- BoC hiked 50bps, more than priced, matching our soft conviction

- Forward guidance struck the right balance toward next steps…

- ...by leaving the door a little less open to another rate hike

- The next move depends highly upon data and event risk over the next seven weeks

- What changed in the statement and what’s next for communications.

The BoC hiked by 50bps and left the door a little less open to continuing to raise its policy rate. On balance the statement was more hawkish than markets anticipated. It was in line with Scotia’s expectations for 50bps and forward guidance, albeit we had warned that conviction was pretty soft around multiple scenarios.

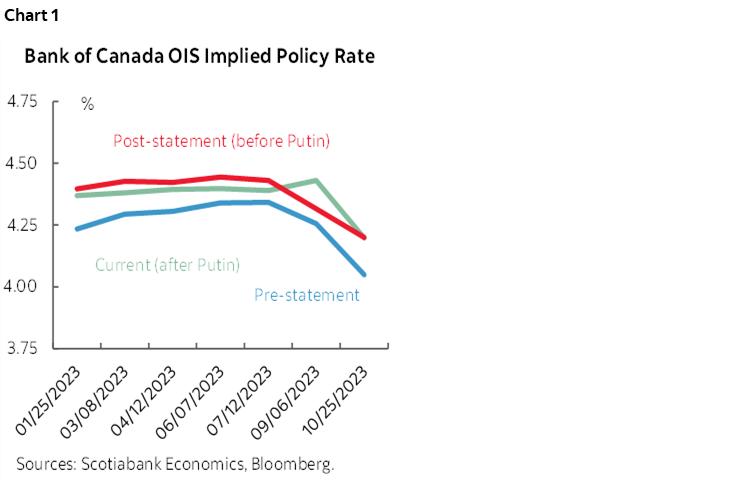

Markets responded by raising the 2-year Government of Canada bond yield by 10 bps, lifting the 5 year yield by 8 bps, and raising terminal rate pricing by about 9bps and are pricing part of another 25bps hike into January and subsequently before starting to price the chance at a rate cut by the end of next year. The Canadian dollar also appreciated by a half penny at first but has since drawn even post-statement partly due to safe haven seeking into the USD on Putin’s repeated warnings about nukes that hit headlines shortly after the BoC statement arrived. Chart 1 shows the meeting-by-meeting market pricing of future moves pre-statement, post-statement but pre-Putin and post-statement and post-Putin.

What they Said

Key in the attached statement comparison is the final paragraph. They are now “considering” whether to continue hiking versus the prior determination.

That’s actually not as big of a change as some are making it out to be. Here’s what they said in October:

“The Governing Council expects that the policy interest rate will need to rise further. Future rate increases will be influenced by our assessments of how tighter monetary policy is working to slow demand, how supply challenges are resolving, and how inflation and inflation expectations are responding. “

And here is what they now say:

“Looking ahead, Governing Council will be considering whether the policy interest rate needs to rise further to bring supply and demand back into balance and return inflation to target. Governing Council continues to assess how tighter monetary policy is working to slow demand, how supply challenges are resolving, and how inflation and inflation expectations are responding.”

And so you could argue that they took the first step to sounding more cautious with their forward guidance at the October meeting and built upon that today. Instead of “will need to rise further” alongside conditional language around future hikes after this one, they are now “considering” whether to hike again after today’s 50bps which sounds a little less decisive.

It’s not, in my opinion, a quantum shift. That language closes the door to further hikes a touch more than what they had already intimated in the October statement but nevertheless leaves it open.

Other notable changes in the statement included the following points with assessments of each points hawkish/dovish slant:

- They acknowledged that global growth “is proving more resilient than was expected” in the October MPR. That’s hawkish in isolation.

- They signalled unease toward the risks facing supply chains by noting that “further progress could be disrupted by geopolitical events.” I swear Putin read that when he warned about nukes 10 minutes after the statement dropped. This is also mildly more hawkish from the standpoint of potentially interrupting disinflationary progress.

- The BoC flagged that Q3 Canadian growth was stronger than they forecast. About double to be exact. That’s also hawkish acknowledgement that the economy pushed further into excess demand conditions, but it’s just a statement of already known fact.

- Netting through the growth drivers, they reaffirmed “the Bank’s outlook that growth will essentially stall through the end of this year and the first half of next year.” That’s the not-recession-because-we-can’t-say-it nod. Dovish, but not incrementally so.

- The main dovish nod was the reference to how “Three-month rates of change in core inflation have come down, an early indicator that price pressures may be losing momentum.” That’s a little stronger than the prior statement’s comment on the 3-month trend. The caution here is whether that’s just a transitory development in the context of still strong underlying cyclical and structural drivers.

- Nevertheless, they took that back in part by noting that “inflation is still too high and short-term inflation expectations remain elevated” while repeating worry about expectations the longer inflation remains above target.

PRESERVING OPTIONALITY

Overall I think they did the right thing here given what we know to this point. Slamming the door shut by declaring an absolute end to the hike cycle would have been too aggressive in my view and as the policy rate pushes further into restrictive territory they should be transitioning toward something that is more sensitive to new information. My conviction toward the BoC’s stance was high from when I was writing notes in late 2020 and early 2021 saying they’d hike by early 2022 while they underestimated inflation risk, but that conviction is much weaker the further we push into restrictive territory for the policy rate.

On that note, the forward guidance sounds more conditional which increases optionality into the January 25th meeting which in today’s world may as well be a decade from now. By then we will have two more CPI prints to inform whether they’ve been head faked of late or something more durable is building, plus another jobs report alongside greater clarity around how high the Fed is willing to go.

HAWKISH OR DOVISH?

So do you call it dovish, hawkish, or somewhere in between? Hiking more than was priced and leaving the door open without a clearer signal that "we're done!" is pretty clearly more hawkish than markets expected. The market reaction is likely sensible to this point. Now we have a job to do in tracking developments on the rather long road until the next full forecast meeting.

LEFT UNANSWERED

Not once was there a reference to wage growth and wage-price pressures. Wage growth is strong in Canada and productivity has tumbled throughout the pandemic. Governor Macklem has delivered a speech that boldly declared wage growth was peaking now which is highly debatable and he also failed to even mention moribund labour productivity. Is the reason such references are absent from the statement a sign he is wavering after the last jobs report? Why not statement-codify such an expectation if he still so strongly believes this?

Also, what does the Governor now think of CAD? He sparked interest with his comments earlier this Fall that suggested greater unease toward the Canadian dollar’s depreciation. Then he went quiet on the topic as CAD appreciated from mid-October to early November. Now that it has resumed trend weakening notwithstanding today’s modest move is he more or less concerned about CAD and layering on lagging price pass through effects into next year? Normally the BoC would look through this, but we don’t have normal inflation or normal expectations and so what the Governor thinks about another modest potential upside catalyst to inflation may be useful to know.

NEXT UP

Deputy Governor Kozicki delivers the customary day after BoC speech tomorrow. The embargo lifts at 12:30pmET and there will be a press conference at 2pmET.

Governor Macklem then speaks next week on Monday to deliver the Governor's usual pre-holiday speech and press conference (here). Last year's was a hawkish pivot (and then he whiffed in January, but anyway...). I think his speech is likely to follow a similar tone to the statement but he may add to our understanding of the probability of approaching an end to the rate hike cycle.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.