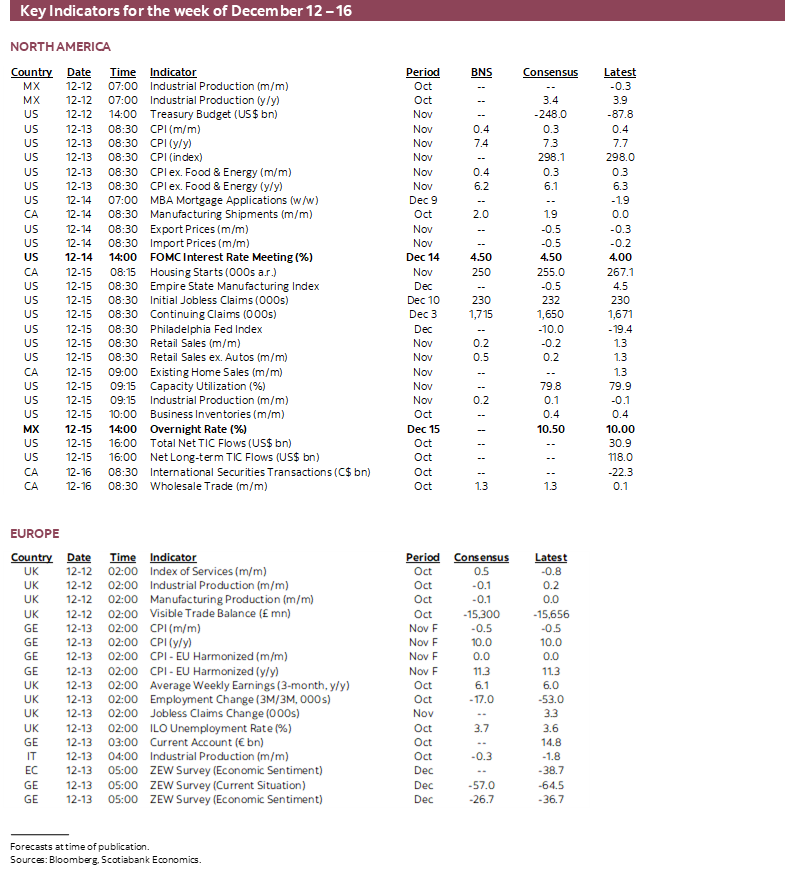

Next Week's Risk Dashboard

- Monepalooza week!

- The 3 worse alternatives to fighting inflation

- FOMC tail risks to a pre-set script

- US CPI expectations

- The ECB’s QT challenge

- BoE likely to downshift

- PBoC unlikely to deliver cuts

- BoC’s Macklem to keep door the open

- SNB to follow the ECB

- Norges Bank to sound more cautious

- BanRep to deliver mega-hike

- Banxico expected to follow the Fed and inflation

- BSP likely to hike again

- CBCT has a little more wiggle room

- Is Russia done cutting?

- PMIs: EZ, UK, US (S&P), Japan, Australia

- Other macro

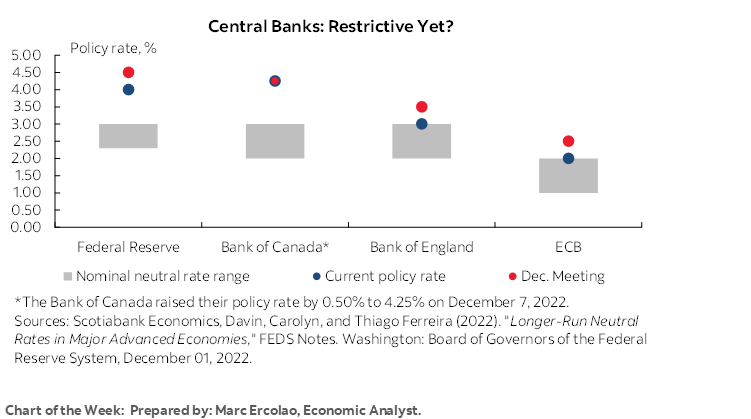

Chart of the Week

As the holiday season beckons across their markets, just about every major central bank is in a rush to jam in their latest decisions and guidance before setting their out of office messages. Of course, that’s a bit of an exaggeration in today’s workforce that never disconnects. No less than ten tier one and regional central banks will weigh in. That will leave only one notable central bank left to opine before the end of the calendar year—the BoJ.

All of them are getting more heat for the increasingly binding effects of tighter policy. They drew deserved praise for their early responses to the pandemic followed by justified criticism for misreading real time evidence of building inflationary pressures and waiting too long to tighten policy. Hiking when they eventually did so this year occurred in most but not all markets within the context of a strong economy and job market and so they looked like the lagging cavalry. They have now entered perhaps the most difficult circumstances of all as the costs of their actions become more apparent. 2023 is likely to escalate the criticism as recessions become more probable.

Unfortunately, the alternative ways of addressing inflation are even more unappealing. I have more faith in the ability of central banks getting their second chance to get inflation under control and being left to do their jobs than the alternative proposals that as near as I can tell fall into three main camps that need to be confronted.

1. Benign Neglect

First is what I call the benign neglect approach while treating the surge in inflation as transitory. If so, then central banks should have perhaps looked through the surge and accommodated it with their fingers firmly crossed. Toes too.

This approach would be a high stakes gamble. In fact, it describes how we got here in the first place as central banks ignored the real time evidence on rising inflation until late in the game. To have continued to do it would have counted upon many people believing that inflation is transitory and hence not changing their behaviour in such fashion as to permanently entrench high inflation in the economy. We’ve already had escalating inflation dating back to late 2020 and expect it to continue into 2023. Not having taken steps to curtail this inflation would have escalated the risk that it never goes away.

This look-the-other-way approach also discounts what I think are more structural and longer-lived drivers of inflation. Supply chains are at a nascent stage of fundamental upheaval that will last for years and in my opinion some of the higher cost consequences are likely to be passed onto consumers for a long time yet.

2. Add Stimulus

Huh? Oh no, I am serious. Yes, you read that right. There are folks who think that applying more stimulus would lower inflation.

How so? People who criticize central banks for raising the cost of borrowing are by corollary revealing a preference for cutting rates. This is often coming from people who also prefer higher government spending to assist people with high inflation.

There is one policy maker in the world who has embraced this approach and he is ruining Turkey’s economy. Let’s just say that nowhere in the time spent studying toward three university degrees in economics and finance plus a professional CFA designation and almost three decades experience as a professional practicing economist have I ever encountered evidence that supports the contention that the best solution to high inflation is to go back to offering practically free loans and giving people more money to spend. That’s just nutsonomics. And you don’t need to be an economist to get that. It’s just common sense.

3. Price Controls

Another alternative is to dredge up price controls such as some variant of the disastrous Canadian Anti-Inflation Act of 1975 that former PM Pierre Trudeau introduced. That prior act was repealed four years later. It didn’t work then and the world has changed a great deal since such that it would be even less likely to work now. This camp sees corporate greed as the dominant driver of inflation and wishes to tell businesses what prices to set. Here are some problems with this old idea.

- At what levels would thousands and thousands of prices be set? Bureaucrats with no experience in business don't have better information on appropriate prices than the businesses themselves.

- Many prices lack transparency. To be effective, you'd have to monitor actual prices in order to be able to enforce them.

- The enforcement costs would be ginormous. Think thousands or hundreds of thousands of price police paid for by your taxes poking their noses into businesses on a high frequency basis. You’d need a new Ministry of the Thoroughly Unenforceable.

- Businesses would have incentives to circumvent price controls. Small business could resort to bartering. Black market activity would probably rise.

- Organized crime could flourish in an effort to capture the difference between regulated prices and black-market prices.

- Setting the price for a product below soaring production costs or limiting the rate of growth in selling prices below the rate of growth in input costs would discourage growth at those businesses and with that investment and job creation.

- For similar reasons, widespread product shortages would probably arise.

- Various product features could be changed if prices are dictated to businesses.

- Businesses could restrict supply at dictated prices, or restrict access only to their best customers.

- Many more businesses could charge membership fees to anyone who wants to buy from them.

- Businesses could offer basic options that meet price controls and then charge additional fees to get the kind of product that people demand. This would introduce more complex tiered pricing. Want a smartphone? You’ll have to pay extra for the screen.

- Some businesses may just pay the fine for charging higher prices and pass that on too!

- Access to some products could move out of jurisdiction. Like an e-commerce site that can serve Canadians but beyond the reach of the price controls.

- There could be negative implications for credit availability as lenders reassess attractiveness of lending to affected businesses.

- If price levels are set below soaring input costs or allowed to rise at a slower rate than input costs then you wouldn't be as inclined to invest and hire. Shortages would be more acute. Inflation would move outside of official statistics.

- For the BoC, the 2% inflation target would be harder to assess. Price controls could sow confusion and require new measures excluding sectors or products perhaps not subject to such controls.

- Controls could drive investment and jobs to other jurisdictions that don’t have them. This is a particularly high risk for smaller to mid-sized economies.

- Price controls could interfere with price discovery and the efficient allocation of capital in the economy to areas where profit incentives are greatest. Sectors with abnormally high returns should attract investment and greater market participation and thus expand the supply side at a time when damaged global supply chains are among the drivers of inflation. I don’t see how damaging supply chains through regulated prices would help ease such concerns.

- Businesses would aggressively lobby for favourable price levels and controls. Think higher regulatory costs and hence waste. That’s just what businesses need to deal with into a recession.

- There could be a multitude of legal challenges that would tie up the courts.

- Price controls set by size of business in order to perhaps lower the administrative and enforcement costs by targeting fewer of them would give artificial and discriminatory advantages to some firms over others and probably wouldn’t exactly help Canada’s productivity problems! It would create artificial incentives to unbundle businesses with smaller average sizes in order to evade controls.

- Price controls could harm a country’s reputation in world markets.

- Telling businesses what price to charge is rather tone deaf in our times when apparently folks don’t like being mandated to do other things even when it may be in their best interests to do so, let alone when that’s not the case. Widespread shortages and government decrees on setting prices could invoke further mass protests.

With that, let’s get onto more serious ways of addressing the problem.

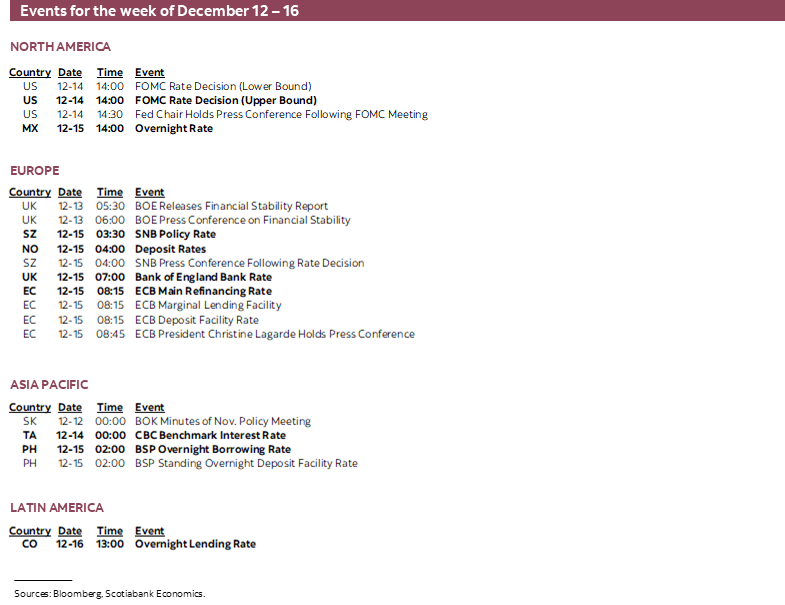

FOMC—TAIL RISKS TO THE PRE-SET SCRIPT

Wednesday’s FOMC meeting will be the full deal in terms of the range of communications on offer. The statement lands at 2pmET along with a refreshed Summary of Economic Projections including a revised ‘dot plot’. There will be the customary press conference starting at 2pmET and to be hosted by Chair Powell for about an hour.

The Fed has set much of the script. There are three main expectations.

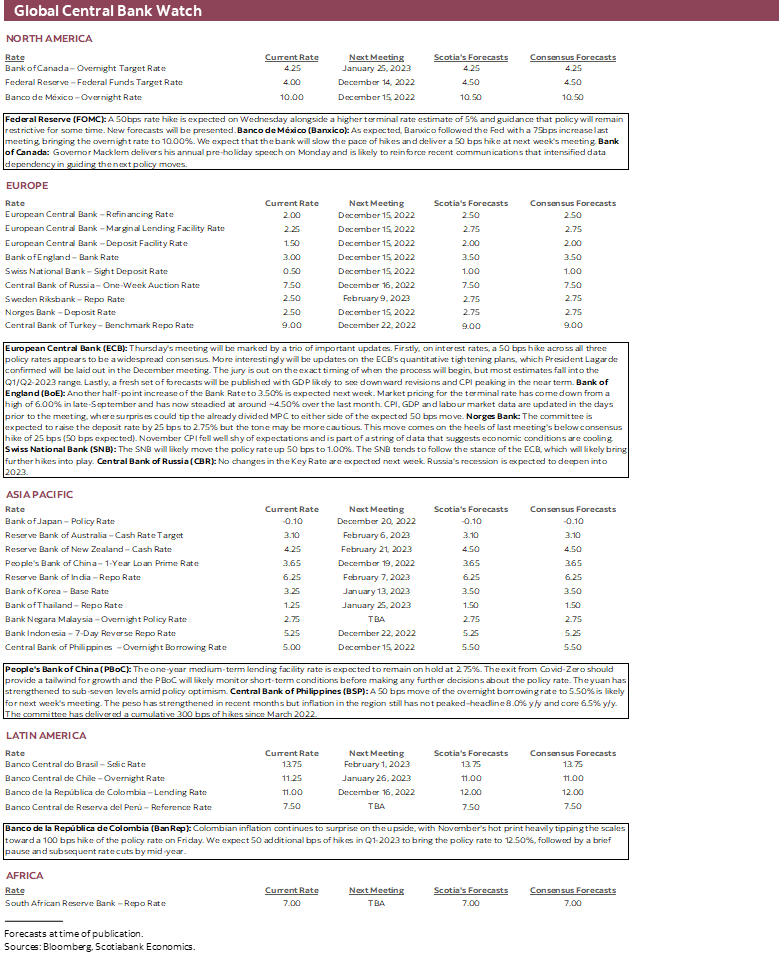

First is that a 50bps rate hike is priced by markets and universally expected by economists. There is very low risk of a surprise given the emphasis Chair Powell places on avoiding game day surprises to this measure. Chair Powell guided at the last press conference in November that “the time is coming and it may come as soon as the next meeting or the one after it” to downshift the pace of rate hikes. The subsequent minutes to that meeting that were published on November 23rd stated that “a substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate.” That strengthened the time reference to this coming meeting given the Fed’s tendency to use “soon” as a guide to something fairly imminent and the fact that Fed officials have not leaned against the market’s interpretation.

Second, there is a bit more uncertainty around the path for the policy rate into 2023 and beyond. The prior projections in September estimated that the fed funds upper limit rate would rise to 4.75% in 2023.

"Even so, various participants noted that, with inflation showing little sign thus far of abating, and with supply and demand imbalances in the economy persisting, their assessment of the ultimate level of the federal funds rate that would be necessary to achieve the Committee’s goals was somewhat higher than they had previously expected."

Chair Powell’s speech on November 30th (here) reinforced this remark that the terminal rate could move “somewhat higher.” So what does “somewhat” mean? We’re guessing that the median vote will move up by 25bps to a terminal rate of 5% and probably with a dispersion of dots to either side of that. How many dots land above 5% may be impactful to markets that are priced for a 5% peak. Any guidance above that would be a hawkish surprise.

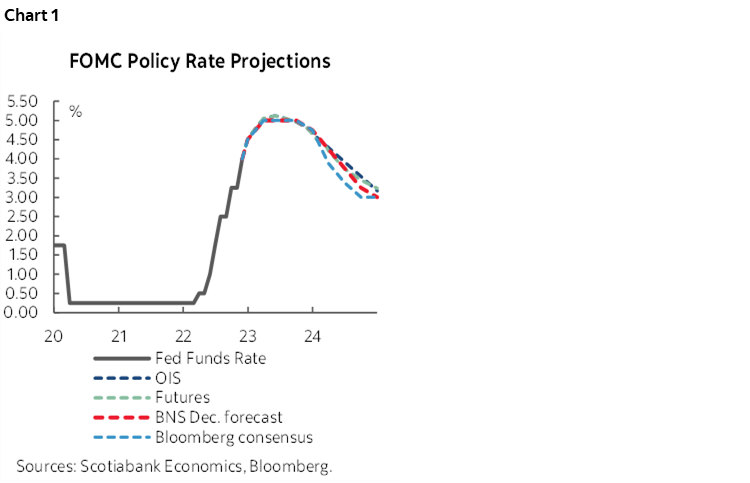

Third is pause and cut guidance. Powell’s speech only said that policy will be restrictive “for some time.” Maybe I should try that language the next time the household job jar gets pulled out – I’ll get to it “some time”. If I’m not at work the next day, well, then you’ll have an idea why. The last Rorschach plot (e.g. July’s dots formed a series of up arrows for each year…) suggested that the FOMC would not cut until 2024 when it would ease by 75bps and then another full percentage point in 2025. That’s less aggressive than our forecast pace of easing shown in chart 1 and compared to market pricing and consensus. I think the FOMC is likely to continue to lean against signalling easing in 2023 but with a repeat of the wide dispersion in dots during 2024.

There are really two issues to consider here though. One is that being “restrictive” is compatible with rate cuts since a 5% or so terminal rate is well above the estimated 2½% neutral rate. They could conceivably ease by quite a bit next year and still be restrictive. Second is defining “some time” which is unclear. I don’t think Powell will go to any great lengths to define this because they frankly don’t know and everyone else is largely guessing.

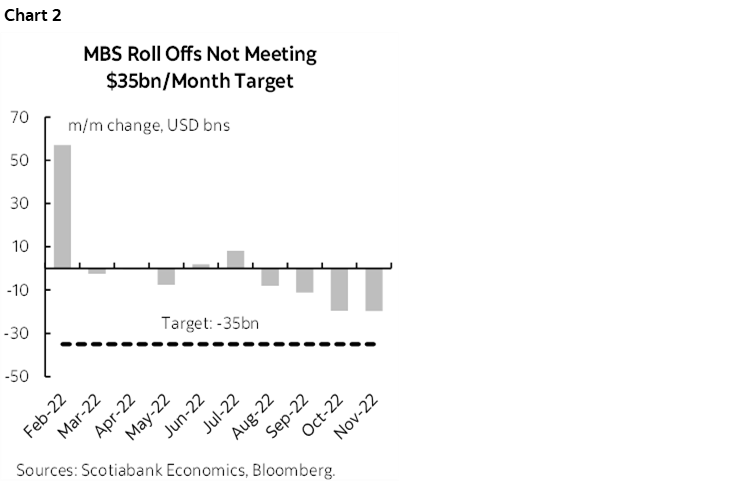

Fourth, the pace at which the MBS part of the Fed’s SOMA portfolio is shrinking is less than the initially targeted US$35 billion per month. Bond market developments that have affected mortgage rates and prepayment risk have been the reasons for a slower pace of MBS roll off for several months now (chart 2). When Chair Powell was asked at the September press conference about actively selling MBS he flatly replied with how this was “not something we’re considering right now or that I expect to consider in the near-term.” Fast forward three months and with more evidence that the MBS part of the SOMA portfolio is not shrinking as rapidly and he may be asked again. He’s likely to offer a similar answer at this point but it remains a policy option in 2023.

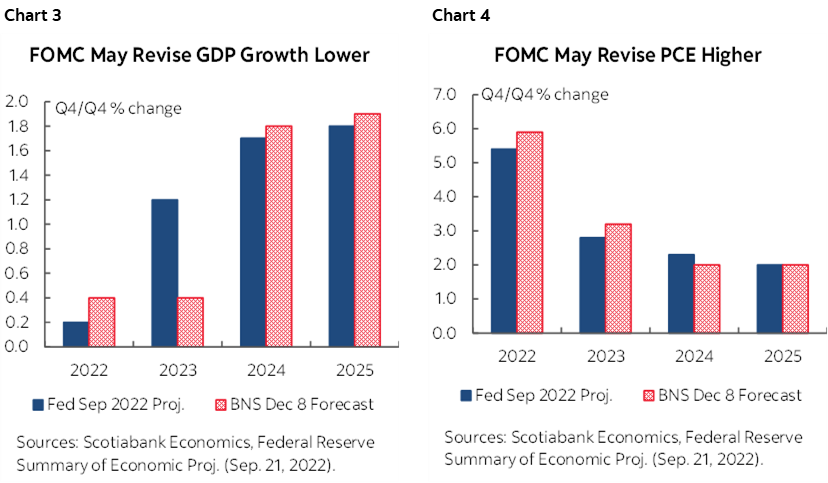

Fifth is the issue of forecast revisions. Our forecasts for GDP growth and PCE inflation on the same Q4/Q4 basis used by the FOMC point to the possibility that the committee may downwardly revise 2023 growth and upwardly revised 2023 inflation (charts 3, 4). There will probably be similar discussion around a narrowing path to a soft landing and a higher unemployment rate projection.

BoC—MACKLEM LIKELY TO REINFORCE DATA DEPENDENCY

Bank of Canada Governor Tiff Macklem delivers the Governor’s annual holiday speech on Monday. It is billed as a speech followed by audience Q&A and a fireside chat. Speech headlines land at 3:25pmET and there will be a press conference at 5pmET.

The Governor is likely to reinforce recent communications. The recent policy statement hawkishly surprised markets with a 50bps hike when something closer to 25bps was priced and by leaving the door open to further hikes (recap here). The next day’s remarks by Deputy Governor Kozicki emphasized that the statement was not about communicating the end of hikes or a pause. Instead, the message they intended to deliver was to signal very high data dependency toward next steps. She also guided that becoming more “forceful”—code language for bigger than 25bps hikes—would require a significant inflationary shock. Former Governor Dodge back up the data dependency interpretation. That has markets cautiously keeping the door partially open to another 25bps hike into Q1 which I think is prudent at this stage. Now we are left monitoring data and developments over the next seven weeks on the path to the January 25th decision including full forecast updates.

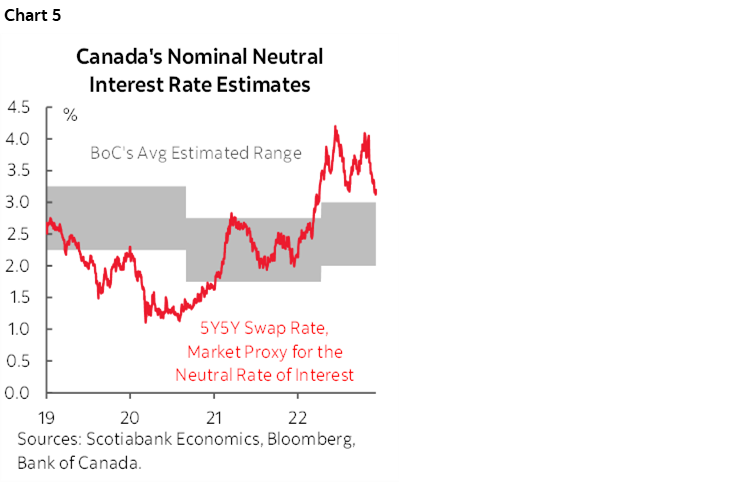

Regardless, the BoC is still likely in the finetuning stage of tightening monetary policy for now and shifting toward monitoring the forward looking and lagging effects. Its policy rate of 4.25% is presently well into restrictive territory according to estimates of the neutral policy rate (chart 5). It is also under rising pressure from political activists.

ECB—ROLL ’EM!

Thursday’s policy decisions by the European Central Bank will offer a full suite of updated communications starting with the statement at 8:15amET and followed by President Lagarde’s press conference 30 minutes later.

A 50bps hike to all interest rates is widely anticipated across consensus and is where market pricing is leaning. This would be downshifting the pace compared to the prior two back-to-back 75bps hikes. Even the typically hawkish Bundesbank has President Nagel saying that a half point hike “constituted just as much of a strong step as seventy-five basis points.”

Markets are largely priced for most of another 50bps hike at the next February 2nd meeting and a terminal rate of up to 3% by Spring. Guidance provided by President Lagarde in her press conference may be impactful.

Much of the focus, however, will be upon plans to unwind the Asset Purchase Program and hence begin exiting from the bond market upon entering the Quantitative Tightening phase. Lagarde reaffirmed on November 28th that “key principles” guiding such intentions would be presented at this meeting. That sounds short of offering all details that may be deferred until the new year.

At issue are two considerations. First, when would the ECB start to implement the unwinding of its bonds held in the APP. There exists a variety of opinions across the Governing Council with some leaning to very soon and some learning toward starting several months later. It may be difficult to achieve consensus, but we’ll be looking for language referencing something like “in the coming quarter” which would be consistent with how the ECB has communicated in the past.

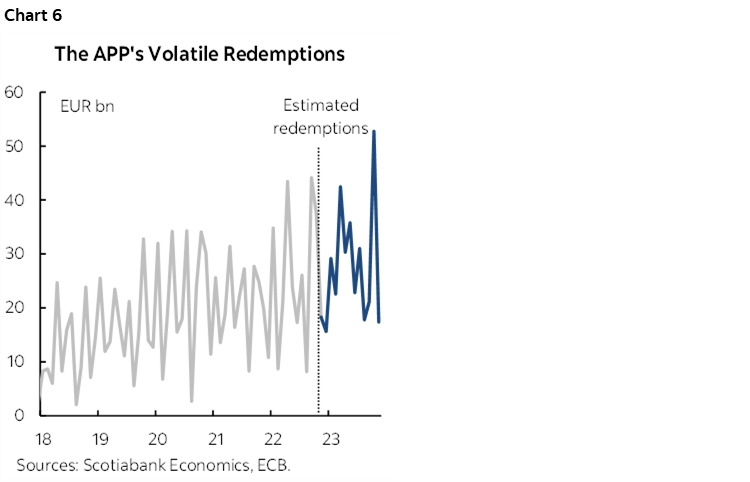

Second, exactly how will the APP be unwound? The ECB probably lacks the confidence in the outlook necessary to trigger outright bond sales at this stage. That leaves us with how much of the expected redemption schedule will be allowed to drop off the balance sheet. Chart 6 shows the historical and expected monthly pace of APP bond redemptions. On average about €29 billion in redemptions will occur each month in 2023 but the volatility that runs between about €17–53 billion per month immediately flags one caution. If they suggest they will allow whatever the amount of redemptions to drop off the balance sheet each month then this could make for whippy influences upon markets. If, however, they pre-commit to a €30 billion target each month then that could undershoot or overshoot monthly redemptions by large and volatile amounts. It might also be too fast since such a target would amount to averaging at a 100% pace of roll-off kind of like the approach adopted by the Bank of Canada.

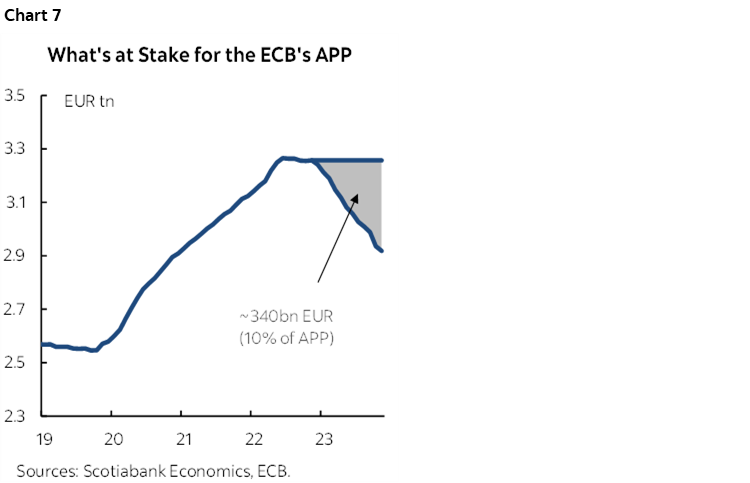

So one approach could be to set a target below €30 billion with estimates all over the map. A perhaps more likely approach would be to set targets one quarter at a time and allow for flexibility as circumstances evolve. Chart 7 shows the range of possible implications for the size of the APP portfolio and shows the difference between continued reinvestment of flows versus full unwinding over 2023.

There will also be forecast revisions that are likely to revise inflation higher and that could also inform market pricing for the policy rate peak and the period during which policy is likely to be restrictive.

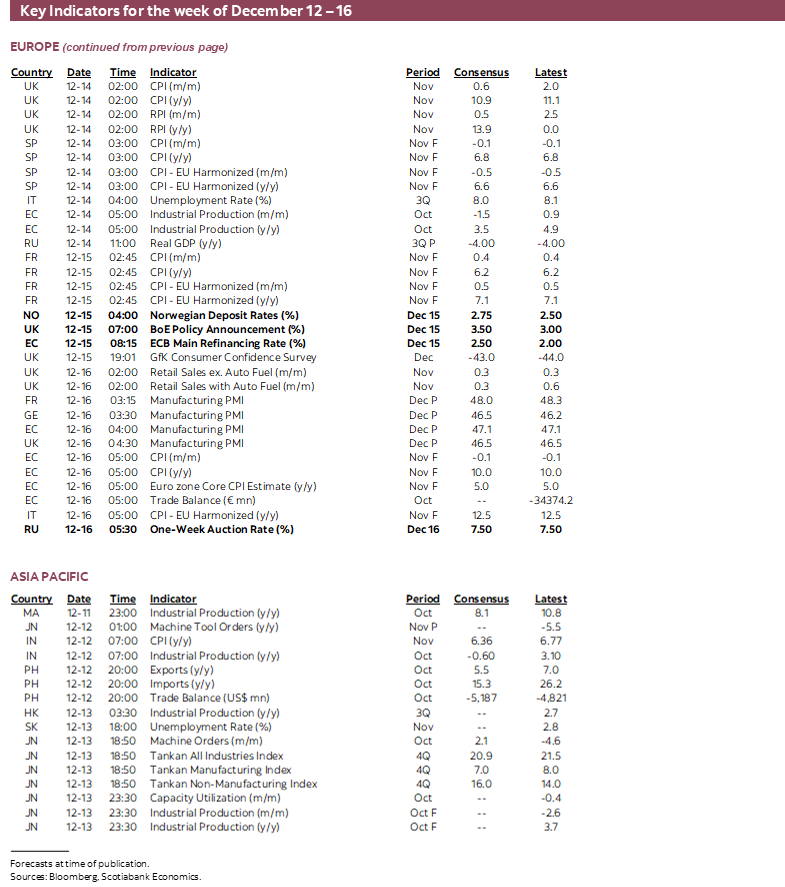

BANK OF ENGLAND—TIME TO DOWNSHIFT?

The Bank of England weighs in on Thursday. The decision and statement arrives at 7amET followed by Governor Bailey’s press conference.

Consensus unanimously expects a slower pace of hiking to arrive at this meeting with a 50bps increase that would lift Bank Rate to 3%. Markets are priced for such an outcome. The broad tone of recent comments by MPC members leans toward downshifting but not unanimously so.

On the more hawkish end of the spectrum are several members. Catherine Mann recently emphasized the importance of managing inflation expectations and the need “to be a little bit more aggressive in the near term.” Deputy Governor Ramsden said “however challenging the short term consequences….the MPC must take the necessary steps” in order to achieve the 2% inflation target. MPC member Haskel stated it is important “to stand firm against the risk of persistent inflationary pressure.”

On the somewhat more dovish end are the recession worries of MPC member Dhingra and MPC member Tenreyro who has emphasized that policy is “already in restrictive territory” ahead of the last meeting in November when they hiked by 75bps.

There is the chance that a round of macro reports in the lead up to Thursday’s decision could prove to be impactful. November CPI will be updated on Wednesday and while the year-over-year rate may ebb a touch, it is expected to follow up the 2% m/m spike in October with another somewhat stronger than seasonally normal gain. Industrial output could slip on Monday while services could rebound from the prior month’s contraction. Job market updates for November (claims and payrolls) and October (total employment and wages) arrive the next day. Retail sales will be updated the day after the BoE.

PBOC—NO SHOCK AND AWE COMING

No change is expected to the 1-year Medium-Term Lending Facility Rate of 2.75% on Thursday. That would probably mean no change in the following week’s 1-year and 5-year Loan Prime Rates of 3.65% and 4.3% respectively.

Chinese inflation cooled in line with expectations last month with headline CPI inflation easing to 1.6% y/y from 2.1%. Core inflation held unchanged at 0.6% for a third straight month. That was followed by further jawboning about offering additional stimulus. This is probably best interpreted to mean continued emphasis upon easing Covid Zero practices while monitoring the state’s tolerance toward potential infections, while easing some macroprudential rules and offering targeted stimulus. It’s unlikely that shock-and-awe stimulus will be forthcoming even after the Federal Reserve attains its peak policy rate given the implications for China’s currency, capital account and financial instability.

SWISS NATIONAL BANK—ALSO DOWNSHIFTING?

The SNB is widely expected to hike its policy rate by 50bps to 1% on Thursday which would also downshift from the 75bps hike at the last meeting in September and generally follow the ECB.

NORGES BANK—MORE CAUTIOUS

Norges had already downshifted the pace of rate increases at its last December on November 3rd when it hiked by 25bps versus expectations for double that. The tone this time around is likely to be more cautious and a hike may not be assured on Thursday. Inflation fell shy of expectations in November at -0.2% m/m (+0.3% consensus). Weakness was broadly based across categories.

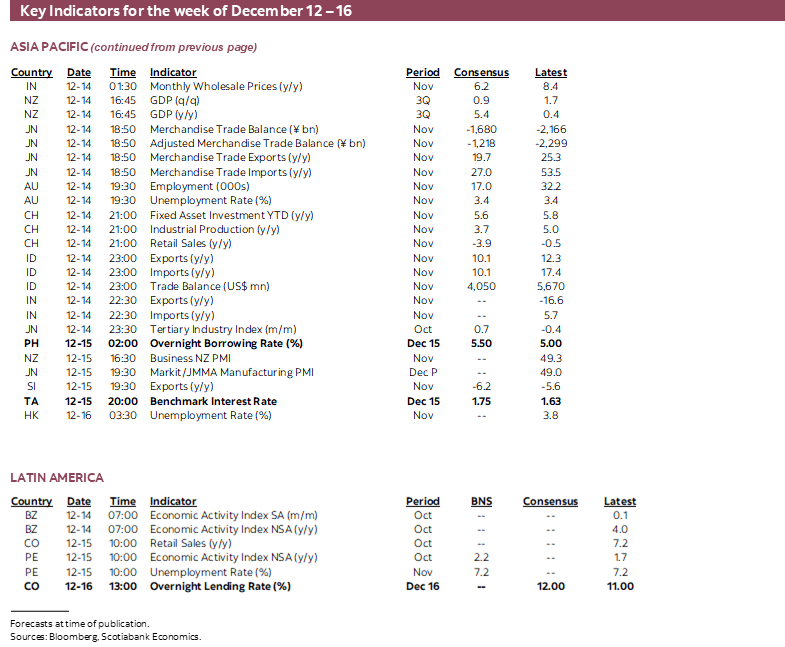

BANREP—HOT INFLATION TO DRIVE BIGGER HIKE

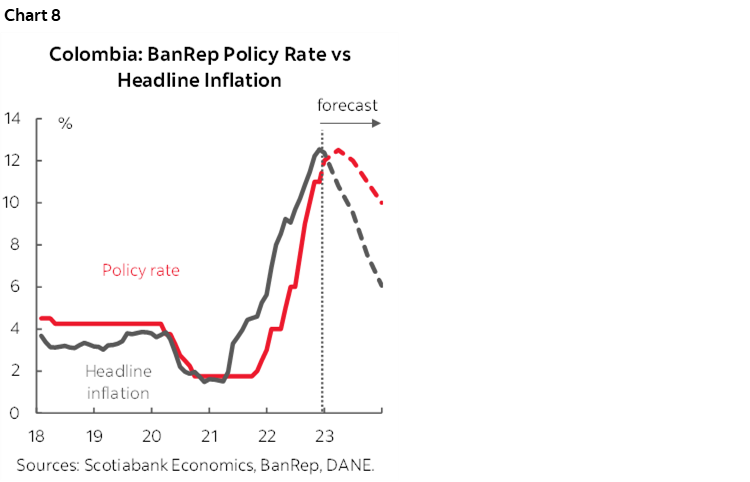

Colombia’s central bank is widely expected to hike its overnight lending rate by 100bps on Friday. November’s hotter than expected inflation reading reinforces a tightening bias with prices up 0.8% m/m and CPI running at 12½% y/y. Chart 8 shows our projected paths for Colombia inflation and the policy rate.

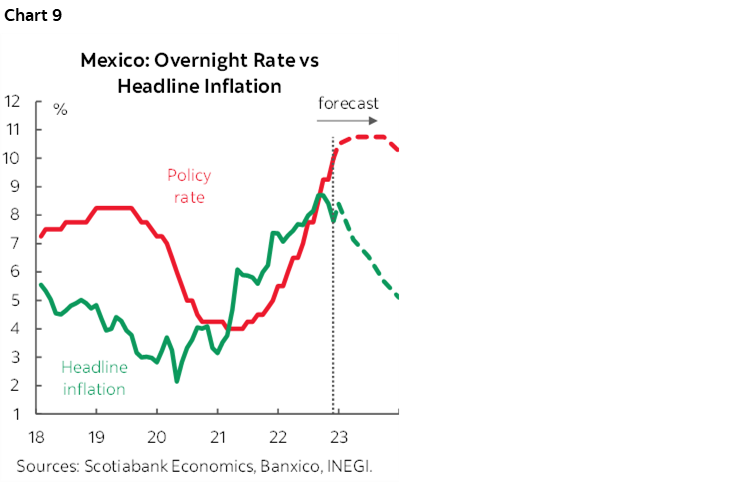

BANXICO—DRIVEN HIGHER BY THE FED AND INFLATION

Mexico’s central bank is widely expected to hike its overnight rate by 50bps to 10% on Thursday and continue to follow the Federal Reserve’s expected moves. November’s inflation figures continued to support policy tightening with CPI up 0.6% m/m and core CPI up by ½% m/m.

Implied market pricing suggests that as the Federal Reserve’s policy rate peaks, so will Banxico’s at between 50–75bps higher after this week’s hike into the new year. Chart 9 shows our forecasts for inflation and the policy rate.

PHILIPPINES CENTRAL BANK TO HIKE AGAIN

Bangko Sentral ng Pilipinas is expected to hike its overnight borrowing rate by 50bps on Thursday and bring cumulative hikes to 350bps since March. Inflation has continued to climb to 8% y/y in November but the 6% appreciation in the peso to the US dollar since October may give the central bank confidence that stability risks have lessened.

TAIWAN’S CENTRAL BANK STILL ON A TIGHTENING PATH

Another small rate hike from 1.625% to 1.75% is expected on Thursday. Inflation recently ease with headline inflation falling back to 2.4% and core declining slightly to 2.9% in November from 3%.

RUSSIAN CENTRAL BANK—ENDING THE CUT CYCLE?

The Key Rate is likely to remain at 7.5% on Friday and probably bring to a close the massive rate cuts that have totally 12.5 percentage points since March. High frequency week-over-week inflation is starting to move higher over recent weeks and may give the central bank room to hold off and monitor conditions.

US INFLATION—INFORMING THE TREND

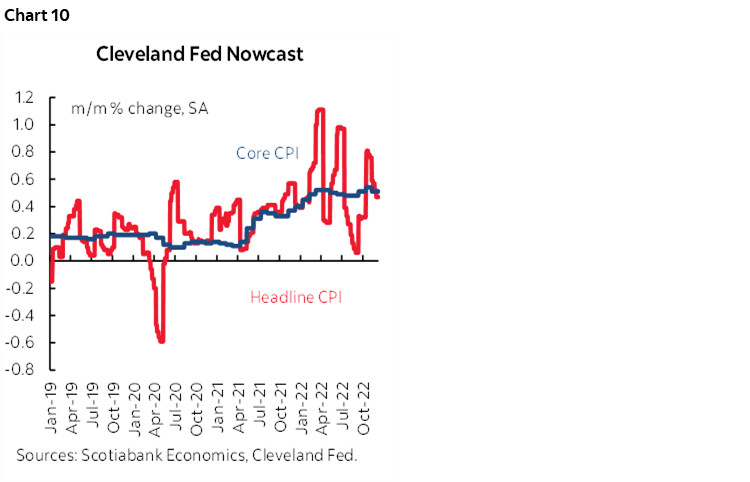

Was the softer than expected core CPI inflation reading of 0.3% m/m in October a harbinger of things to come or another head fake? We’ll get more information when November CPI arrives on Tuesday.

I’ve estimated a rise of 0.4% m/m for both headline CPI and core CPI excluding food and energy prices. The Cleveland Federal Reserve’s ‘nowcast’ points to something a touch firmer at 0.5% m/m for core inflation (chart 10). That measure over estimated inflation the last time around, but the measure often performs well and when it overestimates inflation it can tend to underestimate the next print.

Among the expected drivers are resilient gains in owners’ equivalent rent, broad service prices and another hot gain in food prices. Vehicle prices—both new and used—did not change enough in seasonally adjusted terms to influence the estimate. Gas prices and other energy drivers probably knocked about a tenth off CPI.

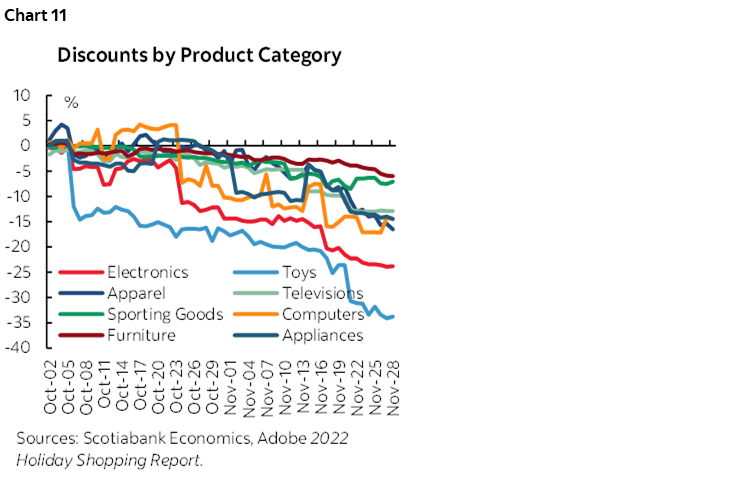

An added consideration is the degree to which mildly greater than seasonally normal discounting of some products during holiday season sales toward month-end may drag on inflation (chart 11). It may somewhat, but the categories that are typically discounted at this time of year have modest weights in CPI compared to other drivers and the discounting mostly occurred late in the month. CPI takes average prices throughout the month.

OTHER MACRO

A rich array of other macroeconomic indicators lies in store over the coming week and I’ll address them in more detail in daily notes. Highlights follow.

At the top of the list will be a round of purchasing managers indices that further inform risks facing the global economy. PMIs will land in the Eurozone (Friday), UK (Friday), US (Friday, S&P gauges), Australia (Thursday) and Japan (Thursday) plus Japan’s Q4 Tankan survey.

US retail sales (Thursday) will require a strong holiday shopping season to offset the effects of a 5.1% m/m drop in vehicle sales and a modest decline in gasoline prices. The US will also update industrial and business gauges such as NFIB small business confidence (Tuesday), and on Thursday each of industrial output in November, the Philly Fed manufacturing gauge, the Empire manufacturing gauge and capacity utilization.

Canada faces a light release schedule including an expected large gain in manufacturing sales during October (Wednesday), a probable dip in housing starts in light of softening permits (Thursday), home resales for the month of November (Friday) and an expected gain in wholesale sales (Friday).

Australia updates job market conditions in November on Wednesday. The country has created about 65k jobs in the past three months and wage growth has accelerated.

China will provide November readings for retail sales, industrial output, job markets and probably financing figures by around mid-week.

India updates CPI for November on Monday and it is expected to pull back from 6 ¾% y/y to under 6 ½%.

New Zealand’s economy probably continued to post solid growth in Q3 (Wednesday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.