- Canadians will get a first progress check on the Carney government’s trillion dollar plan under its new fiscal framework on April 28th. The 2026 Spring Economic Statement will be tabled in a highly uncertain global backdrop that only reinforces the case for Ottawa’s ambitious investment‑led strategy.

- While near‑term economic activity remains weak, a recovery should take hold as risks dissipate. With inflation risk sidelining the Bank of Canada for now, the near‑term burden shifts more squarely to fiscal policy—where preserving optionality may be the safer bet should downside risks materialize.

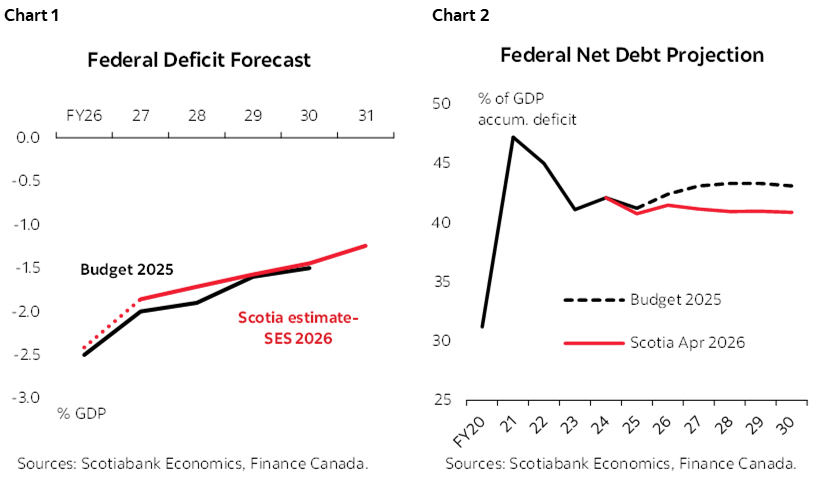

- Despite a long list of headwinds, a stronger nominal growth profile may point to additional fiscal head room in this update. That could open the door to additional spending though we assume they would do so within the contours of the earlier deficit profile. Debt ratios could look materially better under such a scenario, reflecting material historic GDP revisions (charts 1 & 2).

- The update will land in a highly volatile market environment. Well‑channeled fiscal activism—combined with a bottom line that may not look materially different—is unlikely to move markets in the near term. More important will be signs that the investment agenda is gaining traction as some investors may remain cautious on execution—and geopolitical—risk.

- Overall, the update is likely to be about maintaining momentum and sharpening delivery, while laying the groundwork for bolder steps in Budget 2026.

FORWARD GUIDANCE

Canadians will get a fresh take on federal finances on April 28th. The Spring Economic Statement should provide a first progress check since the Carney government unveiled its trillion-dollar investment plan under a new fiscal framework in last year’s budget.

Policy rollout has been rapid with most campaign commitments already tabled barely a year in. The Major Projects Office is up and running with a robust project pipeline currently valued at $126 bn. A new Defence Industrial Strategy now guides the budget’s $82 bn downpayment towards the 5% NATO pledge. A dedicated housing agency is operational, immigration targets are proving binding, and there has been early action on public-sector downsizing.

Momentum should continue. With a slim majority now in hand, the government is well positioned to further advance its agenda. While a fuller mandate reset is more likely in the Fall budget, this update should sustain momentum, using any near‑term fiscal tailwinds to reinforce investment plans without straying far from November’s fiscal path.

PENCILLING IN FORECASTS

The outlook remains highly uncertain. Risks have shifted since the budget, and while 2025 growth came in stronger than expected, the near‑term horizon remains clouded by sizeable downside risks—notably CUSMA renegotiations. Private‑sector forecasts therefore are at best placeholders in this update with a wide range of potential outcomes.

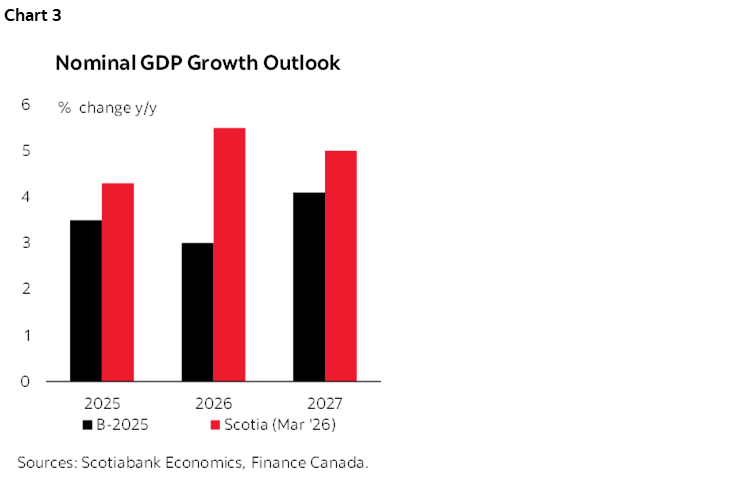

At least the starting point is stronger. Nominal GDP growth in 2025 was almost a full percentage point firmer than expected at budget time, with historical revisions further lifting the base (chart 3). End‑2025 GDP is now estimated to be roughly $63 bn (2 ppts) higher than previously assumed. Looking ahead, a positive terms‑of‑trade shock linked to the Iran conflict should support higher nominal growth—a key benchmark for fiscal capacity.

It may be premature to fully bank those gains just yet. Early‑year data have been soft, inflation risks remain elevated, and uncertainty is high. Activity is still being supported by past rate cuts and government spending, with slack persisting in the economy. A recovery should firm up as the year progresses according to Scotiabank Economics’ latest forecasts, but that hinges on private sector investment picking up the baton.

We remain cautiously optimistic around the longer-term investment plan but it is premature for definitive evidence. With a 0.5 ppt (of GDP) step‑up in government investment already baked into our forecast—and a history of slippage and overruns—Ottawa may limit further balance‑sheet commitments, at least for now, until its agenda gains further traction. (See Box 1: Show Me the Shovel.)

Fiscal calibration is more complicated in this environment. We will be watching for a stance that aligns with near-term economic conditions while reinforcing credibility around the longer-term investment agenda. With roughly $4.2 bn in near-term support already set to flow in the coming months and inflation risk titled to the upside, a prudent, risk‑based approach would preserve optionality to deliver additional stimulus down the road should downside risks materialize.

Even so, this update likely leans modestly toward more fiscal activism at the margin.

FISCAL FOOT FORWARD

The federal government continues to signal a clear intent to lean on its balance sheet to support longer‑term growth. It has shown a relatively contained responsiveness to affordability pressures. Since Budget 2025, Ottawa has announced roughly $14.6 bn in additional stimulus (through FY30), including the GST Groceries & Essentials Benefit, a temporary fuel‑tax suspension, and targeted tax relief for first-time buyers of new homes.

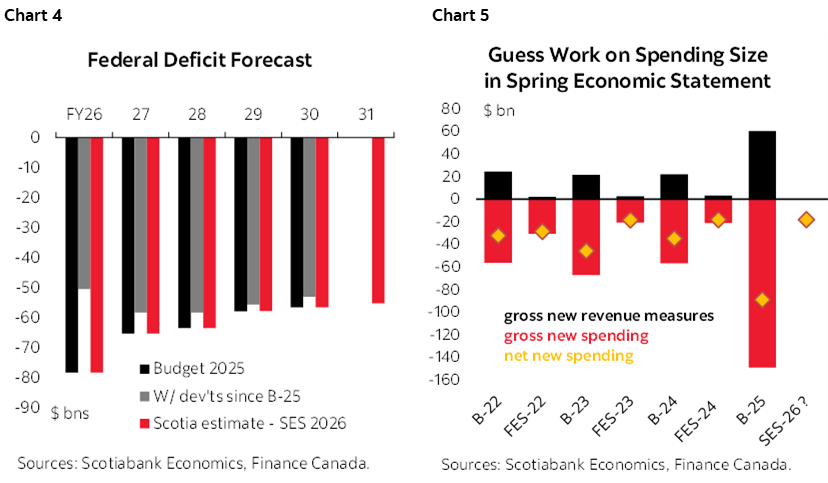

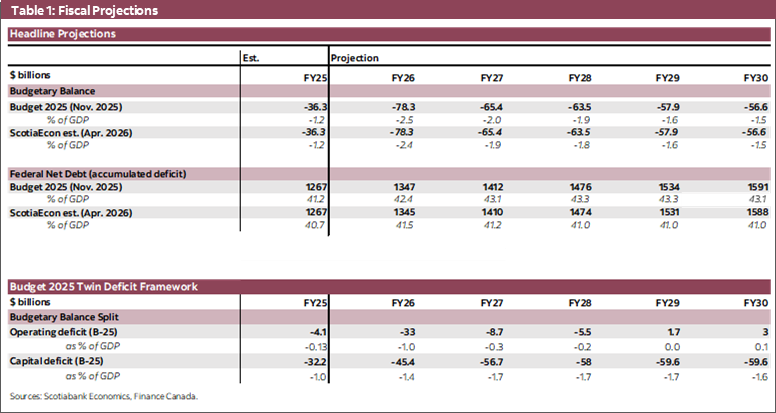

Any further spending should be largely contained within the existing deficit profile. Budget 2025 projected deficits peaking at 2.5% of GDP in FY26 before narrowing steadily to 1.5% by FY30. Since then, the stronger growth hand‑off from 2025 and historical GDP revisions point to potentially meaningful fiscal improvement heading into this update. These impacts alone could shave several billion dollars per year off the deficit outlook before any new measures.

However, details remain uncertain. The preliminary fiscal balance for the year that ended only weeks ago is one wildcard, with data through January tracking materially tighter than projected—the ten‑month shortfall stood at just $31.2 bn versus a $78.3 bn forecast in the Fiscal Monitor. But timelier bond‑issuance data suggest activity broadly in line with the earlier plan so an uptick in late‑year spending (or year‑end adjustments) could reasonably narrow much of the apparent gap.

Our best-guess is that the government broadly preserves the Budget 2025 deficit path in dollar terms by containing any new spending (including measures already announced) within any potential fiscal windfalls (chart 4). With low conviction, we would pencil in a package on the order of $20 bn on top of the earlier announced $14.6 bn measures—broadly consistent with past mid‑year updates (chart 5). If fiscal windfalls come in smaller (or larger) than expected, we would scale back (up) potential new measures accordingly to keep deficits aligned with Budget 2025. We will be watching defence as one possible area for a potential top-up in outer years. (See Box 2: Putting a Price on Security.)

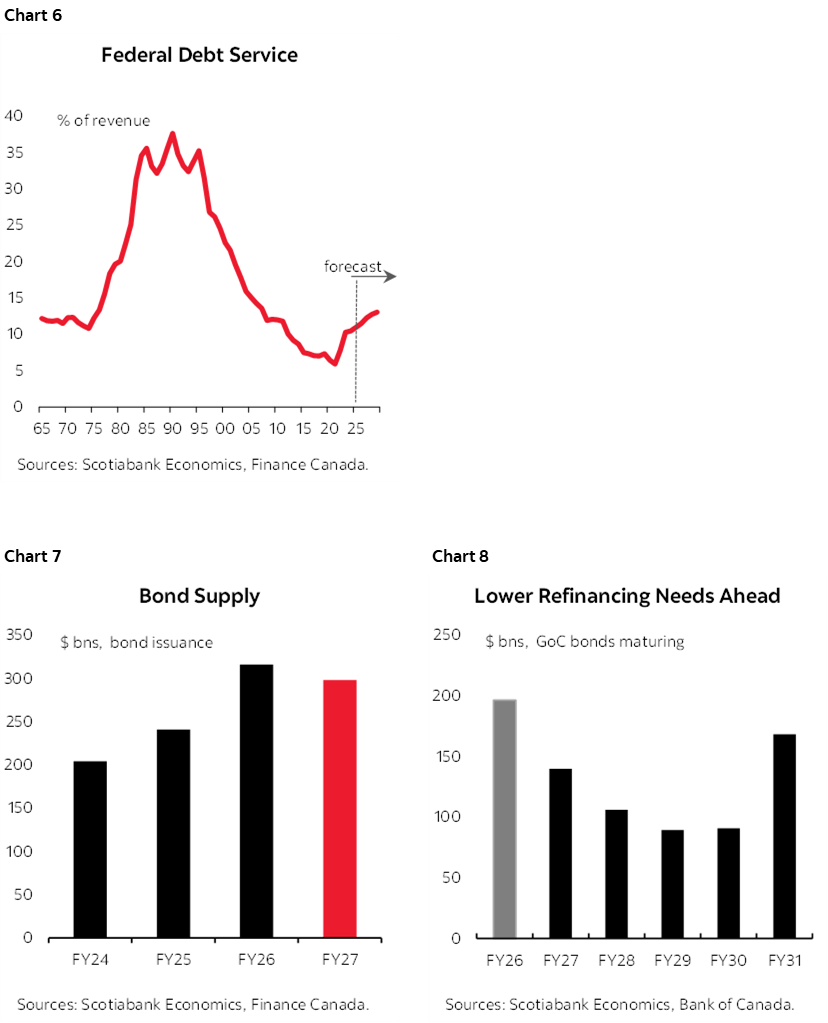

Under these assumptions, debt service projections would be broadly unchanged—creeping up somewhat uncomfortably given exposure to exogenous risk (chart 6). Budget 2025 assumed a 10-year GoC yield of 3.4%, not far from its current (albeit volatile) tracking. Debt as a share of the economy could show a material improvement—possibly as much as 2 ppts—owing to material denominator revisions. Such a scenario would not change bond issuance plans for FY27 set at $298 bn in November’s Debt Management Strategy with some reprieve from lower refinancing needs ahead (charts 7 & 8).

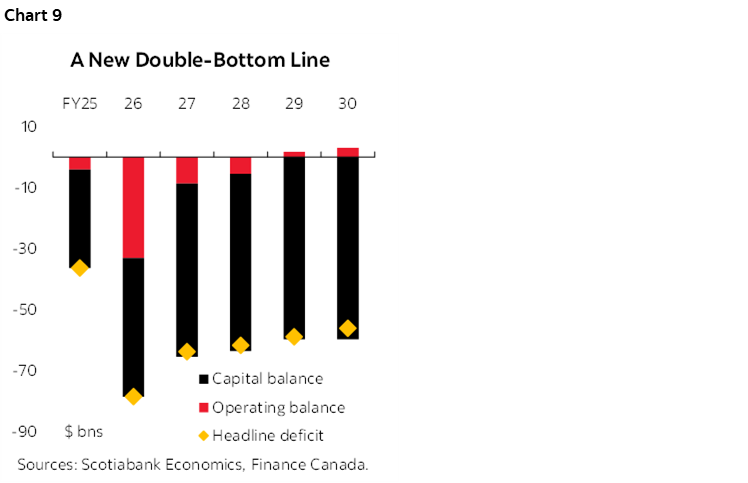

We expect the government would adhere to the fiscal anchors set just months ago. These include deficits that decline steadily as a share of GDP—though recent backward‑looking revisions may complicate that trajectory—and a commitment to a balanced operating budget within 3 years (chart 9). The latter is supported by an expenditure review expected to deliver $60 bn in savings, with early progress evident in announced FTE reductions and scope for further clarity in this update. (See table 1 on page 4 for fiscal projections.)

If the government is to lean further on its balance sheet in this update, the safer bet is to channel that capacity toward longer‑term investment mostly in outer years. Doing so would keep policy consistent with the fiscal framework set out last December, reflect likely limits to further near-term ramp-ups, while further distancing its approach from the prior government’s tendency to spend unexpected windfalls on operational spending.

RESERVING JUDGEMENT

The update will be digested in a volatile environment. Heightened geopolitical turmoil and renewed inflation risk are roiling sovereign bond markets at a time of elevated global issuance and fragile investor confidence. Term premia remain volatile, cross‑market correlations have risen, and price action is increasingly headline‑driven. In this environment, Canada remains exposed to spillovers from global repricing, even where domestic fundamentals compare favourably.

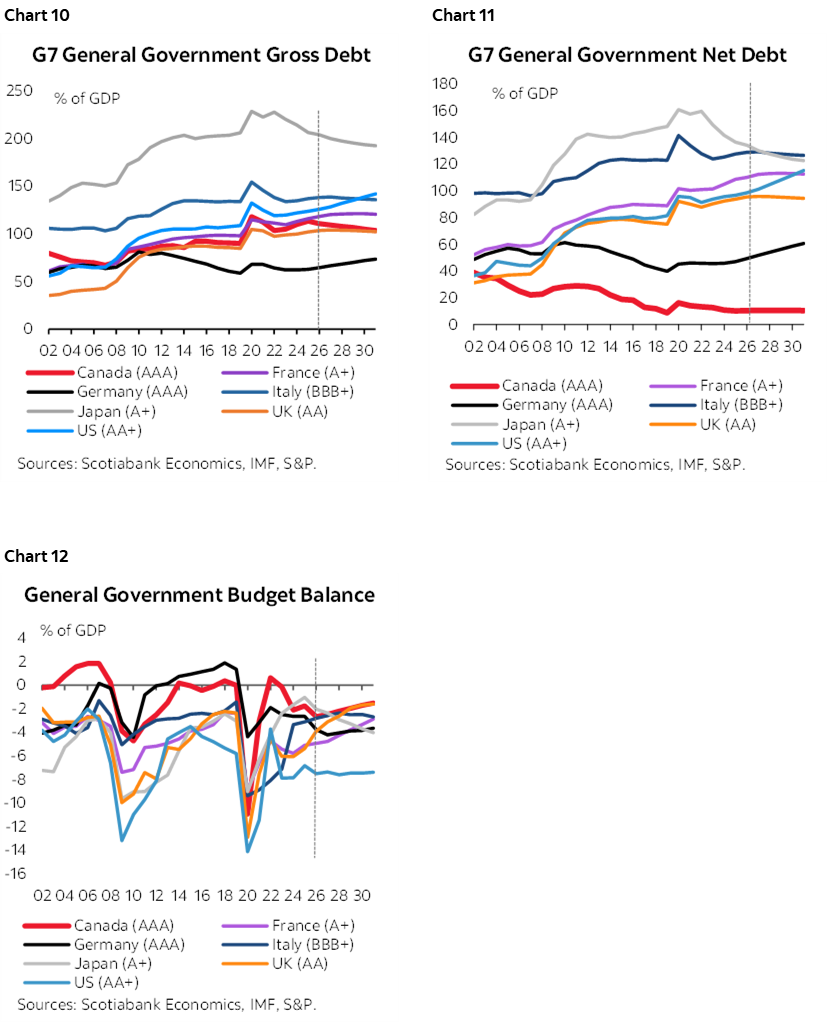

Canada enters this period from a position of relative fiscal strength. Across key metrics—gross and net general‑government debt and the primary balance—Canada screens well against G7 peers (charts 10–12). Its status as a net energy exporter has become more salient amid a renewed global energy shock, but execution risk and CUSMA‑related uncertainty remaining material downsides.

In the near term, a largely unchanged deficit profile—even alongside incremental investment—should largely be a market non‑event.

BOTTOM LINE

Recent global events have reinforced—and emboldened—the federal government’s investment agenda. Interest is building, but it remains early days, with clearer proof points still needed to move markets from cautious optimism to conviction. Any decisive shift in policy or fiscal strategy is more likely a Budget 2026 story. This update is instead likely about keeping momentum going, with execution and delivery still expected to do the heavy lifting.

BOX 1: SHOW ME THE SHOVEL

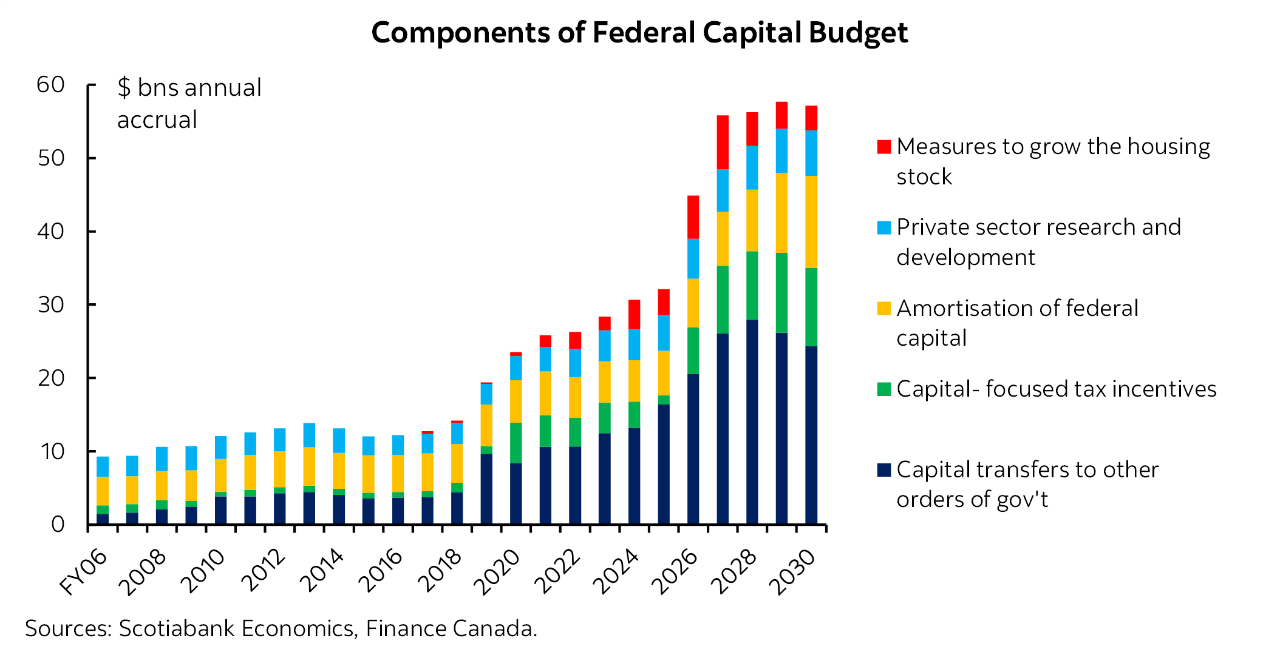

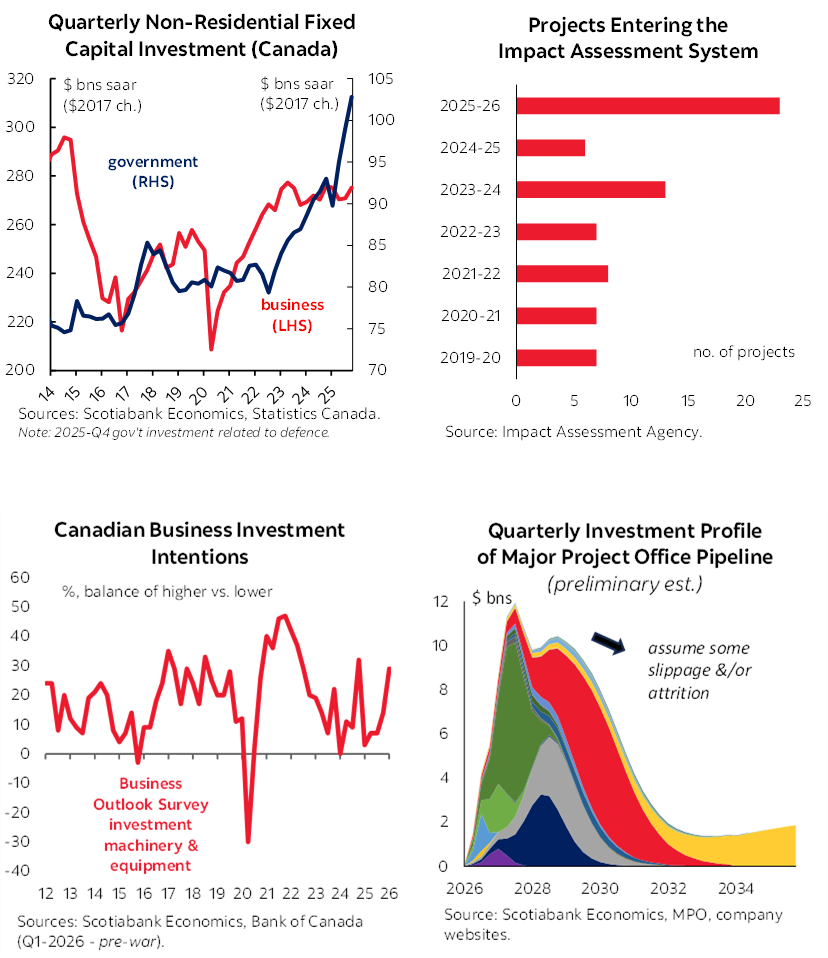

The government has set out an ambitious plan to use its balance sheet to catalyze over a trillion dollars in investment over the next five years. Early signs of a public‑sector ramp‑up are already visible in macro data, notably via a surge in defence‑ and security‑related outlays in late-2025, alongside an anticipated step‑change in transfers to other orders of government embedded in the fiscal framework. Together, these should help underpin broader general‑government capital spending going forward.

It is still too early to see a material private‑sector response in macro data. In our baseline, business investment begins to firm up toward late-2026, with the heavier lift arriving from 2027 onward. That should eventually show up in national accounts investment data, preceded—imperfectly—by investment‑intentions data that are already turning positive albeit from subdued lows.

We are also watching project‑level signals: the Major Projects Office pipeline now totals roughly $126 bn in proposed investment, and project entries into federal Impact Assessment Agency have risen sharply as approval timelines accelerate with a slew of ‘early decisions’ flowing in recent weeks. Not all proposals will proceed, and not all provinces have yet signed on to a one‑project, one‑assessment framework, warranting a sizeable haircut—as reflected in our modelling for now.

Even so, taken together, these indicators tilt risks modestly to the upside. This is a space to watch.

BOX 2: PUTTING A PRICE ON SECURITY

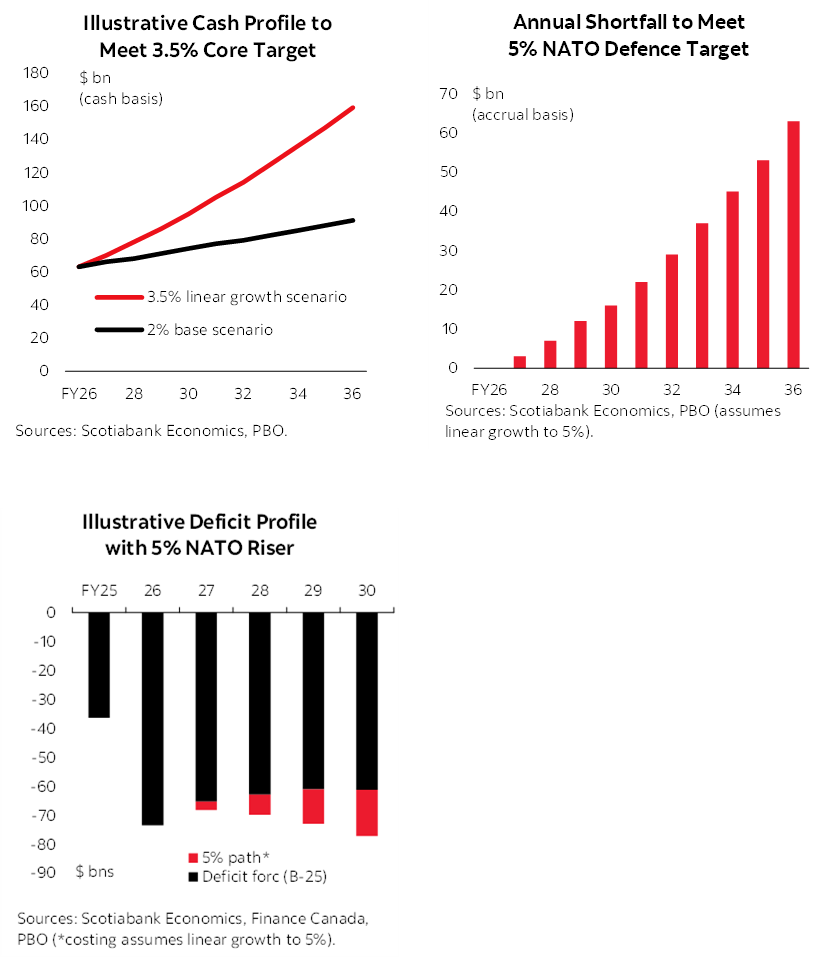

The federal government has committed to meeting NATO’s new defence and security spending target of 5% of GDP by 2035. This includes 3.5% of GDP for core defence spending under NATO definitions, and up to 1.5% for defence‑ and security‑related items, with the latter largely expected to be met through existing plans. Canada reached the prior 2% benchmark in FY26 following a sharp ramp‑up in defence outlays shortly after Prime Minister Carney took office.

Budget 2025 added $81.8 bn over five years—including $6.6 bn to launch Canada’s Defence Industrial Strategy—but stopped short of laying out a clear fiscal path to the 3.5% core target. The Parliamentary Budget Officer estimates that meeting this benchmark could require roughly $159 bn in annual defence spending by 2035–36, implying a sizeable gap relative to currently specified plans.

With a relatively short budget planning horizon, the upcoming update offers scope to fold in additional outer‑year commitments as a way to credibly signal intent while deferring the bulk of fiscal pressure beyond the forecasting horizon—signalling that may carry added weight ahead of forthcoming CUSMA negotiations. Near‑term acceleration, however, is likely constrained by absorption and capacity limits, particularly after last year’s rapid ramp‑up and alongside a stated policy tilt toward boosting domestic production from roughly 30% of procurement today toward a long‑run goal near 70%.

The PBO estimates that a NATO‑consistent path could add roughly $30 bn in cumulative defence spending by FY30, which—relative to Budget 2025 projections—would push deficits modestly higher before accounting for any potential fiscal windfalls in this update. Still, with NATO’s classification of defence‑ and security‑related spending continuing to evolve, some definitional flexibility remains—making defence a key area to watch for both signaling and medium‑term fiscal trade‑offs.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.