- Markets raise pricing for Fed hikes...

- ...as our aggressive Fed forecast got some support today

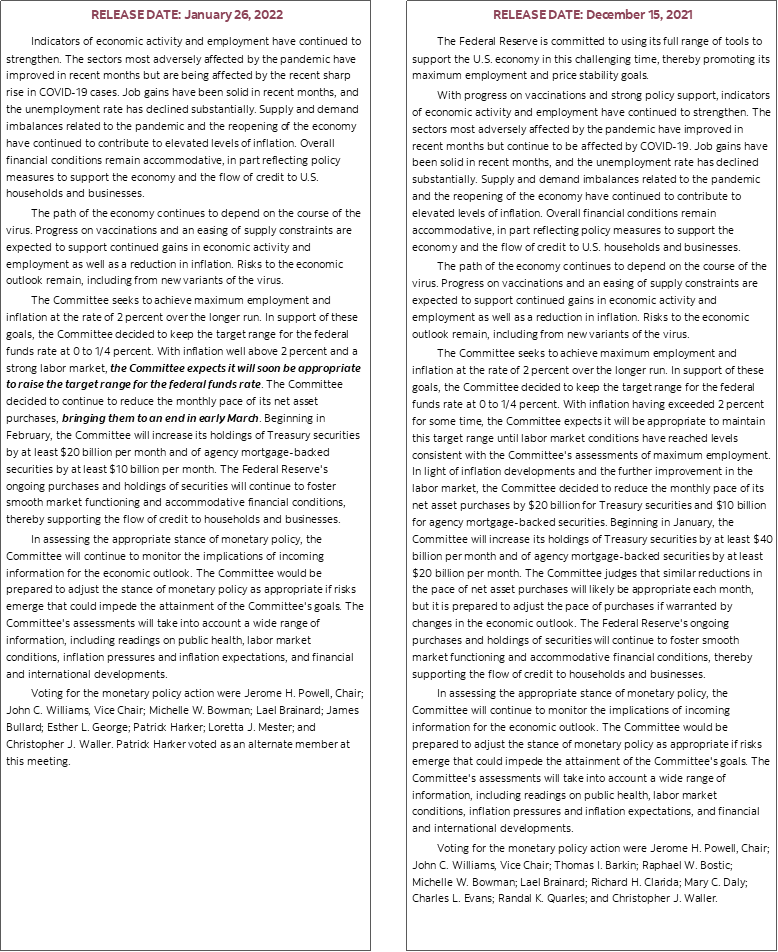

The Federal Reserve generally met most of our expectations today but with some important twists that added a materially more hawkish slant. As a consequence, the whole US rates complex sold off today. The two-year Treasury yield soared by about 13bps through the whole suite of communications as the 10 year yield increased by almost 8bps. The dollar jumped by about ½% on a DXY basis. The S&P500 fell by about 1¾% from the start of the communications in to the close.

Please see the accompanying statement comparison, the Fed’s separate release that added a little more to balance sheet plans (here) and the NY Fed’s implementation notice (here).

What shocked markets leans a little further in the direction of our forecast for materially greater Fed rate hikes than are priced in fed funds futures this year. Recall that the December dot plot guided to expect 3 hikes this year, fed funds futures increased pricing to expect 4½ quarter-point hikes this year and we forecast 175bps to a 2% upper limit.

There were three main issues that drove this market reaction.

1. POLICY RATE: FASTER & HIGHER?

Powell was asked during the press conference whether hikes at consecutive meetings are on the table, whether each meeting is ‘live’ in terms of hike risk, are individual rate hikes in amounts over 25bps possible and would he front-load rate hikes earlier than later?

Let’s just say that markets didn’t like the fact he generally ducked all of these. An experienced central banker seeking to manage markets and tamp down such speculation if he had conviction to do so would have probably leaned against such fears or sounded circumspect with two-sided guidance. The fact he did not do so and instead sounded wishy washy didn’t go over so well and that’s the moment at which yields took off.

Powell did not answer yes, but also did not shoot down these scenarios. He only said “It is not possible to predict with much confidence what path our policy rate will follow. We’ll be humble and nimble and guided by the data and the evolving outlook. We will act with transparency.” Humble? You mean like stridently dismissing inflation risk??

Powell went on to say that “We have not made these decisions on the size of hikes. We fully appreciate that this is a different situation. Back in 2015 –18 we were raising rates but unemployment was not at our natural rate and inflation wasn't where it is now. We also have growth substantially above potential this time and a labour market by so many measures that is historically tight.” That to me sounds like a central bank head who is definitely open to faster and higher hikes this time and perhaps with a fiddy or two slapped down on the table. At present we have +25bps at every meeting this year from March onward.

Powell remarked that “This is going to be a year in which we move steadily away from the very highly accommodative policy. This will involve ending asset purchases, lifting off, and additional increases that we will reconsider at the March meeting. Then we will allow the balance sheet to run off as appropriate. I don't think it's possible to say exactly how this is going to go. The economy is quite different this time across multiple readings.”

2. COMING FORECAST CHANGES?

Secondly, when asked how recent developments may impact FOMC forecasts, Powell responded by stating "I'd be inclined to raise my core PCE forecast by a few tenths today" relative to the December forecast. That was a clear indication that the Fed Chair is more worried about inflation now than at the December meeting. He noted that “I am not saying supply chain problems will be solved this year. We’re not making progress at the moment. I think semiconductor problems will go more than through 2023.”

On the dots, he also noted “We wrote down policy rate forecasts at our December meeting. If it deteriorates further then we'll have to think about that” with ‘it’ being inflation risk. That was a signal that the three dots forecast for this year in the median projection could be raised at the March meeting.

3. SOMA: SMALLER AND SOONER?

Thirdly, the language around when roll-off of maturing securities will commence was ambiguous. Chair Powell had previously said ‘later’ this year but after pulling forward rate hike guidance to March in the statement they left it more open in terms of when roll-off may commence by just saying after lift-off. That could mean our prior assumption that maturing securities start dropping off in Q4, or it could mean as soon as Q2 this year following a hike or two. During the press conference, Powell said ‘no decisions have been made’ on either timing or the pace at which maturing securities will be allowed to drop off.

Otherwise, the Fed’s guidance generally met expectations through the following steps.

1. March lift-off.

The FOMC statement-codified reference to a planned rate increase at the March FOMC meeting. They did so by explicitly referencing “it will soon be appropriate to raise the target range for the federal funds rate.” That is Fed-speak for the next meeting.

2. On track to end net purchases in March

They also statement-codified intentions to end net purchases of Treasuries and MBS in March. The purchase path that had been previously laid out and the general guidance pointed toward such an outcome but now the FOMC is cementing such plans.

3. Reaffirming the order of operations

The separate notice outlining principles for reducing the balance sheet stated that “reducing the size of the Federal Reserve’s balance sheet will commence after the process of increasing the target range for the federal funds rate has begun.” The notice generally reinforced that the policy rate will be the main tool, that balance sheet reductions will be done “in a predictable manner primarily by adjusting the amounts reinvested of principal payments,” and reaffirmed that the longer run goal is to only hold Treasuries (not MBS).

4. No guidance on other balance sheet tools

On balance sheet guidance, Powell was asked “What does it mean to significantly reduce your holdings? Are there any other ways you are thinking about recalibrating this process? Would you consider asset sales.” Powell’s response was “Those are all great questions but the committee is just turning to them now” and promised that at the next meeting they plan on discussing more of the details. Detailed plans were not likely to arrive today and were not expected.

5. Controlling the curve?

Powell did, however, pass on an opportunity to intimate that the FOMC thinks it can steepen the yield curve through balance sheet policies. When asked what is the rate equivalence on shrinking the balance sheet to hikes he said “There are rules of thumb that I am reluctant to weigh in on. Our primary tool is the policy rate.” He followed that by saying “We monitor the slope but don't control it.” That matches our belief that unless we’re holding fire sales anytime soon the Fed’s reinvestment tools are very unlikely to materially raise the term premium through releasing more net supply into the bond market in isolation of all the other drivers of the bond market.

There are three final issues worth flagging from the press conference.

Does Equity Market Volatility Concern the Fed?

When asked how does recent market volatility impact the FOMC’s thinking, Powell responded somewhat dismissively by noting “We look at broader conditions and ask if we are seeing them as consistent and material.” He also said “I don't really think asset markets represent a big risk to stability. They are manageable. Household balance sheets are strong. Banks are well capitalized.” The implied tone was that they are not fussed by equity moves thus far in relation to broader conditions.

Balanced Risks

When asked about the risks to the Fed’s views, Powell said “There is plenty of risk out there and we can’t forget there are risks on both sides” in reference to upsides and downsides. On the hawkish side he noted high inflation and the risk it could move higher than the Fed’s base case. He also flagged supply chain challenges such as in China, and briefly mentioned tensions in eastern Europe clearly as a reference to Russia-Ukraine.

The Fiscal and Monetary Policy Dance

Powell leaned toward a somewhat contentious point that fiscal policy is going to shave growth going forward. There are two counter points here. One is that state and local governments need to be considered. Second, there is a stock versus flow argument in that the stockpiled fiscal stimulus on household balance sheets evidenced by enormous cash balances as stimulus cheques and expedited child benefit cheques were significantly retained could be stimulus that keeps on giving as some of the proceeds are gradually spent.

Did the Fed Go Overboard?

Powell was asked did fiscal and monetary policy do too much and hence drive high inflation he perhaps not surprisingly shrugged it off by saying that will be for historians 25 years from now to tell.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.