- Canada’s federal Finance Minister tabled its Spring Economic Update on April 28th.

- The Prime Minister had mostly scooped the story the day prior in announcing the intention to create a sovereign wealth fund with an initial $25 bn capitalization. This was largely the extent of the ‘investment’ agenda in this update, with net incremental capital outlays otherwise amounting to $1 bn over the horizon.

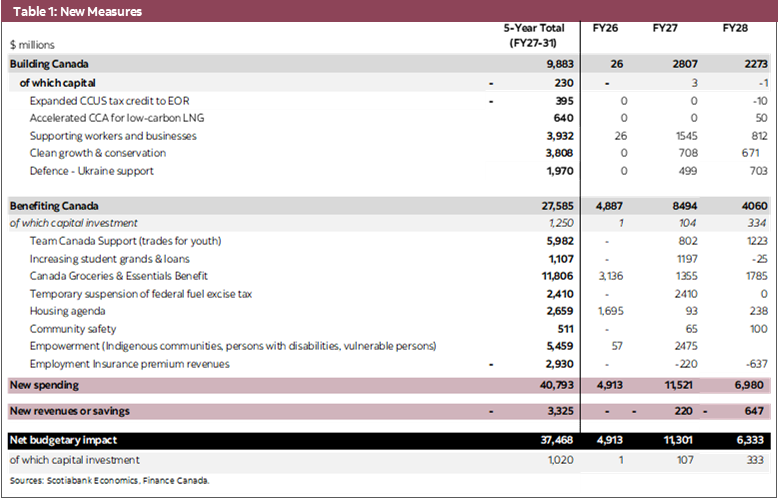

- Much of the anticipated fiscal windfall—at a sizeable $60.3 bn—was ploughed back into an additional $54.5 bn in spending. The picture is somewhat muddled with “new measures” (a net $37.5 bn) encompassing known items such as the groceries benefit and the fuel tax suspension, while “policies since Budget 2025” at $17.0 bn appear as a dizzying list of departmental spending extensions and adjustments in an annex.

- The update estimates the FY26 deficit came in substantially lower—at $66.9 bn versus the earlier-projected $78.3 bn but deficits in trailing years are otherwise near-identical to earlier projections after new spending is folded in (chart 1). Marginal improvements come from a stronger GDP profile over the horizon.

- The net debt profile is on a modestly faster pace of descent owing to lower debt levels as well as a stronger GDP denominator (chart 2).

- The growth impact of new measures is minimal in the near-term as supports were known heading into the budget. The cumulative tally announced in the past six months is growing though—at almost $145 bn in federal fiscal support—but much still hinges on delivery.

- The Bank of Canada won’t be tearing up its playbook for decision day tomorrow (April 29th), but it will likely sharpen its upside narrative against an otherwise volatile backdrop. While a hold is widely expected, the update reinforces Scotiabank Economics’ view that the next move is likely a hike—perhaps sooner rather than later.

- Otherwise, the update will be a footnote in a crowded week. Canada’s investment agenda is gaining traction, but it’s a long-run play with markets likely pricing the potential payoff only gradually.

- Execution and geopolitical risk will dominate for now. Look for greater clarity—directionally at least—on both fronts come budget time this Fall.

- Today we get clarity that the government is comfortable continuing to spend.

MAINTAINING MOMENTUM

Canada’s federal government tabled a 2026 Spring Economic Update on April 28th. The mid-year update largely builds on the government’s earlier tabled trillion-dollar investment plan set out in last year’s budget with the announcement of the sovereign wealth fund but otherwise mostly presents a more traditional spend plan.

The update lands in a highly charged and uncertain geopolitical environment that underscores the imperative of the investment agenda. With a slim majority now, the federal government is expected to accelerate the pace of implementation in the months ahead. They have a lot on their plate—including now the creation of a sovereign wealth fund—that leaves little margin for distraction (and a lot hinging on details).

CLOUDED FORECASTS WITH UPSIDE POTENTIAL

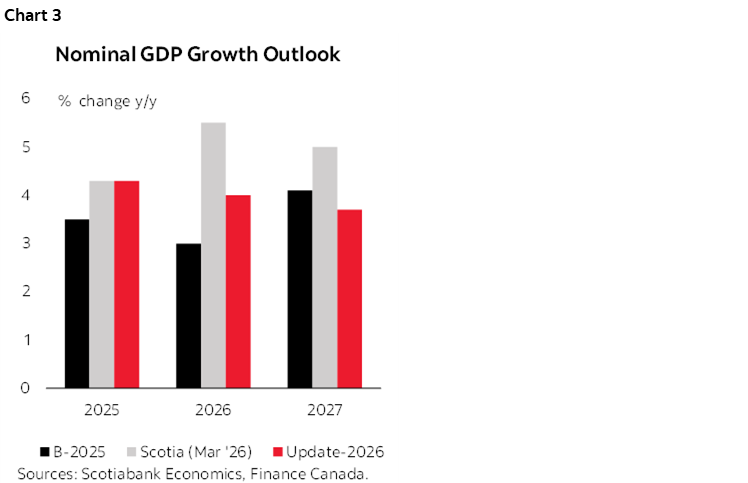

The update continues to cast a cautious economic outlook despite a stronger starting point. Real GDP is now estimated at 1.7% in 2025—roughly 0.5 ppts stronger than previously assumed—leaving the level of GDP at end‑2025 about $63 bn higher (around 2 ppts) with an added lift from historic revisions. Looking ahead, an average of private sector forecasts points to muted momentum with growth of just 1.2% this year before a gradual recovery to 2.0% into 2027. Scotiabank Economics’ current outlook is somewhat more constructive, particularly in budget-relevant nominal terms, as we assume a meaningful terms‑of‑trade shock could bridge to a potentially stronger acceleration in activity as risks abate (chart 3).

The incremental fiscal impulse in the update is minimal. Much of the near-term support was already known coming into the update. Meanwhile the design of the new sovereign wealth fund still needs to pass the additionality test while the $25 bn cash outlay appears roughly evenly spread over the next three years in an economy that invests roughly half a trillion annually—assuming there are no execution delays.

The cumulative impact of this government’s spending to-date is meaningful. The $54.5 bn update (through FY31) stacks on top of the net $90 bn booked in Budget 2025, bringing the 6-month tally to almost $145 bn. This is unfolding in the context of a broader investment and regulatory reform agenda that should amplify leverage over time.

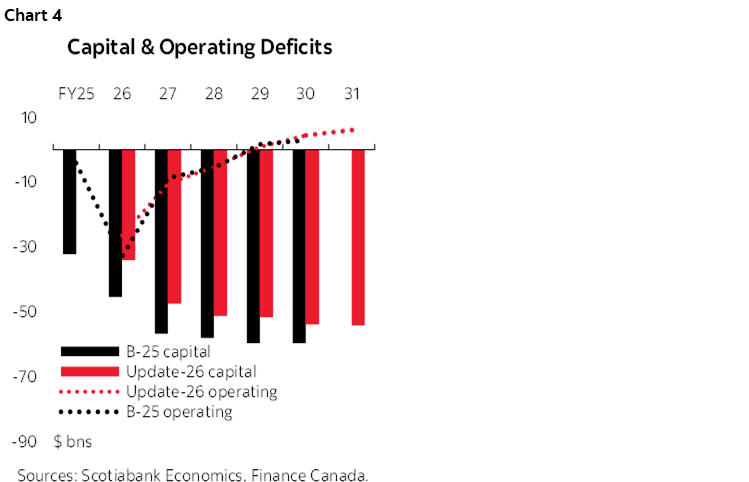

But it is reasonable to continue parking some of this in the upside for now. The update showed preliminary signs of growing pains with delays in tax credit uptake that drives a modestly lower profile in capital outlays in the near-term, and a range of other hints of hiccups (with course-corrections). While the government sticks to its balanced operational plan within three years, there is some modest slippage in the near-term in capital outlays (chart 4). Execution risk is likely further challenged by delivery spanning multiple levels of government and multipliers that are also contingent upon a private sector response which still remains cautious.

As flagged in our preview, it would be premature to see signs of ‘shovels in the ground’ in aggregate data just yet, but there signs should grow as the year advances. This leaves material upside in growth (and inflation) forecasts.

EXECUTION IS THE MULTIPLIER

The Prime Minister tabled the update’s signature measure the day prior. The federal government intends to create a sovereign wealth fund (or the “Canada Strong Fund”) that will invest alongside private investors—with a focus on equity ownership—in major domestic projects and companies across clean and conventional energy, critical minerals, agriculture, and infrastructure. A new arm’s‑length Crown corporation will manage the fund on commercial terms with an initial capitalization of $25 bn. A retail sleeve would allow Canadians to invest alongside the Fund and share in the upside.

The Fund is not expected to impact the deficit or net debt path as it would operate on commercial terms. The $25 bn capitalization would, however, lift borrowing requirements over three years as a non‑budgetary transaction, offset by a financial asset on the balance sheet. However, improvements in other non-budgetary items more than offset these new outlays lowering modestly financial requirements over the horizon.

There are otherwise still a host of unknowns that will be critical to its success including the ability to leverage—not displace—private investment. It is not entirely clear how the Fund will fit into the broader ecosystem of Crown corporations supporting the growth agenda, but the update indicates the government will undertake a review of mandates. A transition office has been set up to consult on design to address these (and many more) considerations.

The update also takes a baby step towards further “asset optimization” for airports. Budget 2025 had committed to explore options to privatization; this update notes they plan to table legislation to obtain the information they need to complete the review, while also modernizing governance structure of airport authorities. Scotia Economics has earlier laid out the case for asset recycling while the sovereign wealth fund release alludes to this direction, but there are few firm plans in the update. While federal leadership in this space could provide an important demonstration effect for other orders of government where the bulk of Canada’s infrastructure assets sits, reading between budget lines resistance is evident.

There is also a material spending package to support younger workers in skilled trades. There is almost $6 bn over five years (settling around $1.3 bn ongoing) to recruit and train 80–100 k Red Seal skilled trades under a Team Canada Strong program that targets youth. This is a positive step in recognizing the serious skills shortage the ambition build agenda will confront. (Another $1.1 bn is provided in student grant and loan relief.)

AND THEN SOME

Earlier-announced near-term supports are folded into ‘new’ measures. For example, the Groceries & Essential Benefit, the temporary suspension of the federal fuel tax, and various known housing measures account for almost $17 bn in the $54.5 bn spending package. Otherwise, it is difficult to pin down broad themes or key measures across the rest of the spending. See table 1, back for a few of the key line items.

There is also a range of tax changes. There is a reduction in the CPP base rate (from 9.9% of 9.5% in 2027).The Employee Ownership Trust tax exemption has been made permanent. Enhanced oil recovery will now qualify for tax incentives under the CCUS program as per the MoU signed in November with Alberta (this is booked in the update as a revenue source assuming it spurs incremental investment). The update provides details around low-carbon LNG eligibility for accelerated capital cost allowance eligibility, while taking steps to address delays in processing of clean economy tax credits.

The update also promises a number of plans, strategies, reviews and summits. This includes a “Whole of Government Competition Plan” that will “focus on removing inefficient government policies that impede competition arising from regulation, procurement, and industrial support”. The Finance Minister will provide details in the coming months. A nuclear strategy is promised, an investment summit is in the books for September, and a Sustainable Investment Summit is forthcoming.

SPOT THE DIFFERENCE

The stronger 2025 economic handoff provides a solid lift to the fiscal baseline. A combination of revenue out-performance and a lower-than-expected expenditure profile drive this improvement. The net effect of economic and fiscal developments are projected to deliver an estimated $17.7 bn windfall in FY26 alone and a cumulative $60.3 bn through FY30.

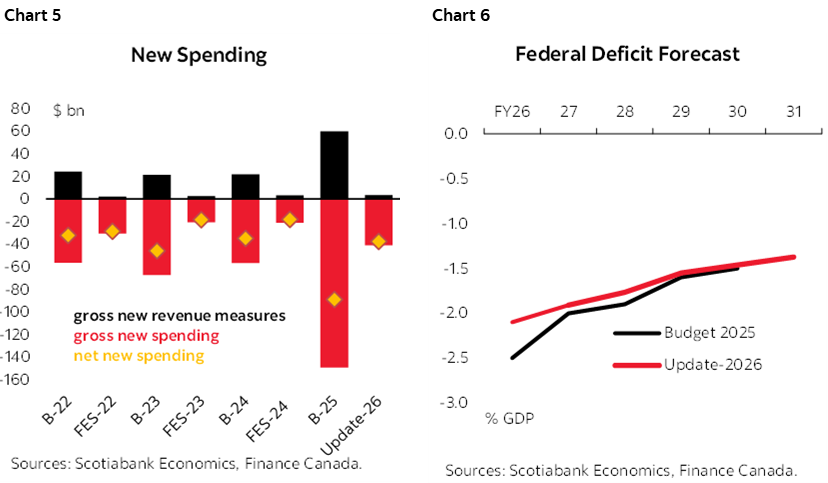

Most of the new fiscal headroom is absorbed by new measures. Net new spending in the update itself totals $54.5 bn over the horizon (or according to the update, $37.5 bn in ‘new’ measures (chart 5) and $17.0 bn in measures since Budget 2025). After banking the $11.4 bn savings in FY26, banked, deficit projections are near-identical over the horizon in dollar terms—and slightly tighter as a share of GDP owing to revisions (chart 6). This profile maintains a declining deficit as a share of GDP—one of the government’s fiscal anchors.

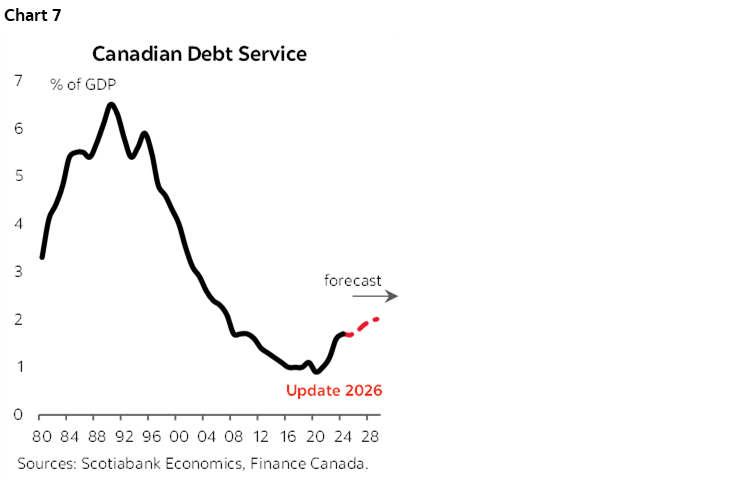

The debt outlook also benefits from a strong GDP baseline as well as modest improvement in outstanding debt levels. Debt is now estimated at 41.1% of GDP in FY26, peaking in FY29 at 41.9% before pivoting to 41.6% by FY31. This reflects over a percentage point improvement over the horizon. Debt charges are expected to rise modestly over the horizon (chart 7).

Debt issuance plans for FY27 remain at $298 billion. Lower financial requirements in FY27 will be accommodated through treasury adjustments, and the profile benefits from a continued descent in refinancing needs.

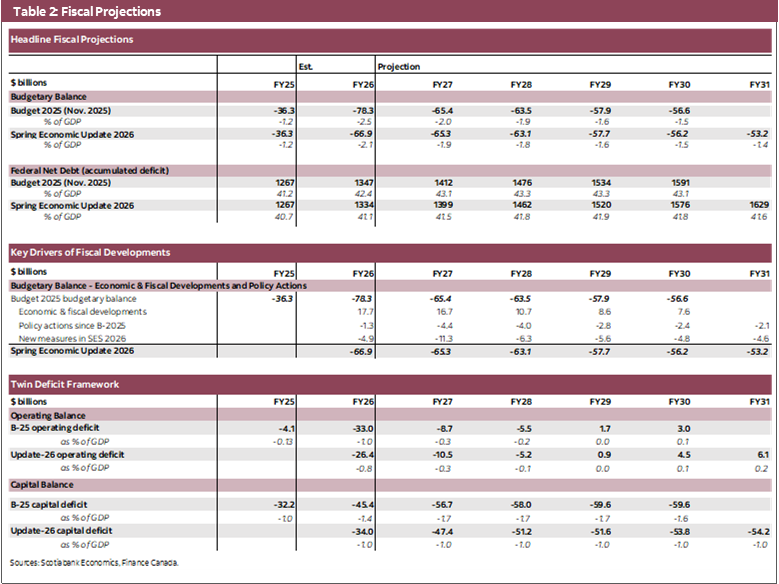

See table 2, back for summary of fiscal projections.

BOTTOM LINE

The update is unlikely to generate significant market attention in a busy landscape. It lands just before key decisions from the Bank of Canada and a series of major central bank announcements—including the FOMC, ECB, and BoE—in the coming days. Ongoing geopolitical uncertainties continue to shape daily sentiment.

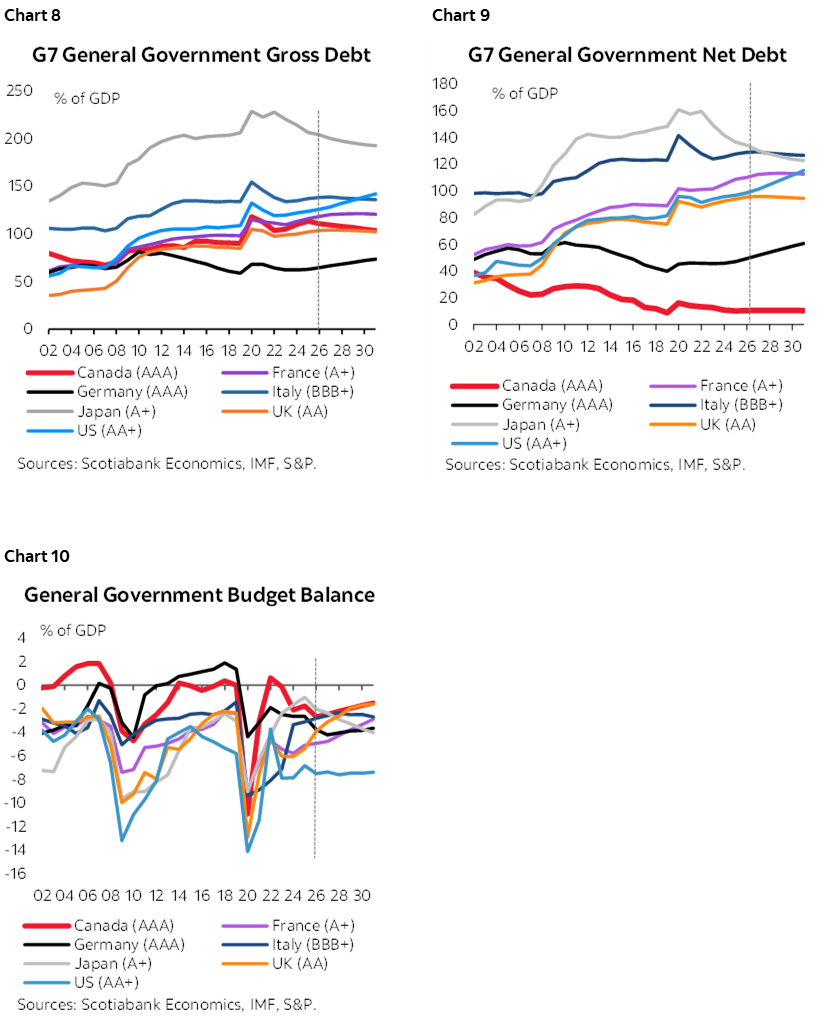

Nevertheless, it signals sustained ambition (and spending bias) over the medium term. Canada’s largely stay-the-course fiscal path preserves its relative advantage—across metrics such as gross and net government debt and its primary balance (charts 8–10)—while its net energy exporter status increasingly sets it apart from peers. It remains one of the few with meaningful fiscal space and the political will to use it in the face of serious geoeconomic threats.

Whether execution can live up to ambition remains to be seen. Greater evidence of solid, sustained implementation is still needed to turn tentative optimism into genuine conviction. With a bit of luck—and a lot of hard work—that is hopefully the foundation of Budget 2026 later this year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.