- Canada posted another job gain with mixed details

- Canada is cruising at full employment in a low hire, low fire environment

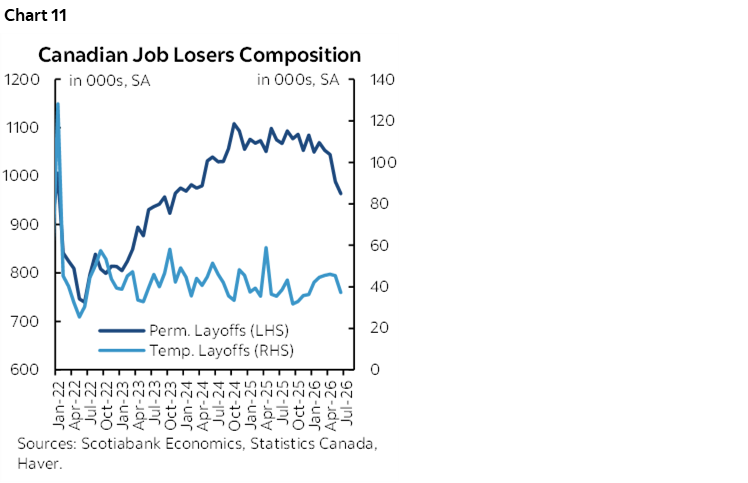

- Permanent layoffs continue to fall

- No clear evidence of World Cup or hockey playoff effects

- Wage growth accelerated

- Hours worked support June GDP, Q2 rebound

- BoC may be a little more encouraged by the recent employment trend next week

- Canadian jobs, m/m 000s // UR %, June:

- Actual: 18.2 / 6.5

- Scotia: 10 / 6.6

- Consensus: 10 / 6.6

- Prior: 87.8 / 6.6

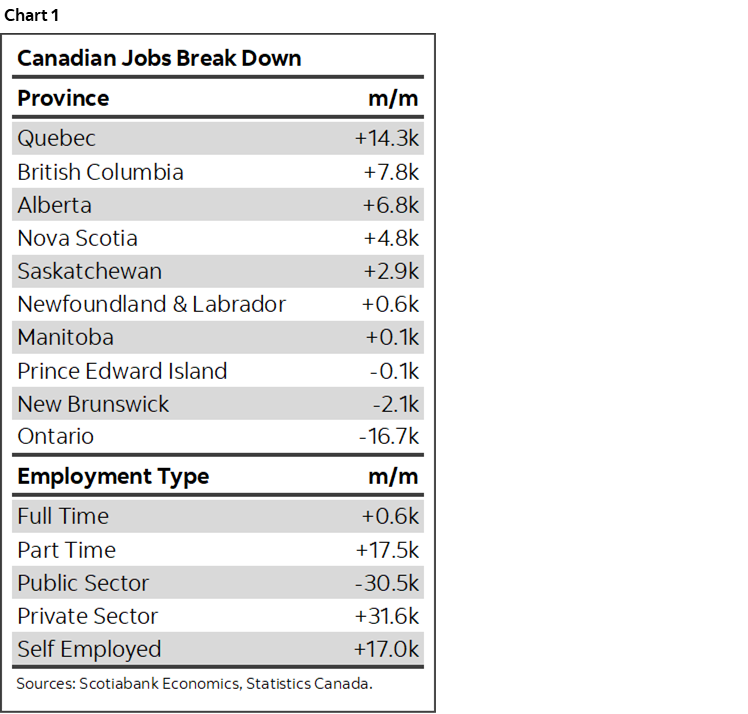

Canadian job growth was sustained in June and roughly in line with expectations. Details were not great but could have always been much worse after a massive prior gain, and no, June’s jobs were not driven by the World Cup. Markets took the broad strokes of the report as supportive of a resilience narrative as the 2-year GoC yield increased slightly but also came under the influence of Trump declaring a formal end to the ceasefire with Iran. Some highlights of the report are shown in chart 1.

The overall punchline? Canada's job market is keeping it together in 2026. Jobs are neither ripping nor tumbling while the UR falls. Canada's unemployment rate is close to the OECD's measure of the natural rate of unemployment. In other words, we basically have full employment in Canada within the context of a low-hire and low-fire labour market where basically anyone who wants a job has one but growth has been curtailed partly as a reflection of tightening supply through immigration policies. In fact, the evidence on layoffs is increasingly encouraging which would go against any narrative that employers are packing up shop.

In any event, Canada is up 88k on total employment over the past three months with much of that driven by May's report. Not too shabby I'd say. The BoC will look to that trend in next week’s communications and conclude that the job market is doing ok.

The rest of this note will summarize instant coverage shared in client and staff chatrooms.

MIXED DETAILS

Full-time jobs were flat in June (+0.6k) with part-time up 17.5k.

Payrolls were flat (+1.1k) with self-employed up 17k, which is another soft detail.

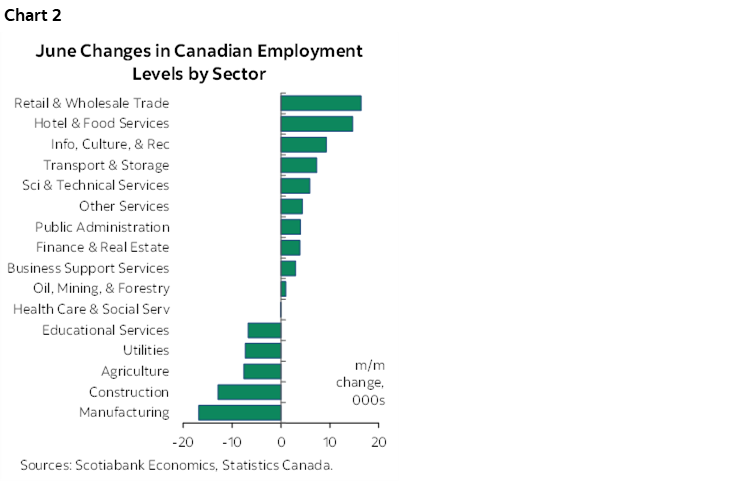

Chart 2 breaks down job growth by sector. Goods sectors shed 44k jobs, while services added 62k. Within services, accommodation and food services were up 15k, wholesale/retail jobs were up 16k, and info/culture/rec was up 9k as the main drivers.

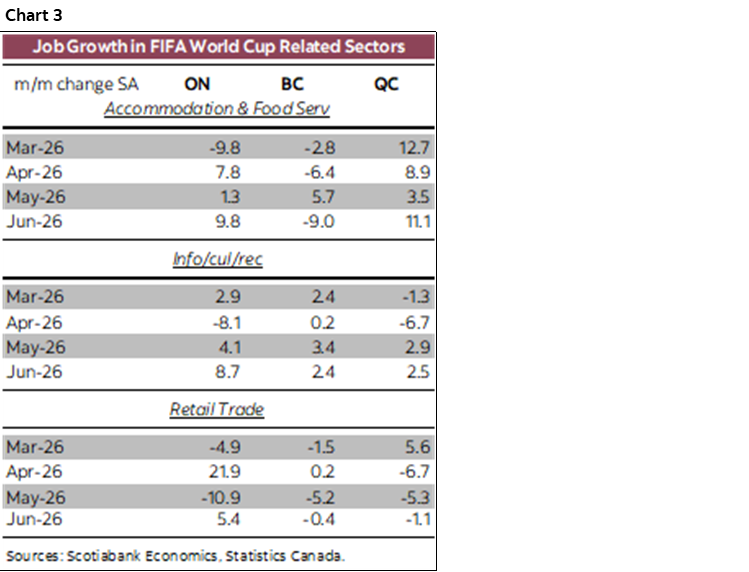

Conjecture is driving sloppy headlines on World Cup effects. I don’t see any clear influences of sporting events on the national data, whether World Cup hiring or the few hockey teams in the playoffs, namely Montreal, but also Edmonton and Ottawa. Chart 3 shows what happened to jobs in Ontario and BC that hosted World Cup games starting with one in Toronto during the LFS reference week. The chart focuses on the sectors that would be most likely to see effects of sporting events. On balance, it’s impossible to disentangle various influences, but I’m not seeing any clear evidence of sporting event effects. Vancouver was a host city, yet jobs in related sectors were soft in BC versus Ontario where Toronto was a host city and that province saw gains.

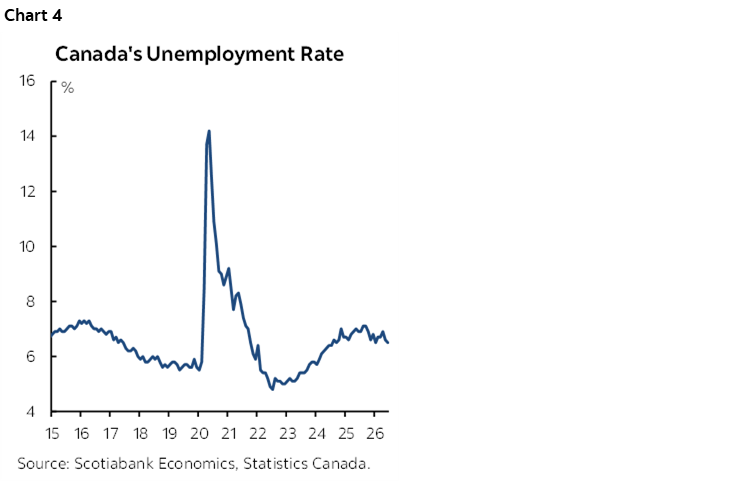

The unemployment rate moved down a tick to 6.5% (chart 4) as job growth (18.2k) exceeded the small rise in the labour force (5k). The UR is performing in line with expectations for it to decline this year at 6.5%, down from 6.8% in December as a reflection of the waning population growth argument. Statcan's LFS lags population changes because it applies a 12-month smoothed moving average to the temps category which is the one being curtailed (temp foreign workers, int'l students and asylum seekers). We may finally be seeing it catch up. The labour force was basically flat in the past two months (+3.8k in May, up 5k in June) while population only increased by 27k m/m in June.

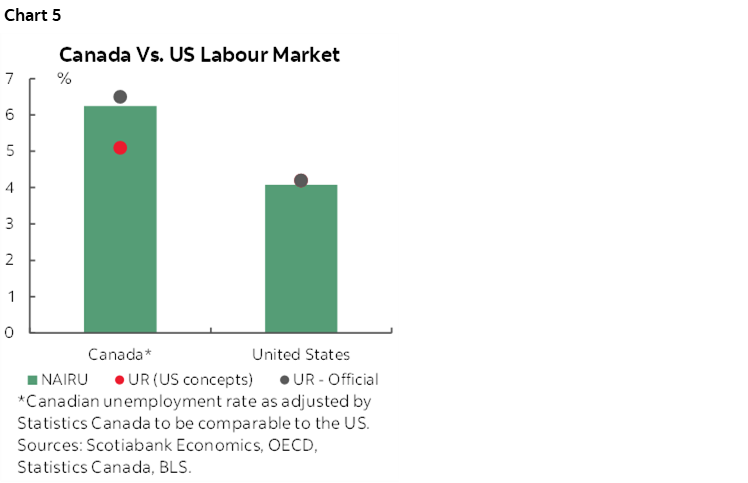

Chart 5 shows that Canada’s UR is very close to the OECD’s estimate of full employment as measured by the Non-accelerating Rate of Unemployment (NAIRU) which is the marker for full employment. It’s an uncertain measurement that indicates perhaps a small degree of labour market slack, but not much.

Measured using US concepts, Canada's unemployment rate would be 5.1% instead of the official 6.5% with both numbers direct from Statcan. There are a lot of differences in methodologies. The US requires stricter evidence that one is searching for a job in order to count in the labour force. The US starts its definition of the labour force a year older than Canada (16 instead of 15). etc

Canada’s R8 unemployment rate which includes discouraged workers is at 8.5% and shown in the same chart. Again, using US measurement concepts it would likely be materially lower but Statcan doesn’t offer that. The US U6 measure of unemployment that is roughly comparable stands at 7.9%, so Canada’s may be lower.

Coming back to payrolls, public payrolls fell by 31k, while private payrolls were up 32k which is a favourable quality sign.

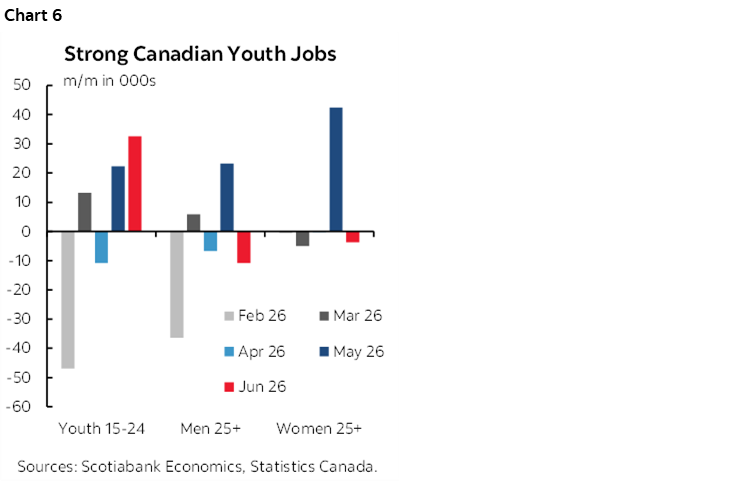

Summer jobs drove part of it, and were up by 32.5k for youths aged 15–24 but led by 25k more part-time jobs. The 25–54 cohort also gained 33k jobs, while the over 55 age bracket lost 47k. Chart 6.

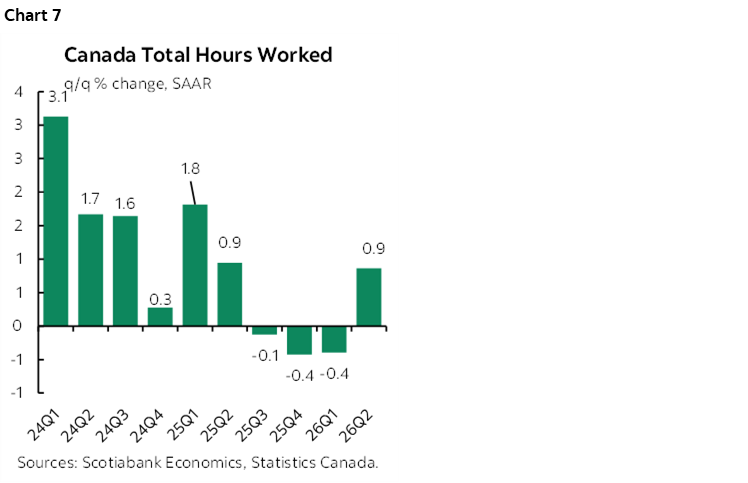

Hours worked increased by +0.2% m/m SA which is a plus for June GDP. Q2 hours worked were up by 0.9% q/q SAAR in support of the GDP rebound since GDP is hours times labour productivity (chart 7).

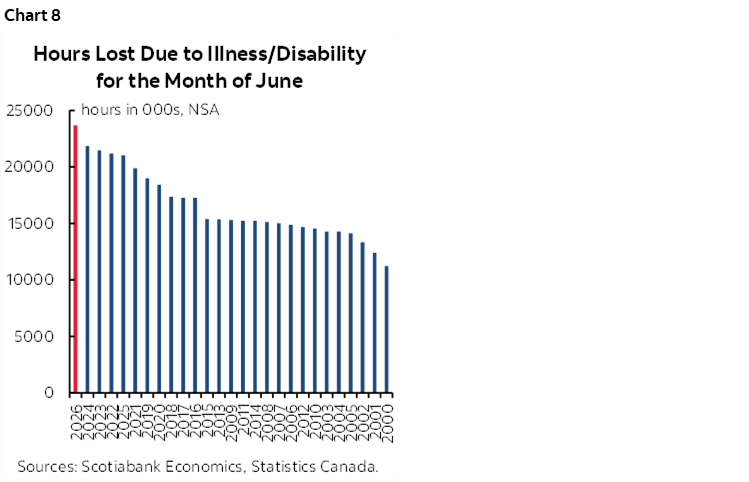

One thing I don’t get is what’s happening to lost hours due to illness (chart 8). June?? We’re well past flu and cold season. This is conjecture, but I’m starting to wonder if, say, whacked civil servants are maxing out sick days.

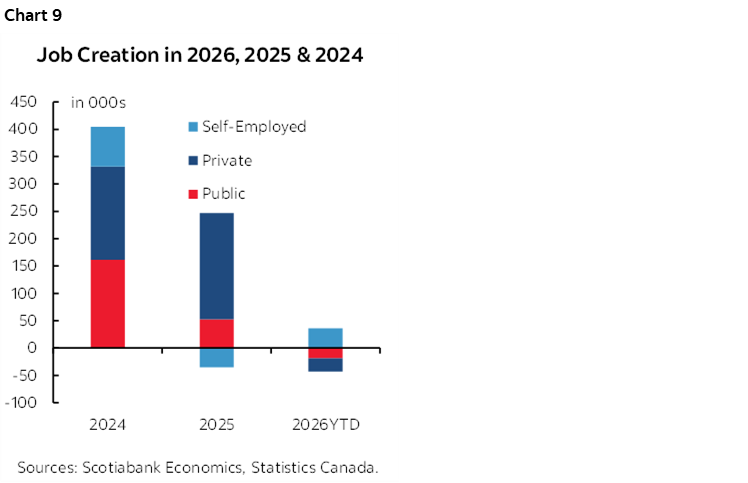

Chart 9 shows year-to-date hiring compared to the prior two years. Canada front-loaded cycle hiring before tighter immigration rules and uncertainty took over. On a ytd basis, total jobs are flat (-6k). Public payrolls are down -19k with private payrolls down 24k, while self-employed positions are up 36k. Full-time jobs are up by 43k with part-time jobs down 50k.

Wage growth was strong as wages of permanent employees (the BoC’s fave) were up by 0.7% m/m SA, or 9% m/m SAAR!

It's a totally different wage setting context than in the US. 10% of Americans unionized, triple that in Canada as the in-between market relative to the US and Canada. Which is why collective bargaining matters more in Canada in driving greater wage growth persistence. Contracts are still setting wage gains per year in the 3-4% y/y range over the typical 3–4 year contract periods. ie: more second-round concerns in Canada than the US where wages are more likely to be set in real-time. Furthermore, in the US they actually have the p-word in their favour— ppppppproductivity which is nearly a swear word in Canada. So, dear inflationistas, poor productivity trends and persistent wage pressures are not great qualities from a BoC standpoint.

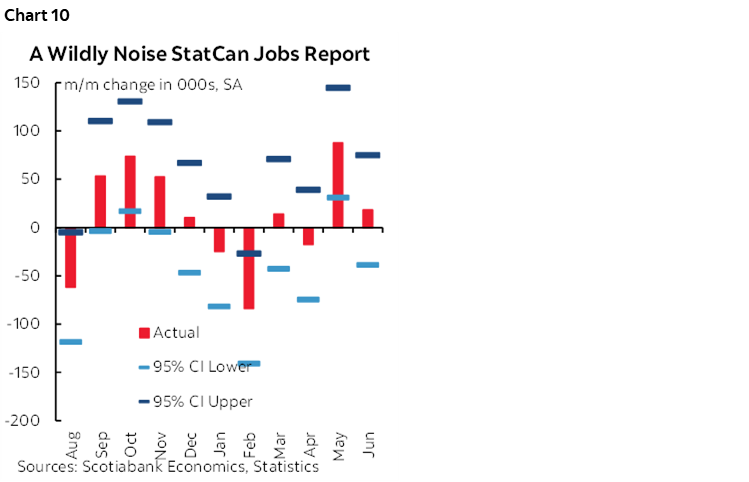

Chart 10 adds in the confidence bands around the estimates of job changes. May was unambiguously strong. Shoulder months more uncertain but statistically speaking we can't lean toward higher or lower than reported from a noise standpoint.

Permanent layoffs continue to fall which is an encouraging sign while temp layoffs remain trendless (chart 11).

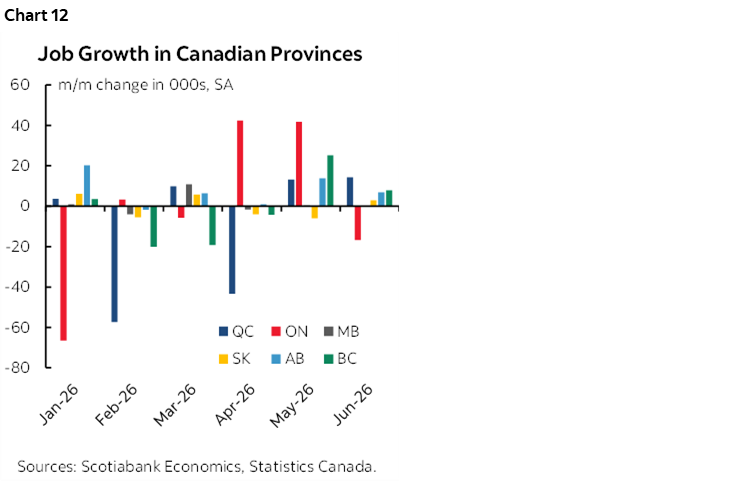

On a provincial basis, job growth in June was concentrated upon Quebec, Alberta and BC (chart 12). Quebec’s country-leading gain was led by professional, scientific and technical services plus accommodation and food services.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.