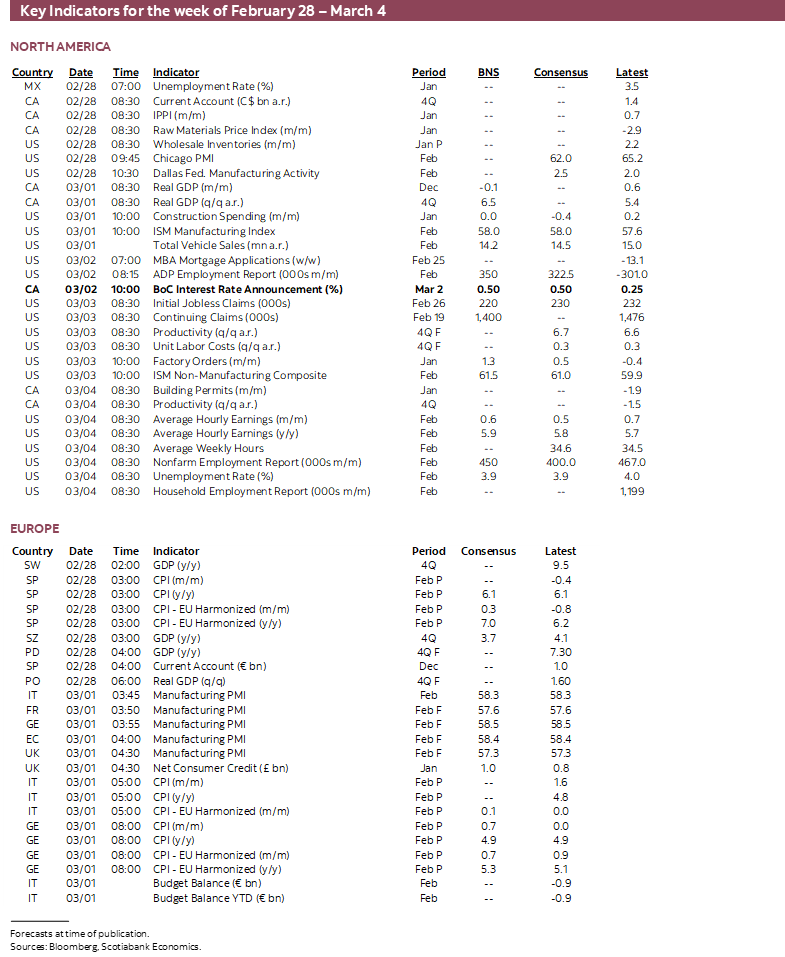

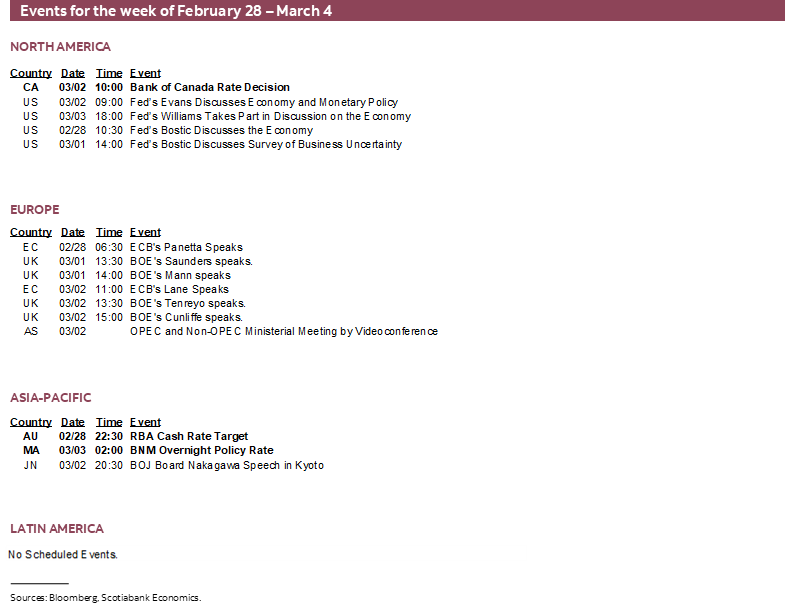

Next Week's Risk Dashboard

• Are markets fairly judging war risks?

• How central banks may respond to developments

• Fed’s Powell to testify

• BoC set to lift-off

• RBA is probably still ‘patient’

• OPEC meeting might be livelier than expected

• Nonfarm payrolls poised for another solid gain

• CDN bank earnings to continue

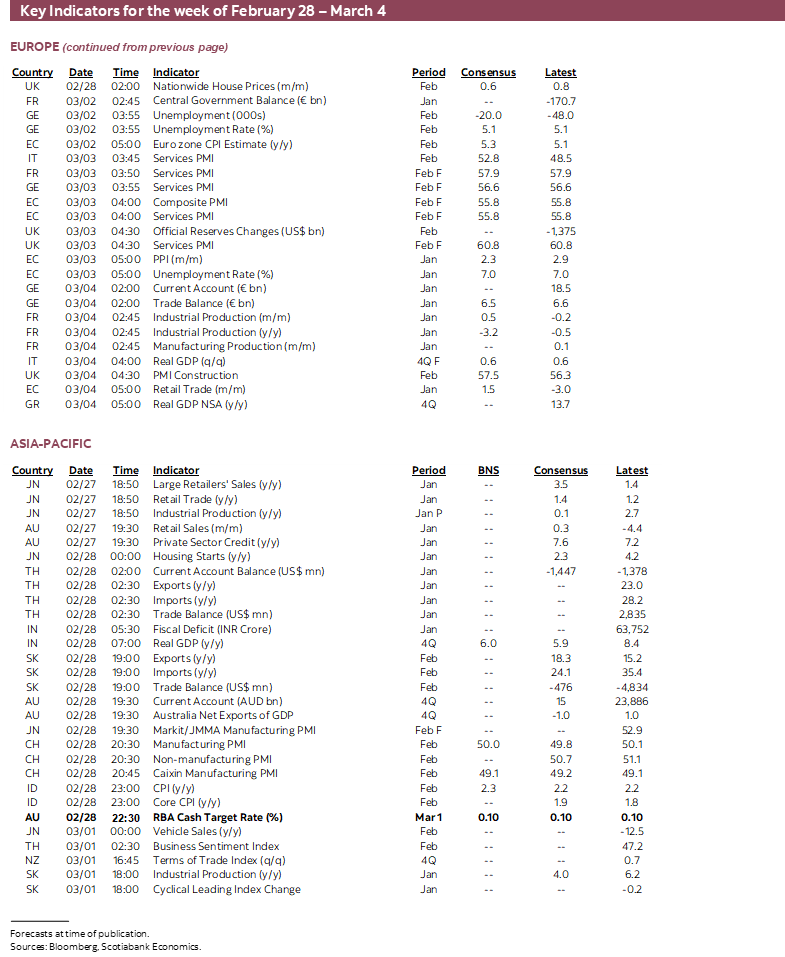

• Eurozone inflation set to accelerate again

• PMIs: US, China, India

• Canada’s economy: soft end to a strong quarter?

• Other macro

Chart of the Week

Has risk appetite been little affected by the course of developments in Ukraine because we’ve had our wysiwyg moment? That’s it, we can’t do anything more about Russia, so what you see is what you get in terms of the limited counter measures? Or are global markets incapable of judging complex developments and are therefore a poor judge of evolving considerations?

It merits reminding ourselves that the S&P500 rallied on September 1st 1939 and kept rallying for weeks until it didn’t in 1940, so perhaps treat what Ms. Market says about current events with a mountain of salt.

Still, for the moment, it may well be that risk appetite is at least temporarily correct in assuming that the limited response from the allies will make this all pass as little more than a regional war with limited consequences for your investments. I’ll come back to how this might be premature, but start by laying out the case for why markets may be thinking this way.

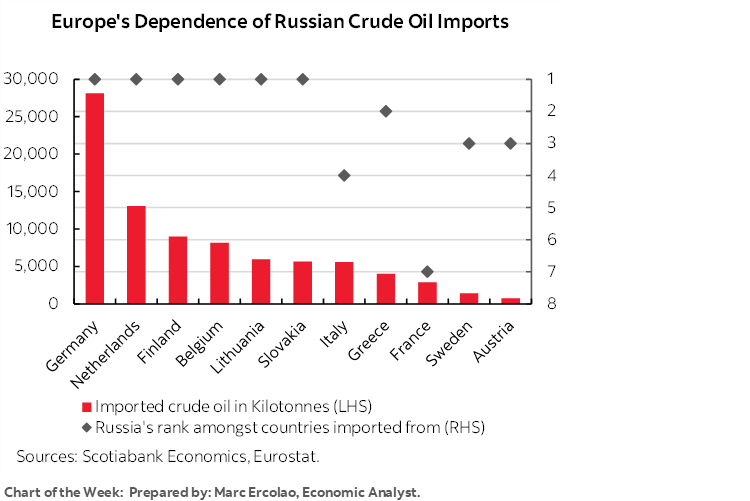

I’m speaking in reference to the very real likelihood that the major policy options surrounding how to stand up to Russia may now have been spent. The remaining policy options are some combination of thoroughly unpalatable or practically unfeasible and nearly impossible to coordinate across a dysfunctional cast that is partly due to the fact that many of them made themselves hostage to Russia as this week’s cover chart illustrates. If so, then the resulting outcome may very well be that what we’re left with is no doubt a great tragedy for Ukrainians, a deep further insult to our collective sense of morality and a major regional war – but with limited further consequences that drive investors to plug their noses and get back to buying snps.

Why? Because the reasonable options for confronting Putin may have been exhausted.

- For one, the US has sensibly ruled out a direct confrontation. So has Europe which is busy being Europe anyway.

- Blocking Russia’s use of the US dollar may be ineffective on its own and intractable with unintended consequences that I’ll return to below. Ineffective because Russia reportedly only has about 16% of its reserves in USD now and has been dramatically reducing this share over recent years perhaps as Putin was preparing for this day all along. Russia’s access to euros, yen and sterling would also have to be cut off which requires broad agreement for each affected country and consideration of the longer-term ramifications.

- It’s unlikely that Putin can be effectively sanctioned notwithstanding moves by some like the US and Canada to do so. That’s because the magnitude and whereabouts of his financial dealings may not be fully or even partially known.

- Russia probably cannot be kicked out of the SWIFT global payments system for several reasons including:

- due to the risks to global markets including potential counter-party risk with non-Russian banks. The aim is to maim, not kill the Russian economy which counsels not fully blocking its access to foreign currencies and global payments systems. If Greece can risk bringing the European and global financial systems to their knees, then Russia’s larger economy could inflict greater damage.

- because SWIFT is governed by European law, not US law, and so the US might have had to threaten sanctions against SWIFT in order to coerce it into blocking Russia.

- to avoid providing incentive to create an alternative payments system. In fact, Russia has already been developing its own System for Transfer of Financial Messages (SPFS) platform that reportedly includes hundreds of Russian member banks already. Blocking Russia’s access to SWIFT could further accelerate the development of alternatives and hence harm financial interests of the US, Europe and others. In fact, it’s arguably the case that under former President Trump’s watch, Putin’s efforts to grow reserves and diversify them away from US dollars and to create an alternative payments system reflected efforts to mitigate the effects of policy responses to the day when the order to invade was granted.

This latter point is important. It's why Biden says that sanctioning Russian banks is more effective since otherwise they could move their payments transactions through alternative channels if all that was done was to block their participation in SWIFT.

If we recall a bit of our history of the development of financial markets, then there is another reason that can be drawn from past lessons for why sanctions may have hit a wall. If the US were to lead a move to block Russian use of the USD and other reserve currencies and block Russia’s use of the SWIFT payments system, then it could risk repeating the historical mistakes made by the US that resulted in the creation of offshore Eurodollar markets. A series of US policy measures in the late 1950s through to the early 1980s reduced faith and trust in the US financial system, pushed business elsewhere and to this day indelibly imprinted upon the minds of regulators and policymakers the need to be extremely careful toward potentially unintended consequences of their actions.

For example, when Russians were worried about US seizure of Russian holdings of USD assets in the late 1950s and early 1960s, the term 'Eurobank' was coined by the Soviets when they began depositing funds in France in a bank with the financial address being "Euro-bank". Eurocurrency markets got their start precisely because business shifted offshore as the US underestimated the unintended effects of past policy stances and ironically it was the Russians who started it.

When the US imposed the Interest Equalization Tax and later went on to freeze Arab and Russian deposits at US banks, the effects were widely cited as among the major reasons for the creation of the euro markets. The Interest Equalization Tax was introduced in 1963 and taxed foreign borrowings in the US in an attempt to reduce acquisition of USD by foreigners. That gave the incentive to foreign branches of US banks to start floating dollar-denominated bonds, or eurobonds, that paid lower interest than available in the US market given the tax. The number of US bank branches abroad subsequently mushroomed. 'Regulation Q' in 1982 further exacerbated this push toward euro markets by imposing a ceiling on domestic deposit rates and a funding crunch on US banks that then had them going abroad to attract funding at foreign branches that in turn lent to their US-based bank headquarters. Regulation Q also served as a fundamental driver of the thrift crisis later on.

The rest is history, as they say. The result was to push a lucrative market outside of the US and with it capital, jobs, expertise and a substantial tax base. So, the point is that when even the US tinkers with the financial system, the unintended effects can be very painful in terms of US interests. Russia likely knows this and in no small part because it perhaps knows the history around the issues and it’s involvement.

In the end, it may not be an implausible scenario if one were to suggest that Ukraine’s economy will be tragically devastated and Russia’s economy and financial system will suffer serious setbacks, but it’s ultimately a regional war sans deeper global ramifications. With China’s Xi Jinping at least on the surface suddenly insisting that Ukraine’s territory and sovereignty should be respected and calling for a negotiated settlement, the message to Putin may be don’t count on support from China either, even if it is just in the form of passive opposition. Maybe. Just maybe. If so, then the effects upon the limited sphere of financial market consequences could be a further illustration of how geopolitical shocks tend to have transitory and limited effects.

The counter narrative that only time will inform is whether the allies have enabled Putin to pursue more aggressive acts in future. There remain the risks of spillover crises, accidents that are unfortunately common in wartime, a humanitarian crisis of potentially epic proportions and that pressure on allies to do more than just appearing to be paper tigers may rise as the tragedy deepens.

The pain from sanctioning Russian banks, oligarchs, and technology transfers may nevertheless be limited in relation to Putin’s years of planning for this assault by beefing up Russia’s foreign reserves, paying down its external debts, developing an alternative payments system and diversifying FX exposures away from the dollar. For now, the allies are unwilling to go further than limited sanctions and tersely worded addresses. Some of that is due to implementation challenges and some of it is because the allies don’t wish to go so far in standing up to Putin that they risk any damage to their own economies. In my personal view, I think they can and should go further. History counsels such a course of action.

CENTRAL BANKS IN THE AFTERMATH

The next logical question is how all of this may affect central banks. Next week brings forth policy decisions by regional central banks like the Bank of Canada, the Reserve Bank of Australia and Bank Negara. It’s also worth exploring how others—particularly key central banks—may respond.

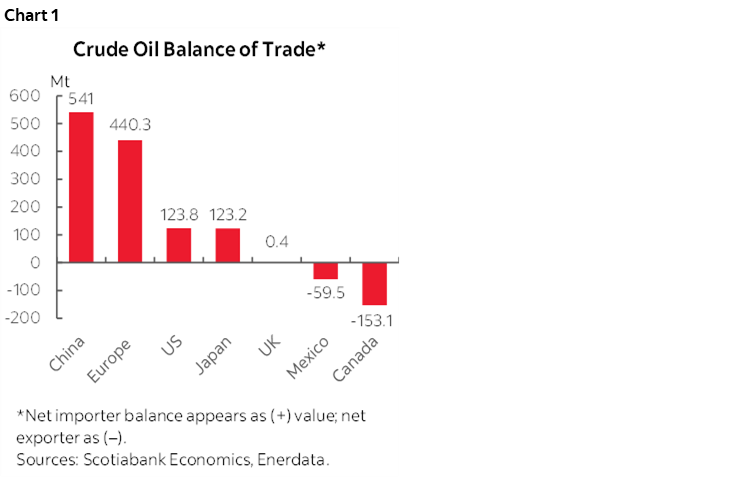

An important point to bear in mind in evaluating the possible incremental impact of the Russia-Ukraine war and its effects on relative central bank postures is the net oil importer status of the monetary policy region. Chart 1 portrays the exposures as the backdrop to a few points that can be made about each of the central banks.

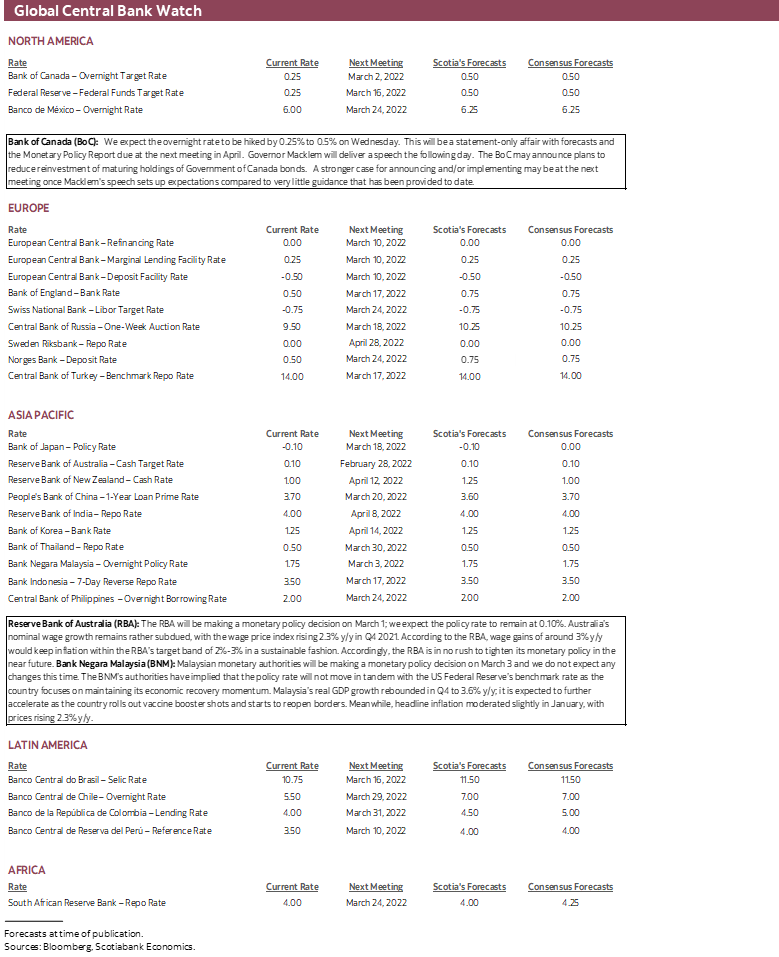

FEDERAL RESERVE: POWELL TO WEIGH IN

So far, there is rather little reason to become incrementally concerned about the risks to US growth. The direct trade exposures to Russia are tiny. Equities have largely shaken off the invasion so far. The bond market impact has been rather small to date. The USD has been range bound since November. Oil has had little reaction thus far to the war but has sharply risen since December.

The growth effects of this oil shock on net are probably fairly manageable. The US net oil importer status has sharply fallen over the past 10+ years. The peak was over the mid-2000s in the lead up to the GFC. At the margin, it’s doubtful that the Fed will be terribly fussed by the net growth effects of higher oil prices on the US economy.

It's more likely to be concerned about another inflationary impulse at the point of maximum employment and full capacity use when it's easier to pass on higher energy and agricultural (including grains) costs through other parts of the basket.

In any event, we’ll see what Chair Powell thinks when he delivers his delayed semi-annual testimony to Congress on Wednesday and Thursday at 10amET both days. His guidance is likely to sound incrementally hawkish given greater inflation risk. Watch for the guidance we didn’t get from the FOMC minutes on size and pace of rate hikes that among other things could inform risk of a 50bps move in March. Also watch for appetite for front-loading hikes along the lines of the preferences of St. Louis President Bullard and Governor Waller, plus potential guidance on balance sheet roll-off plans including caps on the amount of securities allowed to fall off the Fed’s balance sheet and perhaps end-targets for metrics like reserves, the SOMA portfolio and total assets. Governor Waller recently guided that the reserves to GDP ratio should be brought back in line with the 8% mark that existed before the pandemic which is roughly half of the current stock, though he did not inform timing.

PBOC—Yet Another Wrinkle

China's leading net oil importer status has soared over the past decade. The PBOC faces a potentially growth-damaging shock. With slack in its economy, the increased number of downside risks over the past year combined with pre-existing disinflationary pressures, a new relative oil price shock should be more disinflationary on the already-soft core CPI basket. When Xi Jinping suddenly counsels mediation of the conflict, he may be exclusively speaking through the lens of China’s own economic interests.

ECB—On Edge More Than Most

Recent comments from ECB officials are somewhat ambiguous but incrementally a touch more cautious ahead of their March meeting. The net oil importer status of Eurozone economies helps to inform this stance alongside the more obvious point that the conflict is right on its doorstep. Germany is almost as reliant upon imported oil now as it was in years past because, well, it doesn't really have any! Germany’s reliance upon imported natural gas is clear in the context of the original rationale for the Nord Stream pipeline. France's reliance has somewhat diminished over time. On net, a contributing factor to Europe’s tepid response to Russia has been its dependence upon imported oil and particularly Russian imported oil. Furthermore, the ECB's starting point on core CPI inflation (2.3% y/y) is less than half the starting point for US core PCE (~5% y/y) and so there may be less urgency to address the potential for a further inflationary impulse. As for the growth effects, President Lagarde (wisely) cautioned that it’s probably too early to have much to say on it.

Banxico—Upside Risk to Pace

Mexico is clearly a major oil producer and so higher prices can offer an additional positive income shock to the overall economy and with that an added inflationary impulse. As such, higher oil prices could induce an incrementally hawkish central bank. This development arrives after it was revealed that Banxico board member Governor Victoria Rodriguez Ceja was leaning toward a large 75bps rate hike at the February 10th meeting and Deputy Governor Heath had indicated that Banxico is likely to once again hike at the same pace as the Federal Reserve going forward in order to relatively safeguard Mexican capital flows. The combined developments could mean upside risk to the pace of monetary tightening that many expect.

Next up I’ll turn to the central banks facing imminent policy decisions.

BANK OF CANADA—CATCHING UP

Now enter the Bank of Canada’s pending policy decision on Wednesday. There will be no fresh forecasts or Monetary Policy Report until the next meeting in April. This will be a statement-only affair at 10amET followed by Governor Macklem’s Economic Progress Report and press conference the next day at 11:30amET.

We still expect the BoC to take the first steps toward policy tightening at this meeting.

- By hiking the policy rate 25bps as the first move and repeating guidance that a series of moves lies ahead.

- A larger hike is unlikely. Hiking by 50bps is significantly priced, but the BoC doesn’t seem to much care about market pricing after it passed on a nearly fully priced chance to hike at the prior meeting. Hiking by 50bps now may be perceived to be an admission that the BoC messed up the last time and needs to catch up with a bigger hike now. The BoC never tends to admit as much. Furthermore, the BoC has lagged its response to soaring inflation and emphasizes acting in measured, gradual steps that may continue to lag behind inflation risk. Hiking 50bps (or more) would not help the impression that its guidance and messaging is unreliable.

- It’s possible that the BoC will announce that it is stepping away from reinvestment plans, but it may intimate a bias toward doing so that will be implemented at the April meeting. Deputy Governor Lane somewhat awkwardly put it this way: “We’re going to certainly consider starting that process [ed. winding down reinvestment] fairly... We’ll be doing that as soon as we’re starting to raise rates. Quite likely we’ll be saying something about that in a couple weeks time when we’re actually at the stage of changing our, uhh... When we’re actually at our next decision point.”

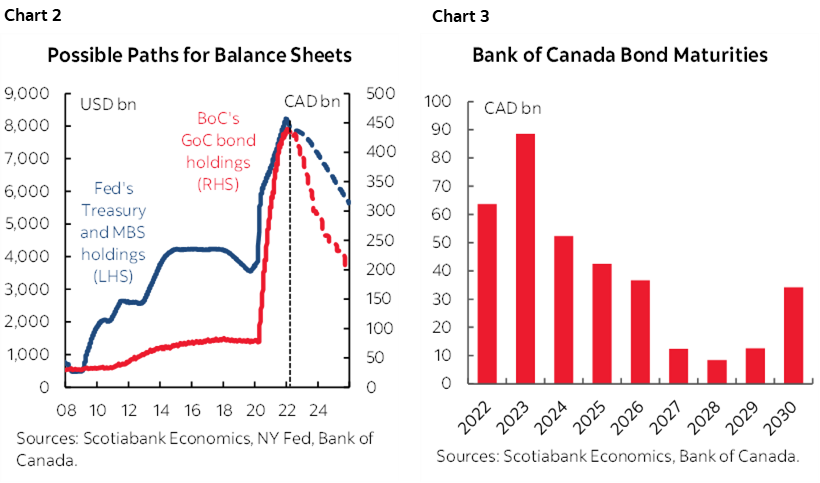

As for reinvestment plans, we haven’t heard any concrete guidance beyond feasible start dates which also counsels setting up such a move perhaps to be elaborated upon in Macklem’s ensuing speech rather than springing it on markets. One scenario I still like is shown in chart 2 and compares to a plausible scenario for the Fed’s path. It assumes that the BoC lowers the gross bond purchase amounts from C$4–5B per month by $1–2B at each MPR meeting starting in April and thus shutting down reinvestment perhaps by the following January or April MPR meetings. The implied roll-off caps would rise toward $4–5B/mth over this period after which the pace of reduction would be driven by the maturity schedule as shown in chart 3 at present.

I would expect Governor Macklem to say that asset sales are not under active consideration at this time. Overall, the more measured, plodding and lagging pace of policy tightening by the BoC is unlikely to emulate the more aggressive stance of the RBNZ that recently went cold turkey in ending reinvestment and embracing managed asset sales.

As for the incremental impact of recent developments on the BoC’s outlook, a deeper discussion on this is likely to be deferred to the April meeting when fresh forecasts are due. That gives the benefit of evaluating further developments.

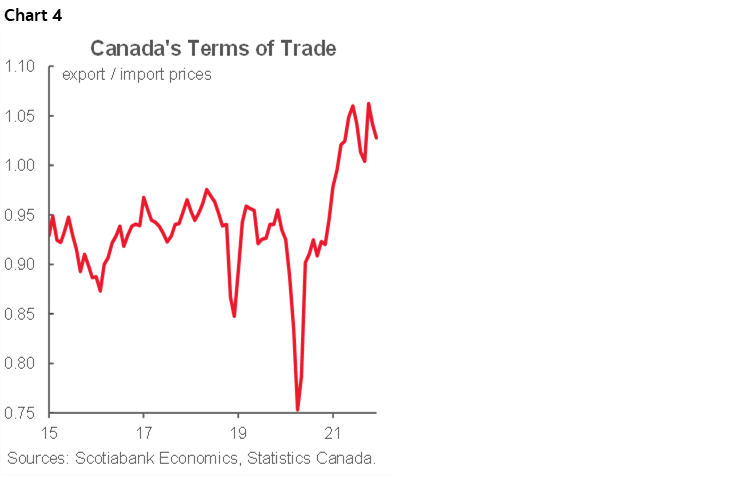

Still, Canada's status as a net oil exporter means Canada is importing an inflationary shock at an unsuitable point in the cycle. Canada is getting a terms of trade (export to import prices) lift through higher oil prices that has not yet fully shown up in lagging trade prices (chart 4). That means trickle-down benefits through government finances, corporate profits in aggregate, and household incomes. That in turn can benefit the real economy through positive revenue windfalls and higher spending across broad sectors. This is occurring at the point of full employment and capacity limits. I don't believe that the BoC will turn dovish here... they'll have a cautious eye on geopolitical risk while noting the limited trade/investment ties with the region. They'll observe the limited impact on the TSX that has basically moved largely sideways since October. They'll observe higher oil and weaker CAD. But the way they have played oil and such drivers in the past is by turning dovish when it plunges (like early 2015 rate cuts) and more constructive or incrementally hawkish when it climbs.

THE RBA & OIL

The Reserve Bank of Australia steps up to the plate on Monday (ET). The major move came at the last meeting on January 31st when the RBA ended its QE bond buying program as expected. It may be likely to repeat the same forward rate guidance this time—if not strengthen it in light of Australia’s status as a net oil importer facing the spike in oil prices over the past three months.

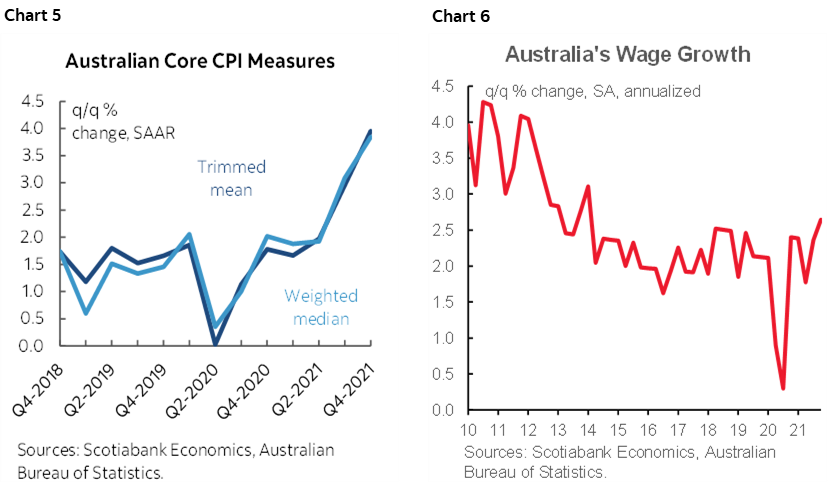

Recall that at the prior meeting, the RBA said in relation to rising inflation that “it is too early to conclude that it is sustainably within the target band” and “there are uncertainties about how persistent the pick-up in inflation will be as supply-side problems are resolved” while concluding “The Board is prepared to be patient…” which was a repeat of the prior month. They might repeat that line. The RBA has already transitioned away from calendar-based guidance for when it thinks inflation will be sustainably on target and rate hikes are a possibility but is buying time to evaluate more data, more developments, and more moves across its peer set of global central banks. Chart 5 shows the trend in Australian inflation with chart 6 showing that nominal wage growth measured the same way at the margin (q/q SAAR) is not keeping up. At issue may be the balance the RBA strikes between higher oil’s damaging growth effects versus inflationary effects.

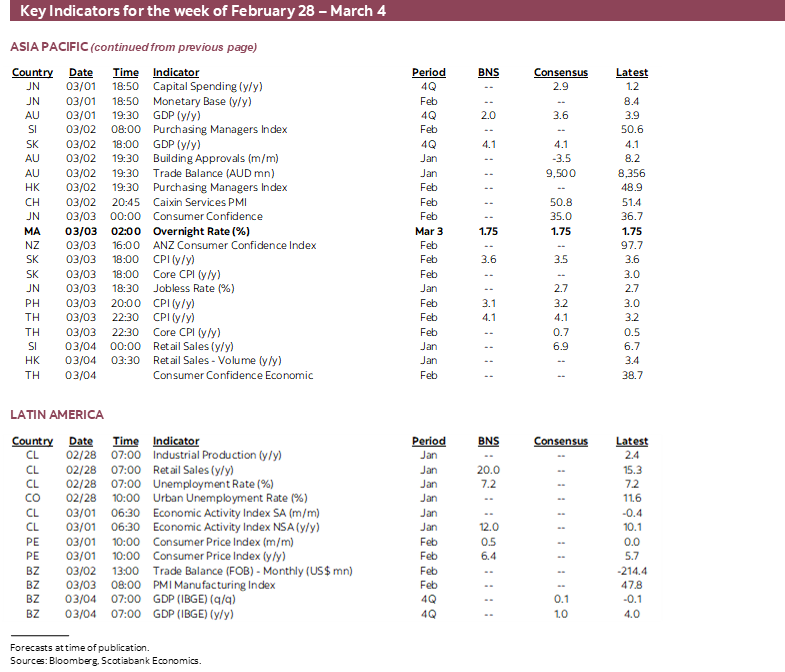

Bank Negara Malaysia also delivers a policy decision on Thursday morning (ET) and is expected to remain on hold with the overnight policy rate at 1.75%.

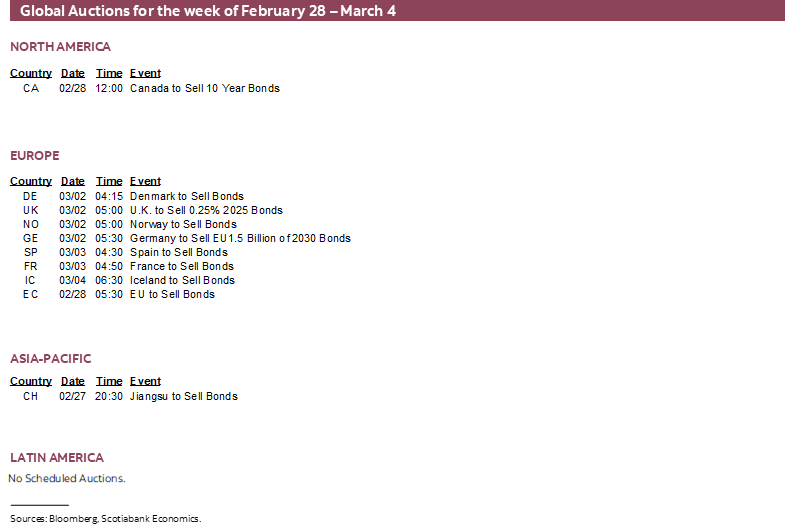

OPEC MEETING: ROOM TO RAISE, IRAN IN THE BALANCE

This could be a raucous one. OPEC+ meets virtually on Wednesday amid speculation toward increased pressure upon members to raise production targets given accelerating oil prices. Momentum has been in place since December when oil prices started to accelerate. Since then, WTI has risen by about US$30/barrel with only a fraction of that resulting from Russia’s invasion of Ukraine.

Efforts by the US and others to release strategic oil reserves as a way of dampening oil prices are as unlikely to sustainably work as in the past when this approach has been tried. That shifts the focus to behind-the-scenes arm twisting that likely has the US and others applying pressure upon the Saudis to increase output as the biggest producer with the ability to do so. With little else going for it, Russia needs high oil prices to fund its invasion and to help mitigate the bite from sanctions and so it may protest a bigger than likely planned rise that is expected to add about an extra 400,000 barrels per day to overall OPEC+ output starting in April. If that’s all that is delivered, then it’s probably already fully priced in oil markets. Key is whether agreement can be reached or whether the Saudis and perhaps a few others need to go it alone if there is added pressure to raise production.

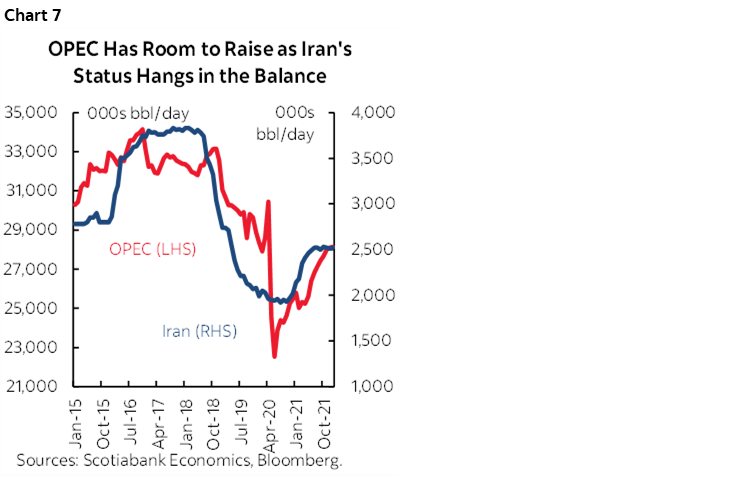

Hanging in the balance is the state of negotiations around resurrecting some form of the Iran nuclear accord that could bring back Iranian production. At stake could be the gap between Iran’s current production of about 2.52 million bpd versus 3.8 million bpd just before the previous US administration tore up the agreement. High oil prices and inflationary consequences may add a particular form of expediency to the talks. In the face of rising demand, OPEC+ output still remains well below pre-pandemic levels as multiple economies are experiencing advanced stages of a full recovery or are getting close to doing so (chart 7). OPEC+ restrictions are therefore at least partly responsible for high oil prices and high gas prices at the pump.

US PAYROLLS HEADLINE GLOBAL INDICATORS

This will also be a week full of significant market risk surrounding major global releases. Key ones to watch for are highlighted below.

1. Nonfarm payrolls

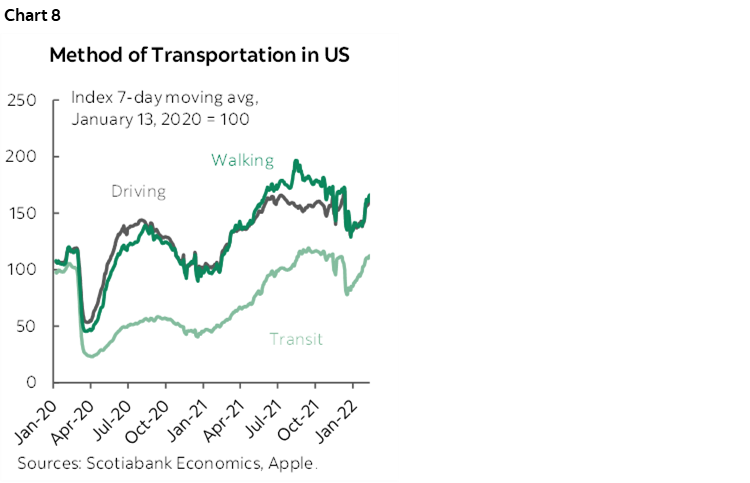

This is usually the world’s pre-eminent macroeconomic report, though some may say it’s a close contest with inflation readings especially these days. February’s nonfarm payrolls land on Friday as the last set of employment and wage figures before the March 15th–16th FOMC meeting. An estimated 400,000 jobs are thought to have been gained in February and the unemployment rate is estimated to have declined by a tenth to 3.9%. One of the indicators we follow is the improvement in mobility readings (chart 8). The Fed’s focus is more upon inflation than the full employment side of its dual mandate at this point and so it would take a really big surprise for this to matter on the path to the next FOMC meeting a couple of weeks later.

2. Canadian GDP

While Statistics Canada had guided that GDP was roughly unchanged in December, the balance of risks might turn moderately negative when the release arrives on Tuesday. Retail sales contracted and the preliminary GDP estimate may have further weakened as more data capturing developments later in the month unfolded. Still, a strong overall quarter is anticipated with growth expected to land at 6½% q/q at a seasonally adjusted and annualized rate. What may be more important is advance guidance on January GDP which is rather likely to be a sour reading given COVID-19 restrictions and already known readings like the ~200k drop in jobs.

3. US ISM PMIs

Little change is expected in the ISM report on manufacturing conditions during February (Tuesday). Regional surveys were somewhat mixed although the Markit PMI gauge moved higher which may be either due to international conditions not included in ISM gauges or domestic conditions. ISM-services are where the greater hope lies (Thursday) in that we could see more of a rise as omicron fades. Other US releases will include expected softening in construction spending (Tuesday) and vehicle sales (Tuesday).

4. Inflation readings

A number of regions and countries will update inflation readings for the month of February over the coming week. At the top of the list will be the Eurozone’s estimate on Wednesday that is expected to accelerate toward 5 ½% y/y after a gain of ½% m/m or so. Core Eurozone inflation is also expected to pick up toward 2½% y/y. Germany will update CPI on Tuesday along with Italy after Spain refreshes on Monday and following the already known stronger-than-expected reading from France.

CPI updates will also arrive in Peru (Tuesday), Indonesia (Monday night), Philippines (Thursday night), South Korea (Thursday night) and Thailand (Thursday night).

5. China PMIs

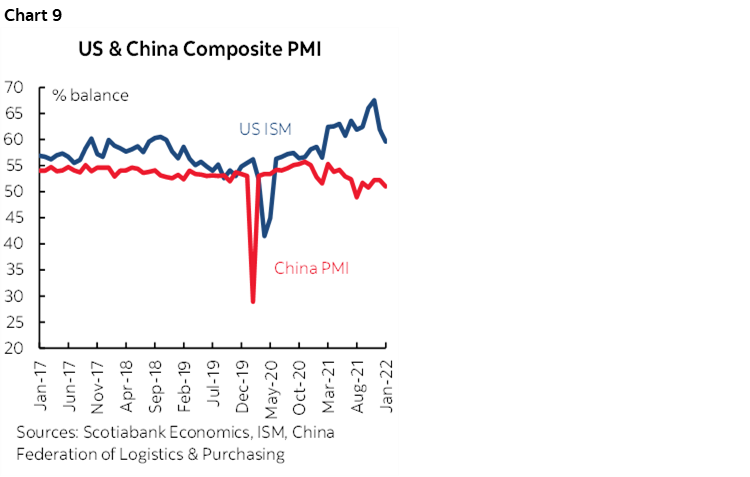

China updates the state’s version of purchasing managers’ indices on Monday night (ET). These readings have been indicating that the economy is at roughly stall speed versus the US economy’s stronger momentum (chart 9). Private PMIs are due on Monday and Wednesday night and are relatively more skewed toward smaller producers than SOEs and relatively more toward exporting companies.

6. Canadian bank earnings

Even though half of the banks have released and set much of the tone with a series of beats, you didn’t think I could leave out my own employer did you? BNS releases on Tuesday (consensus EPS C$2.04) and so does BMO (consensus $3.29). Laurentian Bank releases Wednesday ($1.20) followed by TD Bank on Thursday (C$2.04).

Miscellaneous additional reports I’ll write more about in regular daily publications will include GDP figures from Australia, India, South Korea, Brazil, Sweden and Switzerland plus Japan’s monthly data dump and retail sales figures from Germany and Australia. Alas, these fingers are worn out for now!

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.