- Canada’s Finance Minister Champagne tabled a much-hyped budget on November 4th. The plan sets out a substantive investment agenda paired with operational restraint as the Carney government attempts to rebuild the country’s productive capacity in the face of existential shocks.

- The final price tag for new spending in Budget 2025 comes in at a hefty $90 bn ($149 bn in gross outlays offset by $60 bn in savings measures). Items already legislated since taking office add another $36 bn, while a weaker economic outlook accounts for a further $42 bn deterioration in the fiscal outlook.

- Key measures include a ramp-up in military spending, a new infrastructure fund, as well as a slew of previously announced measures including those related to trade relief and diversification measures. Housing and affordability measures are features but mostly repeat earlier tax cuts and housing announcements. The budget also moves forward with public sector and program spending cuts to offset new spending.

- The budget also leans on off-balance sheet measures to support higher lending through Crown corporations as well as capital acquisition that combined add an incremental $29 bn to financial requirements over the horizon.

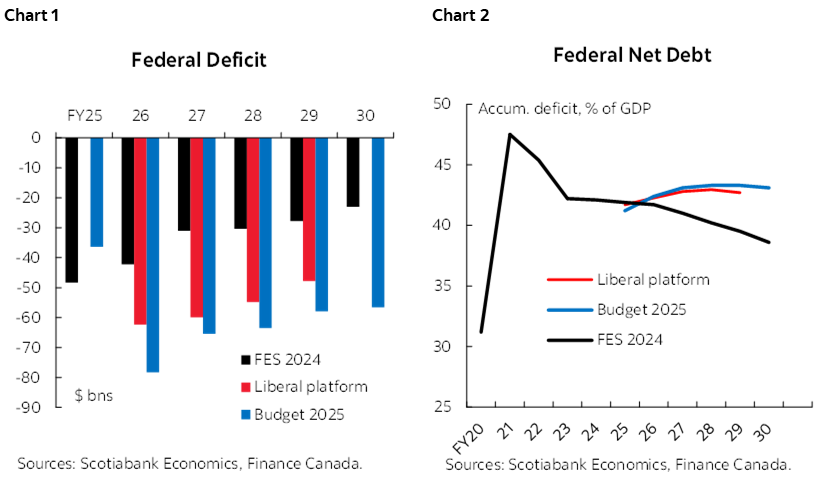

- The government is projecting a series of larger deficits that would peak this year at 2.5% of GDP ($78.3 bn), 2% next year ($65.4 bn), before descending to 1.5% by FY30. This would push net debt up by 1.9 ppts over the horizon to a peak of 43.3% of GDP in FY28 where it would largely stabilize. A declining deficit as a share of GDP over the horizon is confirmed as an anchor in the budget, along with the commitment to balance the operational budget within three years.

- Incremental investment related to infrastructure and public investment adds ~0.3% of GDP annually over the horizon which is largely in line with expectations—if not marginally on the low side but total incremental annual outlays amount to closer to ~0.9% of GDP (before factoring in public sector cuts).

- On net, it’s not clear this would result in an incremental boost to growth given much is already baked into forecasts already, and plans comes with considerable execution risk still.

- All this unfolds against a backdrop of global volatility, where unpredictability is the norm. Canada’s fiscal footing is relatively solid, but its deep ties to US policy mean the budget’s long-term strategy could be buffeted by the news cycle.

- The sleeper risk may be closer to home. The budget asks Canadians to wait for long-term payoffs while managing short-term sacrifices. It will take more than one budget cycle to see results.

- It may be the type of budget Canada needs—but the government still has to convince Canadians it’s the one they want if they hope to catalyze investment.

OPENING THE BOOK

The federal government delivered a big-swing budget on November 4th but may have mismanaged expectations going into budget day. Expectations were high, but the plan mostly delivered on policy proposals that had been channeled if not already tabled. This may leave some pointing to a lack of ‘transformation’ but judging by numbers alone, the $149 bn spending plan is substantial (chart 3).

The Carney government had earlier stated his ambitions of unlocking half a trillion in investment over the next five years—this has been upgraded to a trillion dollars. The math is fuzzy and comes with a host of caveats and cautions—not the least implementation risk—but the budget removes one important one in putting dollars behind promises. The real transformation would come from leverage—only time will tell how effective the plan will be given the host of headwinds impacting business investment in today’s environment.

Look through political posturing in the budget’s aftermath. The minority government will require support (or at least abstention) from others to pass this budget when it is put to vote on November 17th, but we don’t think Canadians will be sent back to the ballot box just yet. Polling suggests the outcome would not likely be that different, but the country would lose precious time in a fast-evolving environment where inertia is a vulnerability.

BACK TO REALITY

A weaker economy provides the impetus and opening to invest at scale. The budget lands in a volatile, uncertain environment with structurally slower growth ahead against trade tensions and pervasive uncertainty. The plan is costed on a path of just 1.1% and 1.2% GDP growth this year and next, respectively. As slack continues to build, there is a solid case for the mostly supply-side investment plan outlined in Budget 2025. With the Bank of Canada rightly sidelined for now, only fiscal policy can shift the Canadian economy onto firmer growth footing over the medium term.

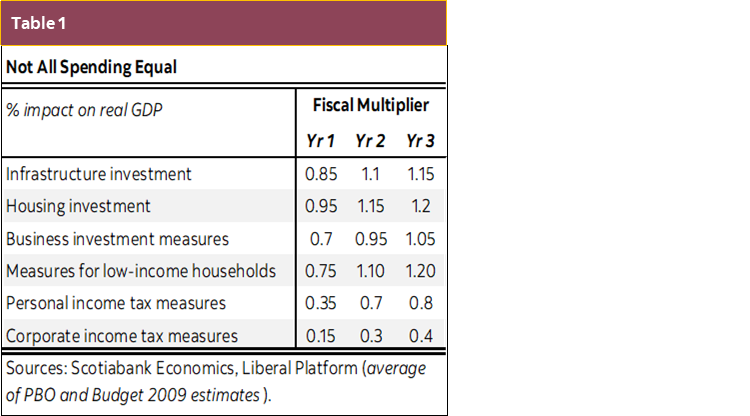

The plan should be growth supportive. Our baseline had already assumed ~0.5% of GDP annually in public investment over the horizon based on earlier signals. Budget 2025 offers an incremental ~0.3% of GDP in capital investment over the horizon but total gross outlays add ~0.9% of GDP—before folding in government expenditure cuts. Rule-of-thumb multipliers suggest investment measures could yield more than a dollar-for-dollar boost, amplified in today’s softer economic conditions (table 1). Importantly, but harder to measure, the plan continues to tackle policy and regulatory barriers that should tip the balance towards greater investment all else equal.

We will have to weigh these factors against near-term headwinds from a tighter immigration path, but on net, a healthy dose of pragmatism is warranted. The plan mostly underpins upside risk to growth (and reinforces our rate outlook that Bank of Canada may need to take its policy rate back to neutral later next year) but it doesn’t leave us rushing to upgrade our baseline just yet.

DIVING INTO THE MIDDLE CHAPTERS

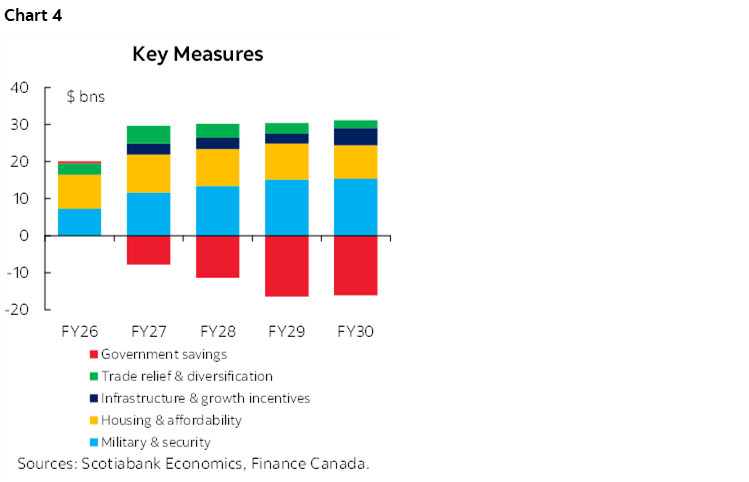

The budget’s overarching theme is an investment-first push. Broadly, it sets out details on accelerating infrastructure and nation building projects, restoring Canada's military capacity, tackling housing and affordability challenges, bolstering (and transitioning) hard-hit sectors, and reorienting other policies including climate and immigration around its growth agenda. While an imprecise metric, spending is mostly aligned with these supply-side priorities (chart 4). (It is challenging, at least at first glance, in teasing out what is truly incremental as many of the measures rolled up in each chapter had already been announced.)

The biggest outlays accrue to restoring military capacity. The budget reaffirmed the-near term path to meet NATO’s 2% spending benchmark this year and providing further investments on a path “towards” its 2035 commitment of 5% of GDP (3% military, 1.5% related. The budget announces another $56.6 bn ($81.8 bn cash basis) over the next five years (but includes earlier-announcements) allocated to wages and capital expenditures. There will also be a new a Defence Industrial Strategy, coupled with the already-announced Defence Investment Agency, to deliver the larger mandate. The budget does not yet give details on a broader financing framework to understand the details.

Infrastructure receives a major boost in the budget. The signature measure is a $51 bn (10-yr) Build Communities Strong Fund to support wide-ranging provincial and municipal infrastructure projects but it repurposes other existing programs (Canada Community-Building Fund, Canada Housing Infrastructure Fund) so the net fiscal impact is more modest ($9 bn over 5 years).

Further foundations are set to unlock major projects on national interest. The new Major Projects Office is mandated to help structure and coordinate financing through the Canada Infrastructure Bank, Canada Growth Fund, and the Canada Indigenous Loan Guarantee Program under a new strategic financing framework. The CIB will be capitalized with another $10 bn (to $45 bn) to further its capacity to support major projects.

There’s no pipeline—for those that were holding their breath—but an otherwise vague climate competitive strategy that hints are making the oil and gas sector emissions cap “redundant” and plans to strengthen the industrial carbon emissions scheme (that is important to making the math work on carbon capture and storage infrastructure.

Hopes around corporate tax competitiveness were likely over-hyped. The budget adds a Productivity Super-Deduction ($1.5 bn, 5 years) that will provide a set of enhanced tax incentives covering all new capital investment to compliment existing tax investment incentives. The budget otherwise reaffirms intentions to move forward with earlier-announced changes including the reinstatement of the Accelerated Investment Incentive, immediate expensing for manufacturing, clean energy, productivity-enhancing assets, and R&D. The government’s estimates suggest the new super-deduction would bring the METR to 13.2% (from 15.6%) and below the 17.6% in the US (albeit with wide variations across sectors). There was no promised corporate tax review and the Minister appeared to walk back from one in the post-budget media scrum.

Housing and affordability is a red herring. It appears substantive at first glance but over half of the $48 bn (5-year) outlay reflects the already-implemented personal income tax cut ($27 bn), Build Canada Homes ($7 bn), the GST elimination on new homes for first-time homebuyers, and the cancellations of the consumer carbon tax. Otherwise, some modest measures related to personal support workers (channeled ahead) and youth work programs are additional.

CUTS COMING (FOR OPERATIONAL SPENDING)

The government is proceeding with well-channeled expenditure reduction plans. The budget books $13 bn in savings annually by FY29 and ongoing thereafter for a 5-year savings of almost $60 bn. These will be achieved through a reduction in headcount—by about 10%—from an FY24 peak of 368 k to 330 k by FY29 (annual attrition is about 10–12 k). Minimal detail was provided on specific program cuts but examples and departmental savings are listed in annexed chapters. Overall, growth in operating expenses is expected to decline from above 8% growth to under 1%.

CUTS CONTINUING (FOR IMMIGRATION)

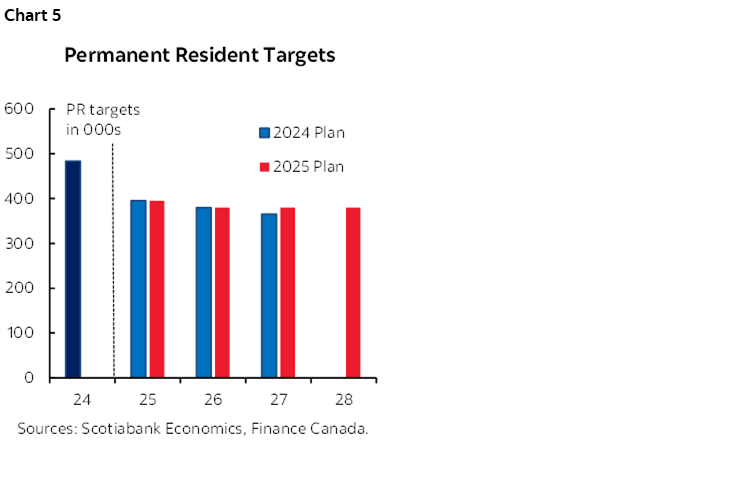

The new immigration plan continues the path of decelerating population growth. The rolling three-year permanent resident targets are frozen at planned 2026 levels (380k) and down from the 395k in 2025 (chart 5). The share of economic immigrants is set higher at 64% versus an earlier 59%. Meanwhile, temporary resident admissions are scaled back materially: 385k, 370k and 370 k over the next three years) that would bring the government on track to achieve its restated attrition target to bring temporary residents to 5% of the population by 2027. A new International Talent Attraction Strategy and Action Plan—with $1.7 bn funding—will aim to attract talent in support of its innovation and growth agenda.

While the net numbers likely pull population growth close to stall speed over the next two years, the stronger focus on economic impact likely offsets some of the impact—if implemented—as population growth has decelerated but not yet at the pace consistent with these targets. Further details will be tabled by the Immigration Minister.

BACK OF THE BUDGET

There is a lot of red ink in this budget. The plan books a net $167 bn fiscal deterioration over five years (FY26–30) relative to the last official update in December’s Fall Economic Statement. This includes $42 bn in economic and fiscal developments owing to a weaker growth outlook, $36 bn in outlays announced prior to the budget, and another $149 bn in gross new spending, offset by $60 bn in new revenues or savings.

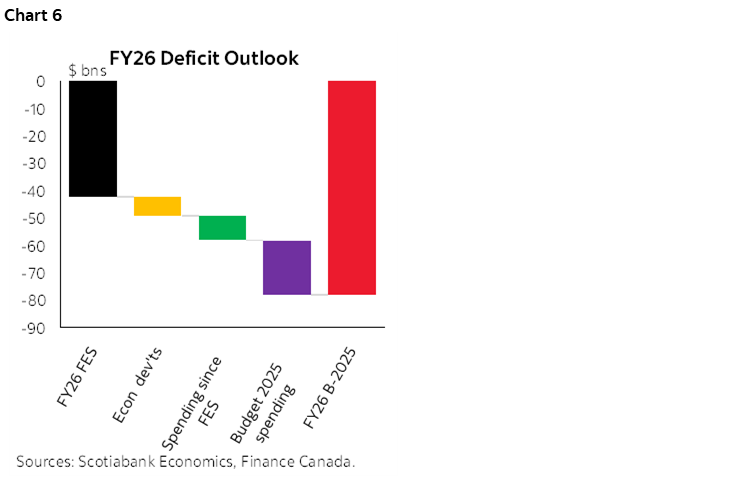

The current year alone is expected to drive a deficit of $78 bn (2.5% of GDP)—$36 bn higher than projected last Fall. While weaker economic conditions account for part of the slippage, new policy measures are the primary driver (chart 6). The latter includes earlier-legislated $9 bn, plus $20 bn announced in today’s budget.

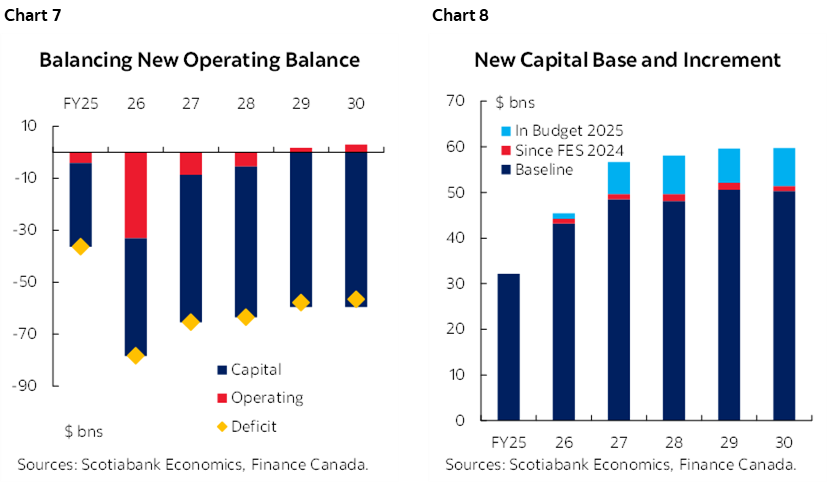

The government plans to run a string of deficits declining modestly over the horizon. A $64 bn (2.0% of GDP) deficit is penciled in for FY27 before settling at $57 bn (1.5% of GDP) by FY30. As promised, the new capital-operating split shows a path to balance for operational spending by FY29 (chart 7). Recall, investment has been defined as outlays that create assets—asset-creation on government or others’ balance sheets ranging from traditionally-defined capital expenditures to more discretionary tools like tax incentives, housing supports, and conditional transfers. Those are expected to nearly double over the horizon, but more than half of that increase had already been planned (chart 8).

Net debt is expected to rise over the next three years before ‘just’ stabilizing over the horizon. The debt trajectory is expected to rise through FY29—1.9 ppts higher than today—before leveling off at around 43.3 % of GDP over the horizon (versus an estimated 41.7% in FY25). The budget sets its fiscal anchors as a declining deficit-to-GDP ratio over the horizon as its fiscal anchor, along with balancing its operating balance. The formal is unusual—and could in theory still drive higher debt trajectories but for now that slope is largely horizontal.

The current fiscal profile would drive an uptick in debt charges with servicing costs growing from $53.4 bn in FY25 (1.7% of GDP) to $76 bn (2.1% of GDP) over the horizon—low by historic standards but directionally uncomfortable—especially as these estimates are based on a relatively benign rate outlook with private sector economist expectations for the 10-year GoC yield hovering about ~3.5% over the horizon (chart 9).

ANNEXES GET INTERESTING

The government plans to leverage other parts of its balance sheet to backstop its plan. Non-budgetary transactions (NBTs) are generally a relatively low pressure on financing needs outside crises, but these had ticked up, notably through “loans, investments, and advances” to Crown corporations. (NBTs also capture the difference between cash outlays required for the acquisition of capital assets and the amortization of capital assets included in the budgetary balance.) This line item is projected to add an incremental $29 bn to financing needs through FY30 relative to those projected last Fall.

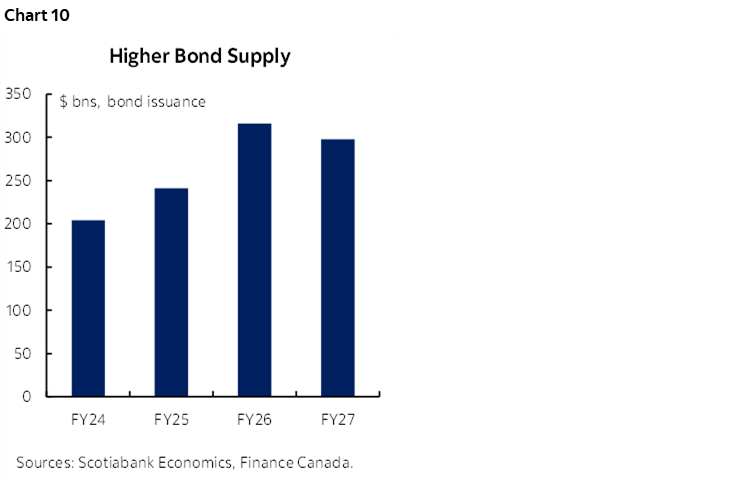

The net impact for bond markets adds to supply at a moment when refinancing needs remain elevated. Borrowing plans for FY26 were unchanged—with $316 bn in bond issuance expected against total borrowing of $614 bn. The budget has provided FY27 borrowing plans as well with an anticipated borrowing of $594 bn—including $298 bn—a modest step-down from FY26 activity (chart 10) but still a long way off—and another budget in between. The FY27 plan would modestly extend the duration (with 35% in long bonds) and a modestly higher share in liquidity (T-bill share at 49%).

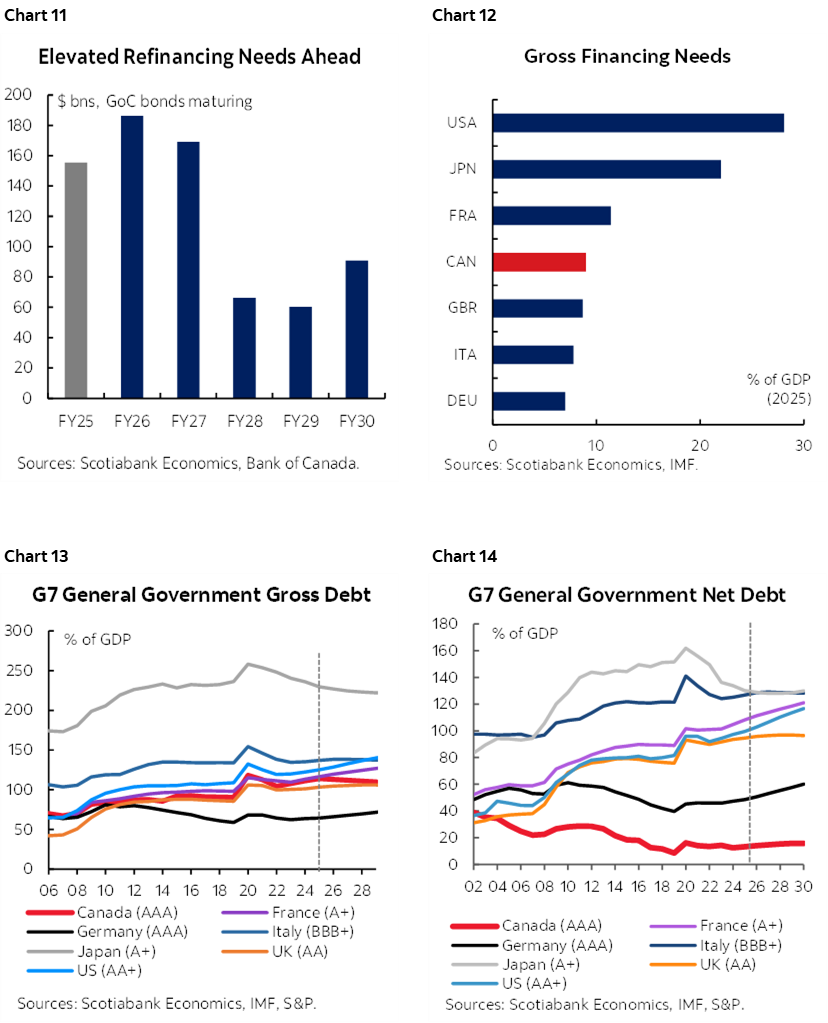

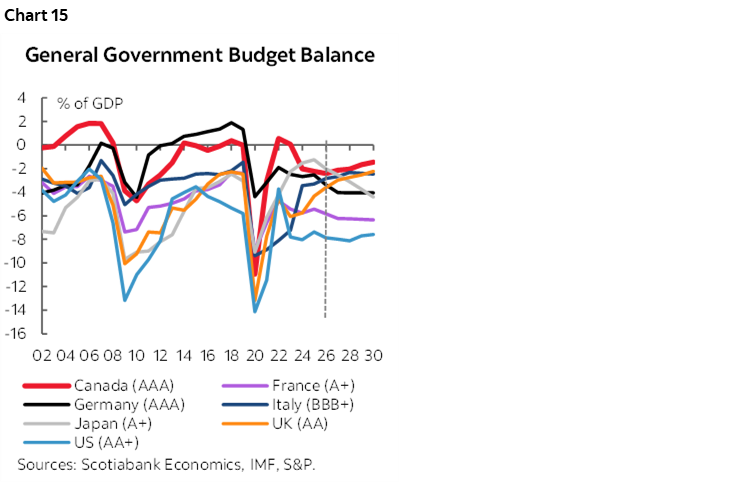

Canada will be raising capital in a volatile market environment. With issuance rising and demand uncertain, especially at longer maturities, a potential supply-demand imbalance could amplify duration risk. Canada’s fiscal position across a range of metrics (gross and net debt, primary balance, and gross financing needs is middling to outright favourable, but it doesn't have the safeguards of reserve currency status (charts 11–15). The composition of Budget 2025 spending should be viewed favourably in isolation but its deep exposure to US policy whim could overshadow the budget’s long-run narrative depending on the surrounding news cycle—in either direction. The durability of the longer play hinges on delivering against this ambitious agenda.

TAKE AWAYS

Budget 2025 should help reset Canada’s economic course with a necessary pivot from consumption to capacity. It’s a credible strategy for a weaker, supply-constrained economy—but delivery is everything and execution risks loom large. The government may have over-hyped ‘transformational’ as the real test will be results that will take time and this is a start.

In a world of deficit-heavy peers, composition—not size—should anchor confidence. Canada’s fundamentals are decent, but its exposure to US policy risk is acute. Tariffs, trade tensions, and CUSMA uncertainty could derail the long game, especially with some of the largest provinces bearing the brunt of sector-specific shocks. The government rightly keep its debt trajectory stable over the horizon as this is not an environment to test market confidence.

But whether the budget Canadians—or Parliament—want remains to be seen. In the near term, Canadians may miss the immediacy of transfer-heavy budgets as there is nothing ‘new’ for households in the budget, while the government asks for patience. This budget is likely to pass but Canadians (and investors) will want to see results soon.

The risk may be a return to complacency—underestimating the volatility ahead and overestimating how long the fiscal runway will hold.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.