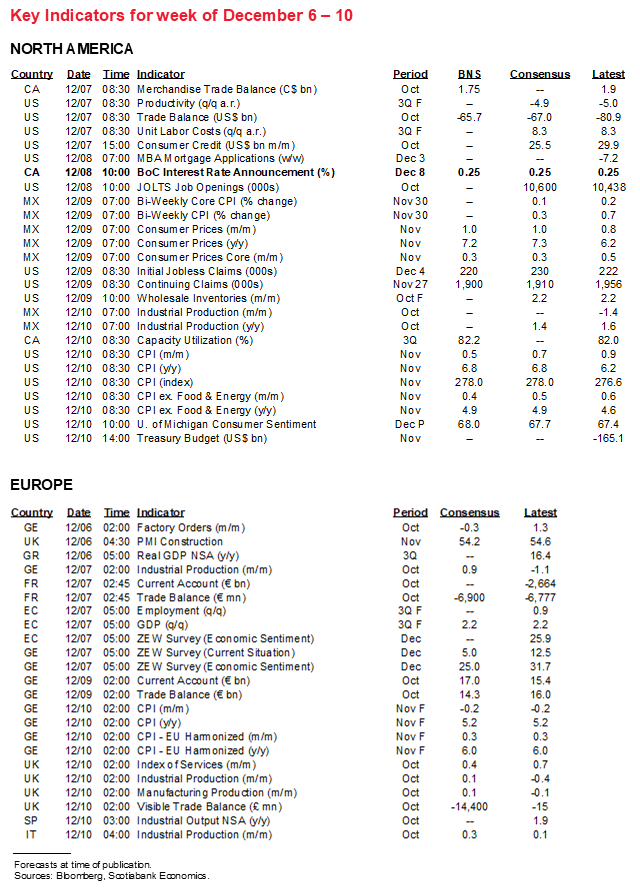

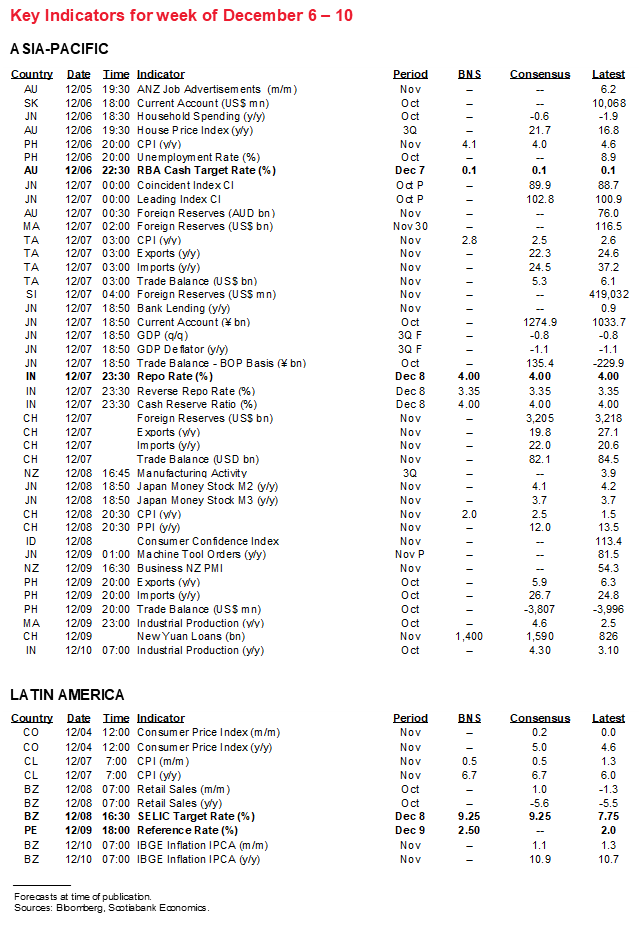

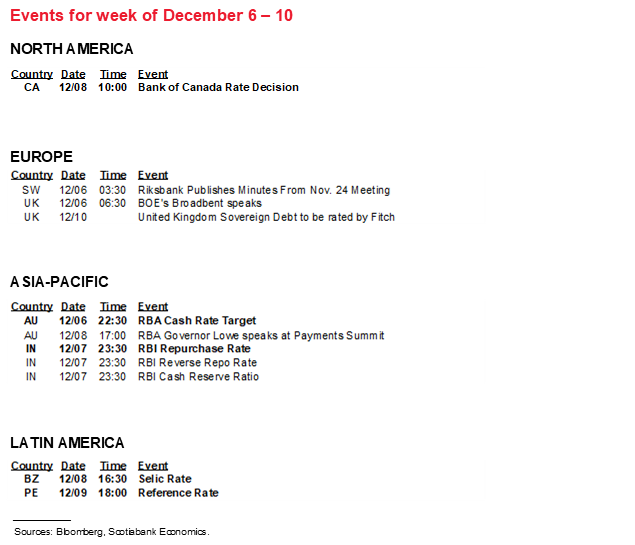

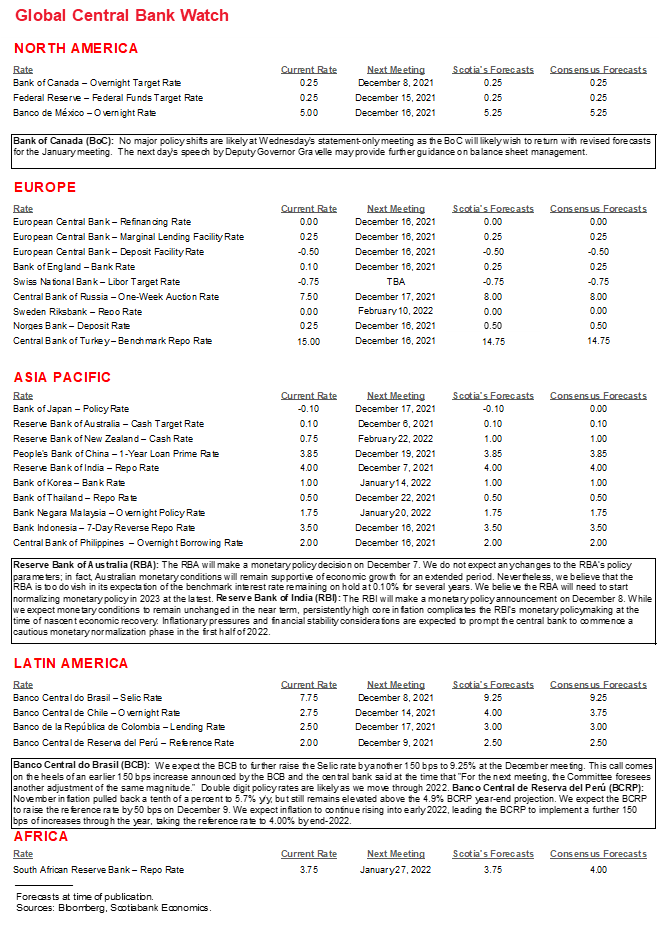

Next Week's Risk Dashboard

• Fed policy has become too easy

• US inflation set for another gain

• Bank of Canada expectations

• China on watch for RRR cut

• Another big hike from Brazil?

• Peru’s CB expected to hike again

• RBA’s big decisions are ahead

• RBI forward guidance on watch

• Inflation: China, LatAm in focus

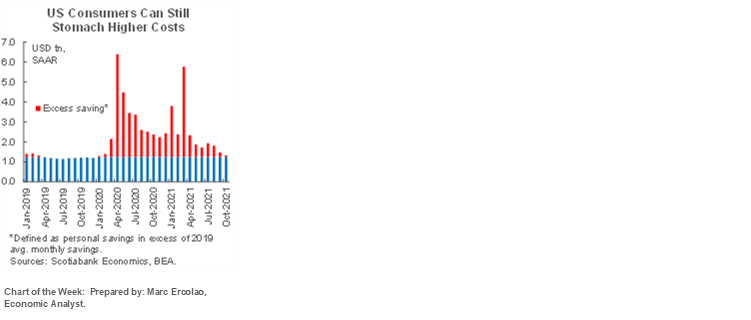

Chart of the Week

US INFLATION—DRIVING EASIER POLICY

Another round of inflation data kicks off with Friday’s US consumer price index for November. I went with a rise of 0.5% m/m for headline that would take inflation to 6.8% y/y from 6.2%, while core CPI is forecast to rise by 0.4% m/m to 4.9% y/y from 4.6%.

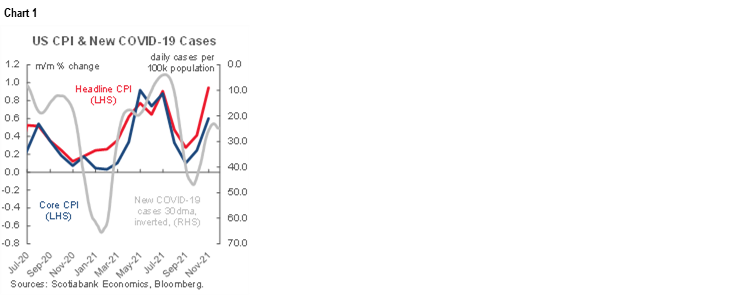

One general driver is that the easing of Delta variant cases from earlier peaks could continue to put upward pressure upon prices. Even though the number of new cases was starting to edge a little higher nationwide later in November and now into December as Omicron uncertainty lies ahead, prior months have witnessed fairly sustained price pressures around reasonably stable easing of cases (chart 1).

Other drivers include tracking of used vehicle prices. They were up by 5% m/m seasonally adjusted according to the Manheim index and 9.3% m/m according to JD Power (NSA) whose prices serve as input into CPI. At a 3.3% weight in CPI, used vehicles could add at least 0.2% m/m to headline and core CPI whether seasonally adjusted or not. Higher gasoline prices could add another 0.1% m/m to headline CPI. November is typically a month with little seasonal price pressure that would impact month-ago NSA prices as input into the year-over-year inflation rate.

HOW SHOULD THE FED REACT?

A popular question among clients is why the Federal Reserve would be turning more hawkish in the face of supply-side driven inflationary pressures. First off, they’re not, it’s arguably the opposite, and secondly, that’s a mischaracterization. Both of these points are worth elaborating upon since they flow naturally from the upcoming inflation update.

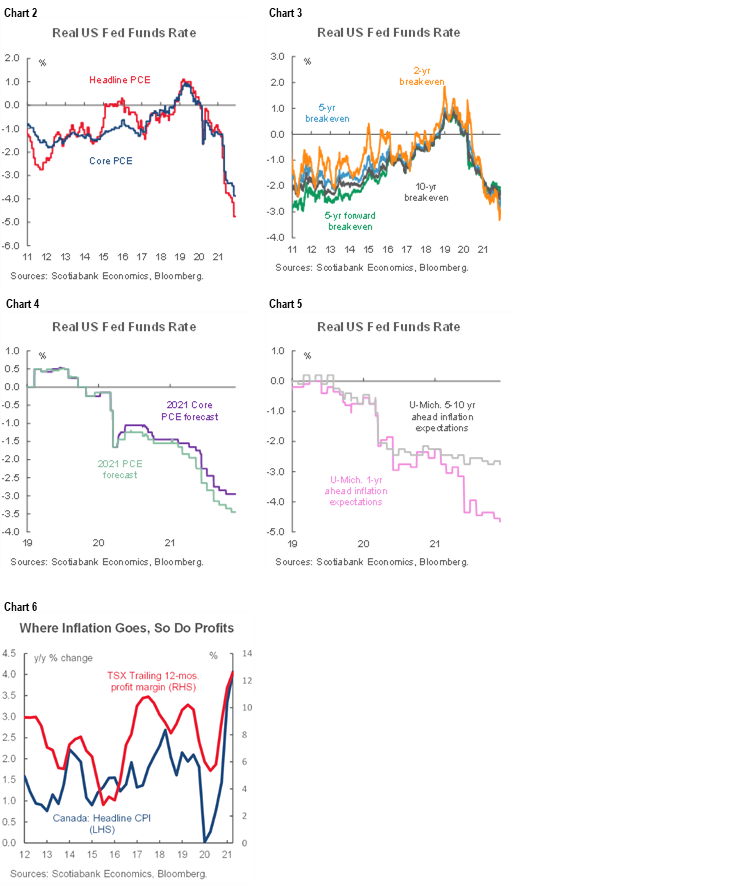

Firstly, hawkish?? I think it’s the opposite and a pivot toward opening the door to hiking the nominal policy rate is needed in order to take some of that back. The Federal Reserve allowed the real policy rate to turn more deeply negative and hence easier as any measure of backward- or forward-looking inflation expectations has risen while they talked through it (charts 2-5). That would be true even if inflation cruises back down from 6–7%+ to materially lower. Macro models use real rates. When real rates go more deeply negative and the Fed’s reaction function to the development is at best described as a policy of benign neglect or at worst outright policy error (I think the latter…), then they invoke more stimulus to the economy precisely when we don’t need it. More stimulus—all else equal—means more inflation. Think of a simple example being a company that is getting more net pricing power in excess of what has happened to their borrowing costs which buoys margins which can benefit the real economy. Chart 6 shows the connection between inflation and profit margins as evidence.

The decline in the real policy rate is also why we shouldn’t necessarily and materially downgrade our growth forecasts just because of Omicron (that we know little about…), as this de facto easing of policy stimulus serves as an offset.

As for the Fed’s balance sheet, it is still expanding and the stock theory of such moves leans to heavy stimulus remaining in place for a long time and in fact increasing until at least March and then turning incrementally neutral. Here too we remain some distance away from balance sheet tools turning more hawkish per se.

In my view, however, the Federal Reserve should be more hawkish and markets should be pricing more hawkish policy outcomes. Markets are too lightly priced for rate hikes in 2022 with fed funds futures pricing two hikes in 2022. It’s hard to imagine it even being worth Chair Powell’s time to get out of bed in order to deliver two hikes in 2022 given the scant effects on the economy and markets.

As for what’s causing inflation, some of it is obviously supply driven, but central banks are trying to let themselves off the hook by exaggerating its prominence and some folks in the markets are rather complicit in this regard! For one thing, chart 7 shows the surge in domestic demand as policy over-stimulated demand. Fitting a pre-pandemic trend-line to final demand shows that if the goal was to right the ship in terms of final demand then mission accomplished and perhaps then some! The rate sensitivity of demand may have been a lot greater than central banks assumed it would be.

Plus there is a lot of uncertainty around where potential GDP and maximum employment sit. With US GDP having already recovered the pandemic hit by 2021Q2, we could now be very close to capacity limits. If we’re dealing with long-lived skills mismatches and retirements from the US workforce, then maybe we’re closer to full employment than job shortfalls suggest. If the US economy is approaching capacity limits, then policy tightening would have merit.

Forward-expectations can also risk becoming a self-fulfilling prophecy and reason to shift toward a tightening stance. If folks expect higher prices next year and subsequently, then the way they behave in practice can add to the pressure through anticipatory buying and investment in capital goods.

Finally, market pricing for the policy rate to lift-off is in the ballpark of when the US economy closes off spare capacity and starts pushing into excess aggregate demand and may even be a little too late. That wouldn’t be tightening for supply-side reasons. It would also be the point at which another set of factors supports inflation—namely excess aggregate demand at or beyond the point of full employment and maybe wages.

In all, Fed policy shifted toward being more dovish via what was allowed to happen to the real policy rate and expectations for its evolution driven by Fed policy rate expectations, while tightening soon could very well prove to be compatible with demand pressures. As previously written, the clock for Fed hikes in 2022 should arguably start at 100bps if it’s going to be anything meaningful.

BANK OF CANADA—C’MON, GIVE US SOMETHING!

The Bank of Canada delivers its latest policy decisions in a statement-only affair on Wednesday at 10amET. It will be followed the next day by the customary ‘economic progress report’ to be delivered this time by Deputy Governor Toni Gravelle who will also host a press conference which we haven’t seen in a little while.

Gravelle heads the financial markets division at the BoC and gave his last speech way back on March 23rd that focused upon balance sheet management and exit guidance (here). Governor Macklem subsequently updated this guidance (here) and the BoC actioned its move into the reinvestment phase at the October meeting (recap here). Perhaps exit guidance will once again be Gravelle’s focus this time around, in which case I would watch for refreshed guidance on reinvestment and maybe asset sales.

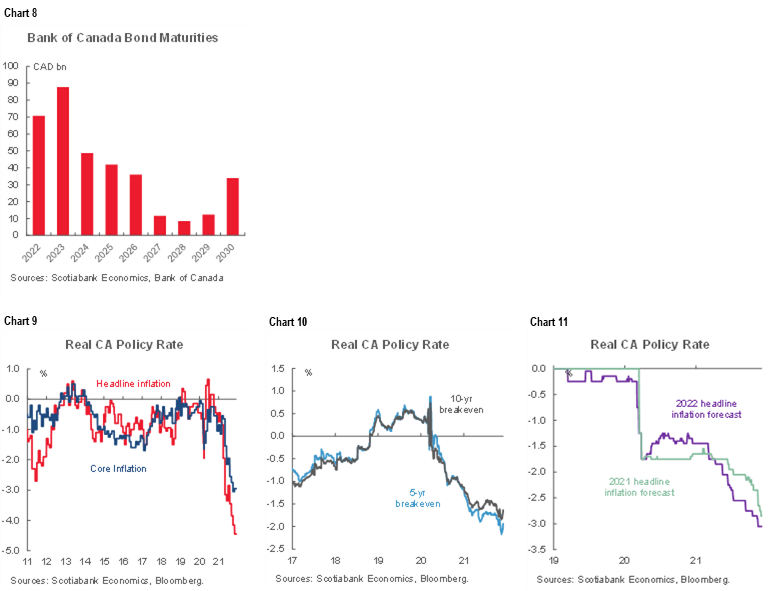

To date, the BoC has only said they will reinvest “at least until we raise the policy interest rate” and they have not provided guidance on asset sales. There are no GoC bonds maturing off the BoC’s balance sheet either over the remainder of this month or in January before a wave of maturities subsequently arrive (chart 8). This could therefore be a window of opportunity for refreshed guidance especially in light of the fact that jobs have increased by another 185k since the October meeting while arguably pushing into maximum employment (recap here). Furthermore, through the monetary policymaker’s version of benign neglect, the real policy rate has pushed more deeply negative and via this measure has served to ease monetary policy conditions (charts 9-11).

One option for the BoC to consider could be to signal reducing the pace of reinvestment and/or refresh guidance on when reinvestment may end. Ending reinvestment now would violate prior guidance. We could also hear more about any openness toward asset sales and efforts to drain liquidity, as market proxies for the Bank of Canada’s policy rate like CORRA have edged a few basis points lower.

As for the statement and Gravelle’s broader guidance, the best course of action for the BoC is likely to play it safe in a short and sweet statement that defers deeper thoughts to the next meeting on January 26th 2022 which will be a full meeting including a Monetary Policy Report containing fresh forecasts. By that time, there may be greater available insight into the threat posed by the Omicron variant once we hopefully learn more about the efficacy of vaccines, antibody drugs and other treatments, the severity of symptoms across broader populations and the speed at which it is spreading. For now, expect a statement reference to this fresh uncertainty while leaving it at that. Also by that time, the Federal Government’s somewhat opaque process to date around setting fiscal policy priorities may be better informed including via the December 14th Budget Update.

We might hear reference to how a second half economic rebound is proceeding in line with expectations, while nevertheless being the case that the BoC’s 2021 growth forecasts may be a touch too high net of all of the GDP revisions of late. Additional downside risk at least through Q4 is likely via the widespread flooding in British Columbia, but reference toward an expected rebound should signal the BoC’s tendency to look through the effects for monetary policy purposes.

We don’t expect to hear word on the BoC’s strategic review this week. Governor Macklem delivers the customary pre-holiday speech the week afterward.

CHINA’S RRR-WATCH TO LEAD OTHER CENTRAL BANK DEVELOPMENTS

Four other central banks deliver policy decisions but the main consideration across global markets is likely to be the PBOC.

Chinese Premier Li recently stated that a cut to the required reserve ratio applied to banks may be delivered “at proper time.” Any day now would be welcome given mounting downside risks. Chart 12 shows the evolution of required reserve ratios. If cut, it could free up somewhat more bank capital to apply to lending which could help to stimulate China’s sagging economic growth. Events over the course of this week might offer a suitable backdrop for such a move including CPI on Thursday and the aggregate financing figures for the overall economy that are due at some point this week or next.

Brazil’s central bank is expected to hike its policy Selic rate by another 150bps to 9.25% on Wednesday. Why? Because at the last meeting on October 27th they hiked by 150bps and rather explicitly said “For the next meeting, the Committee foresees another adjustment of the same magnitude.” Since then, Brazilian inflation spiked higher again on November 10th when it hit 10.7% y/y (from 10.25%). Another update is coming next Friday (chart 13).

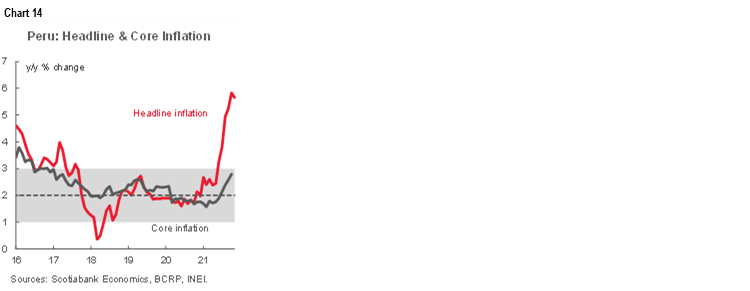

Peru’s central bank is expected to hike by 50bps to a new policy rate of 2.5% on Thursday. Inflation ebbed a bit in November but remains at 5.7% y/y while core inflation accelerated to 2.9% y/y (chart 14).

The Reserve Bank of Australia’s policy decision on Monday evening will be monitored for two possible though unlikely hints in light of the arrival of the Omicron variant and the uncertainties it represents. First, while they have stated that the A$4 billion/week bond purchase program will be re-evaluated at the next meeting in February, we’ll be watching for hints that they are perhaps leaning toward curtailing or ending it. A full discussion at the February meeting likely makes it premature to expect much just yet. This would be a further step after abandoning its 3-year yield target under pressure from financial markets. Second, any discussion around potential timing of rate hikes is unlikely at this meeting but conditions around growing consensus opinions that it may bring forward its guidance somewhat may be discussed.

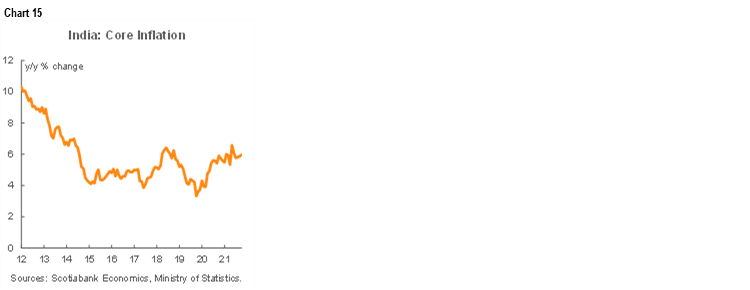

The Reserve Bank of India’s policy decision on Tuesday evening (ET) is not expected to reveal major shifts in policy guidance. Discussion around forward guidance for policy tightening in 2022 may be a risk in light of rising core inflation (chart 15).

While their central banks won’t be making policy decisions over the coming week, local monetary policy considerations may be further informed by a wave of CPI inflation updates for November starting with Colombia on Saturday, followed by Philippines on Monday, then Chile and Taiwan on Tuesday, Mexico on Thursday and Norway on Friday. I’ll write about those during the week as they arise.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.