- Our outlook is broadly unchanged from the June forecast, and incoming data have strengthened our confidence in the underlying narrative.

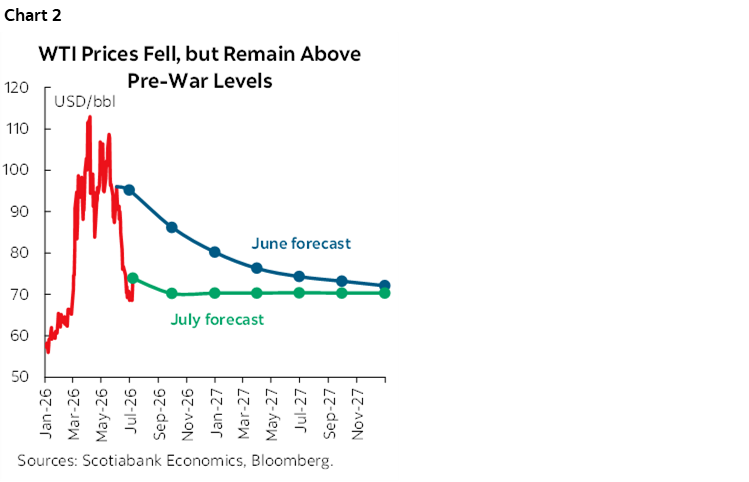

- Canada: Recent data have evolved broadly in line with our expectations and continue to support the view that the economy is moving out of the soft patch seen at the start of the year. Despite the volatile situation in the Middle East, oil prices are lower than in our previous forecast, weighing modestly on the near-term outlook, particularly through business investment and total CPI inflation. However, the weaker Canadian dollar broadly offsets that drag by providing support to exports.

- United States: The story is similar, near-term activity looks slightly stronger than previously expected, partly reflecting weaker import growth. Inflation has continued to surprise to the upside in both headline and core measures, reinforcing the case for caution from the Fed.

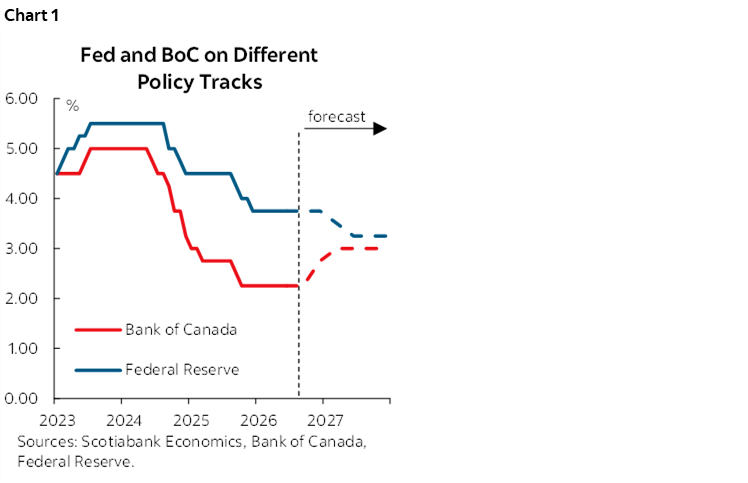

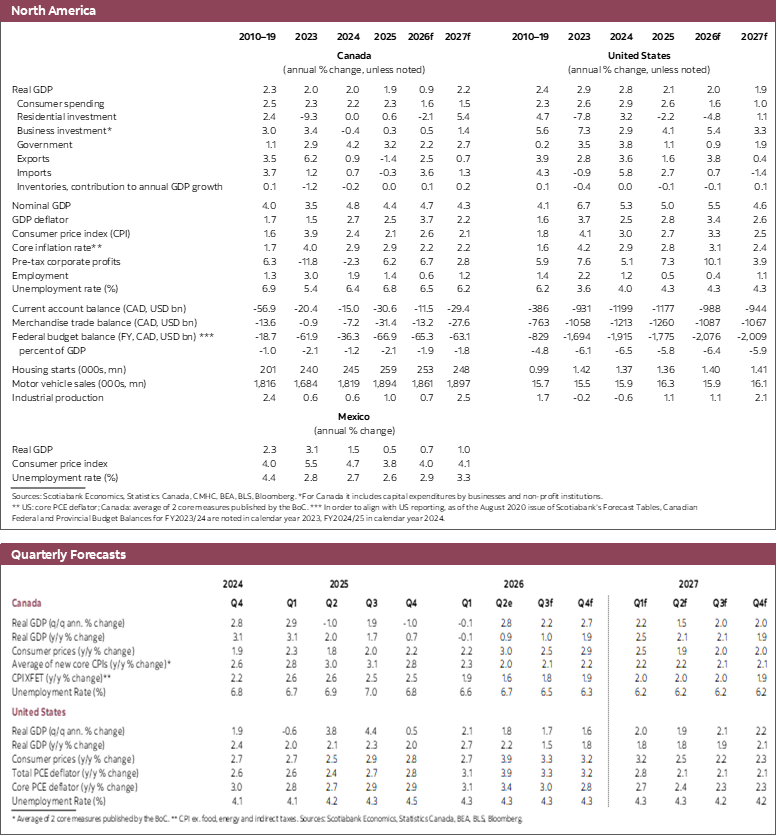

Our outlook remains broadly unchanged from our June forecast, reflecting a series of offsetting developments since our last update. Financial markets have remained volatile, oil prices have declined, and the Canadian dollar has weakened. At the same time, incoming Canadian data have largely reinforced the dynamics outlined in our June note, suggesting that the economy is beginning to emerge from its recent soft patch. Inflation risks remain elevated in our view, which should keep the Bank of Canada cautious and ultimately lead to a gradual normalization of policy rates beginning toward the end of this year (chart 1). In the United States, economic activity continues to display resilience despite the expected moderation in household demand as hiring remains modest and real wage growth stalls. Meanwhile, inflation has proven more persistent than expected, prompting the Federal Reserve to take a cautious approach to potential rate movement.

Oil prices fell sharply in June before renewed geopolitical tensions pushed them higher again in July. Even after that rebound, prices remain well below the assumptions embedded in our June forecast, creating a modest drag on the near-term outlook. Spot prices are likely to remain volatile in the near term given the geopolitical backdrop. However, we continue to expect oil prices to settle around US$70 in 2027, broadly in line with our previous forecast (chart 2). That level remains above pre-war prices, reflecting a residual geopolitical risk premium.

UNITED STATES: MODERATING GROWTH

Aggregate activity in the U.S. has proven somewhat stronger than anticipated, with first-quarter GDP revised up from 1.6% to 2.1%, supported in part by volatile trade flows and continued strength in business investment. Beneath the headline, however, household spending continues to cool gradually as labour market conditions soften. We expect this trend to persist over the coming quarters, with consumer spending losing further momentum as labour demand is slowing and excess savings fade. Equity market gains should continue to provide some support to consumption, although less so than last year, while persistent inflation is increasingly weighing on real income growth. At the same time, business investment—supported by AI-related spending, strong corporate balance sheets, and elevated equity valuations—should remain an important counterweight and help cushion the moderation in domestic demand.

The other notable development has been inflation. Price pressures have once again surprised to the upside, reinforcing the view that the Fed cannot afford to become complacent. Policymakers now face a more difficult balance: inflation remains persistent, while household demand is slowing and the labour market is weakening. In our forecast, this pushes rate cuts later, though we still expect the Fed to move policy back toward a more neutral stance next year.

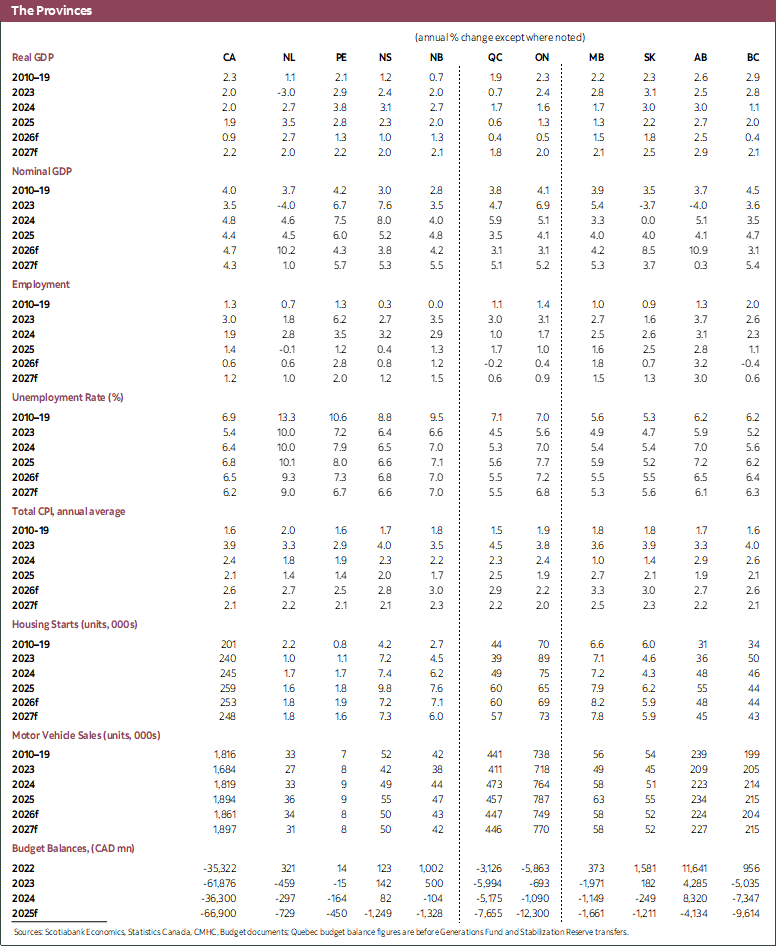

CANADA: EMERGING FROM THE SOFT PATCH

The Canadian economy continues to evolve broadly in line with our expectations. Recent data support the view that activity is beginning to recover from the soft patch experienced at the start of the year. GDP rose a strong 0.5% in April, matching roughly the earlier flash estimate, and recent labour market releases suggest that the anticipated improvement may be arriving somewhat sooner than expected. Although employment gains remain modest, broader labour market conditions appear to be stabilizing after a weak start to the year.

We now expect growth to average 0.9% in 2026, little changed from our previous forecast, although that annual figure masks a meaningful strengthening in momentum through the year. Quarterly growth should firm as the effects of past rate cuts increasingly support domestic demand, particularly in the housing sector and government spending catches up with planned outlays. As a result, we expect GDP growth to strengthen to 2.2% in 2027. The U.S. administration’s refusal to renew CUSMA by the July 1st deadline does not alter our baseline forecast. Canada’s exports remain protected by the agreement and continue to benefit from very low tariffs. We continue to assume that the free trade framework will ultimately be renewed.

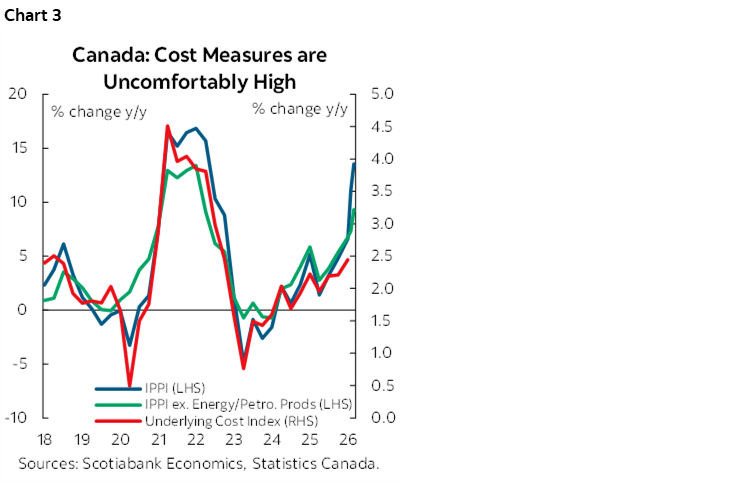

One area we continue to monitor closely is underlying inflation. Momentum has turned somewhat firmer in recent months, with monthly core inflation measures rebounding after a string of softer readings, broadly in line with our expectations. While headline inflation remains relatively well behaved, underlying cost pressures continue to run at levels that are inconsistent with a comfortable return to target. Unit labour costs, IPPI, and our own underlying cost-pressure measure continue to point to elevated inflation risks (chart 3). The recent decline in oil prices is a welcome development and should provide some relief, but we continue to see meaningful upside risks to the inflation outlook. Against this backdrop, the Bank of Canada is likely to remain cautious and lean against the risk of inflation reaccelerating. In our view, these risks warrant a gradual withdrawal of monetary policy stimulus, with the Bank beginning to raise rates twice toward the end of the year.

RISKS

- Persistent geopolitical tensions and upside oil price risks. While developments in the Middle East have recently moved in a more constructive direction, geopolitical tensions remain elevated and the risk of renewed disruptions cannot be dismissed. Oil supply continues to be constrained, and inventories are likely to require rebuilding over time, leaving crude prices vulnerable to renewed upside pressure. A sustained rise in energy prices would lift headline inflation directly and raise transportation and production costs more broadly. It could also feed into inflation expectations, amplifying and prolonging price pressures, requiring a stronger monetary policy response (see our previous note on this risk).

- Upside risk from U.S. fiscal policy. Additional fiscal support—including higher defence spending and potential household transfers—could boost demand, add to inflation pressures, and keep the Federal Reserve on a more hawkish path.

- CUSMA renegotiation risks. The U.S. administration’s refusal to renew CUSMA by the July 1st deadline was not unexpected but an adverse outcome to the upcoming CUSMA negotiations remains a possibility and would represent a significant downside risk (see here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.