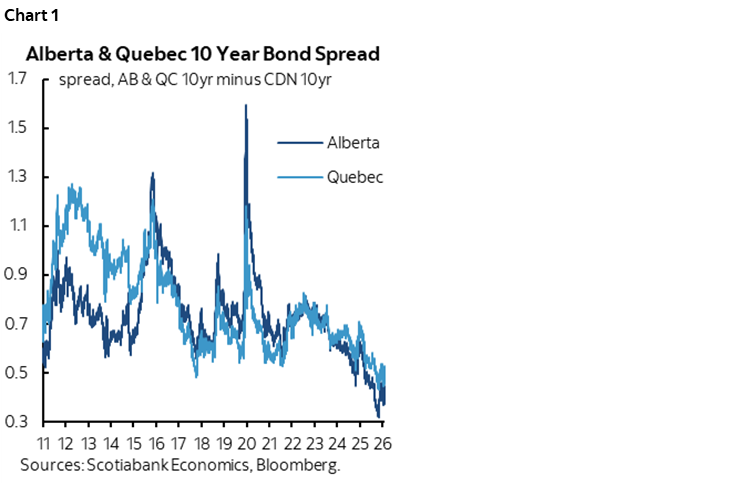

At present, tight provincial government bond spreads over Canadian government bond yields suggest that either market participants don’t believe separation is a real risk or that it’s not yet on their radar (chart 1).

The Timelines

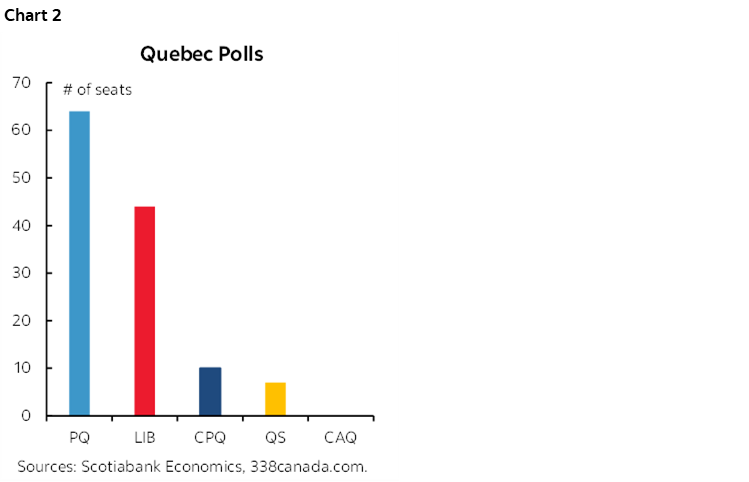

Quebec’s provincial general election will be held on October 5th and the leading party—the Parti Quebecois (chart 2)—has pledged to call a referendum at some point should it win the election.

Alberta’s government won a smaller majority in 2023 and faces a fresh general election on October 18th, 2027. The issue of separation is sure to be on the agenda and the ruling United Conservative Party is closely associated with the issue.

Alberta has a separatist movement that is trying to push a somewhat facilitative Premier Smith toward including a vote on sovereignty as part of a scheduled package of referendums to be advanced on October 19th. Such a vote could happen as early as that date or by early 2027—perhaps ahead of the general election. As of yet, no official separation referendum has been scheduled. If it’s included, then it’s perhaps not entirely coincidental that it would closely follow Quebec’s election.

Gauging Support

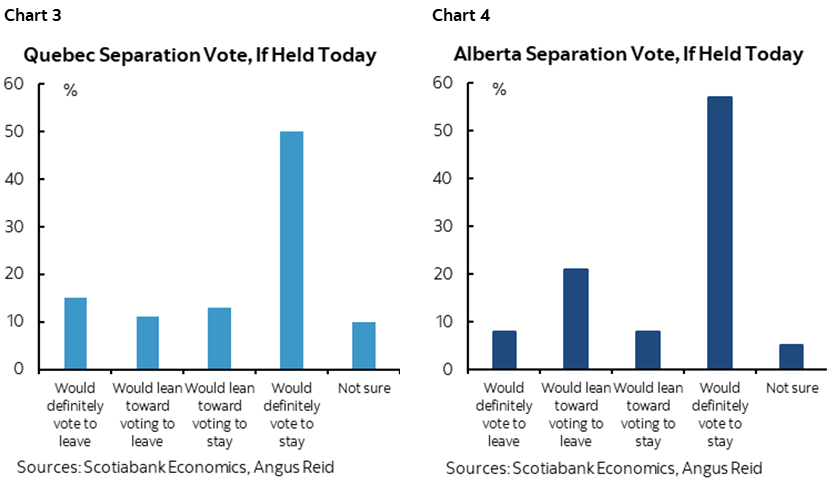

There is no broad support for separation in either province but it’s not overwhelmingly against (charts 3, 4). This is purely being led by fringe groups and some politicians against dysfunctional oppositions.

In both Alberta and Quebec, polls show roughly 60% opposition to separation with just 7% undecided in Quebec and a little higher share in Alberta.

I have no ability to vouch for the quality of the 302k signatures on a campaign to elicit support for Alberta’s separation, but it’s a fairly small number. 302k is a tiny 6% of the province’s population and 10% of eligible voters. Hopefully there are no out-of-province folks, or names drawn from above catchy epitaphs on a macabre stroll, or family pets on the roll.

Hanging in the balance are the signature verification process, the outcome of a voter data breach, and the court challenge by Alberta First Nations that say the petition violates their treaty rights.

The Risk

Think Brexit, only different, and not in a good way. Once the door has been pried open, anything can happen and you must be prepared for all outcomes.

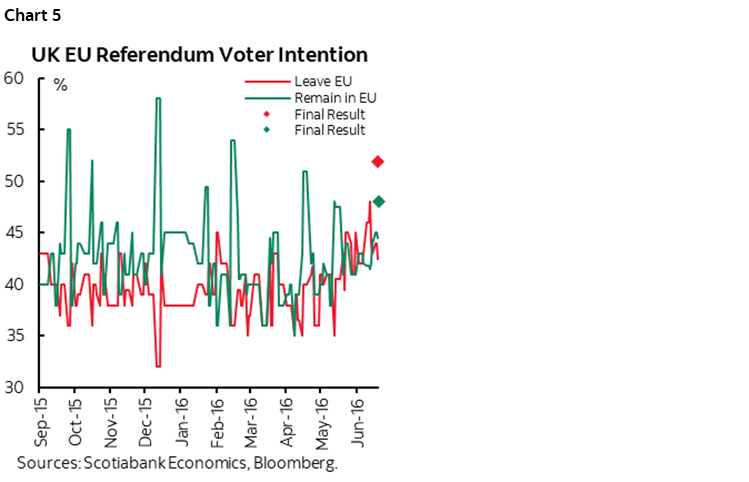

UK PM David Cameron thought that the British people finally deserved a referendum and that they would vote to remain and set June 23rd 2016 as a day that would arguably live on in infamy. Cameron’s speech in 2013 laid out his support for a referendum to be held and said “Because I believe something very deeply. That Britain’s national interest is best served in a flexible, adaptable and open European Union and that such a European Union is best within Britain in it.”

Polls regularly showed strong support for the remain camp, until the only one that mattered (chart 5).

52% of respondents voted to leave.

The immediate market reactions were swift and spectacular. Sterling sank by over 11% to the dollar as the result became known and went on to lose about a fifth of its value that year—effectively a one-fifth pay cut to purchasing power. The UK 10-year yield plunged by about 35bps to just above 1%. The FTSE 100 sank by almost 9%.

Partly because of high import propensities and sterling’s plunge, UK inflation soared from about ¼% y/y just before the vote, to a peak of over 3% y/y by the end of 2017. UK GDP growth temporarily improved on the back of accelerated export growth but quickly reversed course after about eighteen months. Uncertainty prevailed while it took over four years to negotiate a new Trade and Cooperation Agreement with the EU. Employment kept growing both in aggregate and across firms with formal payrolls.

Most economists would say that Brexit was a mistake that was driven by emotions and nationalism, with a healthy dose of false promises and downright deceit. This isn’t the place to resurrect the discussions around Boris Johnson’s tactics.

It’s a lesson to be careful and not sanguine toward courting risks that may spiral.

What was different about the UK case in contrast to the Canadian provinces, however, was that the UK already had an independent central bank, it already had independent fiscal policy, it already had its own currency, and it didn’t need to take on a large share of other debts.

What They Want

Well, to separate, right? Perhaps.

Or perhaps to secure more favourable policies in extractive fashion from the rest of Canada.

Or perhaps not extractive, but partially additive through, say, more liberal controls around investment and development of provincial riches which probably applies more to Alberta.

I understand some of the frustrations facing both provinces. For example, immigration policy has been badly mismanaged by the federal government, although provinces and educational institutions share some responsibility for this. The provinces desire more control over their resources and other policy directions. Albertans have the strongest dissatisfaction with the federal Liberal government’s efforts to thwart investment in its energy sector over many years. Western Canada has long felt that the country’s system of equalization payments that is designed to spread the riches—whether from natural factor endowments or otherwise—unfairly penalizes them and disproportionately benefits provinces like Quebec.

Can They Separate?

No Canadian province can unilaterally secede. The Supreme Court’s case in 1998 (2 S.C.R. 217) stipulated after the close ‘no’ vote in Quebec’s 1995 referendum that no province can withdraw without negotiation and consultation with the federal government and the other provinces. Unilateral secession would be deemed unconstitutional in the Court’s interpretation.

That said, the Court’s ruling did require that if a “clear” majority supports a “clear” referendum question then negotiations must ensue. The Court said such negotiations must address core principles including respect for the Constitution and protection of minorities among others.

One example of international precedence comes from Catalonia’s arrangements within Spain that has never allowed it to take steps to secede outright. In short, it’s the ‘Hotel California’ model.

The ensuing Clarity Act set out the requirements for a clear question in any referendum. The threshold of support that is required is unclear.

The Economics

Setting aside the issues of legality and negotiations, would it make sense to separate? That’s partly a normative issue that reaches across multiple considerations, but I’ll stick to the economics.

You may well remember the debates around arrangements in a separation scenario in the lead-up to the October 30th, 1995 vote. I do, as it was toward the start of my career, and it was a squeaker in favour of remaining. Many of the same issues would resurface. There is no costless, risk-free way to sovereignty.

For one, Quebec (and hence Alberta today) would very likely need to take some negotiated portion of the federal government’s debts with it. How much they would have to take would be the product of negotiations. There are many attempts at estimating how much federal debt the provinces would need to take with them by using different approaches such as share of population, share of GDP, share of per capita GDP, share of GNP etc, but the outcome would be in the tens of billions if not 12-figures. Many federal assets in Alberta and Quebec are immovable, and Albertans and Quebecers have a stake in financial asset holdings of the federal government. Sharing the debts or acquiring the assets with debt would impair either province’s financial standing. It may also create uncertainty around retirement assets.

Alberta’s pre-war budget forecast deficits throughout the three-year horizon with debt payments rising to about 5% of GDP and 6% of revenues from 3% and 4% respectively this year. C$70 billion in net debt as a share of GDP stands at about 8% and was projected to rise to 13% by decade’s end which is still low relative to other provinces. Alberta has about C$124 billion in liabilities, $92 billion of which is taxpayer supported. Its long-term debt rating is highly rated at just shy of AAA by each of the main agencies.

Quebec projects small deficits until 2029 with partial incorporation of the war’s effects. Debt service payments are about 10% of GDP and 6% of revenues, rising to 12% and 6½% respectively by around decade’s end. Net debt as a share of GDP stands at about 39% and is projected to decline slightly over coming years. Gross debt equals over C$270 billion. Quebec was recently downgraded to A+ from AA- by S&P.

All that would likely change in a separation scenario. Alberta’s total liabilities could easily cross $200 billion if forced to assume a share of federal debts and its ability to service this debt would be spread over a smaller, narrower and more volatile revenue base. A similar argument would apply to Quebec. Ratings would probably be imperilled. Albertans and Quebecers would pay more to borrow across governments, companies and households. Credit availability may become more constrained.

As with fiscal policy, there is no assurance that independence would necessarily lead to sound overall stewardship. Alberta’s Heritage Fund is one such example after decades of relatively poor performance and political meddling.

For another, the seceding province would have to negotiate its own trade deals. If rational forces prevailed, then it would be in everyone’s best interests if Canada and the seceding province(s) were to rapidly strike deals, but the feeling of betrayal could mean that it would instead take years. A best-case scenario could be status quo, which would mean existing provincial barriers to trade and mobility would be maintained, but emotions and conflicting provincial goals hardly assure rationality. And negotiating with the US would probably be even more problematic outside of Canada than within; don’t trust otherwise with the US administration. In all cases, a prolonged gap between trade deals would likely ensue—just as in Brexit—and thereby create higher uncertainty against investment and spending.

The same need for new deals would apply to investment and security arrangements.

Which currency would be used? Would you have your own central bank? These are complex issues. Independent monetary policy, free capital flow and a fixed exchange rate cannot coexist as per Mundell-Fleming’s ‘Impossible Trinity.’ Depending upon the monetary regime, fiscal policy independence would not necessarily be assured. Adopting the USD through dollarization at the prevailing exchange rate would enshrine undervaluation relative to current prices and valuations and stoke longer-term inflation risk. With that would go soaring inflation and higher long-term borrowing costs.

Alberta would remain a land-locked province arguably more dependent upon other provinces and territories for passageway rights concerning commercial arrangements including pipelines. That could affect both proposals and existing infrastructure.

Negotiating trade deals with the US could be more complicated if the US is less tolerant toward cultural protections.

What if ‘your’ land isn’t your land after all? Recall the lead-up to the 1995 referendum in Quebec and the complicated matter of indigenous territories and rights. The courts may well have a say in this. What if independence meant smaller.

With uncertainty goes strength in numbers. Should oil plunge to $10, Alberta may wish to have the ability to tap into the safety net of Confederation. That risk is perhaps downplayed at present oil prices! Ditto should an industrial recession slam Quebec’s economy.

To be clear, the pain would spread to the rest of Canada as well. Uncertainty would discourage investment across the land. Confidence would be negatively impacted. The loss of federal revenues over a considerable portion of resource riches would be a weight against sparing some transfers and expenses.

Eventually the country and its regions would reach a new equilibrium and begin to recover, but the adjustment costs could be enormous to a whole generation with the incidence effects being the harshest upon those least able to adapt. Gains in areas of greater control could be offset by lower living standards relative to a world marked by continuity or negotiated improvements.

Most economists, for instance, would argue that Brexit made the UK economy smaller by multiple percentage points of activity in relation to what would have otherwise been the case. Recall the earlier point about the differences between Canadian separation and Brexit that could make Brexit look like child’s play in comparison.

And foreign political interference—especially by the current US administration—could imperil relations with Canada on numerous fronts not least of which in a mess-with-our-politics-we’ll-mess-with-yours way of thinking. Greater instability across multiple areas of coordination could erupt in N.A. This is probably why you have concern and investigations into foreign meddling allegedly by Russians, China and the US.

In wrapping up, I’ve always loved this country and its diversity. My family has strong Quebec roots through French and English elements of the population. Western Canada has some of the world’s most beautiful scenery and tremendous longer-run growth prospects. There is a great deal that can be done to unleash more growth to benefit all—often by getting agreement and coordination among the provinces—and to make the country stronger to confront future challenges. With more growth and better fortunes there is likely to be more Team Canada spirit.

As an economist, I can only think separation would make all of us weaker at home and on the world stage within an increasingly divided world.

US INFLATION—THE SECOND ROUND IS ALREADY HERE

This one could be a doozy. US CPI on Tuesday combined with producer prices on Wednesday will reveal estimates for the Federal Reserve’s preferred PCE inflation gauge on May 28th. That will be the last PCE reading before Kevin Warsh chairs his first FOMC meeting on June 17th.

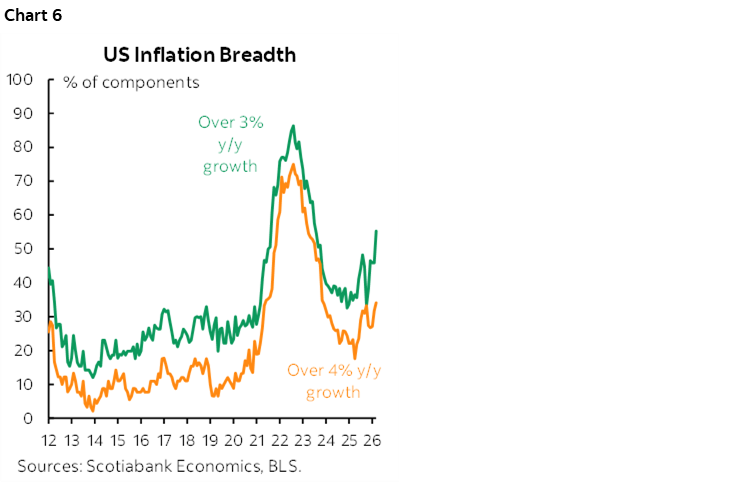

More important is that after the initial energy shock to March inflation readings, April will start the long period of evaluating potential second round passthrough effects into core prices. Keep a close eye on the breadth of price increases that has been on an upswing long predating the war and with further upside likely (chart 6).

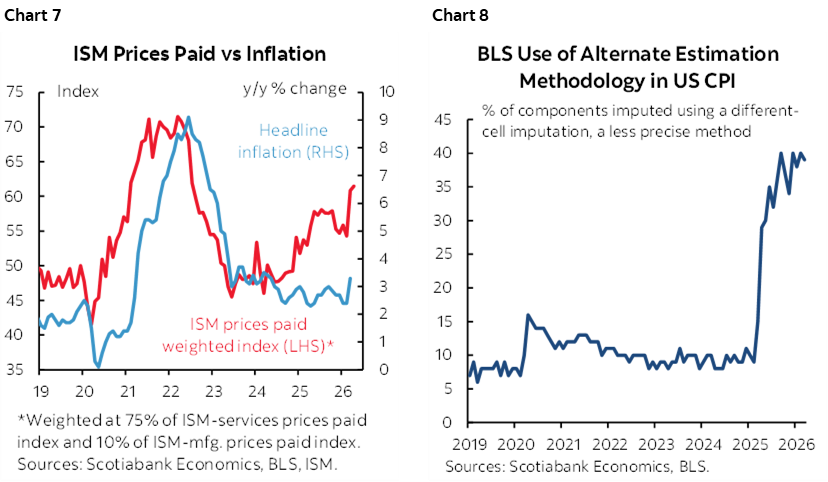

Second-round effects won’t be settled with one batch of numbers, but it’s worth reinforcing that there were signs of broadening pressures long before core measures of inflation started to reaccelerate (chart 7). The need for a lot of data to evaluate developments is further reinforced by ongoing data quality issues like a record high share of the CPI basket that is being estimated with proxy methods in the absence of more complete sampling (chart 8).

CPI is estimated to rise by 0.7% m/m SA and 3.9% y/y. Core CPI is estimated at +0.4% m/m SA and 2.9% y/y.

- April is normally a seasonal up-month for unadjusted prices;

- gasoline will contribute an estimated 0.2% m/m to total CPI;

- food prices may contribute 0.1;

- used vehicle prices may contribute another 0.1 with no contribution from new vehicles;

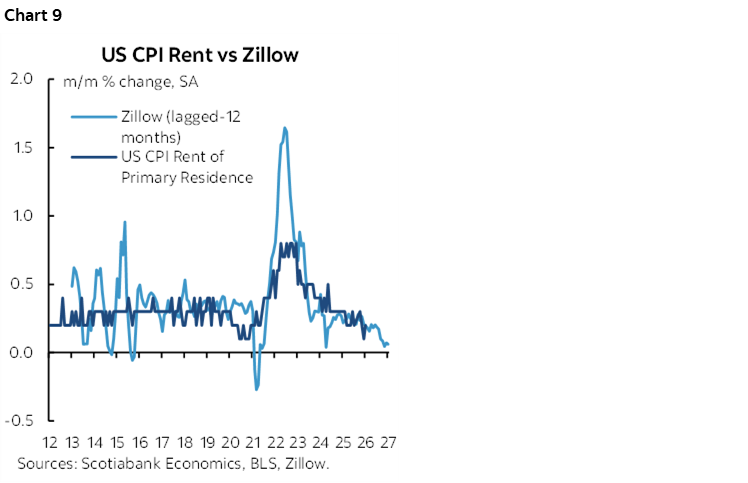

- shelter’s 35% weight in the basket is estimated to contribute another 0.1. Primary rent, for instance, should remain under general downward pressure (chart 9);

- core services CPI (ex-shelter and energy services) represent about one-fifth of the CPI basket and could contribute up to 0.1;

- there are several goods categories that are related to tariffs and they are expected to remain warm. Clothing has been up by 1%+ m/m SA in each of the past couple of months as one example.

Producer prices could rise by a little less than the prior month’s gain at 0.4% m/m SA with core prices ex-food and energy up 0.3%. The PPI categories that will matter as inputs to PCE inflation will be airline passenger services, several health sector categories, and portfolio management & investment advice services.

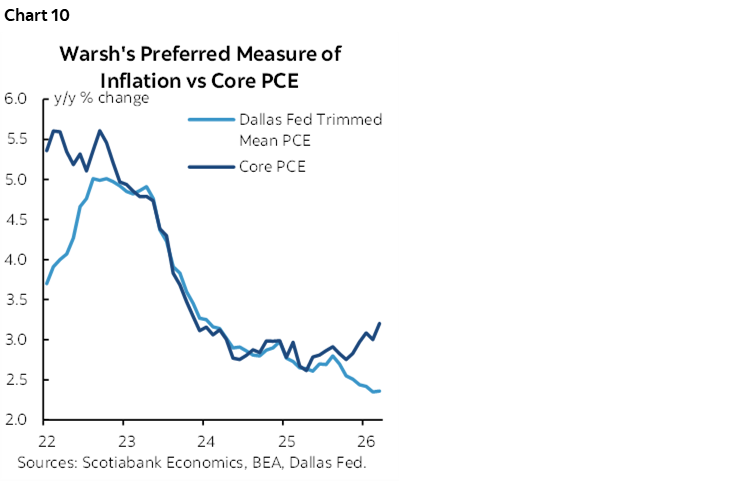

Warsh, however, indicated during his Senate confirmation hearing on April 21st that “The measures I prefer look at trimmed averages.” The Cleveland Fed will update its trimmed CPI measure shortly after the CPI release. The Dallas Fed’s trimmed mean PCE measure will only be updated after PCE toward the end of the month. Chart 10 vividly depicts why Warsh may prefer it despite considerable controversy around its use.

It’s worth repeating earlier cautions on trimmed measures. Deciding what share to remove is somewhat arbitrary and different groups that calculate trimmed measures all remove different shares. The BoC removes the top and bottom 20% of prices, so 40% of prices. The RBA’s preferred measure removes the top and bottom 15% of prices, so 30% of the basket. The Cleveland Fed removes 16% at the top and bottom. The Dallas Fed’s trimmed mean PCE measure removes the top 31% of prices and the bottom 24% of prices. You could be eliminating useful information that shouldn’t be looked through. Some members on the FOMC—including on the Board—have expressed reservations toward using trimmed measures.

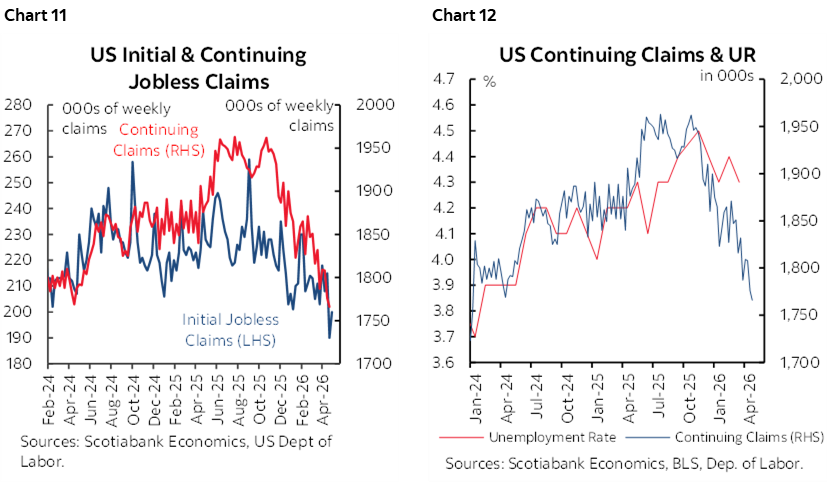

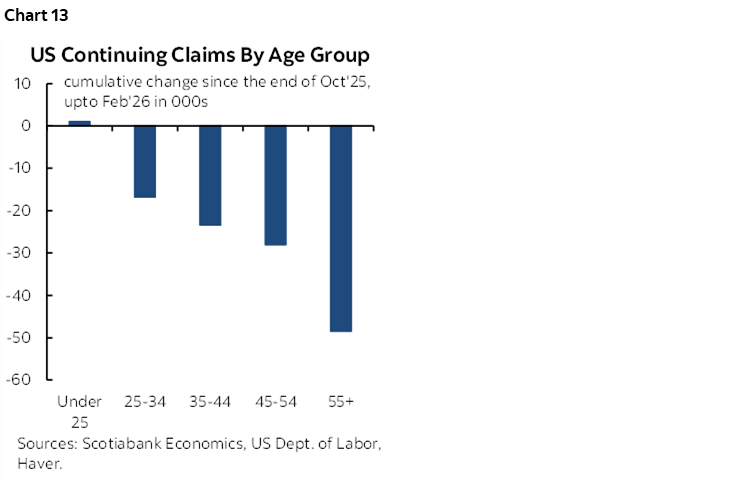

FALLING US JOBLESS BENEFIT CLAIMANTS—USEFUL OR ILLUSORY?

So, what’s going on with low and falling US jobless claims? Initial jobless claims are plummeting (chart 11) and the falling number of continuing claimants is correlated with a falling unemployment rate (chart 12). Some of what follows carries on from an interpretation of recent US jobs numbers including conflicting estimates and work force exits (here).

The bottom line is to treat both sets of claims numbers with high scepticism. I think they provide a misleading picture of the health of the US job market. Here’s why.

1. Labour hoarding: It’s a low hire, low fire environment because companies are unwilling to let workers go out of fear that they will go to the competition in a tight labour market and won’t be able to get workers back when they need them amid all the different forms of uncertainty.

2. Some believe that there have been ongoing shifts of workers into sectors with lower job turnover which is contributing to a nine-year low in labour turnover. Amid the uncertainty, workers are hunkering down and unwilling to move. It’s an indirect reflection of the uncertain climate created by war, tariffs, AI, immigration changes, etc.

3. This is perhaps a repeat of the pandemic experience, except this time, population is shrinking and so is the pool of available workers as the participation rate falls. That compounds the hoarding argument.

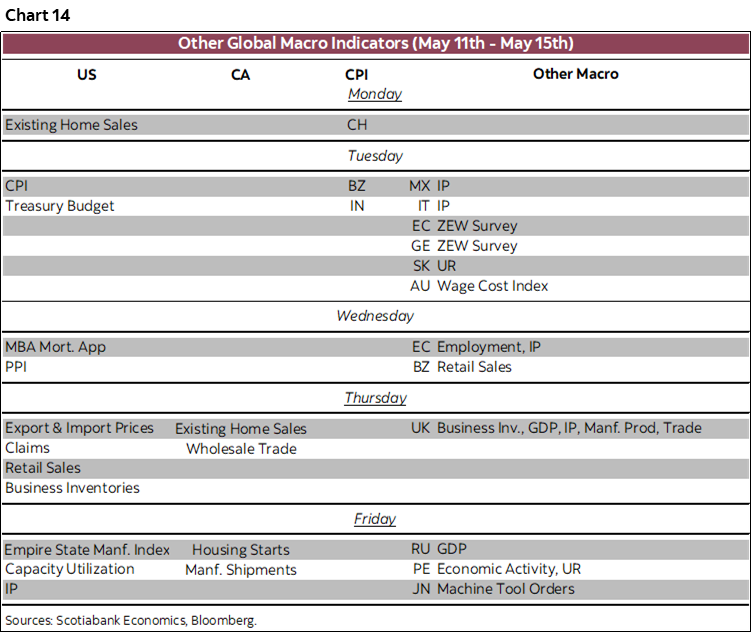

4. Demographics may also play a role in the pandemic and currently, given that there are more workers on the retirement bubble who are simply punching out and not coming back. The participation (part) rate for 55+ workers is falling off a cliff (chart 13) whereas the part rate for 25-54 year olds has been rising and for youths 16–24 is has been volatile but little changed. The 55+ part rate has fallen by 2.0 percentage points since early 2022, which is a lot, and by 0.7 ppts in just the first four months of this year. The 55+ category of workers accounts for the biggest share of the decline in continuing claims since they started to decline after October, although an age-based break down of the data is only available until February. Aging boomers are either being displaced and saying they’re out, discriminated against, or saying don’t want to go through all that again.

5. There have been innumerable changes to unemployment insurance rules that have tightened the criteria. There are many more pieces of proposed legislation that are in the works. Over the years, they have reduced eligibility, shortened benefit amounts/periods, clamped down on fraud, tightened evidence of seeking employment.

6. Jobless claims are not the first to turn in a weakening market. There can be various forms of lags.

GLOBAL MACRO ROUND-UP

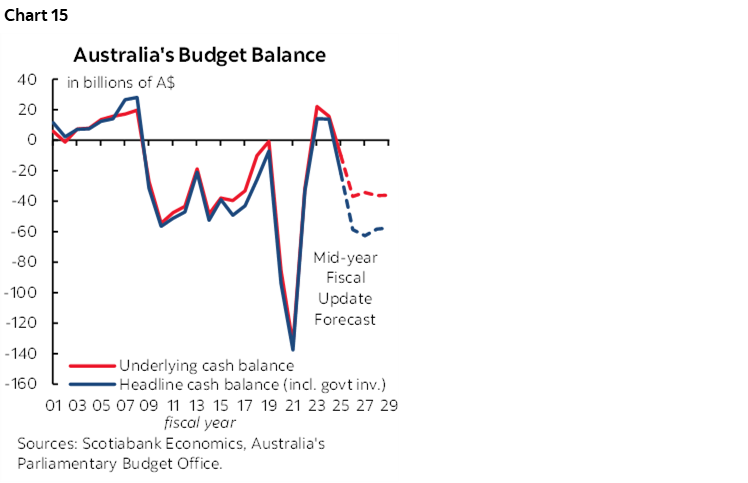

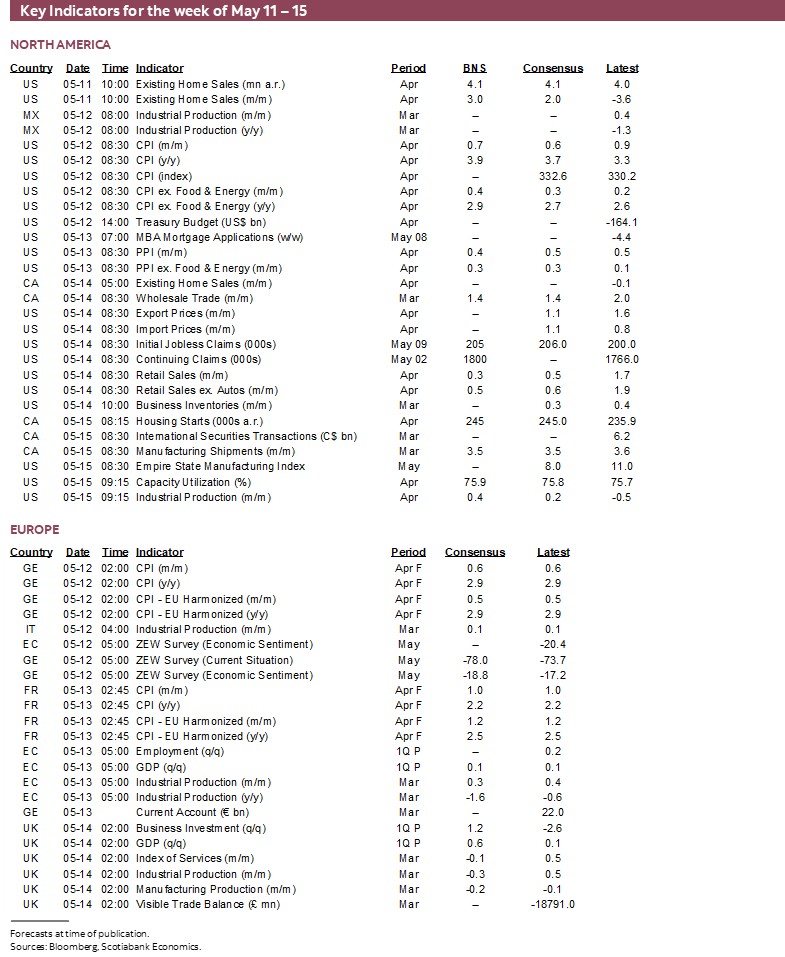

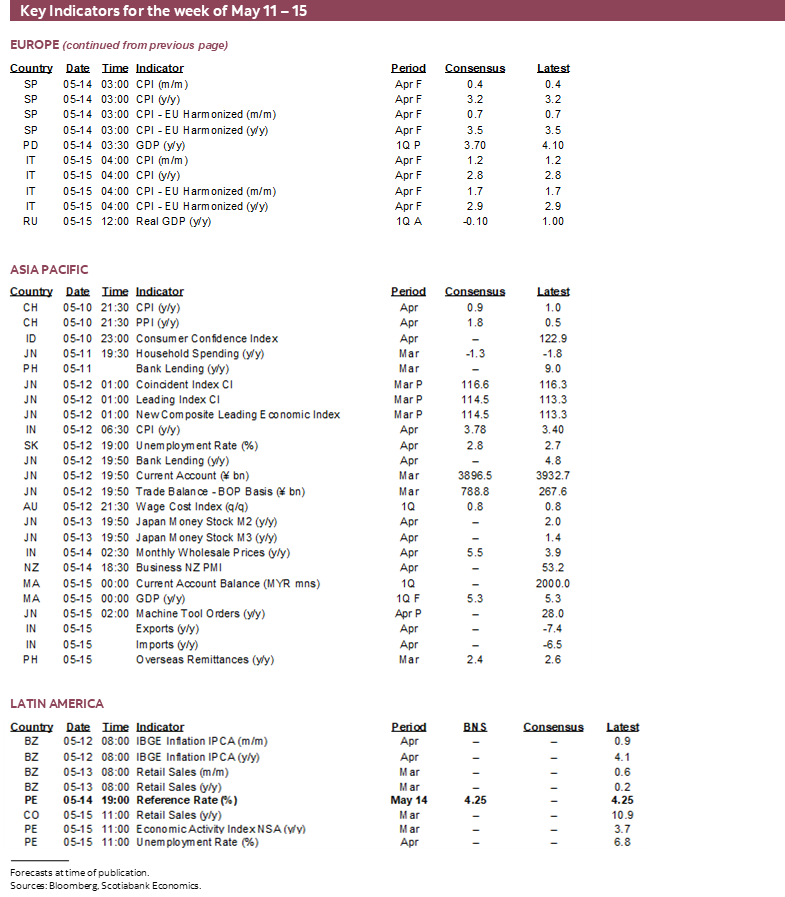

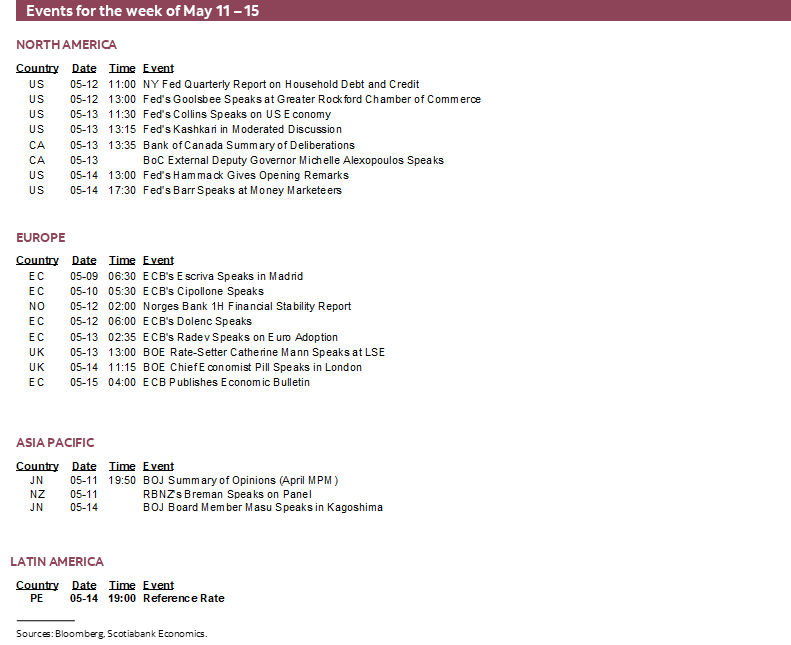

Other macro developments will run from updates on US consumers and factory output, Australia’s Budget, UK macro readings, an expected hold by Peru’s central bank and other light data. Chart 14 summarizes the readings by day.

US—Tracking the Consumer Into Q2

The main US readings beyond CPI will be Thursday’s retail sales and Friday’s industrial production—both for April. Retail sales should post a modest gain in dollar terms as higher gasoline prices cancel out lower vehicle sales with core sales estimated to post a small gain. Q1 was not a good quarter for retail as the volume of sales grew by only 0.7% q/q SAAR. Industrial output could rebound by getting a lift from mining, utilities and possible autos. Existing home sales (Monday) are expected to be little changed based on advance pending home sales.

Canada—Tidbits

Canadian markets will continue to focus upon earnings with little on the macro calendar. Existing home sales have had a rough winter just like many others have but April’s figures (Thursday) start to kick off the important Spring market. The next 3–4 months will inform whether a rebound is in the works. Wholesale (Thursday) and manufacturing (Friday) reports for March are expected to post strong gains based on advance estimates from Statistics Canada but key will be to remove price effects. Minor BoC communications will include Wednesday’s Summary of Deliberations and that same day’s speech by External Deputy Governor Alexopolous on AI adoption and what it could mean to Canada’s economic potential.

Early next week’s focus will be on Asian markets, led by Australia, where Treasurer Jim Chalmers will deliver his fifth Budget on Tuesday alongside Q1 wage data. Market and the RBA will be closely watching the details to help frame the next steps in monetary policy. Elsewhere in Asia, April inflation prints for China and India are due on Monday and Tuesday, respectively.

From this point onward my colleague Jay Parmar takes over the writing to focus on some international developments.

Australia Budget

After the RBA delivered a third consecutive rate hike last week to combat inflation, attention now shifts to fiscal policy, with the 2026 Budget set to be handed down on Tuesday. Treasurer Jim Chalmers will deliver the 2026–27 Budget at around 5:30amET, with “intergenerational fairness” flagged as a key theme. A key challenge for the Treasurer will be to strike a balance between maintaining fiscal discipline and supporting economic activity amid cost-of-living pressures and headwinds from the Middle East conflict, while avoiding any addition to upside inflation risks.

Housing affordability is expected to be a central focus of the Budget, with tax reform measures aimed at alleviating pressures in the housing market alongside increased investment in new housing supply. Potential changes, including the removal of the 50% capital gains tax discount and tighter restrictions on negative gearing for property investors, are likely to feature, with further details set to be outlined. These measures are also expected to support government revenues and strengthen the fiscal position.

In addition, expectations are for the government to rein in spending to create room for higher defence expenditure alongside targeted cost-of-living measures. Early signs of spending restraint are already evident, including adjustments to disability support, the scrapping of certain rail line construction projects, and potential changes to EV tax concessions, with further measures likely to be outlined in the Budget.

At the same time, cost-of-living relief will need to be carefully calibrated to avoid boosting demand and undermining the RBA’s efforts to contain inflation. The government had already announced tax cuts in last year’s Budget, which are set to take effect from July 1st 2026. Further initiatives are expected to include the proposed A$1,000 instant tax deduction for individuals and fuel security measures for both households and businesses, with the details set to be crucial.

Overall, expectations heading into the Budget point to restrained government spending, with the deficit projected to be similar or a bit contained relative to the mid-year fiscal update (chart 15). Any material upside in spending could prompt a more hawkish response from the RBA, potentially leading to a more restrictive policy stance.

Europe—UK Macro

European markets are expected to be relatively quiet as the week progresses, amid a light data calendar and the US delaying its tariff hike plans until July 4. In terms of releases, both the euro area and Germany will publish their May ZEW surveys on Tuesday, followed by euro‑area Q1 employment data on Wednesday.

The UK will be in focus on Thursday amid a heavy macro data calendar. Q1 GDP is expected at a solid 0.6%, slightly above the BoE’s estimate, following 0.1% growth in Q4. Whether markets interpret this as an early signal of BoE tightening will depend on the details, particularly household consumption, real income growth, and business investment. However, the monthly GDP indicator, alongside industrial production and the services index, is likely to show weakness in March.

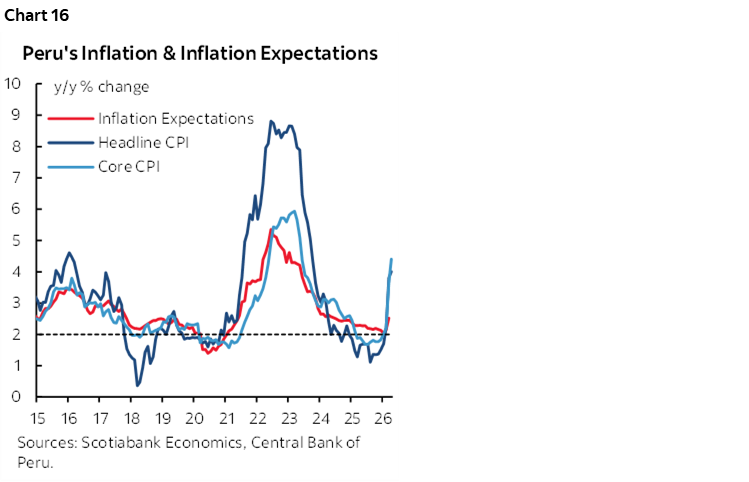

LatAm—Peru’s Hold

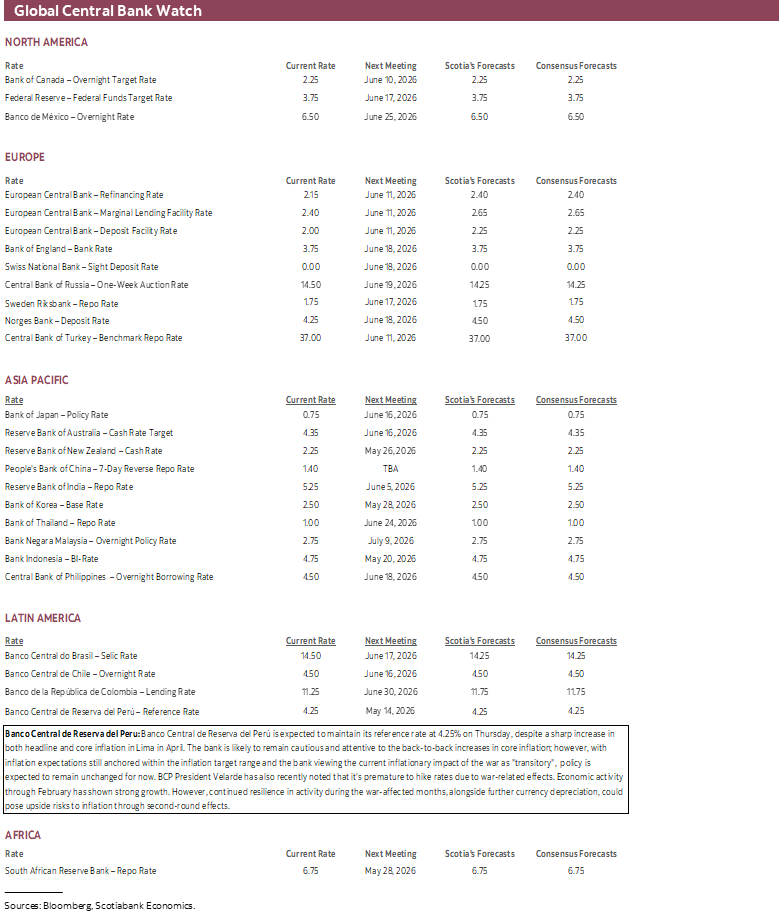

Banco Central de Reserva del Perú is expected to maintain its reference rate at 4.25% on Thursday. Inflation is spiking (chart 16), but the central bank wishes to take more time to evaluate wartime effects and bear in mind that the second- and deciding round of the Presidential Election is next month.

Finally ending the week will be Peru’s economic activity for March on Friday. Markets will be closely watching whether activity remains resilient or begins to show signs of weakening in the first month of the conflict.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.