- FOMC upgrades macro forecasts…

- ...but still shows no rate hikes for at least three years…

- ...even as some participants break rank…

- ...but markets paid too much attention to dots…

- ...as Powell hinted they could move up if forecasts become reality

- ON RRP limit raised by US$50 billion

- Ending agency CMBS purchases is of little consequence

- SLR guidance expected in “coming days”

- Bank capital decisions are “a couple of weeks away”

- We continue to expect 2022Q1 taper, 2023 rate hikes

Markets bought the FOMC’s act for today, but time will tell if they inappropriately lowered their guard. The US Treasury curve rallied very slightly across maturities by 1–2bps, fed funds futures pushed out rate hike expectations by a few months into 2023, the USD depreciated by about ½% on a DXY basis and the S&P500 rallied by about 0.8% following all communications but mostly on the back of the 2pmET statement and Summary of Economic Projections.

In my view, the only truly meaningful new information you can take to the proverbial bank today had to do with the policy changes announced by the NY Fed, the continued deferral of a decision that is forthcoming over “coming days” on the Supplementary Leverage Ratio exemption of counting Treasuries and reserves in the regulatory rule, and guidance that an announcement affecting decisions surrounding bank capital management issues such as buybacks and dividends is forthcoming in the next two weeks. The SLR matter keeps the suspense alive along with the ongoing debate over what it may mean to markets.

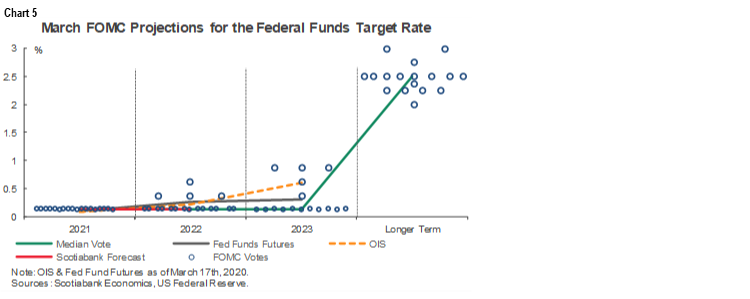

What markets rallied on, however, was the impression that the FOMC still has no desire to hike rates throughout its 2021–23 projection horizon. Well, good luck with that, but I’m not inclined to have high trust for that part of the communications. Markets fed on the median rate path provided by FOMC officials as discussed below. Time will tell whether markets should indeed have such faith in the FOMC rate path and whether it is in sync with the rest of the macro projections, but the press conference offered a veiled reason why astute market participants shouldn’t take the dots quite so literally. In any event, our curve forecasts embed a loosely pencilled in path containing three rate hikes in 2023.

POLICY ADJUSTMENTS

The New York Federal Reserve issued two statements here and here as part of the suite of communications. The first link is the more meaningful adjustment in that it raised the individual counter-party limit on overnight reverse repurchase agreement operations facing the Fed to US$80 billion from US$30 billion previously. This had been debated as a policy option into today’s communications and it serves the effect of draining some cash from the banking system by potentially swapping cash for more Treasuries. It will help prepare the system for a coming liquidity surge as the Fed continues to buy US$120 billion of Treasuries and MBS each month and as the US Treasury deploys stimulus by drawing down its account with the Fed to distribute the proceeds. That liquidity surge could continue to put downward pressure upon measures of short-term rates and risk further steps toward negative rates; today’s step is one tool to help mitigate that risk.

The second link announced the end of purchases of agency commercial mortgage-backed securities due to “the sustained smooth functioning of markets for” CMBS. This announcement carries little effect as the Fed’s holdings of agency CMBS in the SOMA account have been roughly flat at under US$10B for several months now and most of the modest rise to this amount occurred up to June of last year.

FORECASTS—EVERYTHING UPGRADED

The forecast changes (here) were of two types. One was a necessary reset to catch up with consensus on major developments since the FOMC’s last forecasts in December and which showed the generally expected faster growth, lower unemployment and slightly higher inflation. Two was that the median rate projection remained unchanged, but something Powell said in the press conference should have us all fading that guidance that was conveyed in the dot plot.

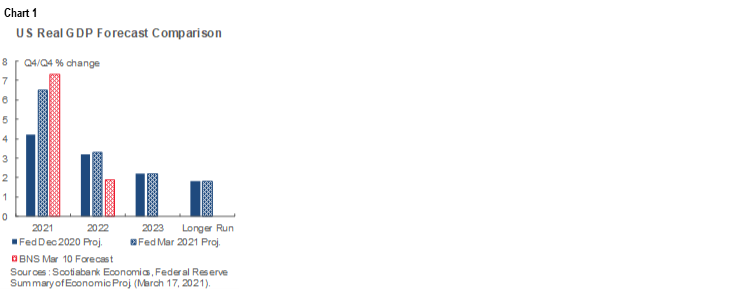

GDP forecasts (chart 1) were raised from 4.2% in 2021 to 6.5% and remain somewhat below our current forecast but above Bloomberg consensus that anticipates 6% growth this year. The FOMC also revised up 2022 by a tick to 3.3% from 3.2% which is stronger than we forecast and a tick stronger than consensus. The 2023 forecast was revised a touch lower to 2.2% from 2.4%. The message is that over the period during which peak fiscal policy effects on growth begin to dissipate into 2022 the Fed revised up growth and maintained solid growth expectations above the US economy’s long-run potential growth rate for at least each of the three years.

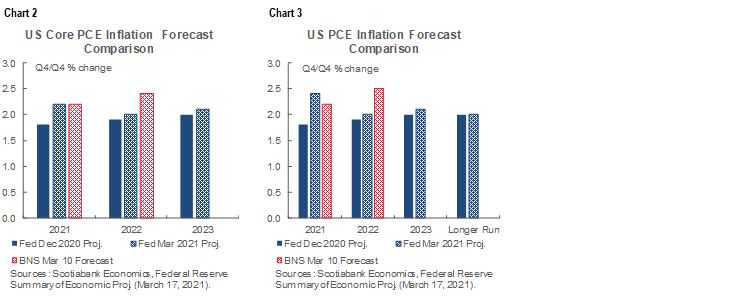

The inflation forecasts were also revised up a touch (charts 2, 3). The FOMC projects 2.4% in 2021 (1.8% prior), 2.0% in 2022 (1.9% prior) and 2.1% in 2023 (2.0% prior) for headline PCE. Core inflation forecasts were also revised up four-tenths to 2.2% this year and then by a tick in each of 2022 (2%) and 2023 (2.1%).

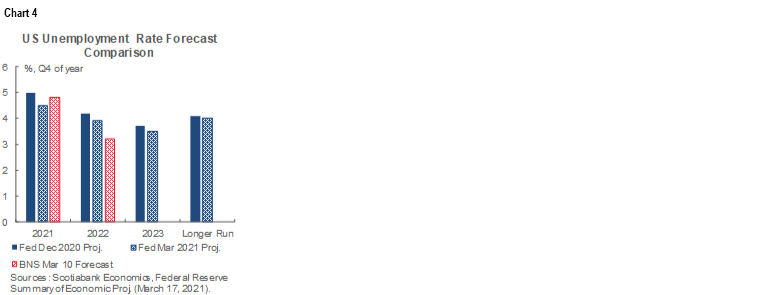

Unemployment rate projections were also revised lower (chart 4).

Before getting to what Powell said about the rate projections, what I continue to find befuddling is how a central bank can credibly say that it still thinks it will be providing emergency levels of stimulus ages after the emergency has passed while projecting a move into excess demand, full employment and inflation averaging slightly above 2% over the full forecast horizon. If you believe it, then the Fed isn’t showing the requisite willingness to alter its rate guidance in the face of major developments in vaccines and fiscal policy.

DOTS & WHY TO VIEW THEM SKEPTICALLY

The median rate projection remained unchanged at 0.1% but the composition of the dots was altered with more FOMC participants indicating rate hikes as soon as 2022 (chart 5, front page). It’s still the case that 14 officials expect no rate change next year, but instead of one forecasting a single hike, three forecast a single hike and one forecasts two hikes next year. For 2023, there are still 11 who forecast no change (down one from previously) but seven who forecast either 1 rate hike (1 participant), two (1), 3 (3) or 4 (2) hikes. The total adds to 18 forecasts, up from 17 the last time.

So what did Chair Powell say in the press conference that should not have markets taking the FOMC’s rate projections so literally and as alluded to above? When probed during the presser on whether the FOMC consensus is weakening with more participants showing hikes in 2022 and 2023, Powell said that the bulk of the FOMC is not showing a rate increase during the forecast period and that “part of that is wanting to see actual data and not just forecasting it.” So more—perhaps many more—participants would shift to hikes if their forecasts became reality? Isn’t a forecast supposed to be internally consistent in order to be credible rather than one component fudged? That says to me that the median rate path could well be adjusted higher with more participants showing hikes if the actual growth, inflation and unemployment forecasts turn into reality or if conviction increases over time. This suggests downplaying the significance of the median rate projection as potentially misaligned with the rest of the forecasts.

My belief is that the investors should not discount the possibility that the FOMC’s forecasts are less of a reflection of what they actually think will happen to inflation and rates going forward and quite possibly a reflection of the unwillingness to entertain greater risks on both counts at this stage. The FOMC is imposing judgement that inflation won’t overshoot and will magically hang in at 2% or so throughout the forecast horizon as the US economy moves into excess aggregate demand driven by unprecedented monetary and fiscal stimulus so they don’t have to show a median hike. Of course they did; to show, say, sustained 2.2+% inflation throughout that might have been more consistent with the rest of their forecasts for sustained above-potential GDP growth and a return toward a pre-pandemic unemployment rate would have led to aggressive questioning on the credibility of not showing a median hike and markets would have lit up. The Fed has no interest in tossing further fuel on the fire at this juncture.

So, it boils down to whose forecasts do you believe and how will the FOMC policy path change as data evolves and I’m not sure that we’re really any further ahead in the wake of these forecasts whatever the market reaction. We’re all in monitoring mode, but our bet is that core inflation will rise somewhat more than the FOMC is inking today and with that will come pressure to raise the policy rate into 2023 after beginning to taper purchases early next year and shutting down bond buying by the end of 2022.

STILL NOT FUSSED OVER BOND MARKETS

During the press conference, Powell reaffirmed that he’s not fussed by higher bond yields and indirectly rejected the option of altering purchases or engaging in an ‘operation twist’ of sorts by repeating the line that the FOMC believes the current stance of monetary policy to be appropriate. He continues to say that he would be concerned about a disorderly move in bond markets which places any potential for concern in a future tense rather than saying he is already concerned about developments to date. The message is that the FOMC remains quite content to have witnessed curve steepening in a way that continues to look like a whisper taper effect.

FEW STATEMENT CHANGES

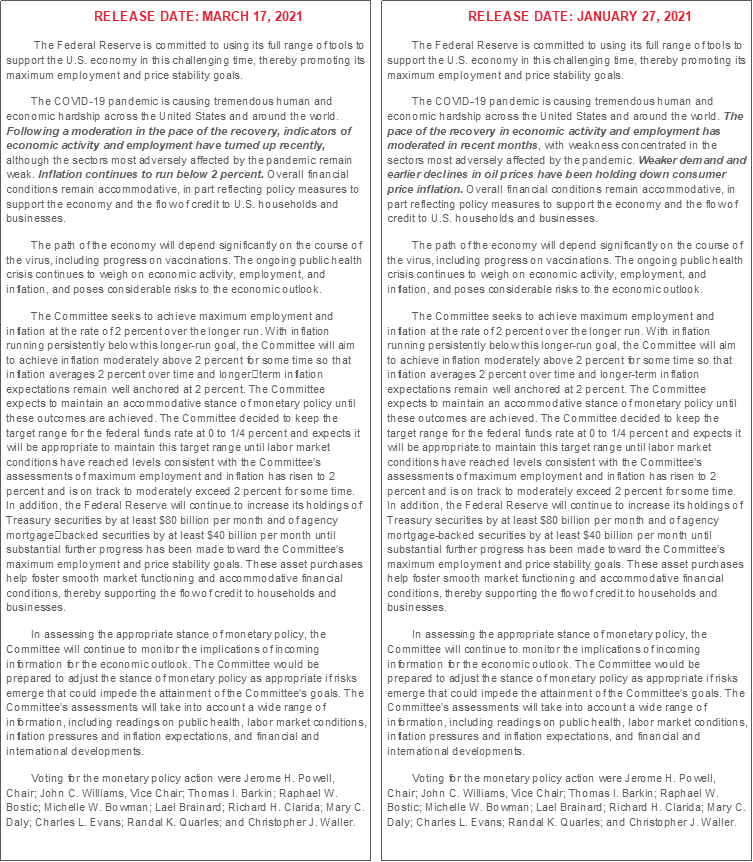

Statement changes were relatively minor but somewhat more upbeat. They were all in the second paragraph of the accompanying statement comparison. They struck out how the recovery has moderated in favour of having “turned up recently.” They also removed reference to declining oil prices holding down CPI—likely given the speed of ascent by oil prices—and now merely factually state that inflation remains under 2%.

BUBBLES

Powell downplayed concern about financial stability. He did so by saying they look at four things. First, on asset valuations, he said “Some asset valuations are elevated.” He did not elaborate, though at another point in the press conference he noted that financial conditions remain broadly stimulative as an offset to higher bond yields. Second and third, he noted that they look at household and business financial conditions and that “nothing in businesses and households really stands out” after taking account of how they entered the crisis and the combination of policy supports, financing activities and cash reserves. Third, on funding, he continues to emphasize that there will remain a focus upon seeking to further strengthen the system in the wake of the pandemic.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.