- Data flow in Canada signals early-year softness, but underlying momentum is stabilizing. Canadian Q1 GDP disappointed, though distorted by temporary factors, with April pointing to a rebound. In the US, growth has also softened at the margin, with consumption beginning to slow alongside a weaker labour market.

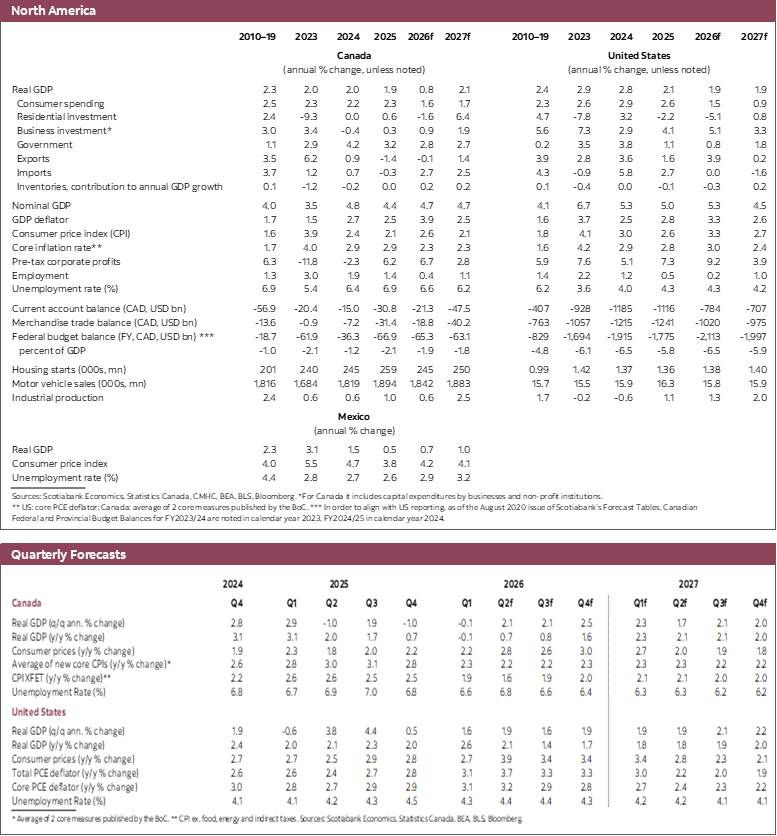

- US: growth slowing, but inflation persistence becomes the defining feature. The expansion is losing momentum as household demand cools, but resilient business investment—supported by AI and equities—provides a cushion. At the same time, broader cost pressures and stronger pass-through dynamics suggest inflation will remain elevated, keeping PCE above 3% in 2026.

- Canada: recovery underway, but inflation risks remain. Following the early-year soft patch, activity is set to reaccelerate, supported by fiscal spending, housing, and a recovery in exports. While core inflation has eased, pipeline pressures remain from elevated input costs, with inflation expected to stay near 3% in the near term before gradually returning to target.

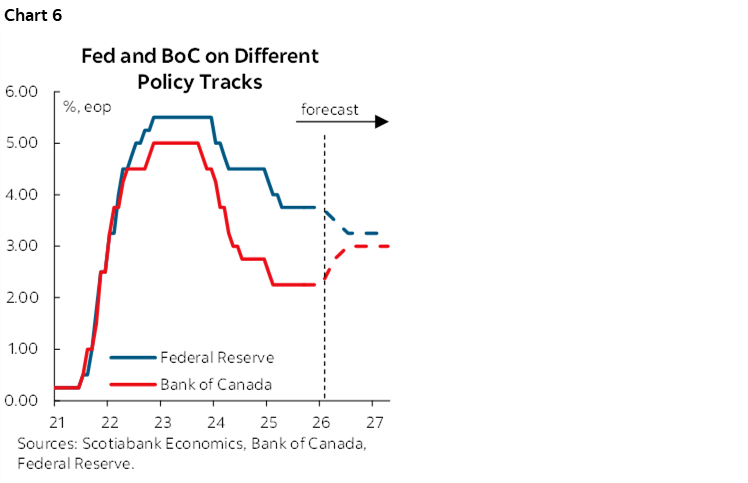

- Monetary policy on different tracks. We expect the Fed to begin easing late this year as it prioritizes labour market weakness, despite still-elevated inflation. In contrast, the Bank of Canada is set to move gradually toward normalization, with two hikes in Q4 taking rates to 2.75%, followed by a final hike in early 2027.

The Canadian economy hit a clear soft patch at the start of 2026, as confirmed by last week’s national accounts release. GDP was essentially flat in Q1, coming in below all expectations and pointing to softer underlying demand pressures. This aligns with earlier signals from the labour market, including weak hiring and a rise in unemployment at the start of the year.

That said, the headline weakness should be interpreted with caution. The Q1 print was affected by several temporary factors that materially distort the signal. Large swings in gold imports should be largely ignored, as should the sharp pullback in government spending, which is likely to reverse in Q2. Encouragingly, the flash estimate for April GDP already points to a meaningful rebound next quarter. Looking ahead, we continue to expect activity to firm, supported by fiscal spending and a recovery in export growth.

In the United States, the growth picture has also softened at the margin. Household spending has started to moderate, in line with a weak labour market and broadly consistent with our previous call. We expect this slowdown to extend through the outlook, although still-solid business investment should provide an important offset. At the same time, inflation has continued to firm—even excluding energy—suggesting the Fed will need to remain cautious on the pace of rate cuts this year.

The Middle East conflict remains a key risk to the global outlook. While oil prices have so far evolved broadly in line with our previous assumptions, the range of outcomes remains wide. A quick resolution would likely push prices lower, while a more protracted conflict would lift oil prices further and risk renewed supply chain disruptions—adding to global inflation pressures. While not our baseline assumption, risks are tilted towards the latter. Our current forecast assumes oil prices to normalize partially over the outlook, reaching $80 at the end of this year and $72 at the end of 2027.

US EXPANSION LOSING MOMENTUM, INFLATION BECOMING THE KEY RISK

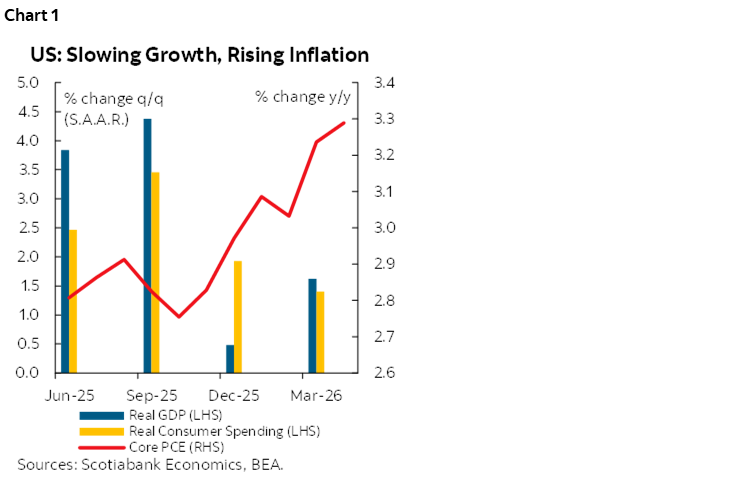

The US expansion is clearly slowing, but remains broadly consistent with our previous assessment. Household spending is set to soften further, in line with a weakening labour market (chart 1). Equity market gains should continue to support consumption, but the impulse is fading compared to last year. At the same time, real wage growth is increasingly being eroded by persistent inflation, pointing to a gradual deceleration in consumption ahead. That said, business investment should continue to provide an important offset. Supported by AI-related spending and still-strong equity market performance, investment remains a key pillar of growth and should help cushion the slowdown in domestic demand.

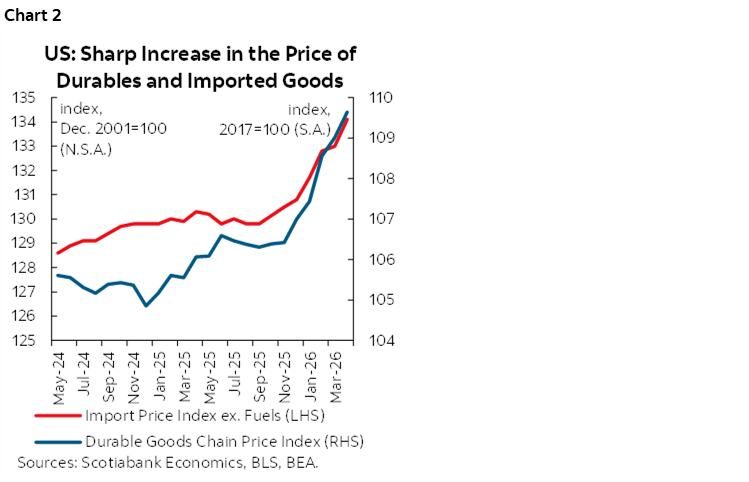

The more meaningful shift in the narrative is inflation. Recent data point to pressures that are becoming more pervasive and less tied to energy alone. A key driver could be a sharper-than-expected pass-through of tariffs and other costs into consumer prices, as suggested by the sharp pick-up in durable goods and imported prices (chart 2). Firms initially absorbed these costs through margin compression and inventory drawdowns but those buffers are being exhausted. With the economy in excess demand, firms have a greater ability to pass through more of these tariffs and increase in costs to consumers. The implication is that inflation will likely prove persistent over the outlook. We view US total PCE inflation well above 3% in 2026 and about 2.3% in 2027.

CANADA: RECOVERY UNDERWAY AFTER EARLY-YEAR SOFT PATCH

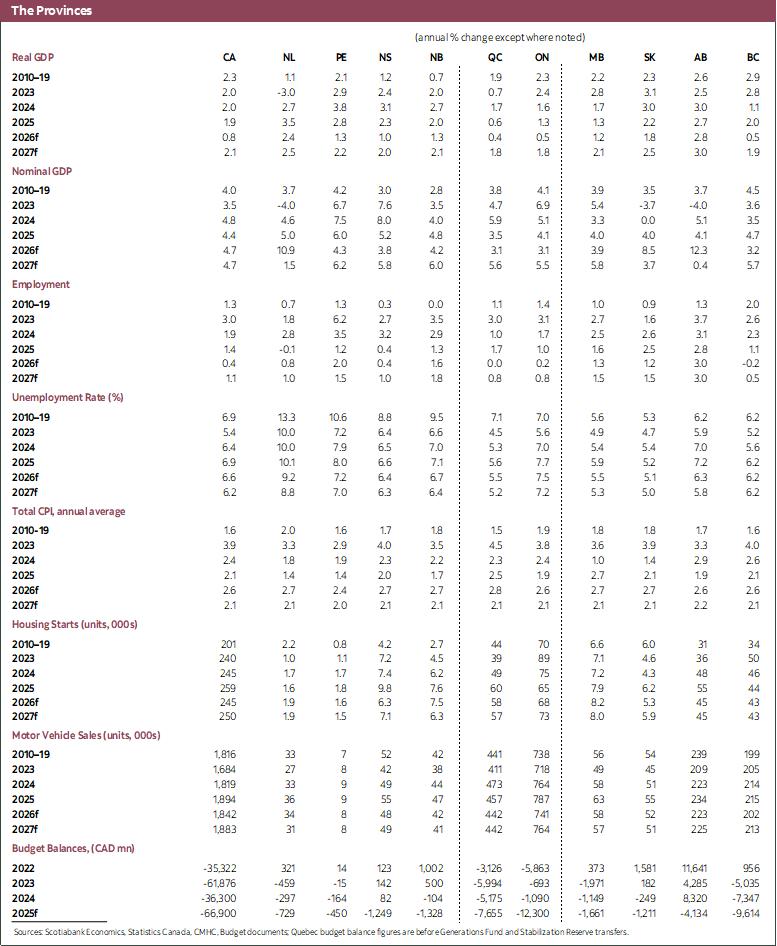

Canada is emerging from the soft patch seen at the start of the year, with a gradual recovery expected to take hold over the outlook. While we forecast growth to average 0.8% in 2026, this headline figure masks a clear reacceleration in underlying momentum. Quarter-on-quarter growth should firm meaningfully as government spending reconnects with planned outlays and the lagged effects of past rate cuts continue to support domestic demand—particularly in housing. External demand should also become more supportive over time. Export growth is expected to recover, albeit more convincingly into 2027 as the drag from tariffs fades. As a result, GDP growth is projected to rise to 2.1% in 2027. Taken together, this profile places growth above our estimate of potential—1.2% in 2026 and 1.6% in 2027—allowing the economy to gradually move back into balance by late 2027.1

Labour market dynamics are consistent with the broad activity narrative. While the unemployment rate has risen by 0.2 p.p. since the start of the year, this still marks an improvement relative to last summer. More importantly, the recent increase likely overstates underlying weakness, as a meaningful share reflects stronger labour force participation. With activity set to firm in the near term, labour demand should stabilize, allowing employment to gradually catch up with growth.

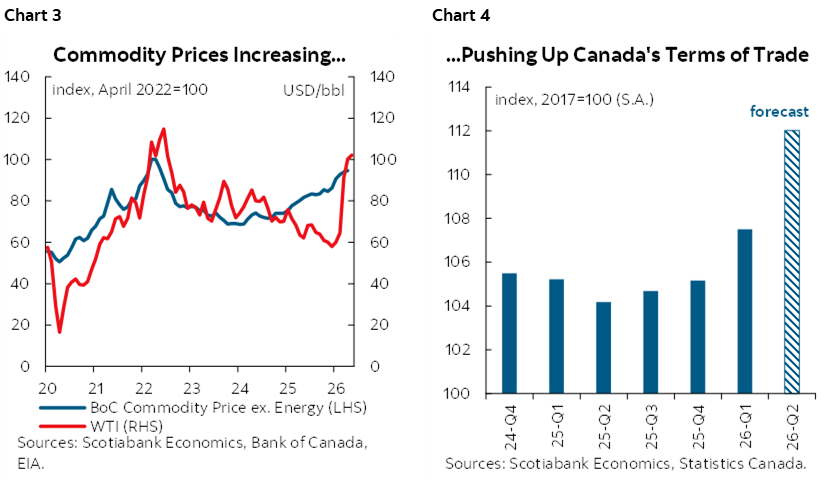

Commodity prices provide an additional, albeit partial, tailwind. Elevated oil and non-energy commodity prices should improve Canada’s terms of trade and modestly support investment and hiring (charts 3 and 4). However, this support is being offset in part by tightening financial conditions, particularly tightening policy rates and rising long-term government bond yields.

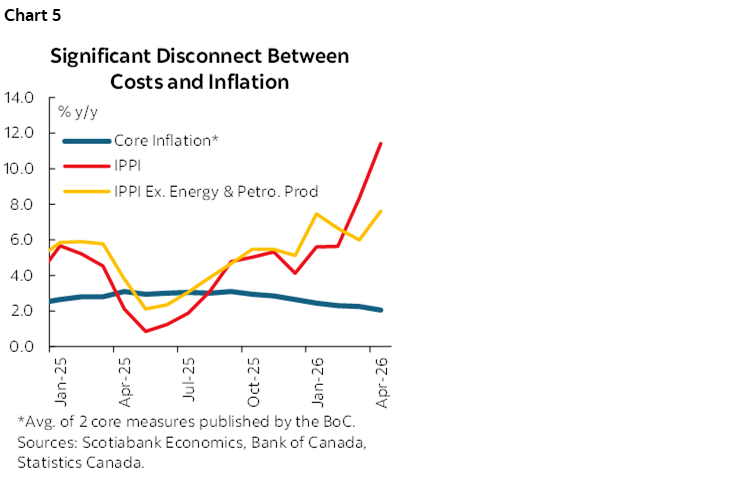

On inflation, the recent data have been more encouraging. Core measures have softened since our March update, pointing to some easing in underlying pressures, in line with weaker demand earlier in the year. However, we caution against over-extrapolating this improvement. Pipeline pressures remain significant. Elevated input costs, both energy and non-energy, are still expected to feed into final prices (chart 5). We view inflation staying close to 3% for the reminder of the year, driven by energy prices, before falling back towards the BoC target as energy prices normalize. At the same time, geopolitical risks remain elevated and could further disrupt pricing dynamics. In this environment, upside risks to inflation remain material, and we expect the Bank of Canada to remain focused on persistence.

MONETARY POLICY ON DIFFERENT TRACKS

The Fed and the Bank of Canada are set to remain on different policy tracks well beyond 2026 (chart 6). In the United States, we continue to expect the Fed to ease at the end of this year. This path remains somewhat more accommodative than what is prescribed by underlying economic conditions. The gap reflects our view that the Fed will increasingly focus on shoring up the tepid labour market and supporting growth, with continued political pressures and administrative changes. In this context, the Fed is unlikely to wait for inflation to fully return to target before moving. We therefore expect the Fed to extend some stimulus as it seeks to prevent a more pronounced deterioration in the labour market.

The Bank of Canada faces a more nuanced trade-off. We continue to see a gradual move toward normalization, but at a slower pace than previously anticipated. We expect the BoC to increase rates by 25 bps twice in Q4 of this year, reaching 2.75%, with one more hike in early 2027. Real rates remain in stimulative territory, suggesting scope to withdraw accommodation as the economy returns to balance. At the same time, the combination of softer growth and recent progress on core inflation gives the Bank time to calibrate the pace of normalization.

UPSIDE RISKS TO INFLATION ARE STILL IMPORTANT

The outlook remains subject to a wide range of risks, with elevated uncertainty on both sides of the growth, inflation, and rates outlook.

- Prolonged Middle East conflict. We are particularly concerned about a more protracted conflict that would not only push oil prices higher, but also sustain broader cost pressures through elevated transportation and production costs, and generating supply chain disruptions. Crucially, these dynamics are likely to interact with inflation expectations. With households highly sensitive to visible price increases—particularly energy and food—a prolonged oil shock could lead to a more meaningful drift in expectations. Our scenario analysis shows this channel can materially amplify the inflation response, with persistent shocks resulting in more entrenched inflation dynamics, requiring a stronger policy response and leading to a significant economic downturn.

- Upside risk from US fiscal stimulus. Additional fiscal support remains a key upside risk, particularly if defence spending rises more than currently assumed in the context of a prolonged Iran conflict. Proposed household transfers could further boost consumption if implemented. Taken together, a stronger-than-expected fiscal impulse would add to inflation pressures and could materially alter the Federal Reserve’s policy path.

- Breakdown of CUSMA negotiations. A breakdown in CUSMA negotiations remains a low-probability but high-impact downside risk. Such an outcome would weigh on both economies but would be particularly severe for Canada, given its strong trade exposure to the US, and would likely be sufficient to push the economy into recession.

- Downside risk from weaker demand and faster disinflation. The combination of weak activity early in 2026, softening labour market conditions, and a clearer slowdown in core inflation may be signaling softer aggregate demand than we currently assume. If confirmed, this would lead to a more sustained disinflation process. In that environment, the Bank of Canada would have little need to raise rates and could remain on hold for longer than currently expected.

1 This outlook is conditional on our population assumptions. We continue to assume roughly flat working-age population growth over 2026–27, at around 0.5% per year. Should population growth prove stronger than expected, it would likely provide additional support to activity, reinforcing the recovery path.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.