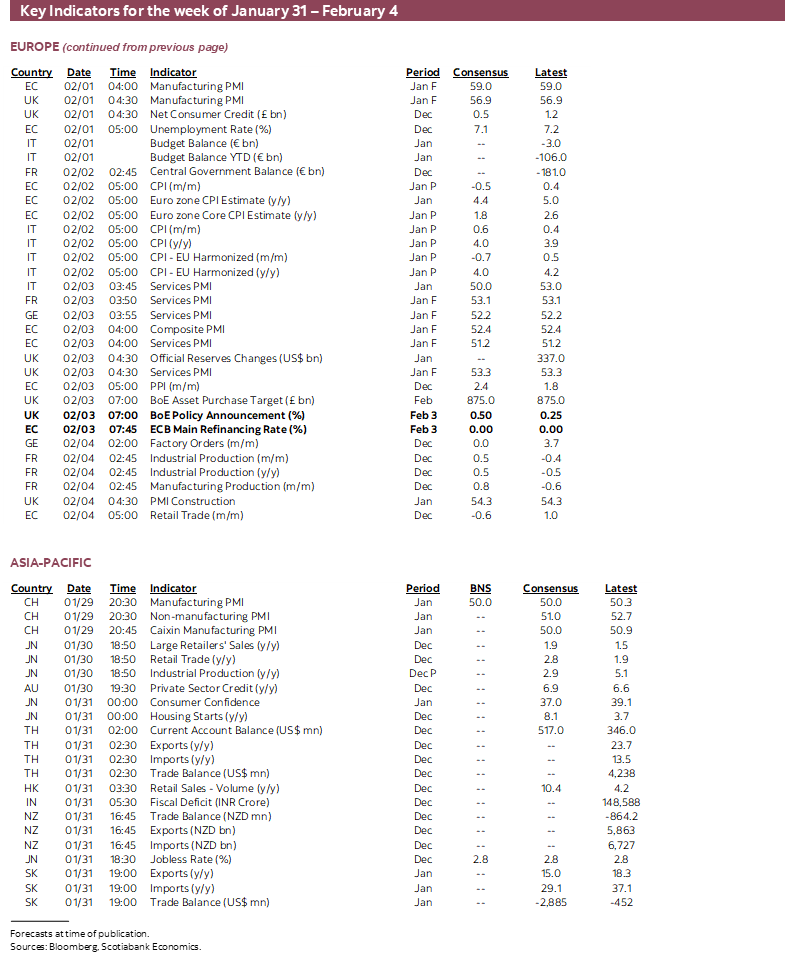

Next Week's Risk Dashboard

• Nonfarm payrolls: Uh oh

• Canadian jobs: Double that

• BoE: Hawkish pivot?

• ECB: Eyes on the Euro

• RBA: We’re so done with you, bonds

• Brazil: Keep on hiking

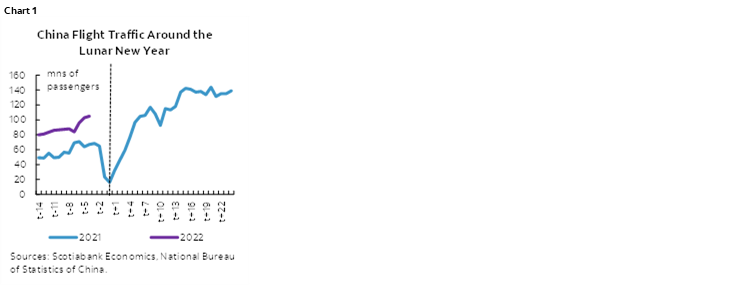

• China’s Spring Festival

• NZ wages to add to inflationary impulses

• Inflation: Eurozone, Peru, SK, Indonesia, Philippines, Thailand

• PMIs: China, US (ISM), India

• Other global releases

• Earnings

Chart of the Week

With Chinese and several neighbouring markets on holiday for the annual Spring Festival that is looking to be a touch brighter than last year’s (chart 1) the main focus will be upon the extent to which the Federal Reserve’s more hawkish pivot created spillover effects of consequence to other central banks in Europe, Australia and Brazil. Our pre-existing forecast for 7 Fed hikes this year is getting some assistance. Omicron’s sharp shock effects will also be evaluated when Friday’s US and Canadian jobs land and face material but probably transitory downside risk. Earnings season continues to unfold with another 106 US companies reporting including a continuation of tech sector reports.

CENTRAL BANKS—FURTHER PIVOTS AHEAD?

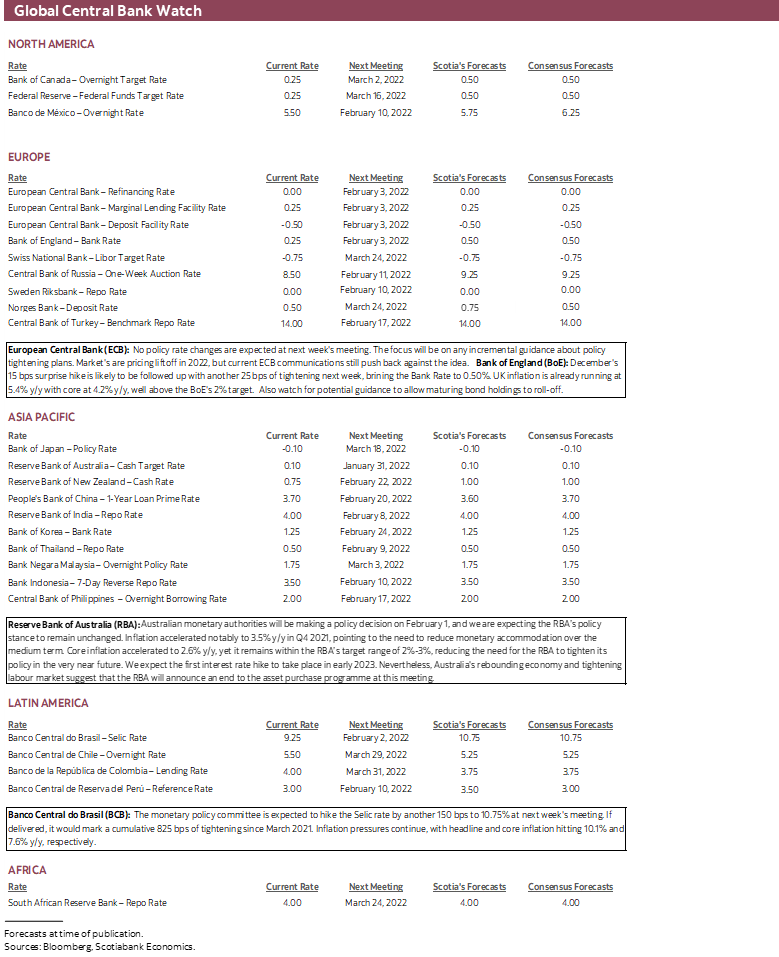

Four main central banks deliver another round of policy decisions. Key issues include the extent to which omicron is influencing their thinking around nearer-term and longer-term growth prospects and inflation risk tailored to unique domestic circumstances, but also whether the Federal Reserve’s more hawkish pivot and its ripple effects across global markets represent material new information. Two of the central banks are expected to hike, one is expected to end bond purchases, and all of them will have to address the magnitudes of market expectations for tightening cycles.

I. BANK OF ENGLAND—HOW HIGH CAN THEY GO?

Consensus almost unanimously expects a quarter point Bank Rate increase on Thursday. Markets are mostly priced for such an outcome. Markets are pricing a series of rate hikes over the duration of this year adding up to 4–5 quarter-point hikes by year-end. The problem? The Bank of England’s MPC members haven’t really said much of late, and Governor Bailey has garnered a bit of a reputation as being unreliable when he does provide guidance anyway.

A fresh round of forecasts will inform policy directions. Near-term growth downgrades and stronger inflationary impulses are likely. UK inflation is already running at 5.4% y/y with core at 4.2% y/y which is the highest core reading since June 1992 and far above the BoE’s 2% target (chart 2). That could also provide the impetus to start allowing quantitative tightening through allowing maturing bonds to start dropping off the balance sheet.

II. ECB—DID THE FED’S PIVOT CHANGE ANYTHING?

ECB President Lagarde is also on the defensive against a rising consensus and market pricing for rate hikes this year. Being between forecast rounds, the ECB will rely upon jawboning to assuage market concerns around ECB policy potentially falling behind inflationary pressures and on the heels of another CPI update this week.

Markets will pay keen attention to whether Lagarde repeats guidance from her remarks last month when she said “It is very unlikely that we will raise the interest rates in the year 2022.” On January 20th, Lagarde again emphasized how the Eurozone faces very different conditions than the Fed does while leaning against rate hikes this year. The complicating factor is that Fed Chair Powell subsequently turned more hawkish this past week (recap here) and the resulting USD strength is contributing to greater euro weakness. The euro is now trading at its weakest level since last June (chart 3). Amid building inflationary impulses, the risk of somewhat greater import price pass-through effects could well soften her conviction against any chance of a rate hike this year.

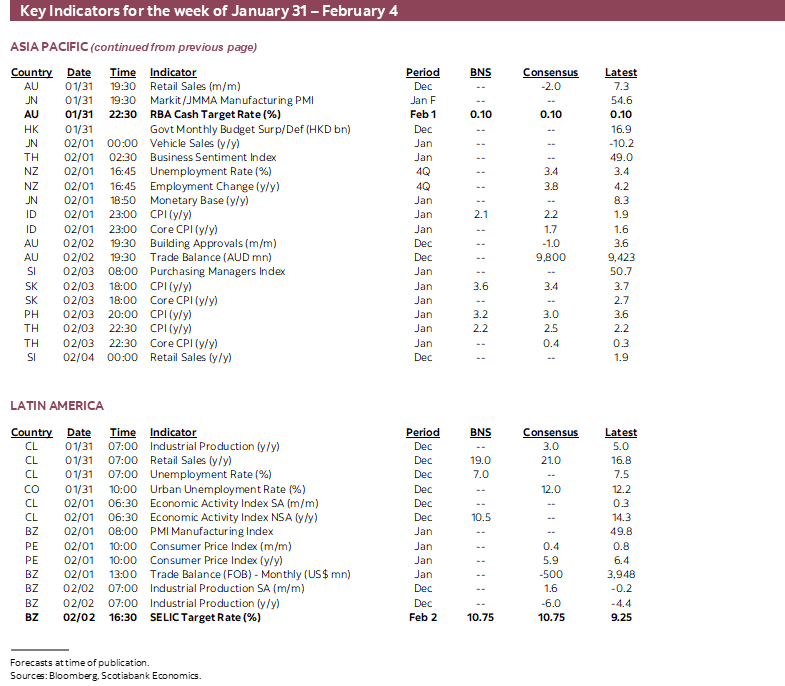

III. RBA—DONE WITH BONDS, RATES NEXT?

The RBA is widely expected to end its government bond purchase program when it delivers its policy decisions on Monday. It is ticking the box on the statement-codified criteria for reassessing its purchases at the February meeting.

First, it said it would consider the actions of other central banks; the Fed’s move toward ending bond purchases in March and intimating it could allow roll-off of maturing securities as soon as Q2 or later this year will factor.

Second, it said it would monitor the functioning of the government bond market, and so the rates sell-off that has taken the 3-year yield up by 60bps this year will likely figure prominently.

Third and “most importantly” the RBA said it would monitor actual and expected progress towards the goals of full employment and price stability. Inflation is soaring especially when q/q annualized increases in the central tendency measures are considered (chart 4). Further, Australian jobs have climbed by 431k in two months and more than recaptured the 360k drop during restrictions over the prior four months which will likely offset potentially transitory omicron effects into early 2022.

At least as important will be potential guidance around timing a rate hike. The December statement noted that the Board will not increase the cash rate until inflation is sustainably within the 2–3% target range and the job market has tightened to support wage pressures. The RBA will want more evidence on both fronts to have enough confidence to pull the trigger, but a consensus among economists and traders is building around achieving such criteria at some point over 2022-H2 (economists) or mid-year (futures) and hence earlier than RBA guidance to date.

IV. BRAZIL—SOME EXPLAINING TO DO

The BCB’s decision on Wednesday will likely see the Selic rate hiked by another 150 bps to 10.75%. If delivered, it would mark a cumulative 825 bps of tightening since March 2021 and would cement the BCB as the most aggressive policy tighteners amongst major economies to date. Inflation continues to run hot, with headline (10.1% y/y) and core (7.6% y/y) inflation in December well above the bank’s target range (chart 5). In a mandatory year-end open letter penned by the BCB to the public providing explanations for its inflation target miss, the bank stressed a “significantly restrictive” monetary policy to control prices over the coming years. Forecasters expect the Selic rate to reach anywhere between 11.50–12.00% by mid-2022 and be held there into the following year before potential loosening.

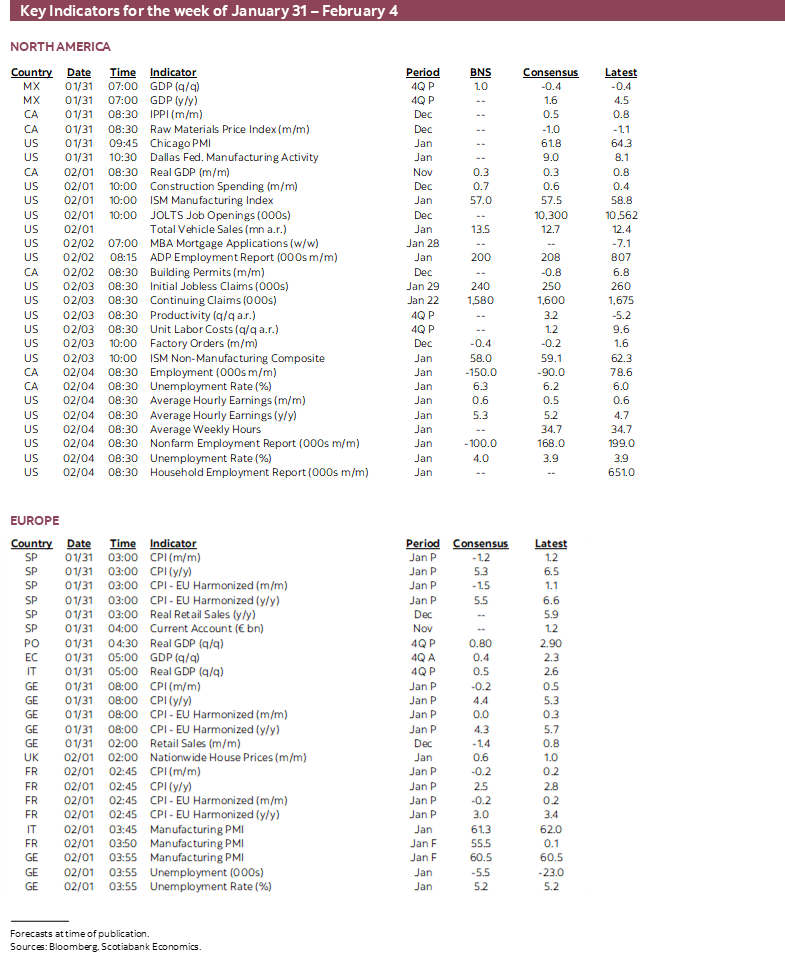

NONFARM PAYROLLS—BIGGEST DOWNSIDE SINCE THE PANDEMIC BEGAN?

Employment might have taken a step backward to start the year. Friday’s nonfarm payrolls are expected to decline by about 100,000 with a mild upward tick in the unemployment rate to 4%. Wage gains are expected to push the year-over-year pace over 5% driven by another monthly gain of about ½% m/m or more.

The United States did not meaningfully embrace tightened restrictions against the omicron wave like its northern neighbour and many European economies did. Chart 6 shows a comparison of US and Canadian stringency measures. On the surface, this might mean that the US job creation machine could keep moving in a forward direction—and it might. If so, then that would be strong evidence of resilience.

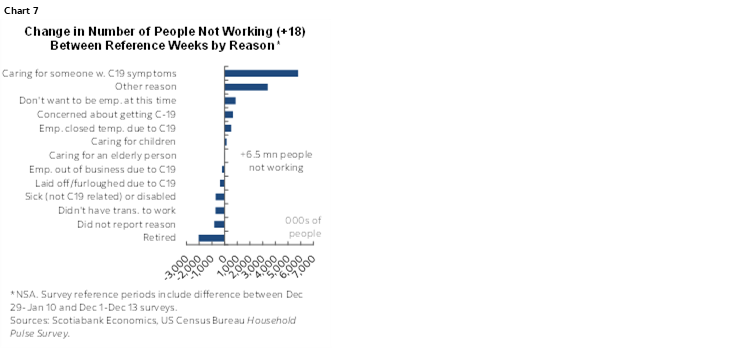

There are, however, two perspectives that explain the caution. Apart from the common-sense factor that might have driven a softer level of engagement with the workplace due to omicron during January, we can point to some soft survey-based evidence of such behaviour. To do this we again used the Census Bureau’s Household Pulse Survey that seeks to measure changes in the number of people not working for varying reasons. We take changes in the responses between nonfarm reference periods (the pay period including the 12th day of each month) as proxies for changes in the attachment to the labour force.

Chart 7 depicts the results. There was a massive ~6 million surge in the number of people who said they were not working in the January nonfarm reference period compared to December because they were caring for someone who was sick with COVID-19 symptoms. A net total of 6.5 million additional people said they were not working in January over December for any of the listed reasons. Many of these reasons are subject to normal volatility, some of which can be seasonal, but it’s the swings in the pandemic-related responses that are meaningful and that have generally served as a useful indicator for estimating swings in payrolls.

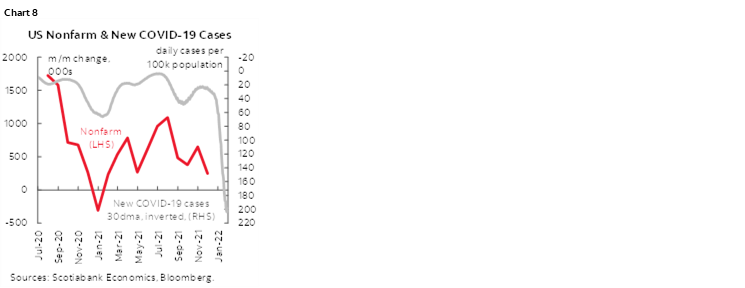

Secondly, chart 8 shows that when pandemic cases rise they tend to drive weaker payrolls. The rise in reported cases this time around is definitely more understated than prior waves but is nevertheless off-the-charts. That could mean that the risk to the above nonfarm estimate may be skewed toward a materially worse number than the forecast that is always issued with trepidation even under more ‘normal’ circumstances.

Of course, for those brave enough—or perhaps fortunate enough—to face omicron in a very tight labour market there may be some recompense in the form of accelerated wage gains.

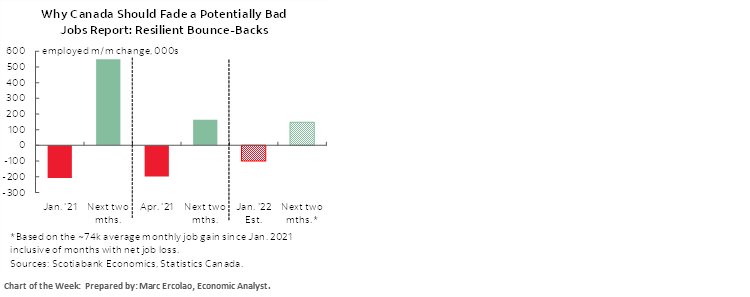

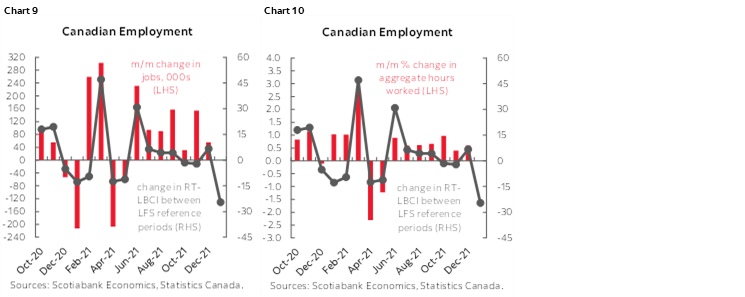

CANADA PROBABLY LOST JOBS IN JANUARY

Canada is likely to post a significant loss of jobs during January when the latest batch of figures arrives on Friday. The signals we are reading also indicate a proportionately greater loss of hours worked and hence reduced cash flow since people who retained employment might have sharply reduced hours during restrictions and school closures.

My guesstimate is that we’ll see something on the order of 150,000 lost jobs. While this will be driven by omicron and related restrictions and is likely to be transitory, it will complicate the optics around a potential BoC rate hike at the March 2nd meeting. They may have held the policy rate this past week because of omicron concerns, despite evidence it is probably fading (e.g. hospitalizations and wastewater tests) while being an added inflationary impulse, but will they then hike when the only jobs report they’ll get before March 2nd is potentially a large drop?

Charts 9 and 10 depict the signal being sent by one of the better advance job survey indicators. The change in Statistics Canada’s Real-Time Local Business Conditions Index correlates reasonably well with monthly changes in jobs and hours worked. It is a composite of readings drawn from Statistics Canada’s Business Register that tracks business revenue and employment, plus mobility readings from Google Places, Yelp Fusion and Zomato as well as TomTom’s Historical Traffic Stats. StatsCan has done well at offering such a reading largely based on alt-data.

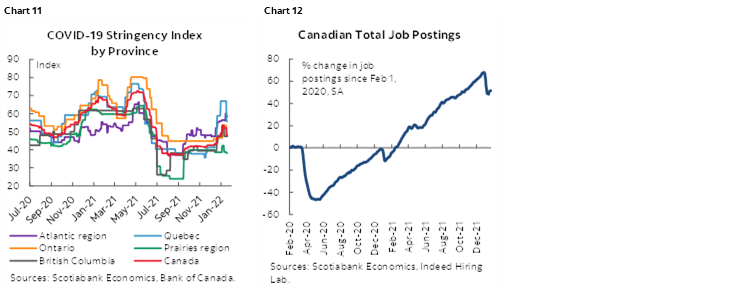

The steep plunge in this composite reading suggests we could see the largest decline in employment witnessed since the earliest days of the pandemic. Some of this is because of self-preservation as many people generally hunkered down through omicron. Some of this is due to tightened restrictions across the country (chart 11) and relative to the United States (see earlier chart 6). We can also observe a larger than usual drop in job postings (chart 12).

One reason why a low six-figure decline might be a reasonable call versus really going more harshly negative on the back of this one indicator is that perhaps hours worked bore more of the brunt of the adjustment. Coming off holidays could have had at least some payroll employees tapping into freshly reset vacation and sick days for fear of being too close to all the sickies. Further, the labour force is better adapted to such shocks now with greater use of technology, work from home and mobile work arrangements.

In any event, as the chart of the week illustrates on the cover of this week’s issue, there is ample evidence that shocks to employment like omicron tend to quickly reverse. To this effect, survey-based measures of hiring intentions remain strong.

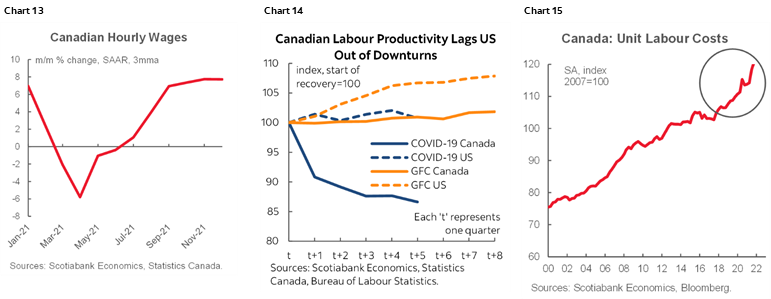

Also watch wages. Month-over-month wage growth has been in the 6–9% seasonally adjusted and annualized range for six months now as a clear sign it has accelerated (chart 13). With Canadian labour productivity tanking (chart 14), unit labour costs (a productivity-adjusted measure of employment costs) are accelerating (chart 15). We should probably expect more of this through 2022–23. And, no, sorry to burst anyone’s bubble but there is no material estimated effect of immigration on wages in the literature even if the rise in Canadian immigration to date wasn’t fake since about 75% of the past year’s “surge” was only due to converting temporary status to permanent.

OTHER GLOBAL MACRO—IT’S NOT ALL ABOUT NONFARM

Central banks and North American jobs will dominate much of the focus across global markets but the rest of the global macro calendar will also contain some key entries.

The Eurozone updates January inflation on Wednesday and Q4 GDP on Monday (+0.4% estimate). Price increases are expected to pull back to 4.4% y/y from 5.0% y/y the month prior but may not go quite that far. France updates CPI on Tuesday along with Italy and after Germany and Spain reported somewhat stronger than expected figures on Monday. The reading will likely be shrugged off in light of the bigger theme of persistently high Eurozone inflation in 2022 and how that feeds into the ECB’s policy guidance in the early stages of the year. Energy price pressures, domestic demand, and continued supply chain bottlenecks all feed into the upward revision in ECB’s 2022 HICP forecast of 3.2%.

Other US indicators will fade behind nonfarm, but there will be a few gems:

ISM sentiment gauges will further inform omicron’s fuller effects upon current growth, appetite for hiring, input and output price pressures and new orders. Anecdotes provided by purchasing managers could be especially informative in terms of impressions around the expected longevity of the shock. Other manufacturing surveys generally suggest January’s ISM-manufacturing reading (Tuesday) will fall. The Empire and Richmond Fed regional surveys landed softer, while the Philly Fed’s measure moved higher and the KC Fed’s gauge only edged up due to downward revisions to the prior month. Markit’s manufacturing PMI also includes international operations of US companies—whereas ISM is focused upon the domestic economy—but the Markit PMI also fell in January.

A deeper decline is likely in the ISM-services reading (Thursday) given the probably more negative impact upon high-contact services, though the packed stadiums and arenas at sporting events might suggest less effect!

Also keep an eye on vehicle sales on Tuesday that are forecast to rebound to ~13.5 million (12.44 million prior). Advance industry guidance for the earlier part of the month points toward a milder rebound that may have gathered steam later in the month.

Canada updates GDP growth for November but more importantly provides initial flash guidance for December. Earlier guidance for November pointed to a gain of 0.3% m/m. December should post a tidy gain. After a 0.7% m/m rise in hours worked during November, a further 0.3% gain was registered in December. That matters given GDP is an identity expressed as hours worked times labour force productivity. Proxies for productivity that rely upon activity readings are mixed. Preliminary December estimates point to a 0.8% m/m rise in nominal manufacturing shipments, but also a -2.1% drop in the value of retail sales, unchanged wholesale sales, and a -22% m/m drop in housing starts albeit mostly in multiple unit housing that tends to have lower value-added per unit. A positive print for December would have to rely upon hours worked, manufacturing and service-related categories especially over the first 2–3 weeks of December before omicron took over.

Even with Chinese financial markets shut for the Spring Festival around the Lunar New Year, we still got some meaningful macroeconomic readings. China released the January editions of the state’s purchasing managers’ indices this weekend. The state composite PMI declined 1.2 points to 51 and hence is still in expansion territory with the manufacturing PMI at the dividing line (50.1, 50.3 prior) and most of the adjustment impacting the non-manufacturing PMI (51.1, 52.7 prior) as zero-COVID bites. The private manufacturing PMI fell into contraction (49.1, 50.9 prior) and places more weight upon smaller producers in coastal manufacturing regions compared to the SOE-dominated state PMIs.

RBNZ-watchers just got an inflation jolt and now they’ll turn their attention to the state of the labour market. On Tuesday (eastern times as always) we’ll get the change in employment and wages during Q4. Employment growth is expected to moderate substantially from the large Q3 gain but continued strong wage growth is expected (chart 16).

Also note that we’ll get some more Bank of Canada-speak. BoC Governor Macklem and SDG Rogers will virtually deliver parliamentary testimony on Wednesday at 3pmET. These appearances have gotten a touch spicier of late and expect aggressive grilling around the BoC’s decision to hold off on a rate hike that was nearly fully priced and in the context of soaring inflation and house prices. Deputy Governor Gravelle also speaks on a panel on benchmark rate reform on Wednesday.

Latin American markets will focus upon the ripple effects of central bank tightening (Chile and Colombia this past week, Brazil this coming week) but limited data could also factor into market sentiment. Mexican Q4 GDP growth is forecast to decline by another 0.4% q/q SA non-annualized (Monday) and PMIs arrive the next day to inform how the economy is coping with omicron into the new year. Peru’s inflation rate (Tuesday) is forecast to slip back beneath 6% y/y with a more temperate pace of month-over-month increase.

Other focal points will include CPI readings from Indonesia (Tuesday) and then South Korea, Philippines and Thailand (Thursday), Australian retail sales during Q4 (-2% q/q consensus, prior +7.3%, Monday), India’s purchasing managers’ indices (Tuesday) and the usual monthly data dump from Japan to start the week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.