- Canadians are primed for a transformative budget on November 4th that will underpin the federal government’s ambitious investment agenda. Prime Minister Carney has signaled a shift in fiscal strategy—pairing operational restraint with greater investment outlays aimed at rebuilding the economy’s productive capacity.

- Numbers are already substantial heading into budget day. Roughly $112 bn in new outlays have been legislated since the spring election, while the PBO estimates another $45 bn shortfall due to a weaker economic outlook (FY26–30). Budget teasers add another $10 bn with a week still to go.

- A widening list of potential measures could be detailed in the budget with the largest fiscal implications likely tied to sweeping security and build agendas. The plan is also expected to pack in a climate competitiveness strategy, corporate tax competitiveness measures, new immigration numbers, and much more—alongside offsetting spending reductions that would balance a new operating budget by 2028.

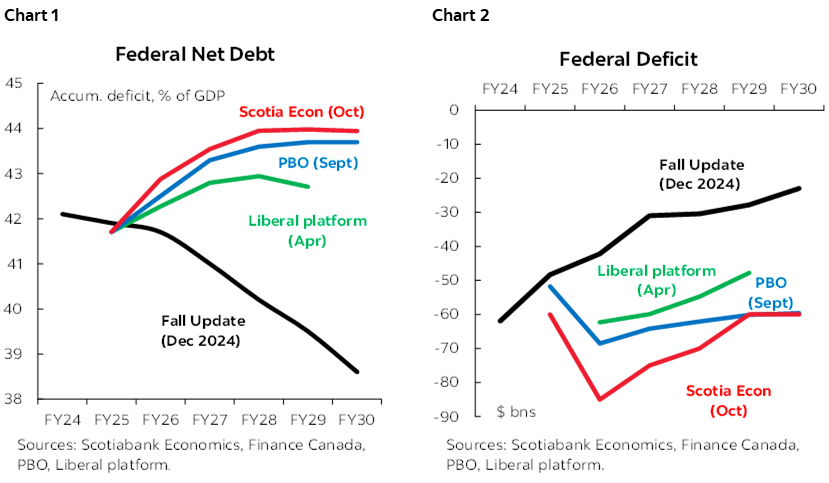

- But pre-budget costing is near-impossible—not all items will necessarily be in the first budget, not all will be on-budget, and not all will be stackable. We speculate (with low conviction) that net debt could rise by about 2 ppts to 44% of GDP by 2027, before ‘just’ stabilizing over the horizon. This path balances the desire to go big without potentially spooking markets with an ever-increasing debt path before the agenda gains traction.

- This would imply front-loaded fiscal outlays of roughly $85 billion (2.7% of GDP) in FY26 and $75 billion (2.3%) in FY27, before settling in the mid-to-high 1% range over the horizon (charts 1 & 2). Importantly, we also assume the feds could leverage non-budgetary tools that could reasonably add $10–15 bn annually in additional borrowing requirements on top of deficit needs, but with a smaller impact on net debt.

- The budget will land in a volatile global environment where ‘anything can happen’. Canada’s fiscal footing remains relatively solid, but its exposure to US policy whim could overshadow the budget’s long-horizon strategy in either direction depending on the day’s newsfeed.

- In this context, Canada has little choice but to play the long game—with patience, discipline, and a willingness to trade comfort for conviction in laying the groundwork for stronger growth down the road.

PRIME TIME CARNEY

Canadians are about to get a first look at the federal fiscal playbook. Finance Minister Champagne will table Budget 2025 on November 4th after skipping the traditional spring budget. Expectations are intentionally high: the government has cast this as a transformational plan to unlock large-scale investment in Canada’s productivity with a steady stream of teasers in the lead-up. The question now is not whether Ottawa will lean on its balance sheet, but how and how hard.

The budget will land in a deeply uncertain landscape. Since the Parliamentary Budget Officer (PBO) released its pre-election outlook last March, Canada’s economic outlook has whipsawed from relatively benign to crisis and back again to an uneasy middle ground, against a constantly shifting political backdrop. The PBO’s latest pre-budget baseline pencils in a $45 bn shortfall over FY26–30 on a weaker economic outlook alone. Our house view is marginally more resilient, but a credible plan warrants a healthy contingency in today’s volatile environment.

Prime Minister Carney—a politician today but an economist at heart—knows that a credible fiscal framework is a multi-year map, not an annual spending plan. We expect this budget will formally frame the fiscal parameters for wide-ranging decisions over the course of this government’s mandate. (And we don’t expect other parties to curtail that minority mandate just yet).

FLOODING THE ZONE

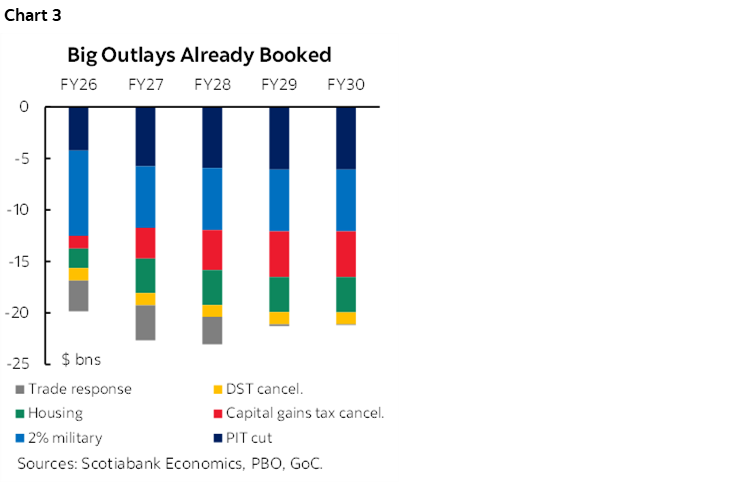

The absence of a budget has not stalled spending. The new government has already booked about $112 bn in new spending (FY26–30) according to PBO estimates. We arrive at similar numbers adding an incremental ~$20 bn annually to deficits over the coming years (chart 3). This includes July’s personal income tax cut, increased military spending to 2%, new housing measures, and the cancellation of the digital service tax. We estimate about two-thirds of campaign promises have already been tabled in the first six months in office.

Bigger outlays have been signaled. In the weeks leading into the budget, the government has pre-announced affordability and security measures worth roughly $10 bn over five years. Meanwhile, there is a widening list of unfunded pledges and pressures. The Finance Minister has conditioned Canadians for bigger deficits ahead or at least not pushed back as some forecasters are calling for triple-digit deficits—a risk but not our baseline.

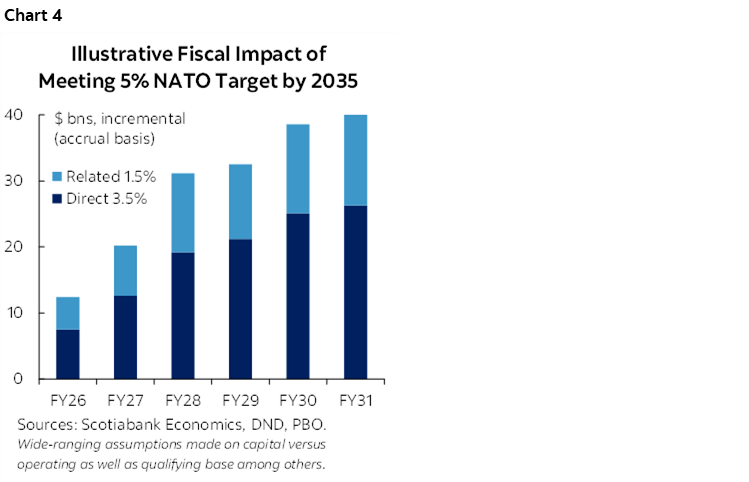

The potentially biggest-ticket item could be a further down payment towards the new (and much larger) security agenda. Ottawa will want to show credible steps toward its new NATO commitment of 5% of GDP annually within the next decade (3% on military and 1.5% on related outlays). Meeting the commitment in full could imply an incremental ~$135 bn in fiscal costs over the next five years (admittedly making sweeping assumptions), but that is unlikely to be fully booked just yet (chart 4). The fiscal impact in the upcoming budget rests on the path, composition, and catchment of “adjacent” spending—and importantly a political judgement on ‘just enough’.

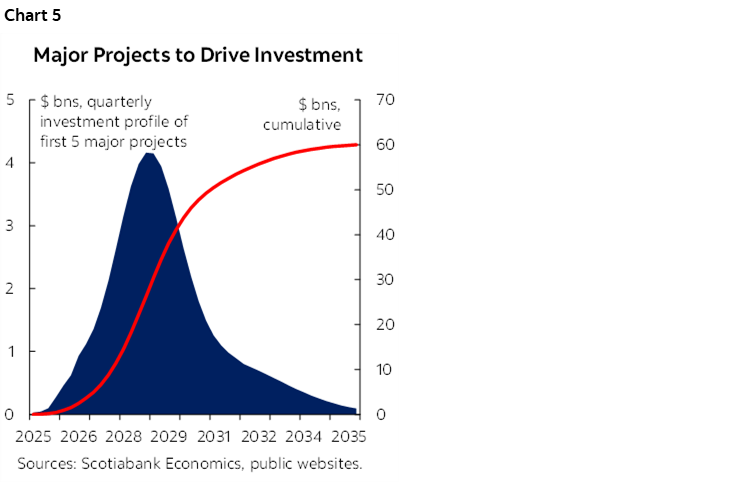

Infrastructure linked—but not limited—to the major projects pipeline is another pressure point. The new Major Projects Office is expected to not only advance projects of national interest but also help structure and coordinate financing as needed. The first of the five shortlisted projects recently secured a firm federal commitment—Darlington SMR at roughly $2 bn—and details on the remaining four could reasonably follow. These should provide some quick-wins in pulling forward the investment pipeline (chart 5). The next round of projects will be announced by mid-November and would likely require more government ballast given their earlier stages of development (and greater risk).

We don’t expect Ottawa to fully cost and book its full investment plan in this budget— spanning infrastructure, major projects, defense, climate, and housing—but we will watch for insights on how those ambitions could be carried on the balance sheet. Delivery mechanics are important: who carries the projects, how they are structured (operational versus capital, on- versus off-budget, etc.), and whether existing entities are sufficiently capitalized or, more likely, how much incremental capital could be added—to existing or newly stood-up ones. We will also be watching for greater clarity on overlap where investments could tick the box against multiple priorities with the same dollar.

Competitiveness is another expected theme with unclear (immediate) fiscal implications. The government has hinted corporate tax competitiveness will feature in the budget, while affirming a new climate competitiveness strategy will be there. It is conceivable the campaign-promised corporate tax review could be triggered, while the possible expansion and/or extension of full expensing of investment is one tangible option that would not likely pre-empt its findings. The climate competitiveness strategy is likely to be integrated into the broader investment agenda. There is already a range of investment incentives in train so we will watch for other policy or regulatory changes such as the elimination of the oil and gas sector emissions cap or potential changes to the industrial carbon emissions scheme.

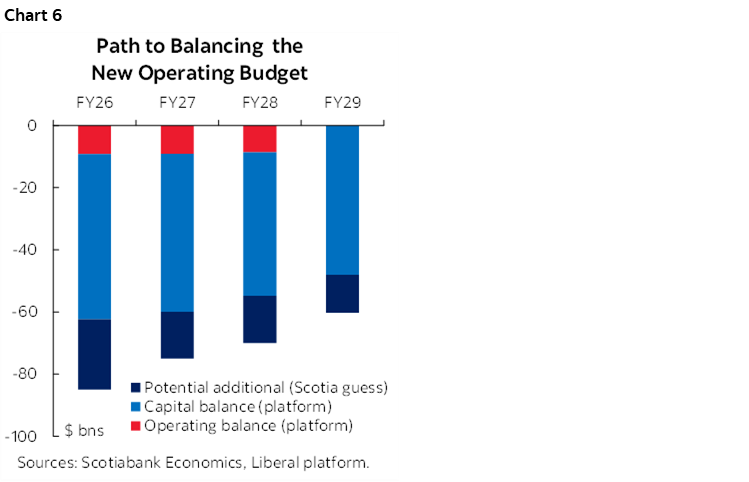

Not all measures are expected to push the government deeper into deficit territory. The government will split the bottom line into operating and capital accounts with the intention of balancing the “operating budget” within three years. Investment has been defined as outlays that create assets—public or private—ranging from traditionally-defined capital expenditures to more discretionary tools like tax incentives, housing supports, and conditional transfers. The election platform portrayed a comfort running deficit-financed investments in the order of 2% over the horizon (chart 6) though a deterioration in the economic outlook (and the case for more spending) likely pushes that higher at least in the near-term.

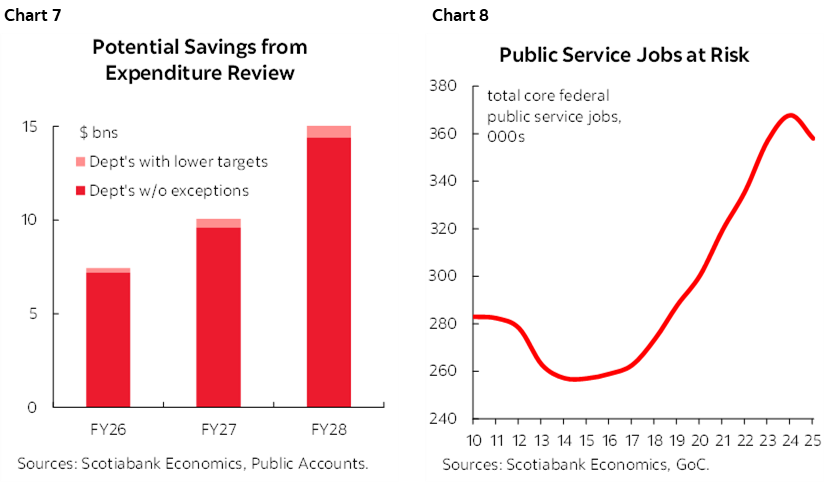

Expenditure restraint plans are ambitious but credible. Mandated departmental savings proposals (starting at 7.5% in FY27 and rising to 15% by FY29) would be consistent with the platform pledge that could return close to $15 bn in annual spending reductions by the third year and are likely to be booked in this budget (chart 7). The government’s resolve was affirmed in the Prime Minister’s pre-budget speech where he invoked sacrifice of “the things we want” for “the things we need”. This would likely entail both program cuts as well as headcount attrition where numbers had escalated in recent years and account for just over half of federal operating expenses (chart 8).

Finally, the budget is expected to include a new immigration plan. Last year’s plan called for modestly lower permanent resident targets, an attrition target for non permanent residents in the country, and a long list of program changes affecting both. By the government’s math, population growth should have stalled this year and next before returning to modest growth in 2027 (chart 9). Our forecast—and the Bank of Canada’s—bakes in execution risk by assuming a slower deceleration consistent with data so far (chart 10). We’ll be watching for tweaks that could alter that path and, indirectly, the fiscal outlook.

SPECULATIVE SLOPE

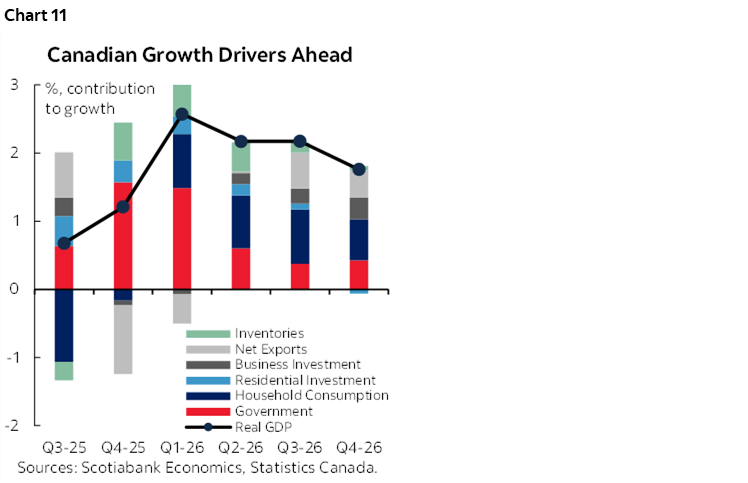

It is a mug’s game to predict how much larger deficits and debt might be in the budget. Softer near-term growth and serious structural headwinds over the medium term give the government some economic cover to run looser fiscal policy. The Bank of Canada has rightly handed off the adjustment to fiscal authorities. Our forecast already bakes in an annual fiscal lift of ~0.5% of GDP in greater public infrastructure investment over the horizon, broadly in line with what’s been announced to-date with government spending expected to provide most of the lift in Canada’s growth profile ahead (chart 11). We see upside revision risk with this budget but will approach it with a healthy dose of realism as infrastructure spending is notorious for cost overruns and implementation delays.

We speculate that the budget could test the waters with a fiscal plan that ‘just’ stabilises the net debt trajectory at a modestly higher level over the horizon. With low conviction, we sketch a debt path that rises into 2027—at roughly 2 ppts higher than today—before leveling off at around 44% of GDP over the horizon (versus an estimated 41.7% in FY25). For reference, the Liberal platform penciled in peak-debt at 42.7% by 2027 before edging down modestly over the five-year planning horizon.

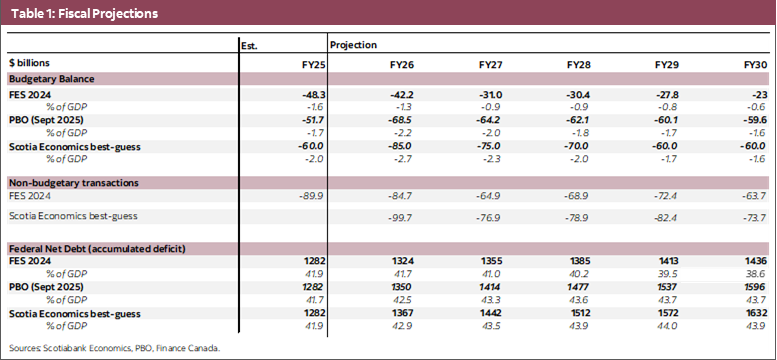

On this math, fiscal firepower is front loaded but still leaves some room for follow-on measures. Deficits could amount to about $85 bn this year (2.7% of GDP in FY26) and roughly $75 bn (2.3%) next year, then drift toward the mid- to high-1% range over the horizon. This is $182 bn higher than the PBO’s pre-election baseline (FY26–30) and almost $200 bn higher than the previous government’s last fiscal update in December 2024. (See table 1, below.)

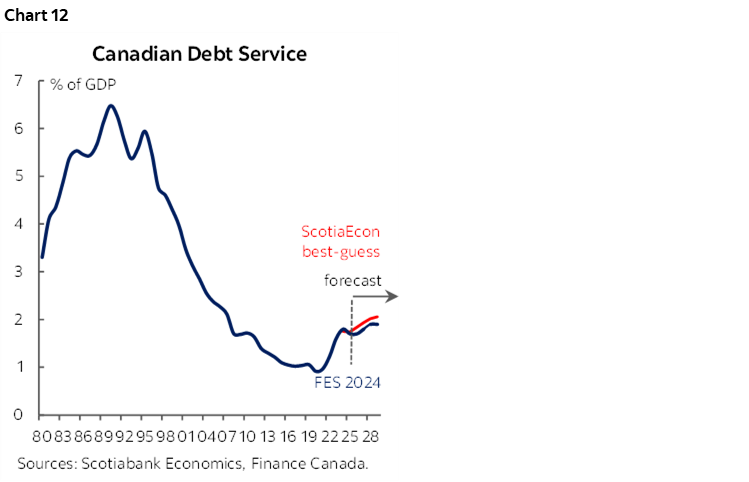

Under this profile, debt service would likely tick up modestly over the horizon. Debt service charges likely amounted to almost $54 bn last fiscal year (FY25) or 1.8% of GDP so the federal government likely ran a modestly positive primary surplus pending Public Accounts details. This could grow to $75 bn (2.1% of GDP) over the horizon—low by historic standards but directionally uncomfortable—especially as these estimates are based on a relatively benign rate outlook (chart 12).

Admittedly, we arrive at this profile largely by triangulation. The federal government aims for an ambitious investment plan anchored in aggressive-but-still-plausible timelines, while not spooking markets with a potentially spiralling debt trajectory. We also expect they would want a framework that could accommodate some modest (additional) economic deterioration, while also reserving space for at least one more budget plan.

Importantly, the government has other fiscal tools it can leverage towards its end goals that—if executed well—would not contribute to deficit and debt loads to the same degree.

THE FINE PRINT

Ottawa can scale its ambitions well-beyond the printed deficit by leaning on other parts of the federal balance sheet. Major projects can be financed through loans, guarantees, equity stakes or other innovative mechanisms—often through Crown vehicles—with an asset backing the financial arrangement even though any upfront cash requirements require higher borrowing in the near-term. Also, capital purchases such as military equipment are booked as non-financial assets and expensed (i.e., amortized) gradually under accrual accounting. Only a fraction of these costs hit the deficit each year, even though Ottawa still has to borrow upfront.

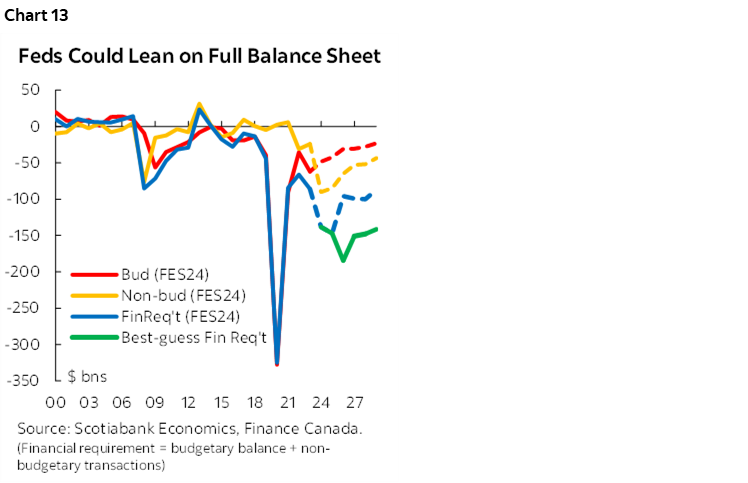

These items would appear as “non-budgetary transactions”. Normally these are muted outside crisis periods because most large economic Crown corporations are expected to be financially self-sufficient, but the Fall Economic Statement still projected them to add roughly $80–90 bn to gross borrowing needs this year and next before easing into a $60–70 bn corridor (chart 13). As a baseline, we guesstimate this budget could add another ~$15 bn this year and ~$10–12 bn in subsequent years. These sums are smaller than the projected deficit increases, but it’s not an apples-to-apples comparison as non-budgetary items can carry higher leverage and more crowd-in potential.

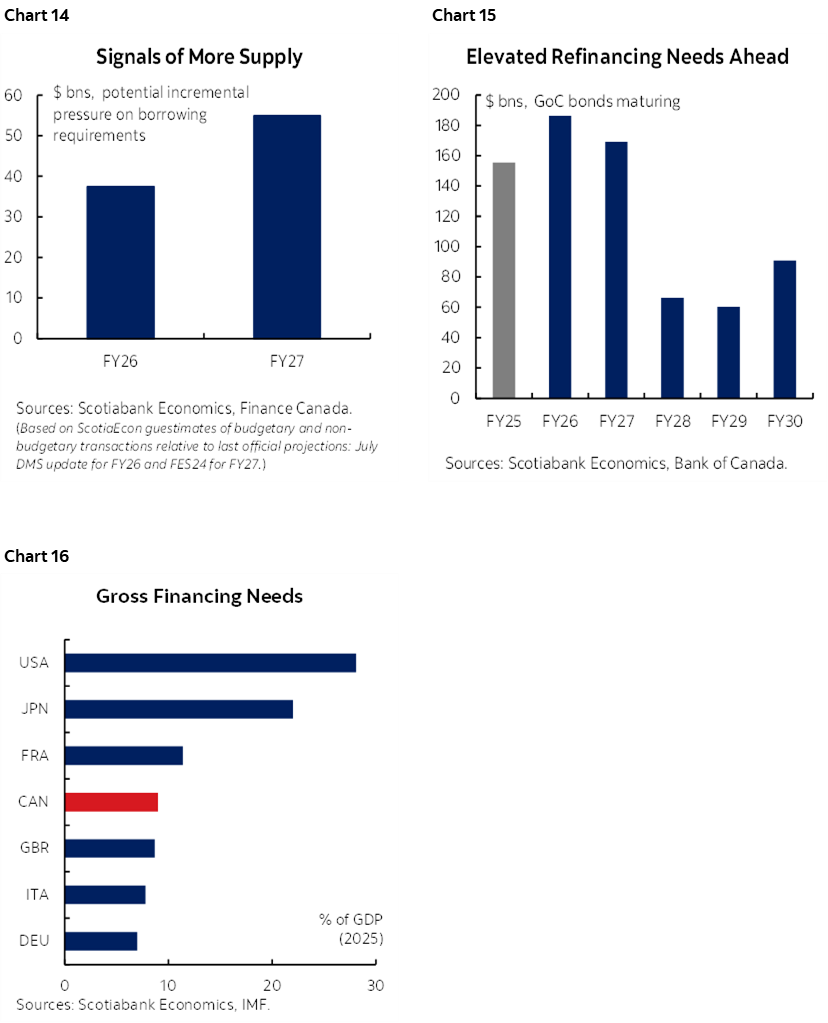

The net impact for bond markets could materially add to supply at a moment when refinancing needs remain elevated (charts 14 & 15). With issuance rising and demand uncertain, especially at longer maturities, a potential supply-demand imbalance could amplify duration risk. Canada’s gross financing needs (general government) as a share of GDP are mostly middling but without the protections of reserve currency status (chart 16). In a small open economy like Canada, these dynamics heighten sensitivity to external shocks and underscore the importance of credible fiscal signaling to anchor demand.

NO WAY BUT FORWARD

A fiscal regime change is underway. The operating budget framework should force discipline on program spending and headcount and explicitly calls for “sacrifice”. The new capital budget, by contrast, is designed to spend—but with broad definitions and a promised “results-oriented” test that will take time to prove out. The credibility test is whether they commit not just to measuring outcomes, but to being held to them.

The path forward is narrow but non-negotiable. Canada’s model of ever-rising current consumption is unsustainable, especially under a new global regime increasingly dictated by US policy. Simply priming near-term demand without fixing structural issues would leave Canada looking more like its low-growth European peers, mirroring the fiscal drift and subdued growth outlook that now defines much of that continent. On the other hand, across-the-board austerity would weaken the country now and leave it less prepared for whatever is coming.

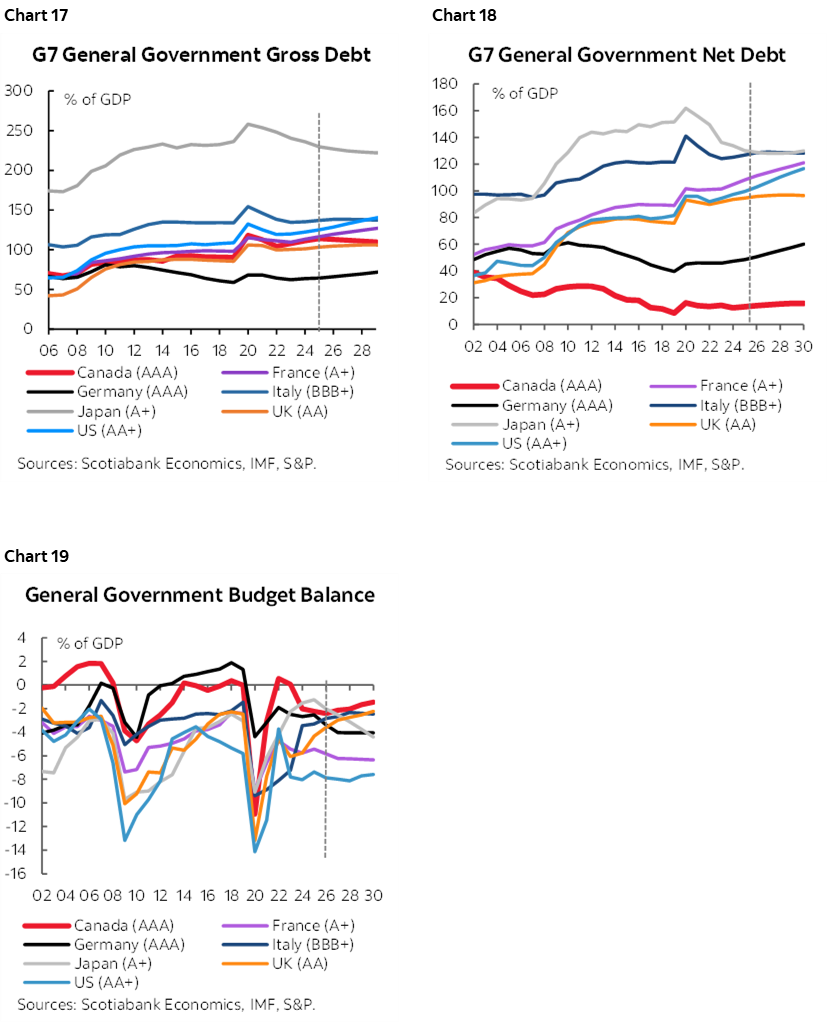

Markets are unlikely to parse every line item in the budget. What they will see is a government that is trying to rotate its economy from consumption to supply by leveraging its relatively healthy balance sheets. That composition usually earns more tolerance for deficit-financed activity, particularly when the debt path eventually bends down. Canada’s net and gross debt positions relative to peers are not alarming, if not attractive, but it lacks reserve status of some and middling liquidity limits near-term comforts (charts 17–19). And we’ve not yet seen provincial budgets where some of the larger provinces are most acutely impacted by current tariffs that will impact their bottom lines too.

The near-term backdrop is unforgiving. Canada’s deep exposure to US trade and security policy coincides with tariff risk, bilateral tensions, and looming CUSMA renewal. A Canada-U.S. détente could be announced—or unravel—at any moment. Any surprise from Washington would likely overshadow a budget narrative built on a long-horizon strategy. In this climate, volatility trades loud—and whether the news is good or bad, Canada’s vulnerability to US policy whims could dominate the story for now.

Patience coupled with disciplined risk-taking may be the best bet in the long run for Canadians.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.