- The BoC held at 2.25% with unchanged balance sheet policies as widely expected

- Canadian markets didn’t care as they followed US data and Fed pricing

- The BoC is signalling no rush to do much of anything

- The BoC can’t make up its mind whether higher commodity prices are good or bad for Canada’s economy and inflation risk

- What the BoC is choosing to ignore on inflation risk

The Bank of Canada held its policy rate unchanged at 2.25% to the surprise of absolutely no one. Also unsurprising was the overall tone of the communications that just kept a steady hand on the tiller, tweaked a few forecasts and words here and there, and stayed on the sidelines monitoring developments and data. The press conference ended with wishes for a happy summer as the BoC goes on vacation which are the customary words often associated with a July presser since the next decision only arrives at the end of summer.

Markets reacted by shrugging as they placed more attention on US developments and largely ignored the BoC. Canada’s 2-year yield is down 4bps on the day versus down 5bps in the US. Canada’s curve reacted in sympathy to the US after weak US producer prices and lower revisions which dragged September Fed hike pricing down by 4–5bps on continued advice to receive September Fed OIS even as it has moved from pricing a full Fed hike at the peak to about half of one now. USDCAD is essentially unchanged. Markets continue to price about 18bps of a 25ps BoC rate hike by year-end which is where they stood going into the decision this morning.

All of that is not the same as saying that I totally believe what we were told by the BoC today. I think there is strong risk that either Governor Macklem is doing the same thing he did in the pandemic or he is waiting until he is good and ready with enough information at hand before doing much of anything. Over time, he may be at risk of hanging out too low for too long and talking through everything and with a curious take on the impact of commodity prices on Canada. I’ll cover what they did before coming back to explain what I mean by the latter point.

The statement is here, the MPR is here, the opening remarks are here and I’ll include an attempt at a press conference transcript below.

FORECASTS

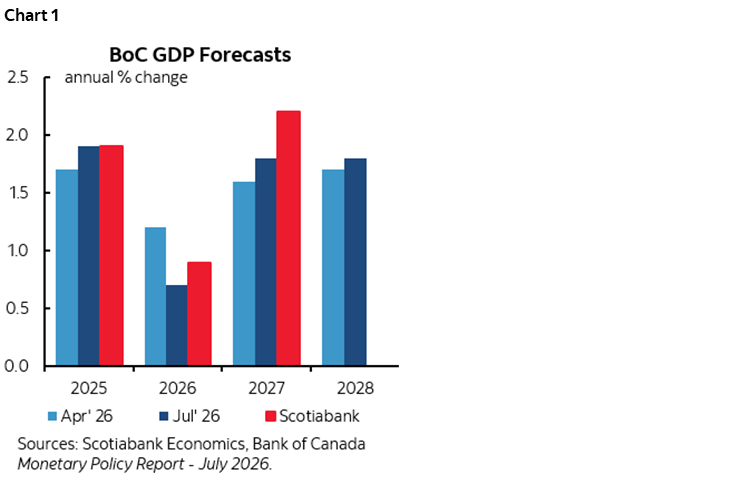

GDP growth was revised down for this year to 1.4% y/y from 1.8% in what is strictly a mark-to-market exercise to acknowledge the impact on full-year growth of the Q1 disappointment that was digested long ago but only now incorporated into BoC forecasts. Growth for next year was revised up by half a point to 1.9% q4/q4 and little changed for 2028 at 1.8% (1.9% previously). Chart 1.

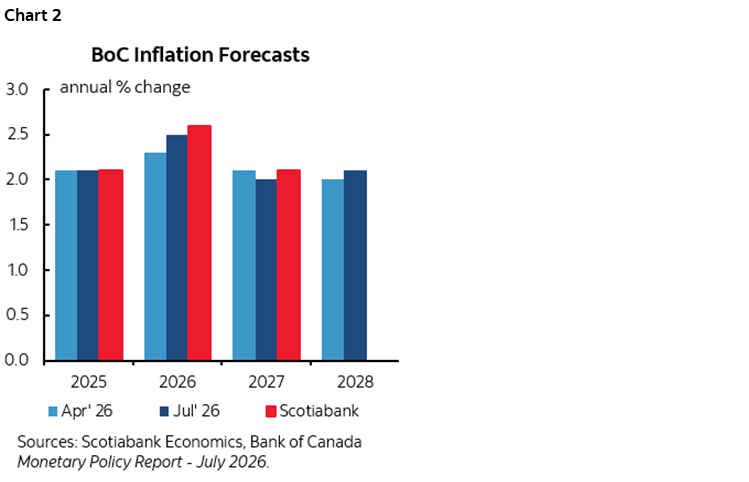

The inflation outlook was revised up on net (chart 2). Total CPI is now projected to rise by 2.4% y/y in 2026 on a q4/q4 basis (from 2.2%), then unchanged at 2% in 2027 and 2.1% in 2028 (up from 2.0%). Core inflation—the average of trimmed mean and weighted median CPI—was unchanged at 2% in 2026 q4/q4 and left at 2.2% for 2027 and then little changed for 2028 (2.1% from 2.0%).

STATEMENT CHANGES

The statement comparison between June and July is offered in the appendix. The BoC more clearly signalled that “Canada’s economy is showing signs of improvement” and “growth is picking up” while “inflation is projected to ease gradually from its recent spike.” Always be careful with the latter as we don’t know the BoC’s imputed rate profile.

The concluding paragraph was little changed and still ended with “and is prepared to adjust monetary policy as needed” while noting that “the current policy rate remains appropriate to sustain the economic recovery and bring inflation back to the 2% target.”

This statement was longer because it was a forecast meeting. They also noted financial conditions have eased.

Also note the explicit reference to how “As the recovery proceeds, economic slack will be gradually absorbed.” The BoC continues to hang onto wishing to see this happen above and beyond any other drivers of inflation which could be highly contestable.

GOVERNOR MACKLEM’S OPENING REMARKS

The main thing that caught attention in the Governor’s opening remarks to his press conference was the contrast between the paragraph on directional risks to the policy rate.

In June’s opening remarks, Macklem said:

"If the United States imposes significant new trade restrictions on Canada, we may need to cut the policy rate further to support economic growth. Alternatively, if the conflict in the Middle East continues and higher energy prices start leading to ongoing generalized inflation, monetary policy will have more work to do—there may be a need for consecutive increases in the policy rate."

In his remarks today, he said:

"As inflation comes down, there is risk that it gets stuck above the 2% target. If cost increases and their pass-through are larger than expected or the economy recovers faster than expected, inflationary pressures will increase. On the other hand, there’s a risk that the second-quarter pickup in growth is not sustained. The recovery in exports could stall, which would likely weigh on business investment and hiring. A weaker economy would put more downward pressure on inflation. "

The first one mentioned cuts and hikes and the second one deleted such explicit references. The intimation is the same in my opinion. With higher for longer inflation you hike, lower for longer you cut. Neither is their base case. If it’s somewhere in the muddling middle then perhaps you just sit on your hands which is their base case. For now.

Which should not surprise anyone. This is not a central bank that does not reach ahead to signal intentions at inflection points. It acts slowly, and when it decides to change, it goes fairly rapidly when all the boxes are ticked. They don’t wish to rock the boat on guidance before that point arrives.

As a side bar comment, a sign of the media’s dovish bias shone through when the first headline to hit on Bloomberg was about omitting the hike reference followed by a long lag before noting they also omitted the cut reference, and then during the press conference when a major national newspaper only asked about omitting the hike reference without noting the omitted cut reference. There is a strong asymmetric dovish bias in the financial press toward the BoC which we also saw in the WSJ article the other day that wrongly stated no one is forecasting hikes this year and did not mention market pricing for hikes while playing up only those economists who still think cuts are possible. There is high uncertainty about what will ultimately happen and when but I’ve long believed the media is routinely too dovish just as they were in the pandemic.

PRESS CONFERENCE TRANSCRIPT

What follows is merely an attempt at capturing the essence of the Q&A during the press conference after Macklem finished reading his opening remarks. Any errors or omissions are likely just to be blamed on my ability to keep up during the presser.

Q1. You say you have growing confidence the economy is working through headwinds. Why?

A1. Macklem referencing improving indicators, improved Q2 growth tracking at about 2 1/2%. Housing market stabilizing. Greater export momentum. US economy is strong and creating strong demand for exports. Businesses are finding new markets in Europe for example. So we're seeing a certain adaptation and with more strength in exports we think there will be a pick-up in investment. The thing we're going to be assessing going forward is how sustainable it will be. We think it will be but there are some risks.

Q2. You removed reference to consecutive hikes. Why? If oil prices once again rise will you expect to see consecutive rate hikes?

A2. The short answer is yes. Today oil prices are lower than their peak but they are now halfway back to where they were and the situation in the Middle East remains very volatile and is a long way from being resolved. If oil prices remain high and move higher then there may be a need for consecutive hikes. Our base case is not that, our base case is oil prices will continue to ease. There are other risks like the sustainability of growth.

Q3. How has the balance of risks shifted since April? Where is the bar for a cut and a hike?

A3. Monetary policy has been facing this dilemma. Inflation has been high and growth has been weak with excess supply. You can't at the same time raise rates to address inflation and lower them to raise growth. There's a dilemma. If this forecast plays out then that dilemma will resolve itself as growth picks up and inflation comes down.

Q4. You noted the role of CAD weakness in driving exports and raising the cost of imports. How much could the C$ play a role in your rate policy decisions.

A4. It's not been a major factor. The C$ has depreciated about a couple of cents since the last decision. We don't target the C$. Flexible exchange rates are an essential part of our framework. Wider Canada-US yields have weighed on CAD.

Q5. Are the major project announcements changing your medium-term outlook and outlook for business confidence?

A5. [Rogers answering]. They are in the development stage.

Q6. You mention the risk of inflation broadening if the conflict goes on. Hasn't enough time passed by now to have more serious concerns about a flare up in inflation?

A6. There are risks. Oil went sharply up, then down, now they've back up quite a bit but are still lower than in April. The longer they stay high the bigger the risk they start to spill over into other goods and services. That would be a warning sign to us. So far it's very concentrated in gas prices. That's not our base case that we'll get pass through but it is a serious risk.

Q7. Comments on the government's plan to buy condos?

A7. [Rogers again]. Describing some general influences on the condo market. Doesn't have a big effect on our monetary policy decisions. A correction in one segment of the housing market is not a direct threat to financial stability.

Q8. Are you being overly optimistic with your caveats on the state of the economy? Your business survey indicated deteriorated business sentiment over the past three quarters. Do you really think the economy is going to improve this year and over the next few years?

A8. Well, we're calling it as we see it, so yes, our baseline forecast is that the economy is going to improve. There are risks around that. Repeating some earlier comments on their growth tracking. We want to see excess supply absorbed. That is going to be important to getting inflation on target.

Q9. How high do oil prices need to get for the impact on inflation to be broad based?

A9. I'm afraid you're going to be surprised. What's key is the persistence. If they are high and remain high then that increases the persistence of inflation, the spread of price increases. We've been very clear we're not going to allow higher oil prices become more generalized inflation.

Q10. Do you sense that monetary policy has lost traction in housing? Could that hold you back in tightening rates going forward given that rate cuts had little effect?

A10. [Rogers again]. Stressing affordability challenges. Uncertainties etc holding back housing.

Q11. Why does your consensus building approach work better for Canada without vote disclosures etc?

A11. As part of the monetary policy review framework we're not reconsidering the consensus based approach.

IS THE BOC TALKING THROUGH INFLATION RISK AGAIN?

It is encouraging to see somewhat less acute concern about trade risks to Canada as Governor Macklem emphasized that businesses are adapting. Yet I feel that the Bank of Canada may be doing the same thing with less extreme consequences that it did in the pandemic by talking through inflation risk. They have some time on their side but forward-thinking markets need to be increasingly thinking about how much time.

First, I’m struggling with the BoC’s current take on the impact of commodity price pressures on the Canadian economy and inflation risk. Macklem says high oil prices are bad for Canadian growth and so as they fall from the peak (even with the recent upturn) they’re raising the growth outlook while dampening inflation concerns. Back in early 2015, his predecessor—Governor Poloz—cut twice after oil prices plunged over 2014H2 during which he said nothing about it, only to say in January 2015 this was bad for incomes, bad for activity levels and growth and a downside risk to inflation. It can’t be both. The same central bank cannot say that high and low oil prices are both bad for growth in a country that produces an awful lot of the gooey stuff!

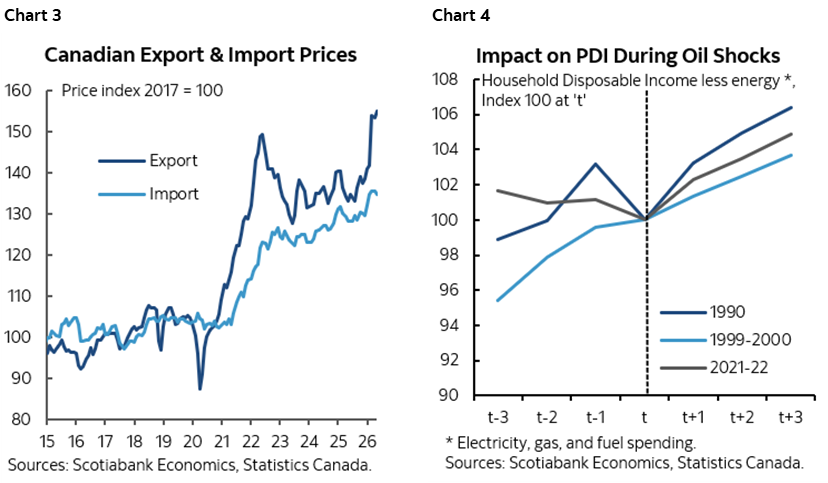

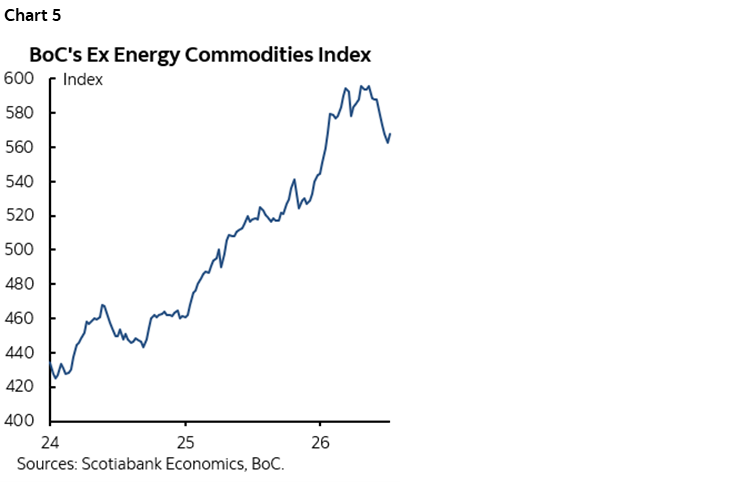

As chart 3 shows, the terms of trade are soaring. Export prices are rising much faster than import prices which is a wedge that represents income being taken out of the global economy and imported into Canada. That carries trickle down benefits across sectors including better fiscal balances—as we’ve seen—and that are getting spent—as we’ve seen. Household incomes tend to be resilient if not stronger in aggregate when oil prices jump (chart 4). Corporate profits benefit in aggregate.

And Macklem continues to avoid mentioning that it’s not just oil prices that have risen. All commodity prices have been on an upswing even if off their precise peak (chart 5). The BoC’s own commodity price index tells them that.

But today’s BoC with Macklem at the helm says this is all bad for a commodity producing country. That’s a tough pill to swallow.

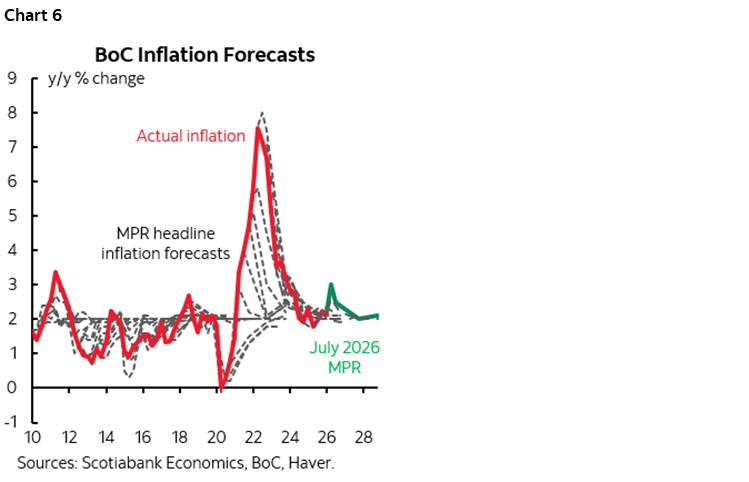

Further, I wouldn’t take their forecast for inflation to be 2% forever very seriously. They always say that. Admitting otherwise would be signalling they’re ok with failing at their mandate. It’s a politicized forecast. And they’re not good at forecasting inflation’s inflection points (chart 6). They routinely miss turning points, routinely fade upside pressure and prematurely call peaks and have a bias toward showing inflation as always expected to be lower than reality. This is why the BoC tends to strongly lag developments in terms of inflation risk.

Among those developments are things you didn’t hear any reference toward in the presser. Governor Macklem only referenced spare capacity in output gaps as a disinflationary force and how they wish to see spare capacity closed before they get excited about inflation risk. Yet output gaps are one part of an inflation forecast and only one, are constructed from guesswork around potential growth on the supply side of the economy and subject to whether or not they get the actual GDP growth picture correct. For instance, AI may drive potential growth much higher in markets where it is vastly more prevalent, like the US and China, but not so much in countries that are well behind, like Canada.

As for all the other drivers of inflation risk there are a few added points.

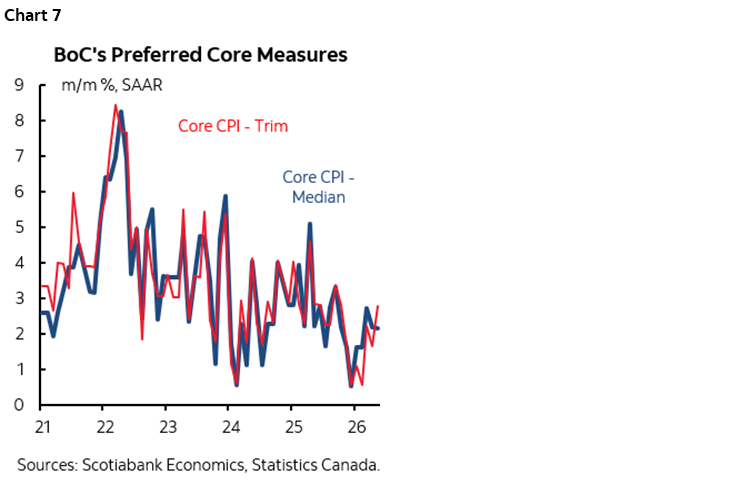

One is you didn’t hear any reference from them about slowly emerging from the core inflation soft patch despite the evidence (chart 7). They were quick to reference the soft patch, but ignore the rebound.

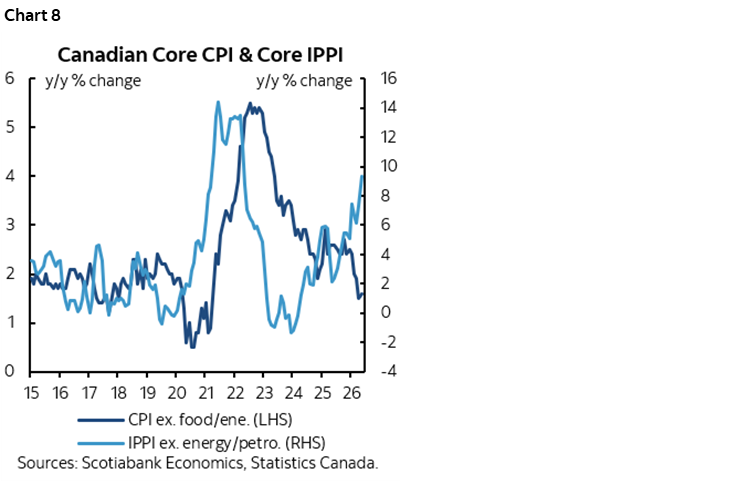

Industrial prices continue to point toward lagging pass through effects into core consumer price inflation (chart 8). Some of that is a reflection of a weaker currency, rising import prices for reasons beyond the currency effect (tariffs, supply chains etc), domestic demand in categories like imported equipment, and external factors like surging global AI investment and effects on electronic component prices.

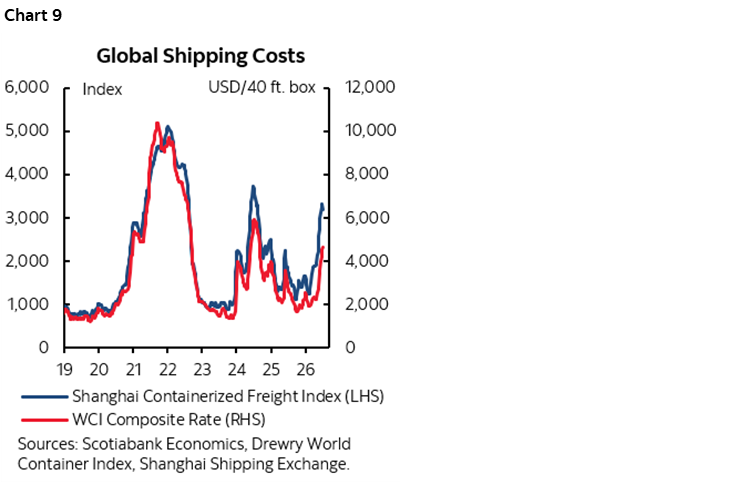

Shipping costs are also soaring, yet ignored (chart 9).

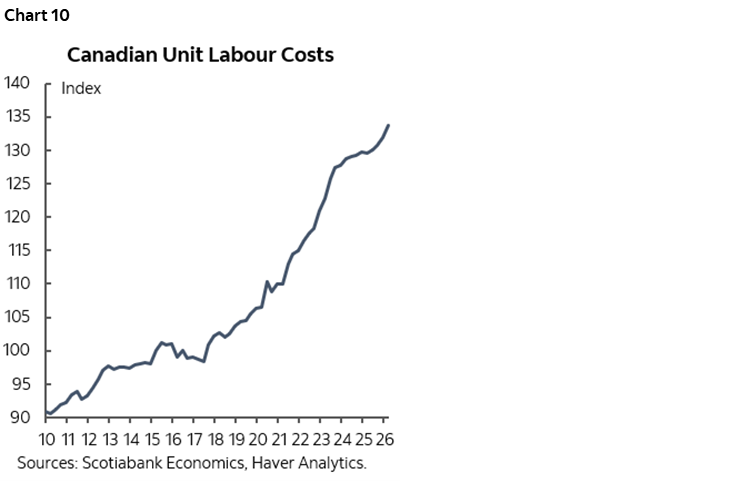

Then we have productivity adjusted employment costs that are soaring (chart 10) as costs are outstripping moribund productivity growth, also unmentioned.

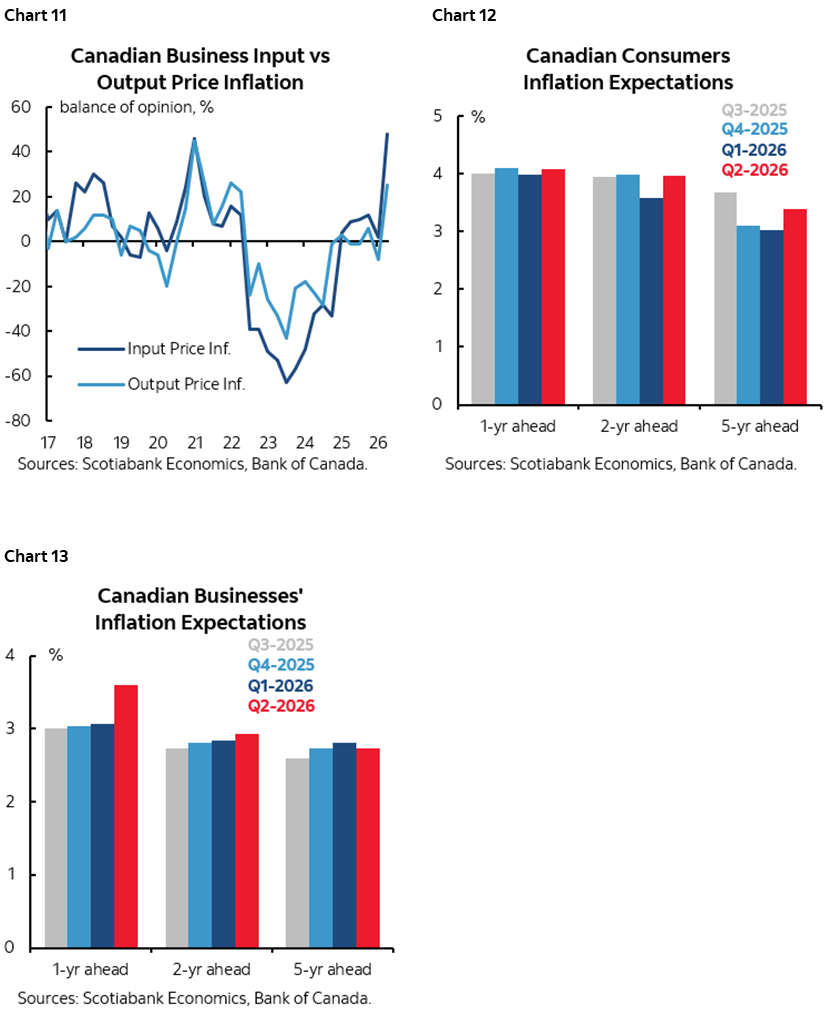

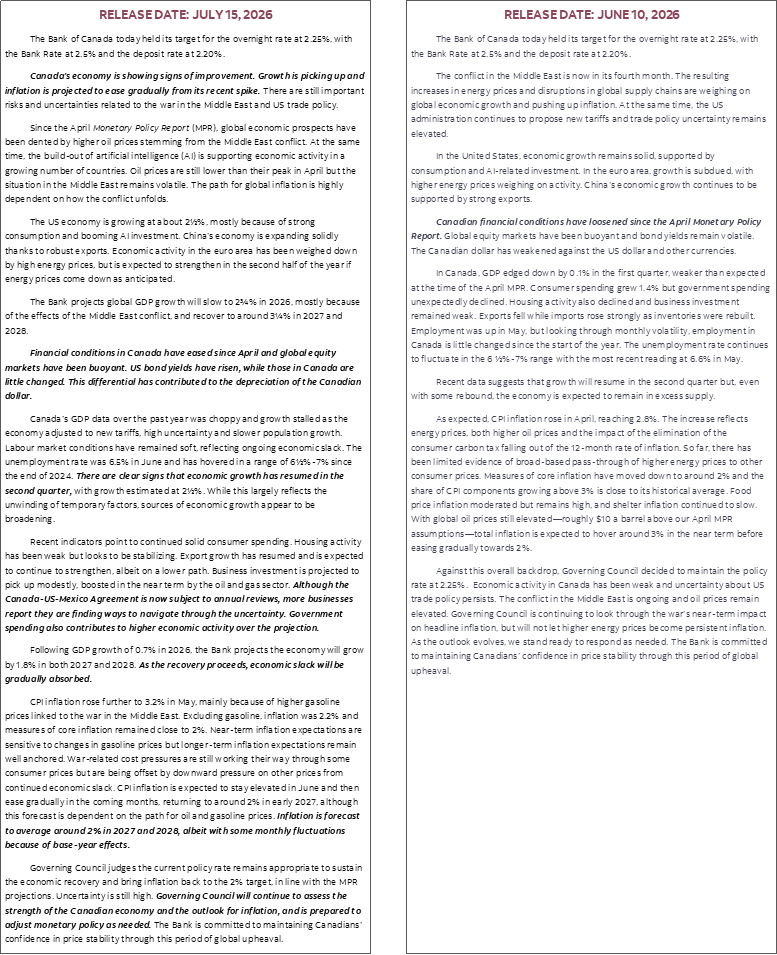

The BoC’s own surveys point to inflation expectations being unmoored at or above the BoC’s upper bound of its 1–3% inflation target range (charts 11–13).

And largely gone from emphasis is Macklem’s prior speech references to cost pressures like searching for new markets, reconfiguring product lines and production, investing in new configurations, spending more management time seeking new markets and developing new products in a changing world etc.

In any event, hanging out at the lower end of the neutral rate range with a negative real policy rate and easing bank capital regs plus fiscal stimulus being applied in serial fashion with more to come as trade policy risks prove manageable should perhaps be prompting a more cautious Governor in my opinion rather than one saying everything will be tickety boo at 2 1/4% forever.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.