The only assumption that one should be comfortable making about what the Bank of Canada may or may not do tomorrow or subsequently is that a new Governor is approaching the task at hand with a fresh perspective and with a reputation for creative problem solving such as during his past stints during the global financial crisis. This makes me uneasy that the central bank will just deliver more of the same with a tweak here or there.

That the Governor is delivering the Governing Council’s decisions against the very recent backdrop of strong domestic data matters little to what follows. He can sound encouraged and cautiously optimistic, but not Pollyannaish as there remains ample reason to transition the BoC’s response to date toward applying new insurance against still high risks. There is also a need to take steps to consolidate and strengthen the overall policy framework to make it durable through future tests.

One should therefore not be so sure that Governor Tiff Macklem will pass on embracing different tools, altered means of implementing existing ones and fresh forms of guidance. This is a Governor with an established reputation for creative problem-solving who honed such experiences during the GFC and who was not directly involved in the delivery of the since somewhat discredited 2015 stimulus playbook.

MARKET REPAIR VERSUS OTHER POLICY MOTIVES

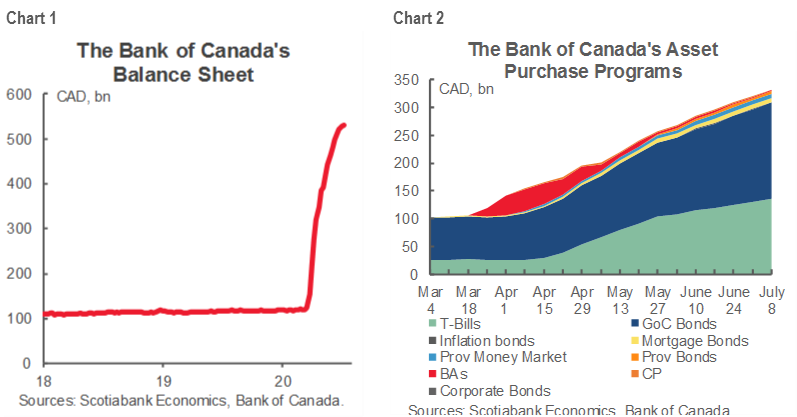

A key issue is the BoC’s degree of satisfaction that its actions combined with the impact of global stimulus and private money have repaired market conditions for spread products. Charts 1 and 2 show the slowing rate of increase in the BoC’s balance sheet and the dominance of Government of Canada bonds and bills among its multiple purchase programs.

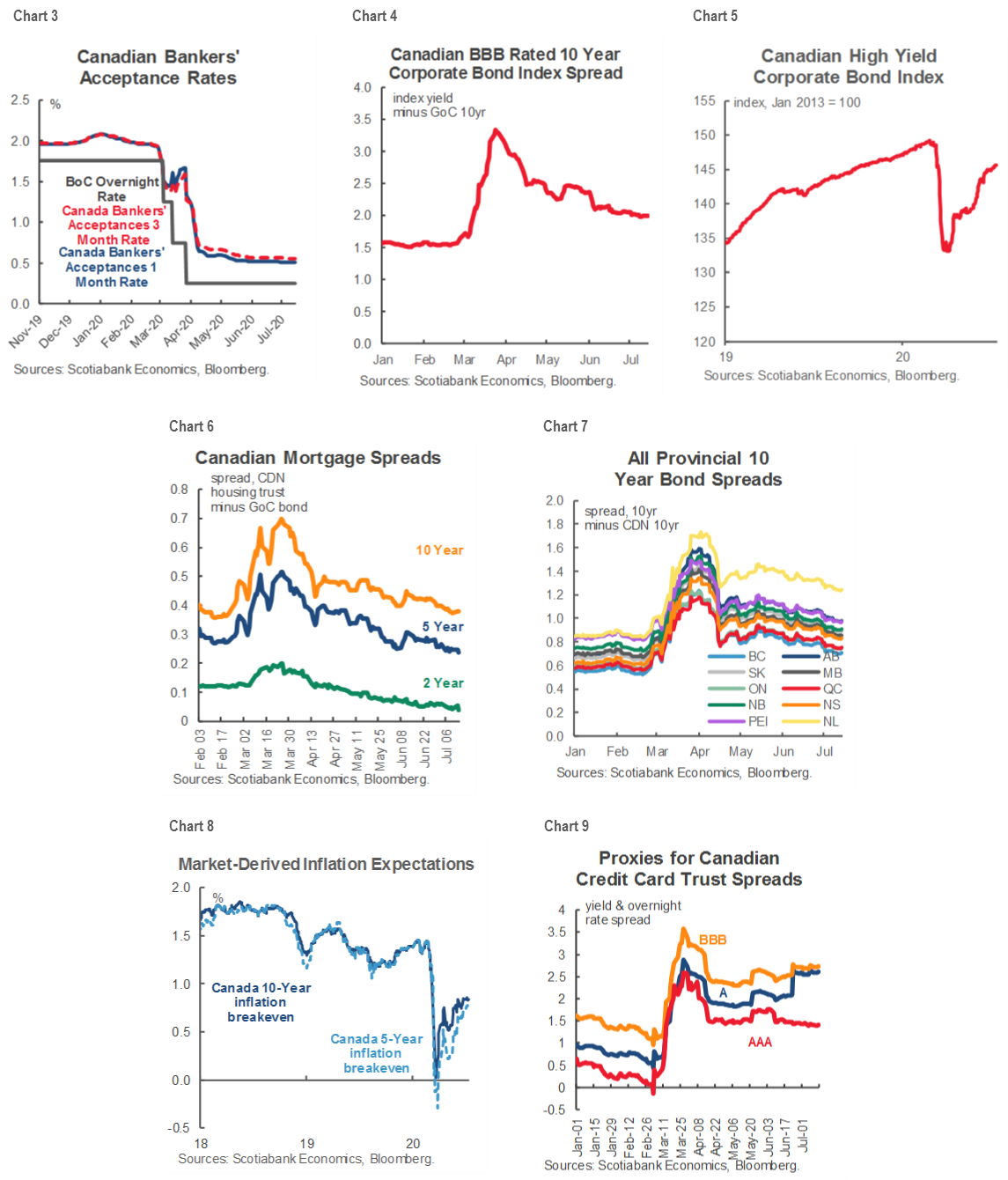

That markets have been repaired is generally true, but in uneven fashion across asset classes as demonstrated in charts 3–9 on subsequent pages using proxies for market functioning. The degree to which the BoC signals comfort could inform expectations about the future path of such purchases across asset classes—and how it might change up policy tools.

The slow pace at which the BoC has been implementing credit purchase programs relative to buying federal government bonds and bills may invite further emphasis upon how the BoC is transitioning toward balance sheet expansion for the purpose of providing offsetting liquidity to soaring government issuance as opposed to driving further improvement in private markets. Another motive remains pre-emptively oriented toward reducing rate risk for dollops of government debt issuance that have only begun to be taken down by markets. Further, the government has rolled out many programs to assist the private sector; the BoC has the government’s back. These additional policy motives beyond market repair are why we expected the BoC to embrace quantitative easing in the first place.

For example, corporate bond spreads remain wider than they were prior to the covid-19 shock. High yield has almost recovered and short-term corporate paper markets have been restored to proper functioning. The BoC doesn’t buy ‘junk’ bonds and has essentially wound up its BA and CP purchase facilities after successfully bringing short-term rates in line with its policy benchmarks, but why proceed at such a slow pace in buying investment grade corporate bonds in the secondary market since starting with the first purchases in early June? Almost all of the C$10 billion facility remains unused with ten months to go. The BoC may reason that there is a sound rationale for wider spreads than pre-covid due to various forms of uncertainty.

Provincial bond spreads are also wider than they were before covid-19, yet the BoC’s facility is only running at about 10% of capacity and with 10 months to go on that program as well. Provincial money market paper net purchases have ground to a halt.

Mortgage bond spreads, however, are arguably tighter than they were before the covid-19 shock. The rate of expansion of the mortgage book has been at a rate well below the potential pace.

Other measures of financial strains remain significant outside of the BoC’s purchase programs. For example, credit card trust spreads remain considerably wider than pre-covid.

The BoC may indicate that it has achieved sufficient progress toward repairing conditions in some markets but is prepared to respond accordingly within its programs should conditions deteriorate. This would strike a balance between not prematurely declaring victory and focusing efforts elsewhere, but there is the risk of an uneven application of this argument across components of its balance sheet programs.

THE BENEFITS AND REQUIREMENTS OF NARROWING THE FOCUS

Narrowing the focus to buying federal government bonds and bills enables embracing new forms of guidance, but meaningful stimulus through this narrowed channel may require extra help to avert potential dysfunction. Indeed, signalling comfort toward the state of credit markets could require the central bank to offer strengthened measures applied to base yields in order to control all-in yields.

For example, at present, the BoC says that it will buy government of Canada bonds in the secondary market at a minimum rate of C$5 billion per week starting back on April 1st and lasting “until the economic recovery is well underway.” It has been exceeding the minimum C$5 billion per week since the program’s inception. The recent increase in bond buybacks (here) was a response to increased GoC bond issuance and the greater focus upon longer term issuance that was met with longer-term buying, but the guidance only goes to the end of July. Markets could use strengthened guidance beyond this time frame.

Thus, one issue may be that the BoC ups the floor on this purchase target range or jawbones how it is more likely to purchase materially above the minimum for an extended period.

It could instead—or also—increase the share of GoC bonds that the BoC buys at auction as part of its normal course of operations from the existing 13%. There is no real compelling reason for holding off on this potential choice for later. The BoC can justify greater buying at auction as compatible with its inflation mandate as a pre-emptive move against future pressures on borrowing conditions that could tighten financial conditions prematurely. There is also nothing in the Bank of Canada Act that prohibits such a move which would be at the full discretion of the governor.

Another potentially compatible option would be to strengthen what is meant by the recovery being ‘well underway’ as a means of informing the longevity of the program. Is that one or a couple of quarters of decent GDP growth? Probably not, but that could cut the purchase program out at year-end. Adding a quarter or two on top of that would match the guidance for other purchase programs to last through to next May. An aggressive step would be to say purchases will continue until the economy is close to closing off spare capacity which could add tens of billions to expected purchases beyond May 2021.

EXIT PRINCIPLES

It may be helpful to markets to hear the BoC spell out general principles for exiting its unconventional monetary policy programs. This would inform market expectations for pricing the entire term structure of rates. It is arguably a necessary step before strengthening forward rate guidance at some point if not tomorrow.

Will they taper bond purchases before stopping? Will they communicate as much or simply let their actions in the market do the talking as they’ve tended to do with the slow pace of take-up on their private bond purchase programs? Will the BoC then enter a prolonged period of reinvestment that flat-lines the balance sheet, or is it open to allowing sudden roll off of maturing assets when conditions merit? This would be a key matter that could keep the BoC buying in the market beyond the course of normal operations gross of retirements for potentially many years to come. Will they commence hikes before or after material balance sheet unwinding? If they follow the Fed’s playbook, then the first hikes will arrive before meaningful balance sheet shrinkage. Are there differences in how a modest central bank in an open economy hitched to the US economy and capital markets can conduct such orders of operations?

I see no good reason why the BoC wouldn’t be having this dialogue with markets now. Yes there is massive uncertainty, but shrugging one’s shoulders and saying it would be too early to go down this path would be a cop out; one can still operate in an uncertain world by informing term structure expectations. We don’t need artificial time lines so much as order of operations and general intent. The Fed deserved high marks for having this dialogue with markets starting years before exiting – and even then made its own mistakes, like the famous taper tantrum—and the BoC should learn from that. Markets don’t like surprises and so reassuring words that the BoC will have an open dialogue with the markets in advance of such steps would be helpful.

FORWARD GUIDANCE

Exit principles are arguably a necessary first step to delivering credible forward policy rate guidance. As a crude example to illustrate this point, injecting liquidity through purchase programs cannot easily coincide with withdrawing liquidity to steer short-term rates toward policy benchmarks. This would confuse markets about overall policy intent and distort their functioning.

Thus, this is new ground for Governor Macklem. When he came into the Senior Deputy Governor role in 2010 it was toward the end of the BoC’s conditional commitment to keep its policy rate on hold until the end of the second quarter of 2010 conditional upon not breaching its inflation target. In the end, they hiked just weeks before because the condition was being violated.

That was an innovative form of hybrid calendar- and condition-based guidance. Central banks across the world have experimented and will continue to experiment with varying forms of such hybrid or just time or just condition based guidance.

This time is more complicated for the BoC. Delivering any said form of guidance absent balance sheet exit principles could backfire on itself by confusing markets and/or forcing them into drawing their own conclusions on the timing and potential order of exit operations. As another crude example, you can’t repeat the 2009–10 version of the conditional commitment through to next summer without spooking markets that bond purchase programs are likely to shut down potentially earlier than guided.

YIELD CAPS

Enter the way in which all of this could be reconciled to potentially significant overall benefit. The BoC could simply embrace a yield curve target level out to, say, 3 or 5 years on the curve or a Bank of Japan style range of, say, +/- X basis points but across a shorter-term maturity especially out to the key 5 year bucket that matters to the mortgage market. There could be multiple benefits to doing so.

- It would enable the BoC to apply the credible threat of purchases across shorter term maturities without having to take down as large a share of the overall secondary market and a large stock of debt issued at auction even with an unchanged share.

- A yield cap could reduce risk of courting dysfunction across shorter term bond markets.

- It would enable the BoC to focus actual purchases on longer term bonds in concert with lengthened issuance horizons.

- A shorter term yield cap could lessen any potential frictions associated with backing away from credit purchase programs.

- Such a move could mitigate concern some may have that the BoC is directly funding government through aggressive bond purchases and risking its independence.

- Substituting threats for actual purchases could keep powder dry if this shock persists for a lengthy period.

- It would also deliver a form of policy rate guidance.

- A yield cap or range would have the added benefit of setting a stake in the ground as markets price in recovery to enable control over shorter term yields. Further, it may carry the benefit of not having to embrace a negative policy rate as a means by which the term structure of rates can be controlled.

FORECASTS

Operating in the background to all of this will be the BoC’s updated macroeconomic forecasts. Meh, it’s going to be awfully hard amidst present uncertainties for the BoC to convey much meaningful conviction to markets. They’re almost too late to matter much. That said, we could possibly see more innovative forecast tools now or in future such as enhanced ways of conveying uncertainty, like cone charts or multiple scenarios.

The last time the BoC delivered a full suite of forecasts was in January, before simply shifting to the thin gruel offered in domestic GDP base case and worse case scenarios sans details. One important ingredient to its views, however, may be how far the BoC goes in revising potential GDP growth lower which would inform an important component to when it expects overall spare capacity to shut, inflation to return to target, and potential monetary tightening to occur.

With the extension of the forecast horizon to 2022, it’s unlikely that the BoC would view it as prudent to deliver forecasts that may get markets thinking about hikes within that time frame when exceptionally little such risk is priced. Macklem’s rich experience would be tested in the hotseat if the overall suite of measures is not delivered with consistency and care.

The statement and Monetary Policy Report including forecasts will be released at 10amET. Governor Macklem and Senior Deputy Governor Wilkins will host a joint press conference at 11amET.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.