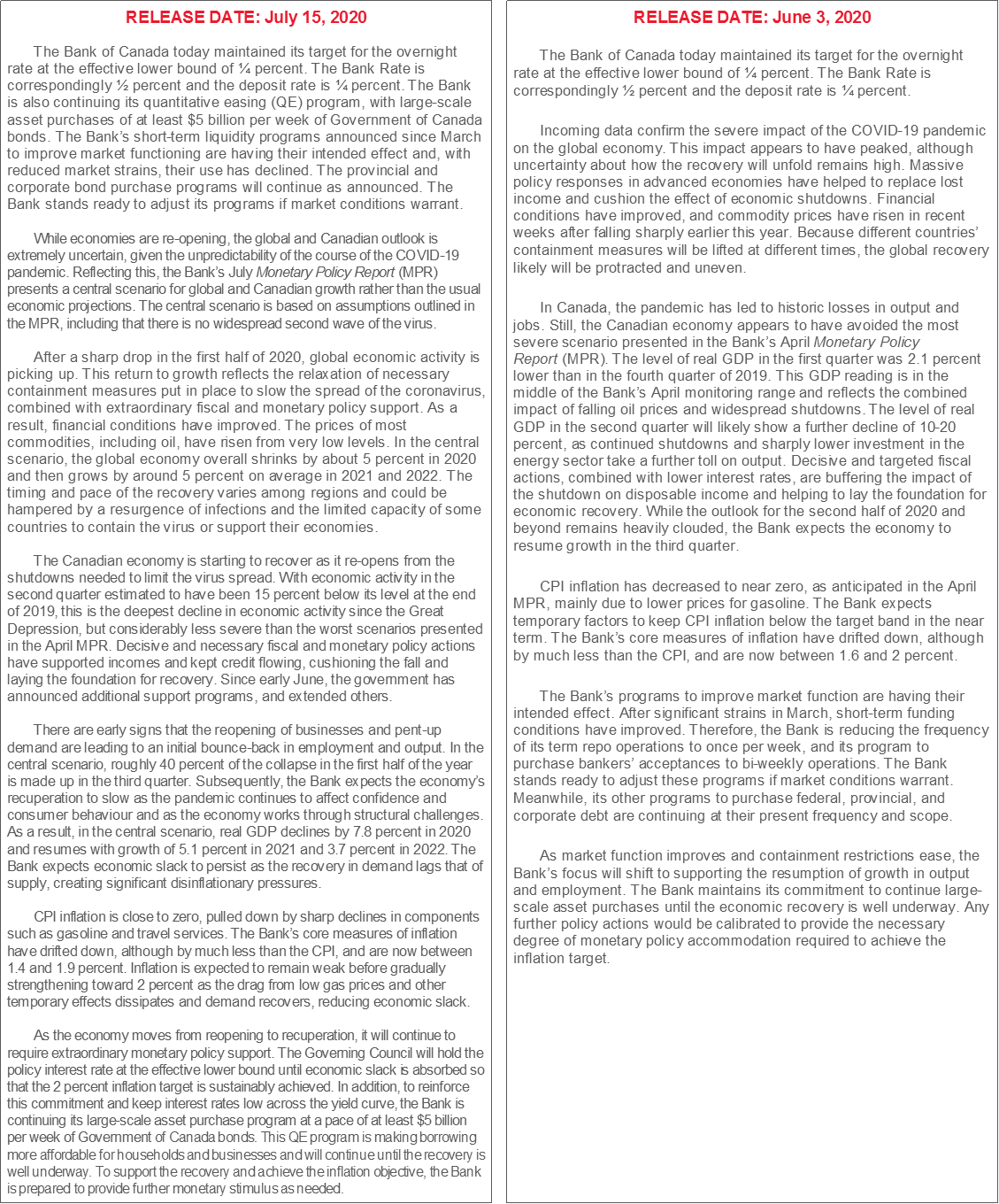

This is a more significant overall set of communications than perhaps markets realize so far (here, here and here). CAD appreciated on a down day for the USD but climbed the ranks of relative performers through the communications. The Canada curve is marginally outperforming the US at the long-end. Here’s what they did.

A POLICY RATE HOLD UNTIL 2023+

Whether it is a repudiation of the prior regime’s tendency to loathe forward rate guidance, or simply a sign of the times given a massive shock to the system is not clear. What is clear is the BoC’s guidance that you can count on the policy rate to be left at 0.25% probably into 2023 if not later. Governor Macklem fully embraced forward rate guidance as I indicated he would immediately after his appointment was announced and in the preview of this meeting. Unlike the last time he was involved during the 2009–10 conditional commitment that offered a time and a condition, this time the BoC is using condition-based forward guidance.

The condition is that spare capacity must be eroded and the inflation target thought to be durably achieved. That doesn’t happen within their 2020–22 forecast horizon. By inference, it could happen as soon as 2023 if spare capacity continues to erode and drive a lagging return to the inflation target. There are upside and downside risks to this guidance framework, but the BoC leans to downside risks.

The BoC said it will require inflation to be sustainably on the 2% target before raising rates and that as long as they judge there to be spare capacity, they won’t view the target as being sustainably achieved. That means if we happen to get a headline inflation pop in, say, 2021 which is feasible, the BoC would look through it unless growth were to rip and shut spare capacity which is doubtful.

PURCHASES TO FOLLOW THE FEDERAL GOVERNMENT

While the BoC left its GoC purchase range unchanged at C$5B per week or more, the press conference confirmed that the two-week buyback announcement reflected a more durable shift toward expanded bond purchases to follow lengthened issuance horizons. During the press conference, Senior Deputy Governor Wilkins indicated the BoC aims to “purchase across the curve proportionate to what is outstanding and being issued.” I had thought they would do this more explicitly as indicated in the preview I wrote, but they’re relying on loose guidance in the presser.

QE TO LAST FOR A LONG TIME

The BoC re-emphasized in both the MPR and the press conference that QE will persist long after having contributed toward repairing market conditions. The MPR said this here: “Initially, the purchases were improving liquidity. With improved market functioning and the reopening of the economy, other channels are becoming more important."

Macklem said it in the press conference when he noted that when the BoC says it will purchase bonds until the recovery is “well underway” they mean "somewhere in that recuperation phase beyond the initial bounce" and that the BoC will be looking for signs that the recovery is self sustaining before ending purchases and that “logically this happens before capacity is well absorbed” and hence before hikes. This implies an almost absurdly wide interval for the longevity of the GoC purchase program between as short as around next May when other bond purchase programs end according to present schedules, to as long as into 2023.

CAN THE BoC REALLY BUY FOR THAT LONG?

If the BoC buys GoC bonds at the minimum C$5B/week rate through to next May, then they would wind up buying at least another C$215B of GoC bonds from here. Scale that up if they continue to exceed the minimum and go longer. If they went to the end of 2021, then they’d wind up buying another C$350B from here. To the end of 2022 would mean C$615B of additional GoC bonds from here. I’m not sure that the markets can handle that over time without courting risk of market dysfunction. It may also limit the BoC’s potential firepower should subsequent shocks emerge.

TEASED ON YIELD CURVE CONTROL, TO BE REVISITED

These are some reasons why I think the BoC may be ultimately forced into a yield curve control strategy. The Governor teased markets by saying the Governing Council discussed the option, but when pressed, offered no elaboration or assessment and deferred the question to Wilkins who didn’t directly elaborate on the topic. I assume it was discussed, but that neither wished to reveal the content of that discussion as a state secret!

I would still maintain there are other multiple advantages to pursuing a yield curve control strategy with explicit targets skewed toward shorter term maturities into the belly of the curve now. Go here for why as I wrote about it in the BoC preview. In short, to be continued.

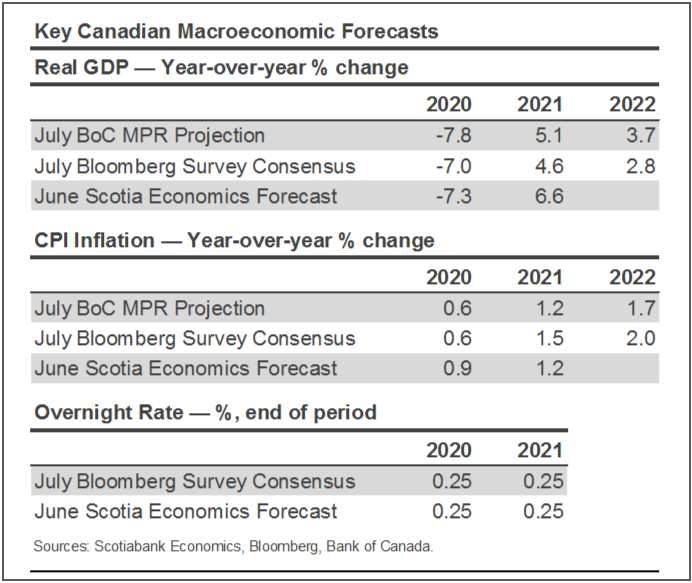

FORECASTS

The BoC presented stripped down projections for 2020 to 2022 which are summarized in the accompanying table. In general, the forecasts largely hugged consensus. There frankly would have been little reason to materially depart from consensus given the uncertainties and to do so in a way that may have raised more communication problems than solutions for the central bank and given how long it took the central bank to publish forecasts. Included within the projections is also guidance that the neutral rate estimate of 2.5% will be more fully reassessed in the October MPR.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.