- Canadians head to the polls on April 28th. The Liberal Party under its recently-minted Prime Minister Mark Carney is polling in majority territory though the chance of a minority government is not completely off the table.

- Trade (and other) tensions with the US have preoccupied voters’ minds as some of the usual hot buttons—like immigration and the environment—have taken a backseat, while others—like affordability and housing—remain at the fore.

- Both leading parties—the Liberals and Conservatives1—have made hefty promises on the campaign trail with gross new spending commitments of $129 bn and $110 bn, respectively, over a 4-year mandate.

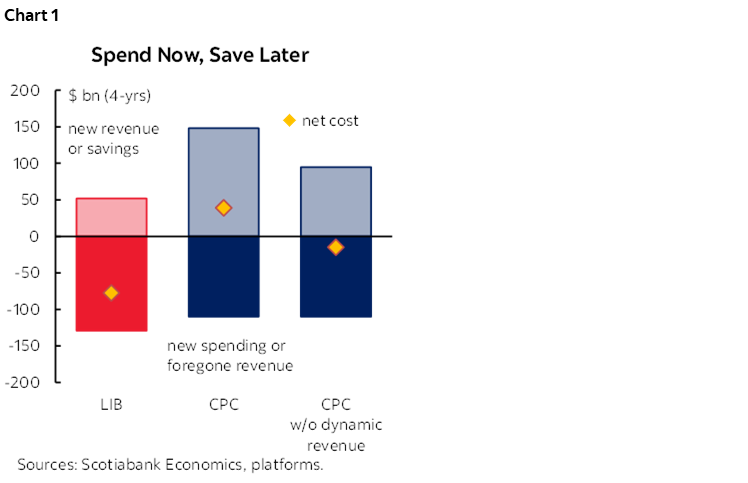

- Savings & revenue plans are somewhat dubious. The Tories’ plan projects savings of $148 bn—$41 bn in excess of spending plans. But over a third of the offset comes from dynamic scoring of estimated revenue gains from growth. Excluding these for comparability, the net shortfall lands at $15 bn (chart 1).

- The Liberal plan, which does not include dynamic revenue gains, offers a partial $52 bn offset for a net platform cost of $83 bn (after debt charges). Both plans bank on substantial savings from efficiencies, in addition to tariff revenues, and warrant a healthy dose of caution.

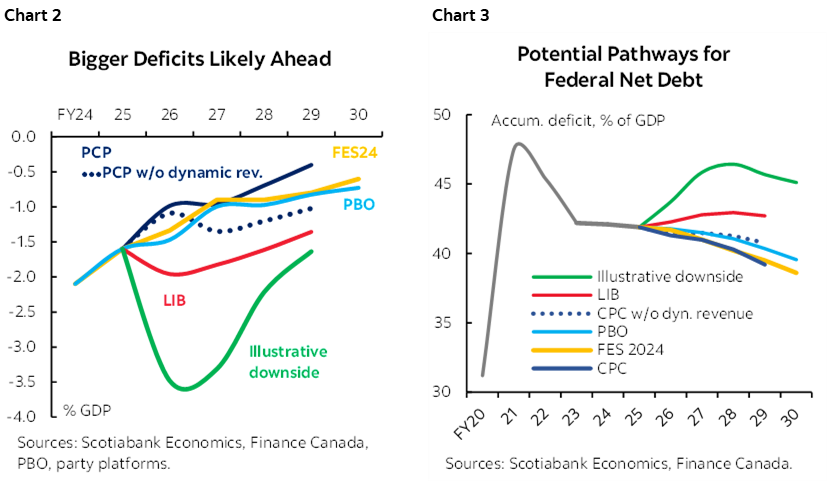

- Neither party is running on fiscal austerity. The Conservatives would run deficits marginally tighter than the pre-election baseline over the horizon—if you accept the dynamic revenue scoring—or slightly wider otherwise. The Liberals would add north of 0.5% of GDP to net new spending annually, while balancing a new ‘operating’ budget over the medium term. Neither platform accounts for a potential tariff-induced recession—or even a slowdown for that matter—that could easily tilt deficit and debt projections materially back up as a share of GDP (charts 2 & 3).

- Both parties promote a growth agenda with emphasis on scaling up investment in the resource sector, while the Liberals couple this with scaled-up public infrastructure investment (adding about ~0.75% of GDP annually in capital-related investments to the fiscal plan). A complicated jurisdictional and institutional landscape means the next leader would have his work cut out to deliver on these important pledges.

- The distance between pledge and policy can be wide. Some policies across a range of issues—if enacted—may have sector- or region-specific implications, but exogenous market forces are mostly dominating headlines in the near-term.

- Most drivers—global and domestic—are at least directionally suggestive of potentially weaker growth and higher borrowing into a dearer landscape. Solid fundamentals may not offer much of a safe harbour for Canada right now, but weaker ones could make it worse. The next Leader does not likely have a wide margin for policy missteps.

- With relatively stable polling in recent weeks and fiscal activism well-channeled, expected election outcomes likely lean against any urgency to cut the overnight rate consistent with our most recent economic outlook. Otherwise, watch for the risk of a minority government that could stall decisive action very much needed right now.

CIVIC PRIVILEGE

Canadians will elect the country’s 45th government on April 28th. The Liberal-led incumbent government put a new man at the helm only weeks ago as Justin Trudeau stepped down in early March. Prime Minister Mark Carney called an election within days of taking office, otherwise facing an inevitable vote of no-confidence as support for the minority government had eroded months earlier. Since then, Liberal prospects have turned remarkably brighter.

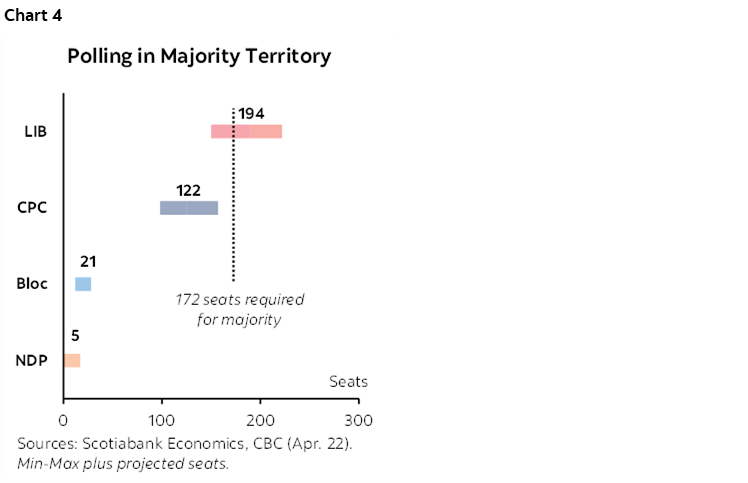

Most pundits now put money on a Liberal win. Less than a week out, polls point to a likely majority outcome—or at least 172 of the 343 seats in Parliament—with probabilities in the order of 4-in-5 (chart 4). The Conservatives hold only a tail chance of forming the next government. The balance of probabilities point to a not-immaterial risk of a minority government (~13% according to this poll).

The next government is expected to hit the ground running. A Speech from the Throne could follow within days, setting out the new government’s agenda for the next Parliament. A budget could follow within weeks to set in motion some of the most pressing priorities. A minority win could stall those timelines as coalition-building (formal or otherwise) would be tricky given other parties are trailing substantially in this two-horse race.

PRIORITIES, PERCEPTIONS & POLITICS

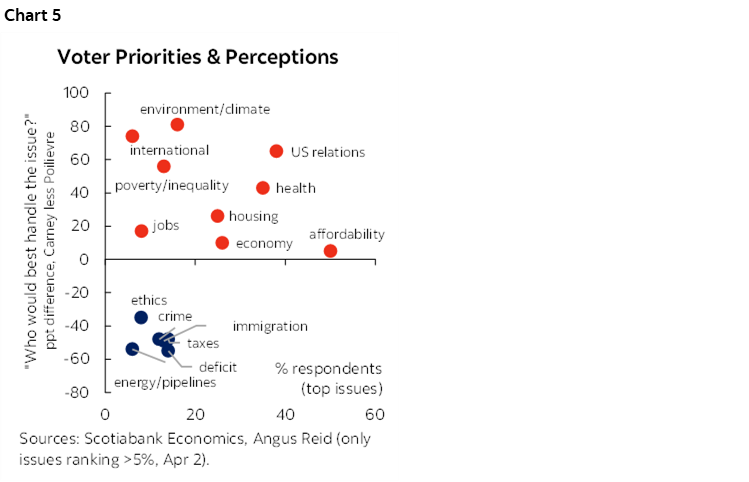

Geopolitical developments south of the border have rapidly reordered voter concerns. Against persistent trade threats and even annexation overtures, relations with the US are top of mind for many Canadians. The cost of living is still very much a concern, along with the usual healthcare and housing pressures. The imperative of economic growth has been rekindled while issues such as immigration, climate and deficits take a back-seat (chart 5).

US President Trump has deferred trade negotiations with Canada until after the elections. On paper, trade positions of both candidates are similar: a dual-focus of strategic negotiations along with domestic reforms. Both support targeted counter tariffs, coupled with a stronger internal trade agenda, trade diversification and sector-specific supports. Both plans bank on tariff revenues—each at $20 bn this year—to offset other spending pressures. Neither party pencils in broader stimulus support in the event of a full-blown trade war and the rather benign pre-election economic baseline mostly predates recent developments.

It’s anyone’s guess if it matters who is in the negotiator’s seat. Angus Reid polling puts Carney’s perceived potential to deal with US turmoil well-ahead of the Conservative Leader Pierre Poilievre but other countries’ experience so far shows little rhyme or reason to tactics.

REVYING THE ENGINES

Canada’s best insurance is doubling down on stronger growth, productivity and competitiveness and both parties set the aspirational bar high. The Conservatives pledge to lift output by half a trillion dollars over five years, suggestive of real GDP growth in the ballpark of 4% annually (and ~3% per capita). The Liberals stop short of setting a top line target but point to an expected mobilization of half a trillion dollars in new investment (public and private) over the next five years. This would be broadly consistent (if not also on the high side) of our earlier pitch for 2% per capita GDP growth target. Our latest economic outlook currently puts the Canadian economy on a path well-short of either of these ambitions even as we have penciled in some fiscal response already against a weaker growth outlook.

Both parties would unlock stronger growth via major infrastructure and resource development, but each differs in approach. There are a surprising number of similarities in slogans at least as each vows to improve the investment landscape: the Liberals with a “One Stop Shop” and a “critical infrastructure corridor” and the Conservatives with “One Window” and a “national energy corridor” to streamline approvals and fast-track development. Otherwise (and at the risk of gross over-simplification), the Liberals would lean on the public balance sheet to crowd in private capital, while the Conservatives would reduce the government’s footprint to achieve similar goals.

A complicated jurisdictional landscape, compounded now by global uncertainties, means either party would have its work cut out to spur greater investment.

SPEND NOW...

Both parties have made enormous spending (or “investment”) pledges—exceeding the $100 bn mark—even if their presentation obscures easy comparison. For ease of reference, we bucket measures into “spending”: any measure that adds to fiscal costs, e.g., new programs, foregone revenue from cutting taxes, etc.). We categorize “savings” as any measure that reduces fiscal pressures (e.g., cutting programs, finding savings or efficiencies, etc.). The Conservative platform also includes estimates of dynamic revenues from policy changes, that is, additional revenues that are expected from stronger investment or economic activity. The Liberal platform does not include these potential gains. These are notoriously challenging to estimate especially in a highly uncertain environment. We present the Conservative plan with and without dynamic revenue estimates for comparability.

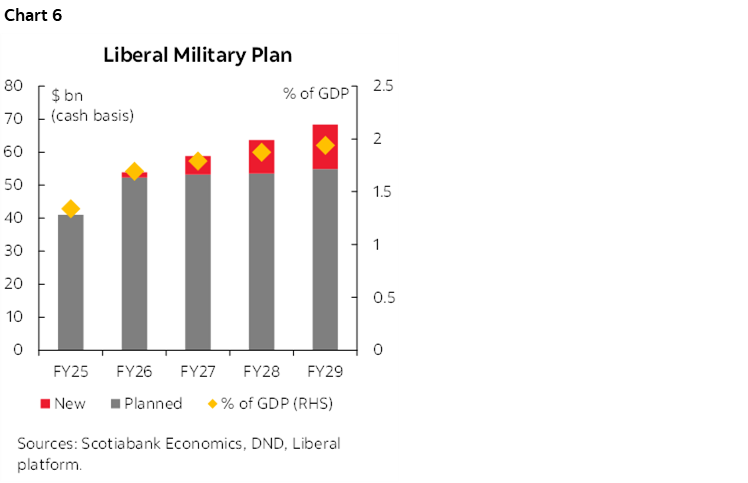

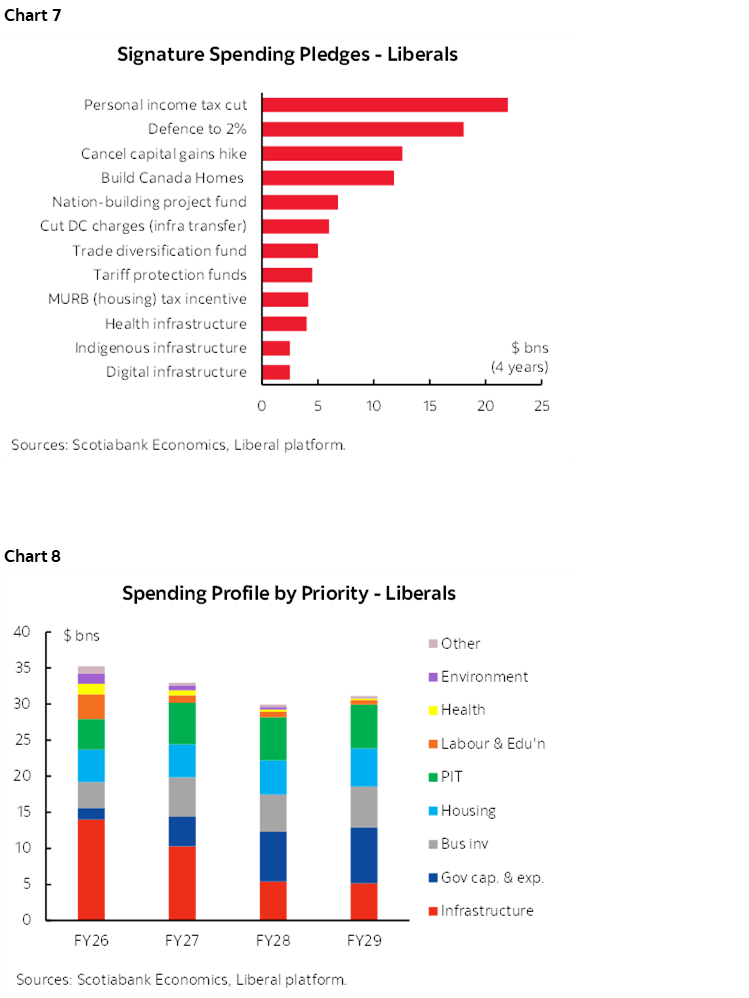

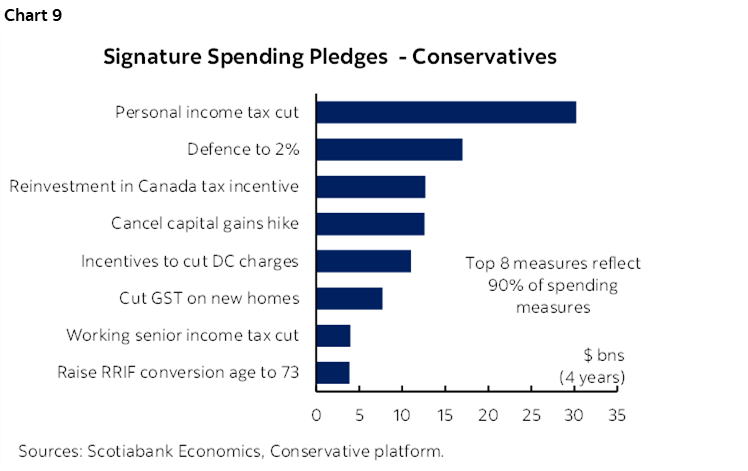

The Liberals are running on a $129 bn (gross) spending plan. Their signature measure—a 1 ppt tax cut to the bottom personal income bracket to 14%—was announced in the early days of the election and is costed at $22 bn over four years. This is followed by a ramp-up in military spending ($18 bn in accrual terms or $31 bn cash) to achieve the 2% NATO target by 2030 (chart 6). The already-announced cancellation of the hike in the capital gains inclusion rate takes third place at almost $13 bn, followed by $12 bn to expand affordable housing investments via a new Build Canada Homes entity that would see the government get back into homebuilding. There is about $5 bn set aside for tariff-exposed protections, otherwise the top 12 pledges comprising three-quarters of new spending are infrastructure related (chart 7). If implemented, the net effect would be some $25 bn per year (~0.75% of GDP) in public investment and/or infrastructure outlays over the horizon (chart 8).

Housing is still very much on the Liberal radar. In addition to the Build Canada Homes budget, tax incentives for multi-residential investors and GST cuts for first-time homebuyers would bring the suite of housing measures to incremental $19 bn in budgetary costs over the mandate (and a higher non-budgetary impact via expanded lending activity). We count an additional $6 bn under infrastructure funding for lower orders of government in exchange for reduced development charges. They’d also extended timelines to get to half a million new homes annually over a longer 10-year horizon, while also pledging to review mortgage markets including exploring potentially longer interest rate terms (an earlier commitment from the Fall update).

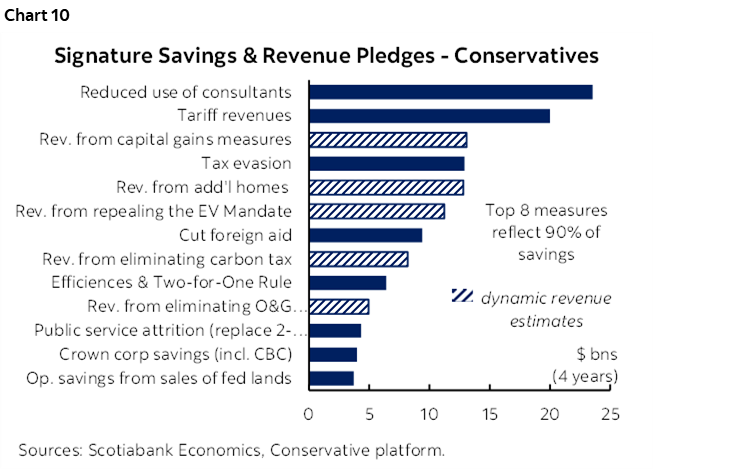

The Conservatives pitch a gross $110 bn spending plan. The party promises to reduce the bottom personal income tax bracket—much more substantially—by 2.25 ppts (to 12.75%) and is costed at $30 bn over 4 years. It also commits to meet NATO’s 2% target by 2030 for another $17 bn. Its capital gains tax deferral for reinvestment in Canada is costed at $12.7 bn, while the cancellation of the capital gains tax hike adds another $12.6 bn. Its two housing initiatives—incentives to lower development charges as well as the GST cut for new homes—combine for another $19 bn as part of a broader plan to build 2.3 mn homes over 5 years. Finally, two signature measures supporting financial security of seniors tally $7.9 bn (chart 9).

...SAVE LATER

The Liberal platform projects $52 bn in spending offsets over 4 years. This includes $20 bn in tariff revenues this year, while noting this is a placeholder for now. (The federal government currently imposes 25% tariffs on about $60 bn worth of goods from the US.) The $32 bn balance is based on “savings from increased government productivity” involving a combination of amalgamating service delivery, consolidating programs, reducing the use of external consultants, and leveraging AI. They would cap (but not cut) public service employment. The plan would cap annual direct program expense growth at 2%. After netting out these savings from the $129 bn spending plan, the platform is costed by the party at $77 bn, with incremental debt service charges bringing that to $83 bn.

The red party would balance a newly-defined ‘operating’ budget by 2028 (estimating the shortfall sits at about $15 bn today). This new measure would net out government expenditures that contribute to capital formation or “anything that builds an asset, held directly on the government’s own balance sheet, a company’s, or other order of government’s”. The plan declares that traditional measures of deficits and debt as a share of the economy would decline over time (after year 1 increases) with the net impact adding about 0.5 ppts (of GDP) to annual deficits and leaving debt almost 2.5 ppts higher after 4 years relative to the PBO’s pre-election baseline.

The Conservative plan would find a whopping $148 bn in savings and/or revenue offsets over 4 years. That number is slightly lower—at $95 bn—when dynamic revenues are netted out for comparability. These dynamic revenues are attributed to the additional growth and government revenues from the new capital gains deferral, from new homes built, and from repealing a variety of policies (the carbon tax, EV mandate, oil and gas caps, Bill C-69 and Clean Fuel Regulations). Otherwise, a reduction in the use of consultants would yield $23.5 bn, a crack-down on tax evasion another $12.9 bn, cuts to aid ($9.4 bn) and a long list of efficiencies and/or program cuts including key Liberal housing programs: the Housing Accelerator Fund and the Canada Housing Infrastructure Fund (chart 10). The party itself costs the platform at a net positive $39 bn when these savings are applied against new spending pledges. When we net out dynamic revenues, the net shortfall stands at $15 bn.

A BIGGER BOTTOM LINE

In short, fiscal expansion looks set to continue in Canada. There is no doubt a need for improved government efficiencies and productivity, but savings are notoriously difficult to achieve and transfers—to households and other orders of government—appear off the table for now. A tax review—promised by both— could eventually deliver savings, but these also take time and both parties have already given up some of the tax space that could help ease its eventual passage. Both parties’ plans warrant a healthy dose of scrutiny pending further details on execution.

Neither party plans for a potential recession. To be fair, that probably wouldn't garner votes even if there is a reasonable chance one is on the horizon. In this case, additional near-term stimulus would be needed, while automatic stabilizers would further erode the bottom line. We’ve penciled in purely for illustration how a moderate downturn could rapidly change the fiscal outlook (charts 2 & 3, again).

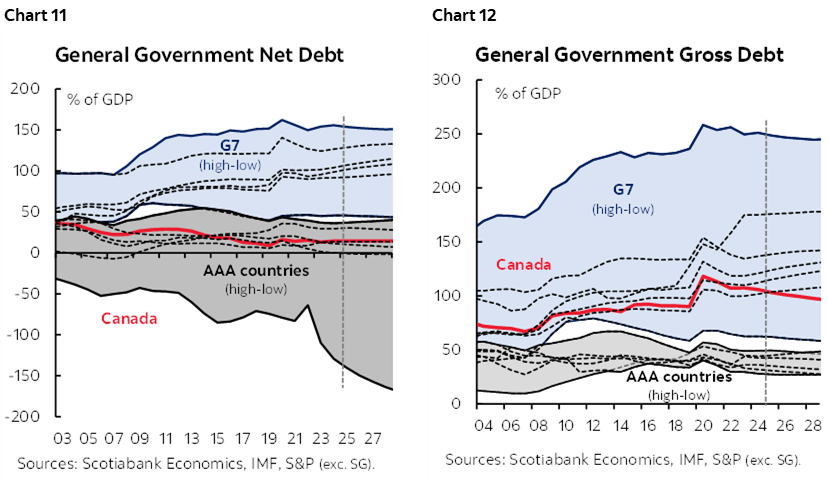

Canada’s overall debt position confers only some comfort. Its general government net debt is still positioned favourably to peers, but its gross debt—more pertinent in times of stress as a proxy for liquidity—is more middling (charts 11 & 12). Meanwhile, rating agencies have recently fired shots over the bow at a few provinces as lower orders of government provision defensively for more spending. This should serve as a reminder that the numbers across all levels of government must add up at the end of the day.

The country is also more trade-exposed than peers. This has borne out most visibly in currency markets on key tariff days. A coherent set of growth-enhancing policies could gain favour in relative bond markets, but would likely provide only a partial offset in the near term. Even though spreads between long term yields on US Treasuries and Canadas narrowed during early-April market turmoil, both sit higher as a result of US policy mayhem.

The net impact of potentially weaker growth, higher borrowing needs and a potentially higher-borrowing cost environment suggest the federal government has reduced margin for policy error.

MAY THE BEST PLAN WIN

Canada needs decisive and bold action. The country’s next leader may not have much control over policies south of the border—and frankly doesn’t have as much authority within its own boundaries as it might hope—to get all the way to another half a trillion in output or investment dollars in a highly uncertain environment. But it does have half a trillion annual spending plan and solid balance sheets at its disposal. Stronger investment begets higher productivity which should, in turn, foster greater living standards for Canadians. The aspirations are there but the gains will be in execution.

1 This note considers only the platforms of the two leading parties given the overwhelming lead they hold. We cite parties’ own estimates of costing.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.