- BoC holds policy rate unchanged at 2.25% as universally expected

- The forward bias was unchanged and nothing new was offered

- The BoC continues to monitor two risk scenarios…

- ...while looking through mixed developments in commodities and data

- The neutral tone awaits fresh forecasts in July, key H2 developments

- The BoC needs to address unreliable press conference feeds

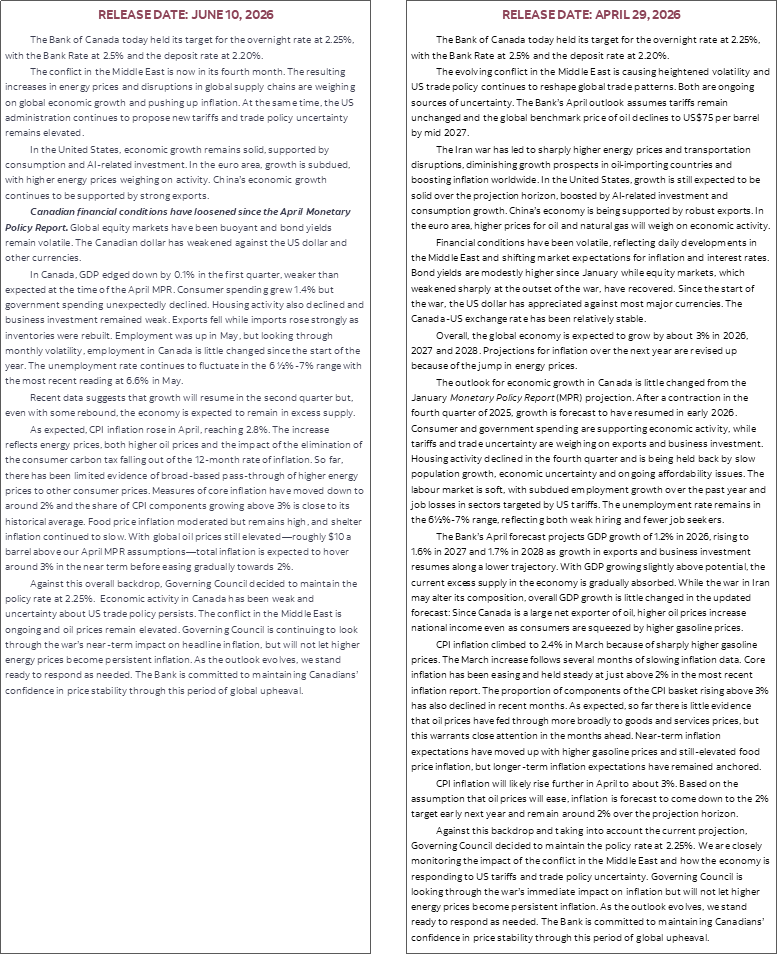

The Bank of Canada left its overnight rate unchanged at 2.25% as universally expected. The broad tone of the statement and Governor Macklem’s opening remarks to his press conference continue to suggest it is in monitoring mode, avoiding overreaction to any developments whatsoever and seeking further clarity on key risks to the inflation outlook. The overall communications were in line with expectations for now and ahead of a key second half of the year. The tone was neutral as they take in more information which is entirely as expected.

Frankly, they could well have just cancelled the event. There was nothing new.

The proof will be in developments over the second half of this year. The BoC took six months to evaluate falling oil prices over 2014 before acting in early 2015 and this is the reverse. We will learn much more about data including an expected rebound, plus trade policy risks over the remainder of the year. For now, we are merely left with the placeholder statement with four more meetings to go this year.

MARKETS LARGELY IGNORED THE COMMUNICATIONS

There was little reaction. The Canadian dollar had been appreciating after soft US core CPI and then retraced much of that move to land very little changed. The Canadian 2-year yield was rising into the statement and then consolidated the move to land about 2–3bps lower post-statement. Canada’s curve is performing very close to the US today. On net there is nothing much to see here. They flagged a “soft” economy amid inflation risk and emphasized that their job is managing inflation to the 2% target.

STATEMENT CHANGES

Key is that these two lines that speak to forward guidance were left entirely unchanged:

“The conflict in the Middle East is ongoing and oil prices remain elevated. Governing Council is continuing to look through the war’s near-term impact on headline inflation, but will not let higher energy prices become persistent inflation. As the outlook evolves, we stand ready to respond as needed.”

The statement noted that “financial conditions have loosened since the April Monetary Policy Report” and particularly flagged CAD depreciation.

The Governor’s opening remarks repeated the two scenarios from the April MPR, noting that they could cut if trade goes south, or they could hike if the energy shock persists. I would note that trade is recovering with trend exports pushing higher since last Summer while the energy shock is indeed persisting and worsening at what the BoC acknowledges to be higher oil prices than they had previously assumed. They still totally ignored the heat across many other commodity prices which is just plain wrong.

I still maintain Macklem is overplaying trade policy risks. ~90% CUSMA compliance and CAD depreciation into a growing US economy is why export volume trends are resilient. Macklem is exploiting trade negotiations to buy time as he monitors the commodities.

Beyond that, the statement merely read like an accounting of known data to date. For instance, the reference to Q1 GDP merely noted it was weaker than expected which we knew, but otherwise left it at that. It went on to note that “even with some rebound” in Q2, “the economy is expected to remain in excess supply.” That too matches everyone’s expectations, conditional upon defining how strong “some rebound” turns out to be. The statement also noted “So far, there has been limited evidence of broad-based pass-through of higher energy prices to other consumer prices” which is as expected but we only have April CPI to go by and greater pressure likely lurks ahead. On May’s job gain, the BoC noted “there has been a lot of volatility in the monthly job numbers” and “when you look through the bumpiness, employment in Canada is little changed since the start of the year” and the unemployment rate has fluctuated between 6.5–7%. I’d like to know the BoC’s estimate of the breakeven rate of employment changes given tighter immigration policy and falling population.

PRESS CONFERENCE TRANSCRIPT

The video feeds for these press conferences must improve. Bloomberg’s gapped out midway and froze. CPAC’s with translation entirely froze for an extended period. More stable IT feeds are vitally important and the BoC should be applying pressure to achieve as much. Here is a truncated press conference transcript in light of other pressing deadlines this morning.

Q1. At what point do you stop looking through the near-term impact of commodity prices?

A1. It's less about a timeline and more about the conditions. We don't want to see a big rise in energy prices turn into generalized inflation. We assess generalized with very little pass through into other goods and services prices so far. [ed. of course not! We only have 1 post-war CPI report!]

A1 cont'd: If we see more pass through then that would get our attention. We will also watch inflation expectations. Near-term expectations have moved up. If we see medium-term expectations move up then that would be a sign inflation is becoming entrenched. [ed. watch the BoC's July surveys....]

Q2. Why do you expect inflation in Canada to be more muted than in the US? Is it because of more slack?

A2. That's certainly part of it. We started at 2% inflation until the war. There are some other factors pushing up US inflation like tariffs but that should start to way absent new trade actions. And yes the economy is soft.

Q3. Does the Q1 GDP miss alter your estimate of slack and extend the normalization phase?

A3. Big picture, not a great deal has changed since our last decision in April. Largely just repeating what he said in the statement and his written opening remarks when it comes to GDP, inflation, jobs data.

Q4. Do you believe Canada is in a recession right now?

A4. Based on the data to date the economy is weak but it is not clearly in recession. [ed. lol, the BoC would NEVER say otherwise unless it is an unambiguous fact. Which it is not in any event.]

Q5. Are telling us it's unlikely the economy can get through this awkward phase on its own without some change in policy?

A5. [Rogers answering]. No. Went on to emphasize the two competing scenarios in terms of trade risk and energy shock risks. We're telling you today those risks are about balanced so the rate is about where it needs to be right now.

Q6. How are you thinking of extended uncertainty in CUSMA talks as a potential reason to cut rates?

A6. The good news is that the majority of trade is compliant and continues to be tariff free. Even with a deal I don't think you can be certain about anything. Businesses are adjusting by diversifying their trade.

Q7. Are you more or less concerned today about the risk of energy pass through to core inflation than in April?

A7. The war is ongoing, there is no clear resolution in sight. The fact the energy price futures curve has shifted up is reflecting that. The longer they are higher the bigger is the risk that starts to pass through to other goods and services prices and the more likely we need to respond. We've been very clear that we will not allow the war to become an inflation problem in Canada, but that is not the only thing going on. We will be updating our forecasts in July.

Q8. What do you view as the bigger risk to the Canadian economy: trade or energy shock?

A8. Both.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.